North European Euro Nations Preparing to Slaughter the PIGS

Currencies / Euro-Zone Jun 02, 2010 - 04:10 PM GMTBy: Jim_Willie_CB

Natural forces are at work in Europe, powerful forces, in fact forces that are not evident. It is amazing how little the financial analysts notice the forces at all. Since the year 2007, a hidden force began to put pressure on the European Union financial underpinning. Like any fiat currency, the foundation resorts to debt. It came to my attention almost three full years ago that Spanish EuroBonds had a yield slightly higher than the benchmark German.

Natural forces are at work in Europe, powerful forces, in fact forces that are not evident. It is amazing how little the financial analysts notice the forces at all. Since the year 2007, a hidden force began to put pressure on the European Union financial underpinning. Like any fiat currency, the foundation resorts to debt. It came to my attention almost three full years ago that Spanish EuroBonds had a yield slightly higher than the benchmark German.

Commentary swirled that the EuroBonds were not homogeneous, and therefore the Euro currency was badly flawed. They were identifiable by the markings on the bond IDs. German EuroBonds carry an 'X' in the ID. So the arbitrage professionals went to work, buying the German and selling the Spanish bonds. The flaw was to the structural foundation to the Euro currency, not the market that traded them, surely not the alert speculators. In time, the Greek, Italian, and Portuguese bonds, even the Irish bonds, showed significant separation from the German benchmark. Last December, the Greek bond broke first. Its arrival to the crisis was not part of evolution (natural selection) as much as European tribal leader selection. Greeks are neither Latins nor Teutonics. The bust of the EuroBond structure invites the arrival of a gold-backed currency, urgently needed to provide stability.

Commentary swirled that the EuroBonds were not homogeneous, and therefore the Euro currency was badly flawed. They were identifiable by the markings on the bond IDs. German EuroBonds carry an 'X' in the ID. So the arbitrage professionals went to work, buying the German and selling the Spanish bonds. The flaw was to the structural foundation to the Euro currency, not the market that traded them, surely not the alert speculators. In time, the Greek, Italian, and Portuguese bonds, even the Irish bonds, showed significant separation from the German benchmark. Last December, the Greek bond broke first. Its arrival to the crisis was not part of evolution (natural selection) as much as European tribal leader selection. Greeks are neither Latins nor Teutonics. The bust of the EuroBond structure invites the arrival of a gold-backed currency, urgently needed to provide stability.

A second natural force has arrived in the gigantic bond marketplace. While as many political analysts as financial analysts promote the wisdom of a preserved European Union, and a shared Euro currency across that union, a natural force works to separate the entire group of PIGS nations. Refer to Portugal, Italy, Greece, and Spain. As much force comes from the Nordic Core power center to push the PIGS nations away from the common European financial structure, as does the force from the PIGS nations to sever ties and go it alone. A German banker contact has repeated an important point on numerous occasions. The European Monetary Union experiment has cost the nation of Germany over $300 billion per year, all for what clearly appears to be a welfare program directed toward the benefit of wasteful inefficient nations not deserving of a low bond yield. After ten years, the cost has been $3 trillion to Germany. It is not a matter of German willingness to continue the Southern Europe Welfare Program, as much as their ability to continue. They cannot continue. They cannot afford it.

My forecast made since January was that Germany would not aid Greece, but would say all the right things. Their leaders did occasionally show human tendencies, like when some critics claimed Greece possessed innate specialty in dance, drink, and song. My longer standing forecast is that all PIGS nations would revert to their former currencies, the Greeks to the Drachma, the Italians to the Lira, the Spanish to the Peseta, and the Portuguese to the Escudo. The forecast is of decentralization and increased local autonomy. However, and very importantly, the path is a very slow one with political obstacles, face saving requirements, economic pressures, and social pressures too. Notice the Germans appeared to be cooperative in aiding Greece, but when money had to be committed, arguments ensued surprisingly. Not a surprise to the Jackass. The German High Court will surely reject both the Greek aid and the Euro usage itself, all in time.

