U.S. Consumers Refusing to Debt Deleverage Will Be Dragged Kicking and Screaming into the Age of Austerity

Economics / Economic Austerity Sep 30, 2010 - 02:43 PM GMTBy: James_Quinn

10% Savings Rate + Consumer Spending At 65% Of Gdp = Retail Disaster

10% Savings Rate + Consumer Spending At 65% Of Gdp = Retail Disaster

Now that the Wall Street Journal, New York Times, CNBC and every other mainstream media outlet have figured out what some financial blogs had figured out months ago The Great Debt Deleveraging Lie , everyone knows that the American consumers have not yet begun to deleverage. Consumer credit outstanding peaked at $2.58 trillion in July 2008. It has plummeted all the way to $2.42 trillion today, a 6% reduction over two years. The full $160 billion reduction can be attributed to write-offs by the Wall Street, Ivy League MBA run, banks.

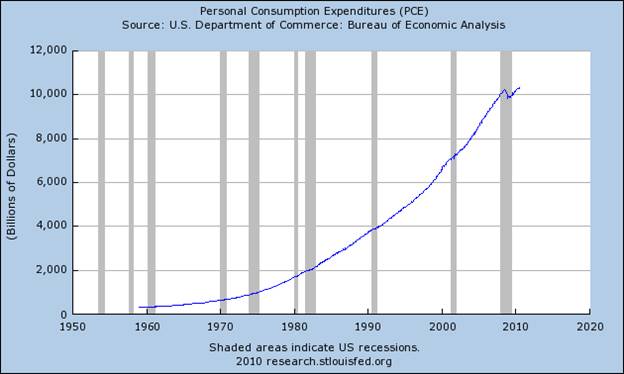

American consumers do not want the Age of Mammon to end. They will need to be dragged kicking and screaming into the Age of Austerity. Consumer expenditures peaked at $10.2 trillion in the 3rd Quarter of 2008. They reduced spending for two quarters, but when Big Daddy Government handed them billions and told them to spend it on cars, appliances, and homes, they dutifully obeyed. Today, consumer expenditures stand at an all-time high of $10.3 trillion, still accounting for 70.5% of GDP. There really has been no hint of austerity by Americans. It is a false storyline. The major reductions in consumption still loom in the future.

The myopic financial "experts" have no sense of history or the concept of reversion to the mean. They didn't get it with home prices and they don't get it with consumer expenditures. The country has been on a 30 year drunken binge of debauchery, debt accumulation and delusions of never ending 10% annual home price gains funding a glorious 30 years of retirement on an island in the Caribbean. These visions of a sugar-plumb life of leisure are slowly giving way to the nightmare scenario of eating cat food in your very own cardboard box McMansion. The bombastic Boomers are turning 50 years old at a rate of 10,000 per day. A staggering 38% of workers between the ages of 45-54 have less than $10,000 of retirement savings and a mind boggling 29% of workers over 55 have less than ten grand in their retirement savings, according to the Employee Benefit Research Institute. It is no longer a matter of people deciding whether to save, it is a matter of saving or else living in abject poverty in their old age.

In the good old days, before the advent of the credit card in 1969, Americans saved up to buy a house, a car, or an appliance. Consumer expenditures as a percentage of GDP stayed in a range of 61% to 64% from 1960 until 1980. This range was reflective of a balanced economy that provided good paying wages to blue collar workers who produced products that were sold in the US and in foreign countries. What a concept. America ran a trade surplus. The financial industry did not drive the economy, they provided financing for businesses that wanted to grow and produce. Sounds quaint. As the Boomers entered their 30s in the early 1980s the easy credit delusion, promoted by Wall Street and the mainstream marketing machine, convinced the spoiled materialistic Boomers that wealth was measured in cool stuff rather than accumulated savings invested over time. Consumer spending as a percentage of GDP surged from 62% to 70% over the next two decades.

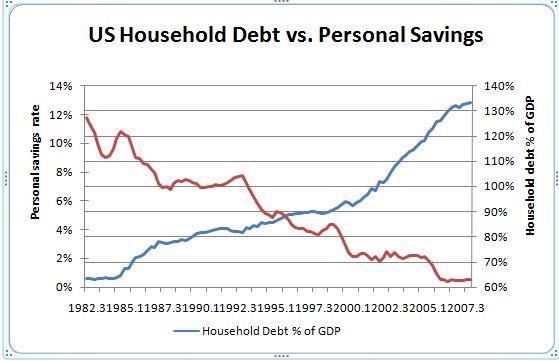

Real wages have been stagnant since the early 1970s. With moribund wage growth there was only one way for Boomers to live the faux American Dream - Borrow to the hilt. And borrow they did. The personal savings rate fell from 12% in the early 1980s to below 2% in 2007. The concept of deferred satisfaction was cast aside by the "no worries" Boomers. Saving and frugality was for the Depression era old fogies. The old timers didn't understand modern finance. Why wait until tomorrow when you can have it today by just whipping out a plastic card? The delusion of debt based "wealth" grew for 25 years, encouraged and stimulated by Alan Greenspan and his bubble blowing machine.

