World Economic and Financial System Trending Towards a Serious Breakdown by Spring 2011

Economics / Financial Crash Sep 19, 2010 - 07:18 AM GMTBy: Global_Research

GEAB writes: As anticipated by LEAP/E2020 last February in the GEAB No. 42, the second half of 2010 is really characterized by a sudden worsening of the crisis marked by the end of the illusion of recovery maintained by Western leaders (1) and the thousands of billions swallowed up by the banks and the economic « stimulation » plans of no lasting effect. The coming months will reveal a simple, yet especially painful reality: the Western economy, and in particular that of the United States (2), never really came out of recession (3). The startling statistics recorded since summer 2009 have only been the short-lived consequences of a massive injection of liquidity into a system which had essentially become insolvent just like the US consumer (4).

GEAB writes: As anticipated by LEAP/E2020 last February in the GEAB No. 42, the second half of 2010 is really characterized by a sudden worsening of the crisis marked by the end of the illusion of recovery maintained by Western leaders (1) and the thousands of billions swallowed up by the banks and the economic « stimulation » plans of no lasting effect. The coming months will reveal a simple, yet especially painful reality: the Western economy, and in particular that of the United States (2), never really came out of recession (3). The startling statistics recorded since summer 2009 have only been the short-lived consequences of a massive injection of liquidity into a system which had essentially become insolvent just like the US consumer (4).

At the heart of the global systemic crisis since its inception, the United States is, in the coming months, going to demonstrate that it is, once again, in the process of leading the economy and global finances into the « heart of darkness » (5) because it can’t get out of this « Very Great US Depression (6) ». Thus, coming out of the political upheavals of the US elections next November, with growth once again negative, the world will have to face the « Very Serious Breakdown » of the global economic and financial system founded over 60 years ago on the absolute necessity of the US economy never being in a lasting recession. Now the first half of 2011 will dictate that the US economy take an unprecedented dose of austerity plunging the planet into new financial, monetary, economic and social chaos (7).

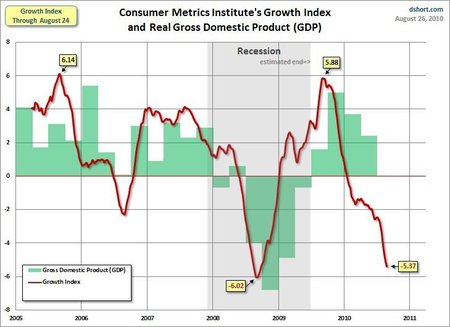

Comparative progress of the CMI (red) and US GDP (green) growth indices (2005 – 2010) - Source: Dshort, 08/26/2010

In this GEAB issue, our team therefore anticipates for the coming months, different aspects of this new development of the crisis, especially the nature of imposed austerity process which will affect the United States, the development of the accursed « inflation / deflation » argument, the actual progress of real US GDP, the strategy of central banks and the direct consequences for Asia and Euroland. As we do every month, we set out our strategic and operational recommendations. And, specially, this GEAB issue offers an excerpt from the new book by Franck Biancheri « The Global Crisis: The Path to the World After - France, Europe and World in the Decade 2010-2020 » : the French version will be published on 7 October next by Editions Anticipolis and the English one later in December.

In this issue we have chosen to present an extract of the anticipation concerning the forthcoming austerity which will be imposed on the United States beginning Spring 2011: « Welcome to the United States of Austerity ».

« United States – the double whammy: no equity, no jobs » - Correlation of falling property prices and unemployment trends state by state (2006-2009) - Source: FMI / OIT / OsloConference, 07/2010

The coming quarters will be particularly dangerous for the world economic and financial system. The Chairman of the Fed Ben Bernanke passed on the message as diplomatically as possible at the recent meeting of world central bankers at Jackson Hole, Wyoming: even though the policy to revive the US economy has failed, either the rest of the world continues to fund US deficits at a loss and hopes that at some point the bet will pay off, avoiding a collapse of the global system, or the United States will monetize its debt and turn all the Dollars and US Treasury Bonds held by the rest of the planet into funny money. Like any power at bay, the United States and is now forced to introduce the threat of pressure to get what it wants. Barely a year ago the rest of the World’s leaders and financial officials had volunteered to « refloat the USA ship ».