ADVANTAGES OF REVERTED CURRENCY

The political ideals of a unified Europe are all well and good, but might be fantasy built upon folly in ignorance of practicality. The national differences are significant in work habits, industrial efficiency, tax structure, credit practices, federal bureaucracy load, economic diversity, educational depth, native intelligence, demographic makeup, arable land & sunny climate, and more. The pursuit of a unified Europe has proved elusive for a millennium. Not gonna go there here. The pope in the Dark Ages had the most success, except that its church accumulated an outsized collection of wealth, even in the form of gold, enough to be a clandestine global player.

Enter the London financial analysts and economics brain trust. They have entered the room with some interesting counsel, not the typical self-serving defense of their system. Instead, a prominent think tank suggests to Athens leaders a debt default and return to the Drachma currency. Greece is urged to leave the Euro currency. We are moving gradually toward a restructure of Greek Govt debt, and a corresponding stimulus to the Greek Economy via devalued currency. When tied to the Euro currency yoke, such a Greek stimulus is impossible. British economists advise Athens to abandon the Euro and default on its €300 billion debt under the basic motive to save its economy. The Centre for Economics & Business Research (CEBR) out of London has warned Greek Govt officials of the horrible bind. The CEBR believes Greece will be unable to escape a debt trap without devaluing their own currency to boost exports. Greece must pursue economic expansion, but cannot with the Euro straitjacket. The only workable path is for Greece to return to its own currency, the Drachma. To date, the EU Bailout is a poorly disguised rescue for German and French banks, even London banks. The dirty secret across Europe is that the major nations all own a huge raft of PIGS debt, and each nation within the PIGS pen all own a huge raft of the same debt. Any departure by Greece from the Euro would create a grand shock for banks across all of Europe, cause great disruption, and subvert the banker plan for their latest welfare program in continuation of public governmental adoption. It all ends in ruin.

Doug McWilliams is chief executive of the CEBR. He said "Leaving the Euro would mean the new currency will fall by a minimum of 15%. But as the national debt is valued in Euros, this would raise the debt from its current level of 120% of GDP to 140% overnight. So part of the package of leaving the Euro must be to convert the debt into the new domestic currency unilaterally... The only question is the timing. The other issue is the extent of contagion. Spain would probably be forced to follow suit, and probably Portugal and Italy, though the Italian debt position is less serious." McWilliams called the move virtually inevitable (in his words) but he minimizes the devaluation potential. See the Business Times article (CLICK HERE).

The advantages are as numerous as they are deep, all significant.

Defaulted Restructured Debt: A return to the Drachma currency would enable a restructure of the Greek Govt debt. Look for at least a 50% debt reduction, but against a currency devaluation. The Athens leaders can win a very large portion of debt forgiveness, or else threaten default. European banks will choose a writedown rather than a total wipeout loss. These bankers will realize the futility of carrying full debt on their books, all too aware of the poison pill nature of the compulsory austerity programs heaped upon Greece.

Economic Stimulus: A return to the Drachma currency would enable a strong stimulus to the Greek Economy. Nothing is free, however. Currency devaluation is a double-edged sword. The benefit to be realized with cheaper exports (including tourism) will be offset by higher energy costs and other import costs (like cars, cellphones, and machine equipment). The historical effective tool is for a currency devaluation, one that leads to valid stimulus but with a steady dose of price inflation. Greece, like other European nations, is no stranger to socialist solutions to spread the misery.

Poison Pill Revenge: A return to the Drachma currency would enable a national rejection of the IMF/EU poison pill solution. The austerity measures have no precedent of effectiveness. They are ruinous, lead to greater federal deficits, worse unemployment, and more social disorder, yet the Banker Elite continue to push such non-solutions. Rejection of the austerity programs would incite a national rally of pride and celebration. Obviously, when Greek reverses the austerity cuts, the maneuver would ensure a second thump one year afterwards. Bloated government payrolls would remain, at a heavy cost. The Drachma would suffer a continued devaluation later on. Stimulus would be required in additional doses. The shared pain from price inflation would follow.

