Are Stocks a Screaming Buy Relative to Bonds, or a False Premise ?

Stock-Markets / Stock Markets 2010 Aug 18, 2010 - 11:07 AM GMTBy: Mike_Shedlock

Josh Lipton writing for Minyanville is asking the question Are Stocks a Screaming Buy Relative to Bonds?

Josh Lipton writing for Minyanville is asking the question Are Stocks a Screaming Buy Relative to Bonds?

Dr. Ed Yardeni of Yardeni Research takes one side of the debate and says "stocks are cheap" according to a model, now dubbed the “Fed’s Stock Valuation Model”.

I am quoted in the article, taking a different view of course, but I want to add to the thoughts I expressed in the article.

First a few snips from Lipton's article ...

Certainly, by employing some basic measures to compare the relative value of stocks and bonds, equities appear attractive. Dr. Ed Yardeni of Yardeni Research made the case this morning that stocks seem cheap and bonds seem expensive according to a simple model that compares the market’s earnings yield to the US Treasury bond yield.

Yardeni first started studying this model after seeing it mentioned in the Federal Reserve Board’s Monetary Policy Report to the Congress dated July 1997. The strategist dubbed it the “Fed’s Stock Valuation Model” (FSVM), and that’s what it's been called ever since.

During the week of August 13, Yardeni says, the forward P/E of the S&P 500 was 11.8. The forward earnings yield, which is just the reciprocal of the P/E, was 8.5%. The 10-year Treasury bond’s yield is 2.60% this morning. So its P/E, which is the reciprocal of the yield, is 38.5.

According to the FSVM, that means stocks are 64.8% undervalued relative to bonds.

James Swanson, chief investment strategist at MFS Investment Management, agrees that stocks now look cheap relative to bonds and that, as an asset class, equities boast more opportunity for investors looking ahead.

In short, the stock market is now priced for an economic future that Swanson thinks remains unlikely. “This only makes sense if the world is going into a deflationary scenario,” the strategist says. “Otherwise, this is a mispricing.”

Yes, stocks might look cheap relative to bonds, but that’s because the economic outlook remains bleak. Mike Shedlock, a well-known registered investment adviser for Sitka Pacific Capital Management, argues that the economy is already mired in deflation, a dangerous downward spiral in prices that will prove lethal for corporate profits.

"Why are Treasury yields low?" Shedlock asks. "It’s because the economy is in recession."

Furthermore, Shedlock argues that investors are ultimately best advised to judge the two asset classes independently. “It is important to evaluate stocks based on normalized earnings estimates and bonds based on default and inflation risks,” he says. “Comparing stocks to bonds is simply an invalid comparison.”

Shedlock points out that equity market valuation measures still look rich. The Shiller P/E ratio, for instance -- which uses a 10-year average of inflation-adjusted earnings -- still points to a market that's about 20% overvalued.Relative Valuation Comparisons are Problematic

The question "Are stocks cheap compared to bonds?" is pretty much like asking "Are rubber bands cheap compared to oranges?"

When both stocks and bonds are unattractive, assuming one has to choose between those classes is tantamount to asking "Would you rather risk losing an arm or a leg?"

The correct answer to that last question is "Why risk either?"

False Premise

Thus, right off the bat, the initial question implies a false premise "Should one be in stocks or Bonds?" Why does it have to be either?

Relative valuation comparisons can get one in all kinds of trouble. Both asset classes may be overvalued or undervalued.

Indeed, If stocks and bonds are richly priced, perhaps one should be in gold, commodities, currencies, cash, or hedged in some fashion. There is absolutely nothing wrong with sitting on the sidelines.

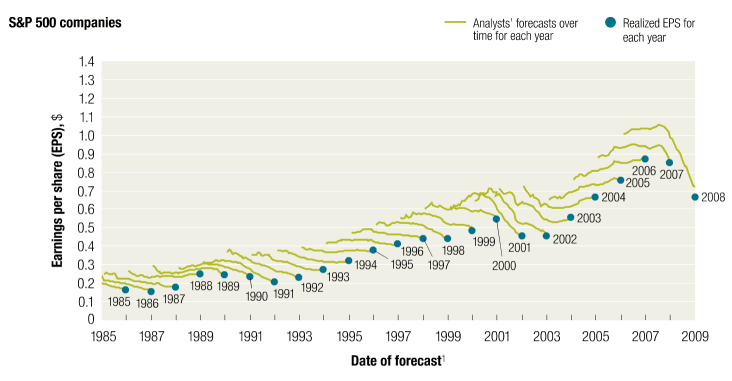

Forward Earnings Estimates Persistently Optimistic For 25 Years

A a McKinsey Quarterly report Equity analysts: Still too bullish

No executive would dispute that analysts’ forecasts serve as an important benchmark of the current and future health of companies. To better understand their accuracy, we undertook research nearly a decade ago that produced sobering results. Analysts, we found, were typically overoptimistic, slow to revise their forecasts to reflect new economic conditions, and prone to making increasingly inaccurate forecasts when economic growth declined.