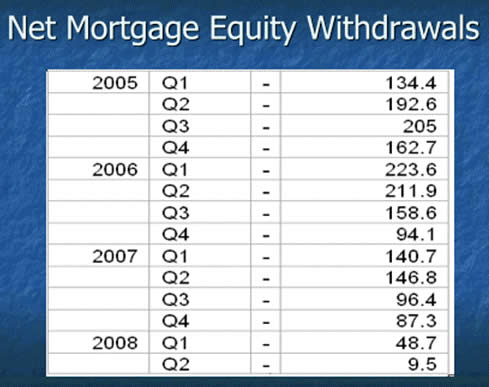

The debt party reached its apex between 2005 and 2007. Boomers willfully ignored or chose to not comprehend the concept of reversion to the mean. They believed with all their hearts that their homes would appreciate at 10% per year for all eternity. To prove their faith in this belief, they used their homes like an ATM and withdrew $1.9 trillion of "equity" between 2005 and 2007 and spent it on 2nd homes, cars, boats, flatscreens, vacations, home theaters, and other assorted must have doo dads. They borrowed against their homes at the absolute peak in home prices. Prices have fallen 30% from the peak, with some markets down 50%. This has left millions up to their eyeballs in debt. The home ATM flashes "INSUFFICIENT FUNDS" when they attempt a withdrawal today.

So here we stand, two years after the financial system collapsed. Government stimulus has provided an artificial boost to GDP. They have tried every trick in the book to convince Americans to keep consuming at a rate higher than they are earning. It is failing because consumers have been shaken from their materialistic stupor. They are slowly coming to the realization that they must save or they will suffer greatly in the next 30 years. The savings rate has been moving erratically higher and is now in the range of 5% to 6%. Ideally, it would need to reach 14% in order for Americans to save enough to cover their retirement. This will never happen. Americans will cut back but they will not revert to the frugal ways of their grandparents.

The GDP of the country is $14.5 trillion. Over the next decade consumer expenditures as a percentage of GDP will fall from 70% to 65% because it must. With stocks destined to return 5%, bonds yielding 2.5% and no equity left in their houses, consumers have no choice. The annual reduction in consumer expenditures will be north of $700 billion. The annual disposable personal income of Americans is $11.3 trillion. The savings rate is 6%. It will rise to 10% over the next few years. This would be $450 billion more savings and $450 billion less spending. This will not happen overnight. It will take at least a decade. Mass delusion wears off slowly and one person at a time. Charles McKay summed up the last 30 years in two quotes from his book Extraordinary Delusions and the Madness of Crowds, written in 1841.

"Money, again, has often been a cause of the delusion of the multitudes. Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper."

"Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one."

Does this paint a picture of an economy roaring ahead? We have at least a decade of low or no growth ahead. Deleveraging after the biggest debt party in history is really a *****. The industry which is about to be dealt a mortal blow is the retail industry.

Retail Death Knell

Our entire consumer society has been built upon a foundation of lies. The biggest being you could get wealthy without saving. The other being that you were wealthy if you owned stuff that made you look wealthy. There are 1.5 million retailers in America. There will not be 1.5 million retailers in 2020. The winnowing of the chaff from the wheat has begun, but will accelerate over the next decade. The mom and pops are already closing up shop in record numbers. The shocking revelation that major mega retailers such as a Target or a Kohl's might not exist in ten years will not be believed today. Ever hear of Montgomery Ward?

What most people don't understand is that the mega-retailers' strategic plans were based upon never ending store growth, 5% comparable store growth for all eternity, a continuous flow of increasing easy credit, the American population staying frozen between the ages of 30 and 50 years old, and a delusional materialistic greed embraced by the masses. Mega retailers without growing comp store sales are like sharks that can't swim. They will die. The comp store sales growth is essential to overcome the effects of cannibalization from new stores. The CEOs of these companies have never modeled a decade of declining sales. They still believe it can't happen, even though it must happen. Delusions die hard, especially for CEOs.