Autonomy & Control: A return to the Drachma currency would enable a national movement for the Greek people to take control of their fate. Their population feels on the receiving end of dictums and forced solutions, complete with massive job layoffs and budget cuts. They detect duplicity, since other nations in Europe are in violation of guidelines. Nevermind that something like 11% or 12% of all Greek jobs are located within the government sector. Turn a deaf ear to the rampant tax evasion and other corruption that might be more prevalent than Italy. The psychological benefit to a reversion to the Drachma is to spit in the faces of bankers and to take the reins of national control. This has a value in national pride and spirit, which ironically would avoid most internal reform.

PRECURSOR TO NEW NORTHERN EURO

Prepare next for a Euro currency with a more trim look, one with the PIGS fat trimmed off. The next three big big shoes are about to hit the floor, with severe crises erupting much worse for Spain, Portugal, and Italy. Banks in those nations will suffer failures, liquidations, stock declines, CDSwap contract rises, rescue requests, mergers in desperation, and more. These three nations represent the remainder of the famed PIGS descriptor, as Greece has captured far too much news and attention. When the Greek Govt debt news broke out and was developed from February through May, was Spain deeply committed to reform? NO! Was Spain deeply involved in liquidations and bank asset writedowns? NO! They delayed. Attention turns to the other PIGS in distress. Greece has served to distract attention not just from the other PIGS nations but from the United States and United Kingdom as well. Sovereign debt default will not end as a story until the USTreasurys and UKGilts default, even if technical defaults. All four PIGS nations will be removed from formal Euro currency participation. Economics and nationalism dictate it.

Prepare next for a Euro currency with a more trim look, one with the PIGS fat trimmed off. As the PIGS sovereign debt is discharged, written down, and defaulted, the demand will increase for the survivor Euro core, the healthy strong core. The new Northern Euro currency will initially be comprised of a PIGS-less Euro, which awaits on the other side of the door, here and now. The PIGS-less Euro currency will have much less debt to refinance in the short horizon. The PIGS-less Euro currency will have much stronger fundamentals with smaller annual deficits and better looking debt ratios versus economic size. The PIGS-less Euro currency will have a much healthier trade surplus picture. The PIGS-less Euro currency will realize much greater respect in a faith-based fiat world. But it is a transition vehicle.

The events in the next few months regarding the European Monetary Union are set to accelerate rapidly. The Greek Govt debt situation was replete with delay, debate, deliberation, confusion, distortion, false starts, deceptive fixes, reversals on decision, difficulty in endorsement, revealed lies on debt volume, harsh criticisms, low blows, violence, and much more. The new few months will be different. One well connected banker source told me a few months ago that the Greek debt situation will come to a resolution, all rescues will fail, as default is inevitable, complete with a return to the Drachma currency, but afterwards, the default of Italy and Spain will occur with lightning speed. He expected the events to occur in a fast chain reaction. We are seeing it.

The transition currency stripped of PIGS fat-ridden lining will eventually make way for the new Northern Euro. It was described in last week's article. It will contain much more independence among its members and their central banks. It will contain an embedded gold component. Watch in the future for a crude oil component, even possibly OPEC oil sales tied to new Northern Euro currency payments. Time will tell. Events are moving rapidly. The PIGS-less Euro currency forces the monetary issue, as it demands a better and more perfect form of currency. An old maxim goes "A paper currency cannot be replaced by another paper currency, but rather by a metal currency." How true!! Regard the PIGS-less Euro currency as a vehicle whose arrival will serve as a penultimate event in the Competing Currency Wars. The arbitrage will continue to pull apart paper currencies, tethered to lost integrity and faded trust. The PIGS-less Euro currency will require the broader adoption of a strong viable realistic currency born of crisis, a currency formed in a golden crucible.