However, today things have drastically changed since the noble assurance from Washington (the Fed’s, like that of the Obama administration’s) proved to be only pure arrogance based on the pretense of having understood the nature of the crisis and on the illusion of possessing the means of controlling it. However, US growth evaporates quarter after quarter (8) and turns negative again from the end of 2010. Unemployment hasn’t stopped growing and between the stability shown in official figures and the exit, in six months, of more than two million Americans from the workplace (LEAP/E2020 believes that the real unemployment figure is now at least 20% (9)); the U.S. housing market remains depressed at historically low levels and will resume its fall from the fourth quarter 2010; last but not least, as one can easily imagine in these circumstances, the US consumer is and will be absent on a permanent basis since his insolvency continues and even gets worse (10) for the one American in five without work. Behind these statistical factors hide three realities that will radically change the US and global political, economic and social landscape in future quarters as and when they dawn on the public consciousness.

Broad-based anger will cripple Washington from November 2010

First of all, there is a very depressing widespread reality, a real trip « to the heart of darkness », which is that tens of millions of Americans (nearly sixty million now depend on food stamps) who no longer have a job, no longer have a house, no longer have any savings, are wondering how they will survive in the years to come (11). The young (12), retirees, African-Americans, workers, service employees (13),… they constitute this mass of angry citizens who will speak violently next November and plunge Washington into a tragic political impasse. Supporters of the « Tea Party (14) » and « new secessionist (15) » movements... want to « break the Washington Machine » (and by extension that of Wall Street) without having feasible proposals to solve the country’s myriad problems (16). The November 2010 elections will be the first opportunity for this « suffering America » to express itself on the crisis and its consequences. And, won back by the Republicans or even the extremists, these voters will help to further cripple the Obama administration and Congress (which will probably swing to the Republicans), only pushing the country into a tragic gridlock just when all the signals turn red again. This expression of widespread anger will in addition, from December onwards, collide with the release of the Deficit Commission report set up by President Obama, which will automatically place the issue of deficits at the heart of public debate at the beginning of 2011 (17).

For example, we are already seeing a very specific expression of this widespread anger against Wall Street in that Americans have deserted the stock market (18). Each month, an increasing number of « small investors » leave Wall Street and the financial markets (19), today leaving more than 70% of transactions in the hands of major institutions and other « high frequency traders ». If one keeps in mind the traditional image that the stock exchange is today’s temple of modern capitalism, then we are witnessing a phenomenon of loss of faith comparable to people’s disaffection with official demonstrations experienced by the communist system before its fall.

The Federal Reserve now knows that it is powerless

Finally, there is a financial and monetary effect that is particularly tragic since the players are aware of their unenviable situation: the U.S. Federal Reserve now knows that it is powerless. Despite the extraordinary efforts (zero interest rates, quantitative easing, huge support to the real estate mortgage market, massive support to banks, tripling its balance sheet, ...) that it carried out from September 2008, the U.S. economy will not restart. Fed leaders are finding they are only a part in the system, even if it is a vital part and, therefore, can do nothing against a problem that affects the very nature of the system, in this case, the US financial system, designed as the solvent heart of the global financial system since 1945. But the US consumer has become insolvent (20), the consumer who, during the last thirty years, has gradually become the central economic player of this financial heart (with more than 70% of U.S. growth dependant on household spending). It is this insolvency of US households (21) that has broken the Fed’s efforts.

Accustomed to the virtualism and thus to the possibility of manipulating the processes and dynamics of events, US central bankers believed that they could « mislead » households, once again giving them the illusion of wealth and thus pushing them to revive consumption and behind it the whole United States’ economic and financial machine. Until summer 2010, they did not believe in the systemic nature of the crisis or they did not understand that what was causing the problems was out of reach of the tools of a central bank, as powerful as it may be. Only in recent weeks have they discovered two pieces of evidence: their policies have failed and they have neither arms nor ammunition.

Hence the very depressed tone of the discussions at the central banks meeting in Jackson Hole, whence the lack of consensus on future action, whence the endless debates about the nature of the risks to be faced in the coming months (e.g. inflation or deflation, knowing that the system’s internal tools used to measure the economic consequences of these trends are no longer even relevant, as we analyse in this issue (22)), whence increasingly violent clashes between proponents of renewed growth via debt and followers of deficit reduction... and whence Ben Bernanke’s speech full of veiled threats to his central banker colleagues: in ambiguous terms, he passed the following message: « We will try everything and anything to avoid an economic and financial collapse and you will continue to finance this « everything and anything », otherwise we let inflation loose and thus devalue the Dollar whilst US Treasury Bonds will no longer be worth much » (23). When a central banker expresses himself like a common cash extortionist, there is danger in the house (24).