Moreover, analysts have been persistently overoptimistic for the past 25 years, with estimates ranging from 10 to 12 percent a year,4 compared with actual earnings growth of 6 percent. Over this time frame, actual earnings growth surpassed forecasts in only two instances, both during the earnings recovery following a recession. On average, analysts’ forecasts have been almost 100 percent too high.Market Valuations and Earnings Estimates

John Hussman discussed earnings estimates on July 12, 2010 in Misallocating Resources

On a valuation basis, the S&P 500 remains about 40% above historical norms on the basis of normalized earnings. The disparity between our valuation assessment and the putative undervaluation being touted by Wall Street analysts is so great that a few remarks are in order. First, virtually every assessment that "stocks are cheap" here is based on the ratio of the S&P 500 to year-ahead operating earnings estimates, and often comes with a comparison of the resulting "earnings yield" with the depressed 10-year Treasury yield. What's fascinating about this is that this is the same basis on which analysts deemed stocks to be about 40% undervalued just prior to the 2007 top, following which the market plunged by more than half. There's a great deal of analysis regarding forward operating earnings that I published in 2007, but probably the most comprehensive piece was Long Term Evidence on the Fed Model and Forward Operating P/E Ratios from August 20, 2007.

For still more on earnings estimates please see Five Reasons for Nonsensical Forward Earnings Estimates

A forward P/E estimate of 11.8 for the S&P 500 is quite simply preposterous.

Risk Analysis

A comparison of stock dividend yields (or earnings estimates) to bond yields fails on risk analysis. Sure you can find stocks yielding higher dividends than yields on US treasuries. However, yields in treasuries held to term are 100% guaranteed. Stock performance is not, nor are earnings estimates as noted above.

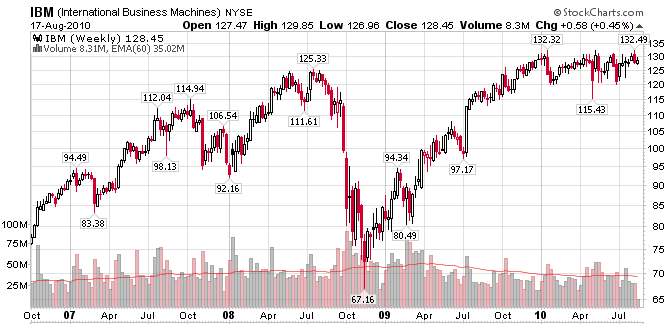

The 2.6% dividend yield on IBM vs. a 1% yield on the IBM 3-year bond or .75% on the 3-year treasury is not enough to cover the risk of an equity price collapse.

A "value" stock like IBM can easily drop 25% or more in the next three years regardless of its reported PE of 12.

Correlation among stocks is a high as it has ever been and it is a huge mistake to think that a low PE will protect value stocks in case of a significant tumble in the stock market.

IBM's low PE did not stop it from plunging in 2008, why would it do so in 2010 or 2011?

Bear in mind I am not making a case for IBM bonds at 1%, I am merely making a case that the Fed model ignores risk. Currently equities in general face significant risks of a double dip recession, an earnings scare, a stock market crash, or any number of painful happenings.

Note that bank stocks crashed in 2008 and early 2009. They were considered "value" stocks every step of the way down because they had low PEs and respectable dividends. What happened? Earnings vanished, dividends were cut, and the stocks collapsed.

Saying stocks are cheap after an 80% straight up run, on the basis of presumed forward earnings estimates without taking into consideration many other risk factors is lame.

Rolling The Dice On Stocks

Just because stocks are overvalued by 40% does not mean they won't go up. Indeed they certainly can. Moreover, (and this is an important point) it will not make any of the bears wrong if they do. Things happen against the odds all the time.

Say you walk into a casino, go up to the craps table, place a bet, are handed the dice and roll a 4. You will lose your bet unless you roll a 4 before you roll a 7.

Can you win? Sure you can, but the odds of it happening are only 33.33%.

Likewise, stocks might go up, but that does not make them a good bet.

Fed’s Stock Valuation Mode Fatally Flawed

- The first mistake is assuming choices are limited between stocks and bonds. The question "Will it be stocks or bonds?" creates an unnecessary false premise. One does not have to be in either.

- The second mistake is believing stocks and bonds can be compared straight up on the basis of earnings plus dividends vs. bond yields. They can't because risk factors are different.

- The third mistake is assuming forward earnings estimates are accurate. Both history and common sense say they aren't.

- The fourth mistake is thinking stock dividends and low PEs will protect against equity losses. History and common sense again suggest they won't.

- The fifth mistake is failing to take into consideration the likelihood of dividend cuts, earnings misses, or even bad market reactions to good earnings.