The reversion to local currencies, complete with more autonomy taken back by individual central banks, will demonstrate a strong DECENTRALIZATION TREND. Even the new Northern Euro currency will feature greater decentralization. Those who feared a continental Amero currency for North American usage, a sustained Euro currency for European usage, and an emerging Yuan currency for Asian usage, must go back to the drawing board or replace the perceptual prisms. Prepare for several gold-backed new currencies. China is talking of a gold component to the Yuan currency. So is Russia. My hunch is that Russia will either participate in the new gold-backed Northern Euro currency or launch its own gold-backed Ruble currency.

The Americans and British will be last on board, as their nations tumble into the Third World where corrupt leadership and tight corporate mergers are their calling cards. Gold will be the stability mainstay, the common anchor applied across the world, but its application will enable decentralized power to be managed. Gold will emerge as the great liberator. Those nations first to embark on true remedy and reform will be the new global leaders. Those nations stuck in stubborn refusal will elect themselves Lord of the Flies in the Third World, where apparently oil-soaked shorelines and dead marine ecosystems will be the norm, maybe even toxic rain.

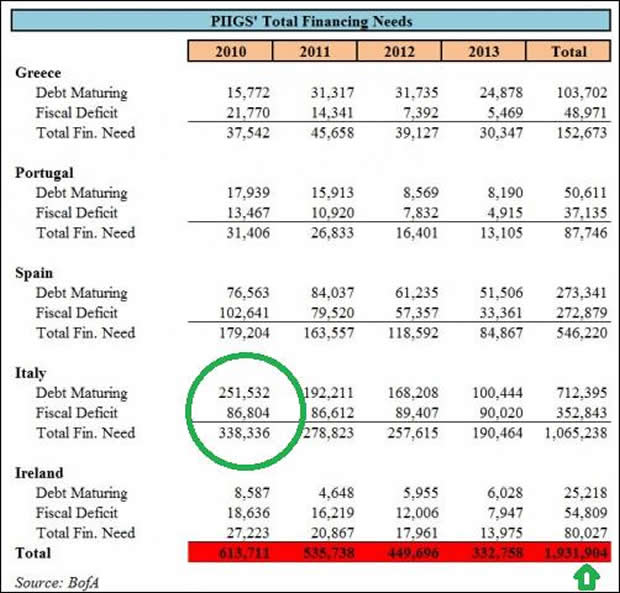

ITALY NEXT ON THE BLOCK

The Italian Govt debt picture is seriously distorted. Financial analysts point to more favorable debt ratios as a proportion to their larger economy. The debt volume in Italy to be refinanced this year alone is almost ten times that of Greece. The important factor is the volume of short-term debt to be financed, that must come from the bond market. So what if its ratios look more favorable? The money aint there!! Over half of all the 2010 total finance needs for PIGS nations plus Ireland are derived from Italy alone. The needs for Italy diminish somewhat in following years, but the volume remains grand. Unlike other European nations, the Italian vendors and shopkeepers have maintained a stubborn habit of showing sales receipts in both Euro terms and Lira terms over the years. Never argue with an Italian, since their hands move faster than others.

The Italian Govt debt is under sharp attack. During this week, the sovereign risk returned with a vengeance as the Italian Govt debt took heavy blows. The reminder is stark, that sovereign debt is a major contagion across all of Europe. The Credit Default Swap contract, which insures the 5-year bond, rose in a big way on Monday. MarkIt reports the Italian CDSwap went from 200 basis points to 250 bpts in a single day, to mark a new record high level. The new story to replace Greece has arrived to take away attention in the financial news media. The contagion is spreading globally now, even to South Korea, far beyond Iceland from two years ago. An important new trend evident in the last few months is the appearance of sovereign nation debt as the most actively moving in the official CMA reports. The trend of national debt struggles and deep distress will continue until a true monetary anchor can be constructed, fashioned of a gold alloy, urgently needed to provide stability.