I'll use Target as an example. Almost everyone would agree they have been one of the best run retailers of the last two decades. They have over 1,700 stores in the US, with annual sales exceeding $65 billion and profits of $2.5 billion. How could a retailer this large and successful ever go bankrupt? They have $16.5 billion of debt and $15.3 billion of equity on their balance sheet for a 52% debt to equity level. This is not a dangerous level, but it is a heavy debt load. The deterioration always begins on the sales side. Comp store sales have been deteriorating since 2005 and were negative in 2008 and 2009.

The impact of this sales deterioration can be seen in their net income over the last five years. It is at the same level as it was in 2005 and $361 million lower than 2007. Target opened 343 new stores between 2005 and 2009 and its net income is the same. Net income per store has dropped from $1.72 million in 2005 to $1.43 million in 2009, a 17% drop per store. In their peak profit year of 2007, they generated $1.79 million profit per store.

What most people don't know is that Target goosed their profits using the same method that Americans used to get “rich”. EASY CREDIT. When you've run out of ideas to grow your business, offer easy credit to your customers. It worked like a charm for Target until it didn't. They issued millions of credit cards to the delusional masses. Who needed to sell stuff, when you could make so much lending money? In 2007, the Target credit card accounted for $1.06 billion of their $2.85 billion profit, or 37% of total profits. This was up from 22% of their profits in 2004. They've been learning a difficult lesson as credit card profits plunged to $400 million in 2009 as they desperately tried to sell their rapidly deteriorating portfolio with no takers to be found.

Annual Earnings Data |

|||||

|

2009 |

2008 |

2007 |

2006 |

2005 |

Net Income (1,000′s) |

$ 2,488,000 |

$ 2,214,000 |

$ 2,849,000 |

$ 2,787,000 |

$ 2,408,000 |

YoY % Chg |

12.4% |

-22.3% |

2.2% |

15.7% |

27.7% |

Diluted EPS |

$ 3.30 |

$ 2.86 |

$ 3.33 |

$ 3.21 |

$ 2.71 |

YoY % Chg |

15.4% |

-14.1% |

3.7% |

18.5% |

30.9% |

Annual Store Operating Data |

|||||

|

2009 |

2008 |

2007 |

2006 |

2005 |

Store Count |

1,740 |

1,682 |

1,591 |

1,488 |

1,397 |

Store Sq Ft (1,000s) |

231,941 |

222,588 |

207,945 |

192,064 |

178,260 |

Employees |

351,000 |

351,000 |

366,000 |

352,000 |

338,000 |

|

|||||

Net Sales per Store (1,000′s) |

$ 37,075 |

$ 38,426 |

$ 39,929 |

$ 40,123 |

$ 37,908 |

Net Sales per Sq Ft |

$ 290 |

$ 301 |

$ 318 |

$ 316 |

$ 307 |

Net Sales per Employee |

$ 180,726 |

$ 175,409 |

$ 171,228 |

$ 167,762 |

$ 162,765 |

The beautifully constructed staircase of store growth seen in the chart below has reached the top floor. If Target foolishly continues to build new stores while Americans ratchet up their savings and ratcheting down their spending, they will end up taking an elevator straight to the basement. The credit card fountain of profits is gone. Same store sales growth is gone. New market growth is gone. It's time to get real. The upper management of every retailer in America better pull out their little models and plug in declining consumer spending for the next decade. This will reveal the stores that won't cut it. They will need to close them based on profitability. Will this be done? Absolutely not. The hotshot CEOs will think a better advertising campaign will do the trick. Delusions die slowly.

Many might think I'm being overly pessimistic. I would contend that I've presented a best case scenario. I've completely ignored the implications of peak oil and $5 per gallon gas on mega retailers that require you to drive miles to shop at their stores and source all of their goods from thousands of miles away. Combine that with an ever declining USD that drives the prices of imported good higher and you have a perfect storm for retailers in America. I'm sure the scenarios I've presented will do wonders for commercial real estate and the banks that are on the hook for those loans.

In the immortal words of David Byrne, "the future is certain".

WELL WE KNOW WHERE WE'RE GOIN'

BUT WE DON'T KNOW WHERE WE'VE BEEN

AND WE KNOW WHAT WE'RE KNOWIN'

BUT WE CAN'T SAY WHAT WE'VE SEEN

AND WE'RE NOT LITTLE CHILDREN

AND WE KNOW WHAT WE WANT

AND THE FUTURE IS CERTAIN

GIVE US TIME TO WORK IT OUT

We're on a road to nowhere

Come on inside

Takin' that ride to nowhere

We'll take that ride

Feelin' okay this mornin'

And you know,

We're on the road to paradise

Here we go, here we go

Road to Nowhere - Talking Heads

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2010 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Richard

07 Oct 10, 04:48 |

Meh...

Why pay back my debt when the Fed will wipe it out with inflation? Savers will pay it back, not me. |