- The sixth mistake is failing to understand bear market psychology. Sometimes it is better to sit on the sidelines in cash or hedged to avoid risk.

- The seventh mistake is failing to understand reversion to the mean on earnings and stock market valuations. Stocks never did fall to historic bear market valuations at the last market trough. Historically speaking, odds suggest they will.

Quite frankly, that is a lot of mistakes and mistakes are just what one would expect when comparing rubber bands to oranges in an attempt to figure out which one is cheaper. Even IF rubber bands are cheaper than oranges, the correct thing may be to buy neither. The same holds true for stocks and bonds.

I see no reason to be net long stocks here regardless of how cheap they look compared to bonds. Of course the main problem is stocks are not cheap in the first place, only careless analysis makes it seem so.

On False Premises

My friend Rich replies ....

Hello Mish

You said: "The first mistake is assuming choices are limited between stocks and bonds. The question "Will it be stocks or bonds?" creates an unnecessary false premise. One does not have to be in either."

Well, that is not true - at least on Wall Street! The question "will it be stocks or bonds?" is driven by money managers and fund managers and stock brokers, all who are committed to you being fully invested so they can earn their fees.

Indeed. I have commented on this before. Wall Street does not generally get paid on funds sitting in cash. The second money comes in it is "put to work" earning fees, regardless of the risk-reward setup for the client.

Conflicts of Interest in "Stay the Course" Advice

Here is a snip from Long Term Buy And Hold Is Still Bad Advice

Clearly, stay the course is bad advice. So why is it so common? A personal anecdote might help explain things: In January of this year, an investment advisor from Wachovia Securities called me up and stated "Mish, I am sitting on millions because I see nothing I like". I told the person I did not like much either and that Sitka Pacific was heavily in cash and or hedged. His response was "Well, I do not get paid anything if my clients are sitting in cash".

I called up a rep at Merrill Lynch and he said the same thing, that reps for Merrill Lynch do not get paid if their clients are sitting in cash.

Massive Conflict of Interest

Notice the massive conflict of interest possibilities. Reps for various broker dealers have a vested interest in keeping clients 100% invested 100% of the time, even if they know it is wrong. And so it is every recession, bad advice permeates the airwaves and internet "Stay The Course".By the way, that person at Wachovia mentioned above did the right thing. He did not see investment opportunities he liked, so he kept client funds in cash. Such action is certainly is not the norm.

Discrediting the Fed Model

"VegasBob" writes ...

One point Mish alluded to but didn't explicitly state is that John Hussman has thoroughly discredited the 'Fed Model' that is used as a stock valuation metric.

There is no evidence of any cause and effect relationship between stock prices and T-Note rates. Ergo, the 'Fed Model' is just another crock.I posted a link to the Hussman above.

Here it is again: Long Term Evidence on the Fed Model and Forward Operating P/E Ratios.

In recent years, price/earnings ratios based on “forward operating earnings” have been embraced by Wall Street as a replacement for valuations based on trailing net earnings. The beliefs of investors about what represents a “normal” P/E, however, have not changed – despite the change in the earnings measure being used. Meanwhile, the Fed Model – the notion that the earnings yield of the S&P 500 (based on forward operating earnings) should be equal to the 10-year Treasury bond yield, has been embraced as a simple and reliable method of valuing stocks.

It's likely that these beliefs will prove disastrous for investors.

The assumed one-to-one correspondence between forward earnings yields and 10-year Treasury yields is a statistical artifact of the period from 1982 to the late 1990's, during which U.S. stocks moved from profound undervaluation (high earnings yields) to extreme overvaluation (depressed earnings yields). The Fed Model implicitly assumes that stocks experienced only a small change in “fair valuation” during this period (despite the fact that stocks achieved average annual returns of nearly 20% for 18 years), and attributes the change in earnings yields to a similar decline in 10-year Treasury yields over this period.

Unfortunately, there is nothing even close to a one-to-one relationship between earnings yields and interest rates in long-term historical data. ..."Likely Disastrous"

Hussman's August 20, 2007 statement "these beliefs will likely prove disastrous for investors" was right on the mark.

My friend "HB" writes ...

The Fed's 'stock market valuation model was a brainchild of the dot-com mania. It has been the funeral rite for many an unwisely invested dollar.

Another friend writes ...

Yardeni has been saying stocks are cheap relative to bonds for the last 8-9 years, since shortly after the tech bubble burst. By the same token, stocks were cheap in Japan from the mid-1990's onward. Such analysis clearly shows the limitation of valuation studies without an understanding of market cycles. Like the saying goes, "what is cheap can always become cheaper."

Deja Vue All Over Again

As Yogi Berra said "This is like deja vu all over again" with the same tired, disproved, "stocks are cheap" arguments. The worst part is investors are bombarded with such nonsense, fresh on the heels of a 80% runup in stock prices, in other words, at precisely the worst time.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post ListMike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2010 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.