SPAIN NEXT ON THE CROWDED BLOCK

The Spanish Govt debt picture is seriously distorted, in different ways. The banks in Spain have chosen to ignore the reality of lower property prices, and have carried credit assets at absurdly high values. It is safe to say that the Spanish banks are ready to enter freefall. A major shock comes to Spain. For well past a year, they have refused to mark down much of any credit assets tied to property. Furthermore, their property markets have refused to mark down prices seeking buyers on the open market. The result has been a mammoth reduction in sales volume, as sellers want prices that buyers are unwilling to offer, with huge price gaps that are sometimes described as comical. Reality is set to strike, and strike very hard. The Greek focus will soon turn to Spain, and also Italy.

Not being an expert, this analyst regards the Caja sector of the Spanish banks to be the large group of savings banks. They are all operating in a fantasy land, as their credit portfolios have been shattered for a long time. The common practice of carrying lofty valuations is slamming against the wall of reality. The Spanish Govt has been attempting to enforce a grand restructure process among its cajas. They are in deep debt and teetering. Merger with larger banks is seen as a potential solution, but that constitutes fusion of insolvent pieces with bad glue. The Govt has created a Fund for Orderly Bank Restructuring, (FROB) to facilitate the process. Usage of the fund comes with a timetable, as the savings banks have until June 30th to make formal requests for the money urgently needed. The FROB fund has a total value of €99 billion and is funded with €9 billion of capital and up to €90 billion of new government supported debt. Yet more monetary inflation enters the picture.

The savings banks within the Spanish Caja system total 45 in number. They, like the bigger banks, have stalled on taking proper liquidation and writedown action. The Bank of Spain has stirred things up with a recent seizure of troubled Cajasur one week ago. Other merger announcements have followed. Cajasur had a distinction, since its board of directors contained some stubborn priests, who refused to merge with the bigger Unicaja. Bank analysts are coming to the conclusion that the collective costs of the bailouts in Spain by their government will be an order of magnitude higher than what it anticipated. The Spanish Govt deficit ran at 11.2% of GDP in 2009. That ratio must come down. My forecast is that it will rise, not fall. The reason is simple. Just like with the United States and United Kingdom, no reform has come, no bank liquidations have come, no housing market remedy has come, no initiatives to plow under generally have been embraced, and those in charge of the disaster remain at their posts. So the banks will face continued losses. So the housing market will face continued declines. So the economies will face continued recession.

Rumors swirl that Caja Madrid said to ask for €3 billion of aid from the official rescue fund. The news has captured much attention since it is the second largest among the cajas. By the way, caja in the spanish language means box, cage, booth, register, teller unit, or repository. Confirmation came in the form of an official denial by the bank, calling it speculation. The savings bank did reveal last week as being in talks to merge with several regional cajas. Caja de Avila, Caja Insular de Canarias, Caixa Laietana, Caja Segovia, and Caja Rioja were mentioned.

COMPARTMENTALIZED PERCEPTIONS

Think nation, not bank! Until 2008, perceptions and evaluations of the banking sector were specific. Talk was about Santander in Spain, their big bank, and not about Spanish Govt bonds. Talk was about Societe General in France, and not about French Govt bonds. Talk was about Royal Bank of Scotland and Northern Rock and Lloyds in Great Britain, but not about UK Gilt bonds. Talk never was much about individual Italian or Greek or Portuguese banks. But now, talk is replete with Italian and Greek and Spanish Govt debt securities, and not of private banks.