The response of the world’s major central banks will be unveiled in the next two quarters. Already the ECB has made it clear it thought that a new policy of stimulation through an increase in US deficits would be suicidal for the United States. Already China, whilst saying it would do nothing to rush things, spends its time selling US assets to buy Japanese ones (reflected in the historic level of the Yen / Dollar rate of exchange). As regards Japan, it is now forced to align itself simultaneously with Washington and Beijing ... which will probably cancel out all its financial and monetary policies. In future quarters the Fed, like the federal government, will find that when the United States is no longer synonymous with juicy profits and / or shared power, its ability to convince its partners declines quickly and heavily, especially when the latter question the relevance of the chosen policies (25).

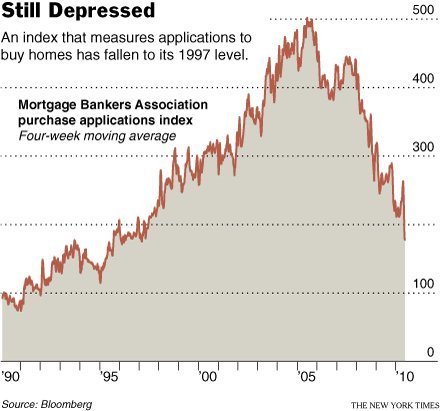

Index of mortgage applications (1990-2010) (4 week moving average) - Sources: Mortgage Bankers Association / Bloomberg / New York Times, 08/2010

The consequence of these three realities that are gradually making their presence felt in US and global consciousness will, therefore, for the LEAP/E2020 team, come to pass in Spring 2011 by the United States entering an era of austerity unprecedented since the country became the heart of the global economic and financial system. Fhederal political blockages in the context of an electorate sick and tired of Washington and Wall Street, heavy reliance on federal funding of the entire US economy and the Fed's impotence against a backdrop of growing international reluctance to finance US deficits will combine to push the country into austerity. An austerity that has, moreover, already begun to affect at least 20% of the population head-on, and wich directly affects at least one in two Americans worried about joining the ranks of the homeless, those without work and other long-term unemployed.

For these tens of millions of Americans austerity is here and it's called lasting impoverishment. What is going to come into play between now and Spring 2011 is, therefore, the shift into official speeches, budgetary policies and international awareness to the idea that the United States is no longer « the land of plenty », but « the land of few ». And beyond the domestic political choices, it is also the discovery of a new limitation for the country: the United States cannot afford a new stimulus (26). Rather than a multidecade collapse like the Japanese situation, many decision makers will be tempted by shock therapy ... this same therapy that, with the IMF, the United States recommended to Latin American, Asian and Eastern European countries.

This is normally a good reason for the rating agencies, always so quick to see the straw in the eye of most countries in the world, to threaten the United States with a strong downside rerating if they not implement a comprehensive austerity plan as quickly as possible. But anyway, for LEAP/E2020, due to the internal and external conditions in the country described above, it is really in spring 2011 that the United States has an appointment with austerity, an appointment that the rest of the world will impose if it is paralyzed politically.

Until then, it is likely that the Fed will try a new series of « unconventional » measures ( a technical term meaning « desperate attempts ») to try and prevent arriving there because, at this stage, one thing is certain concerning the consequences of the United States entering a large-scale programme of austerity: that will be financial and monetary chaos in the markets accustomed for decades to the exact opposite, that’s to say, US waste; and an internal economic and social shock unparalleled since the 1930s (27).

Notes:

(1) In this regard, in the next GEAB issue in October, our team will prepare, as it does each year, its country risk and economic outlook list for 2011. What is already clear to our researchers is that the end of 2010 will be marked by a sharp downward revision of all current forecasts (including already reduced forecasts for the United States). Source: Reuters, 09/09/2010

(2) Sources: Bloomberg, 07/20/2010; Oftwominds, 07/15/2010; New York Times, 08/09/2010; CNBC, 08/12/2010

(3) The chart below illustrates how growth is already collapsing. The CMI growth index has been one of the most reliable leading indicators in forecasting the changes in US GDP. And 92% of Americans believe the country is still in recession. Source: GlobalEconomicAnalysisBlogspot, 09/09/2010

(4) As outlined by our team from the GEAB No. 9 of November 2006 onwards.

(5) To borrow the evocative title of Joseph Conrad excellent novel which especially inspired Francis Ford Coppola for his film Apocalypse Now.