The line of thinking, the analysis, the focus is much more directed at national debt exposure, the sovereign debt. The insolvency of big banks has been transferred to insolvency for entire nations and their governments. After 18-20 months of shifting the debt risk from individual banks to the government balance sheets, the impact has finally come to be felt. The sequence of formal debt downgrades reads like a parade of disasters, mostly concentrated on the distressed nations and their sovereign debt. It has become a global phenomenon, since Korean debt, Brazilian debt, and other nations have joined the sovereign debt crisis. Remember that the clownish popular financial analysts called the Dubai debt default isolated. My analysis actually forecasted the Dubai debt event over three months in advance. My analysis also pointed out the interwoven nature of the sovereign debt exposure, since banks across London, France, Switzerland, and Germany share the debt risk as underwriters and investors. We have vividly seen the interwoven debt exposure.

The Spanish Govt debt situation has provided a gloomy cloud over their entire banking system.

Last week, Fitch Ratings became the second major ratings agency to downgrade Spanish sovereign debt. They marked it down to AA+ from AAA. Standard & Poors had cut the same Spanish debt rating back in April, lower than AAA. In their formal announcement, Fitch stated belief that the unemployment rate in Spain over 20%, along with the reversal of fortune tied to the construction boom, will weigh heavily on their economy struggling under extremely high debt burden levels. Neither the Spanish Govt nor their banking leaders have any firm resolve or grip on the situation. Recall that delay to remedy and reform always results in much worse bank losses and much deeper economic recession. Their government has delayed on bank accounting practices, and only last week worked the austerity measures through the Parliament by a single vote. Fitch offered a mealy mouthed vapid statement about how the special FROB fund to clean up their banks should be sufficient, in a total denial of the depth of the problems and future losses. The FROB fund is designed to aid the caja banks heavily exposed to the real estate and construction sectors. Fitch noted that their restructuring process is progressing slowly, which means not quickly enough. The politicized wrangled process could intensify constraints on the supply of credit and affect the pace of economic recovery for the country, so claims Fitch rightfully so.

The next three big big shoes are about to hit the floor. The bang will reverberate around the world. The Spanish, Portuguese, and Italian banks will next go belly up and quickly, as they sink with PIGS debt and other credit assets tied to fallen property. Spain will make the most shrill sounds, for a simple reason. They were the worst offender in holding onto mindless unreasonable lofty property values. Their bank books have the biggest drop to realize, after re-entry to reality. The crises underway in the remainder of PIGS nations will continue unabated, and usher in magnificent events where a legitimate gold-backed currency arrives, urgently needed to provide stability.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts such as the Lehman Brothers failure, numerous nationalization deals such as for Fannie Mae, grand Mortgage Rescue, and General Motors.

“You freakin rock! I just wanted to say how much I love your newsletter. I have subscribed to Russell, Faber, Minyanville, Richebacher, Mauldin, and a few others, and yours is by far my all time favorite! You should have taken over for the Richebacher Letter as you take his analysis just a bit further and with more of an edge.” - (DavidL in Michigan)

“I used to read your public articles, and listen to you, but never realized until I joined what extra and detailed analysis you give to subscription clients. You always seem to be far ahead of everyone else. It is useful to ‘see’ what is happening, and you do this far better than the economists! I can think of many areas in life now where the best exponent is somebody not trained academically in that area.” - (JamesA in England)

“A few years ago, I was amazed at some of the stuff you were writing. Over time your calls have proved to be correct, on the money and frighteningly true. The information you report is provocative and prime time that we are not getting in the news. I was shocked when I read that the banks were going to fail in one of your prescient newsletters.” - (DorisR in Pennsylvania)

“You seem to have it nailed. I used to think you were paranoid. Now I think you are psychic!” - (ShawnU in Ontario)

“Your unmatched ability to find and unmask a string of significant nuggets, and to wrap them into a meaningful mosaic of the treachery-*****-stupidity which comprise our current financial system, make yours the most informative and valuable of investment letters. You have refined the ‘bits-and-pieces’ approach into an awesome intellectual tool.” - (RobertN in Texas)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.