(6) As LEAP/E2020 called the American economic crisis from April 2007 in the GEAB No. 14.

(7) Moreover, without even incorporating this anticipation in their analysis, even the OECD experts warn that global growth will suffer a setback between now and the end of 2010. Source: Marketwatch, 09/09/2010

(8) The Wells Fargo / Gallup index of US SMEs continues to fall month after month. Source: Gallup, 08/02/2010

(9) Even Wall Street continues to plan mass layoffs in the coming months. Source: Bloomberg, 09/07/2010

(10) Even high earners are now affected by the problem of foreclosures. Source: USAToday, 07/29/2010

(11) To clarify this alarming social situation, it is worth reading the joint IMF / ILO report initiated by the Norwegian Government on « The challenges of growth, employment and social cohesion » in the context of the current crisis. Source: OsloConference, 07/22/2010

(12) A very telling indicator showing the price that young Americans are paying because of the crisis.The number of summer jobs, a traditional feature of independence for young Americans for the following year, fell to its lowest level since 1948. Source: USAToday, 09/03/2010

(13) These images of drastic cuts in police numbers in Auckland are emblematic of what is happening countrywide in terms of public services. Source: DailyMotion

(14) On this topic USAToday of 08/16/2010 had a very interesting portrait gallery of the « Tea Party » movement's supporters.

(15) See GEAB issue N°45

(16) The success of the « tea-partisan » gathering in Washington on 08/28/2010, organized by Glenn Beck, is an obvious example. Source: Washington Post, 08/29/2010

(17) Source: New York Times, 08/31/2010

(18) Stock exchanges have stalled or been declining for several quarters despite continuous attempts by the financial authorities to try to restore their shine ... and once again are approaching a violent spasm tied to « the Hindenburg Omen » or the anticipation of global economic and financial conditions. Source: Telegraph, 08/27/2010.

(19) Source: New York Times, 08/22/2010

(20) Even when they manage to find a job, it’s usually a job much less well paid than the previous one. Source: CNBC, 09/01/2010

(21) Thus the foreclosure process is a reflection of an alarming phenomenon of a decline in the value of US households’ assets. Source: Foxnews, 08/23/2010

(22) If the prospect of deflation is that which officially « spoiled the mood » of the central bankers’ meeting in Jackson Hole in late August 2010, it is actually growing doubts about the Fed's ability to select and implement appropriate measures to revive the US economy which makes the whole of the small world of central bankers so nervous. Sources: CNNMoney, 08/31/2010; FT, 09/10/2010

(23) It should be noted here that in front of the growing reluctance of the rest of the world to buy US Treasury Bonds and GSE, the Fed has not only officially begun to buy them for its own account (or more unobtrusively via its « primary dealers ») but it has begun to organize the massive sale of federal debt to US individuals operators. In effect it must seem easier to manage the plundering of many dozens of million people more or less unaware of the economic and financial nuances than that of the major strategic players such as China, Japan, the Gulf oil countries,.... (see chart in GEAB N°47):

(24) After explaining that the use of a moderately inflationary policy had been discussed but wasn’t on the agenda, Ben Bernanke said that however, if deflation risks grew, then the usefulness of some intervention methods could be reconsidered. Clearly, if nothing else works and if the other global players do not want to feed the US deficit machine, then debt monetization will be implemented on a large scale. At least, things are now clear. When LEAP/E2020 warned that it was the only option for the United States in the looming crisis it seemed outrageous. Today, it is the Fed Chairman himself who sets the tone. Source: US Federal Reserve, 08/27/2010

(25) The failure of the mammoth measures to support the housing market is well illustrated by the chart below.

(26) We are even beginning to hear voices suggesting « copy Europe » like Jim Rogers and Doug Noland who publishes the excellent « Credit Bubble Bulletin ». Sources: CNBC, 08/31/2010; Prudent Bear, 07/30/2010

(27) As the historian Niall Ferguson points out in this article published on 07/29/2010 by The Australian, « the sun can suddenly set on a superpower when debt bites ». An historical reminder that columnist Thomas Friedman, though very patriotic, doesn’t refute, who emphasized that the sharp decline of American power was due to the economic crisis in the New York Times on 09/04/2010.

Global Europe Anticipation Bulletin

Global Research Articles by Global Europe Anticipation Bulletin

© Copyright Global Europe Anticipation Bulletin -, Global Research, 2010

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.