The Morality of Chinese Econimic Growth, Crude Oil at $125 a Barrel, Gasoline at $5

Economics / Global Economy Oct 02, 2010 - 05:39 AM GMTBy: John_Mauldin

Oil at $125 a Barrel, Gasoline at $5

Oil at $125 a Barrel, Gasoline at $5

David Rosenberg and Capacity Utilization

Gary Shilling: Commercial Real Estate and Employment

The Morality of Chinese Growth

This week I am at a conference in Houston. I must confess that I don’t attend many of the sessions at most conferences where I speak. But today, the guys at Streettalk Advisors have such a great lineup that I am there for every session. But it’s Friday and I need to write. The solution? This week you get a “best of” letter. The best ideas I’ve heard and the best charts I’ve seen at this conference. Then we close with two short but very thoughtful essays from Charles Gave and Arthur Kroeber of GaveKal on “The Morality of Chinese Growth.” Lots of charts and something to make you think. Should be a good letter.

Oil at $125 a Barrel, Gasoline at $5

John Hofmeister is the former president of Shell Oil and now CEO of the public-policy group Citizens for Affordable Energy. He paints a very stark (even bleak, as he gets further into the speech) picture of the future of energy production in the US unless we change our current policies. First, because of the aftereffects of the moratorium. It is his belief that the drilling moratorium will effectively still be in place until at least the middle of 2012. There won’t even be new rules until the end of 2011, and then the lawsuits start.

Gulf oil production will be down by up to 1 million barrels a day. Imported oil is now 67% of oil usage but will go to 75% by 2012. He thinks crude oil will be up to $125 and gasoline between $4-$5 at the pump. And it will only get worse.

He describes the problem with the electricity from coal production. The average coal plant is 38 years old, with a planned-for life of 50 years. Our energy production capability is rapidly aging, and we are not updating it fast enough.

He argues that the fight between the right and the left has given us 37 years without a realistic energy policy, as policy gets driven by two-year political cycles but good energy planning takes decades. There are 13 government agencies that regulate the energy industry, with conflicting mandates that change very two years. There are 22 congressional committees that have some level of involvement and oversight of the energy industry.

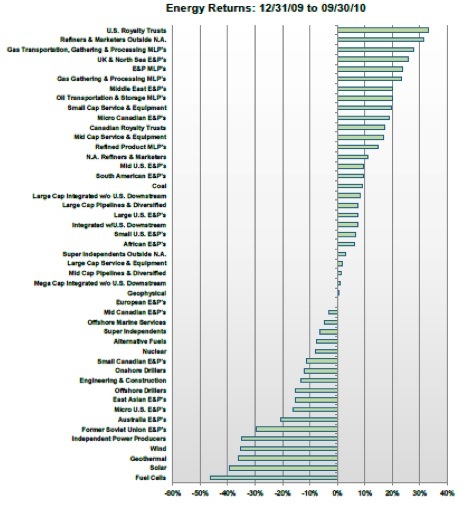

The following table is from data provided by Triple Double Advisors LLC, an energy specialty investment firm in Houston, Texas. John White was sitting next to me and showed me this table, pointing out the poor performance in terms of investor returns from renewable energy sources and the larger returns from Master Limited Partnerships where investors are seeking yield. It seems the market is voting that it doesn’t have much confidence in the renewable energy world. Hofmeister suggests that government subsidies for renewable energy will go away under the pressure to get the fiscal deficit under control. Maybe the market senses that. He says we need to create a 50-year plan for our energy policy that transcends the political cycle. (I am going to get this speech transcribed and will post it so you can read it. This guy talks sense.)

David Rosenberg and Capacity Utilization

I am a big fan of David Rosenberg (former chief economist at Merrill and now with Gluskin Sheff in Toronto), and have really enjoyed getting to know him the last few years. He is a fun guy, even if his data is not exactly bullish. It was hard to pull out the best of his charts for this letter, because he had so many.

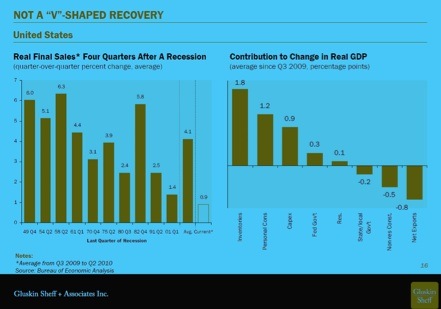

The first chart shows that real final sales are the lowest, four quarters after the end of a recession, that they have ever been. Average growth is 4%, but we’re up less than 1% in the current recovery. The second chart (side by side with the first, below) shows the contribution of various sectors to real GDP growth. You find that of the 3% average growth over the last four quarters, 1.8% was inventory rebuilding. His point (and one I have made as well) is that this is not sustainable. At some point rebuilding will no longer be as big a factor, as inventories will get closer to equilibrium. And the consumer does not look like he is going to ride to the rescue.

Rosie thinks we could slip into negative growth by the end of the year.

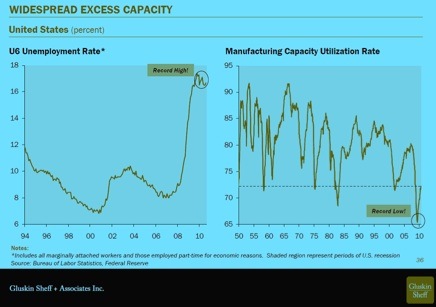

This next chart shows U-6 unemployment compared to manufacturing capacity utilization rates. Unemployment will have difficulty getting better as long as capacity utilization rates are at what is typically thought of as recession levels.

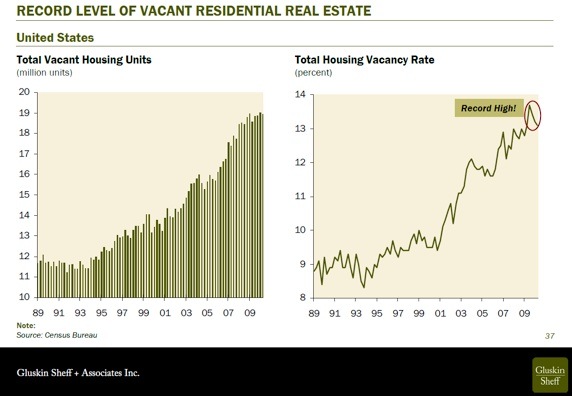

The next and last chart from Rosie is on housing, showing us the large number of vacant homes and the vacancy rate. Home values are not likely to rise nationwide (there will be some good local pockets) until the vacancy rates come down. Ditto for new home construction and the jobs from that sector. Gary Shilling (see next section) says he thinks home prices could drop another 20%.

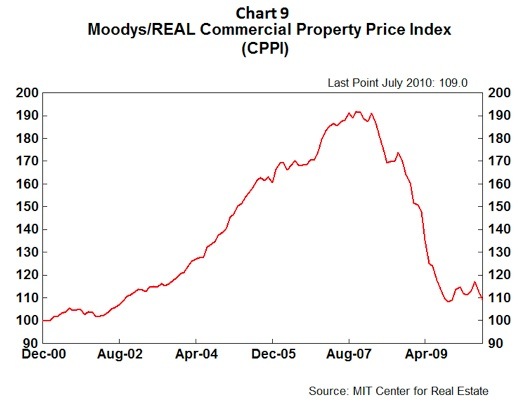

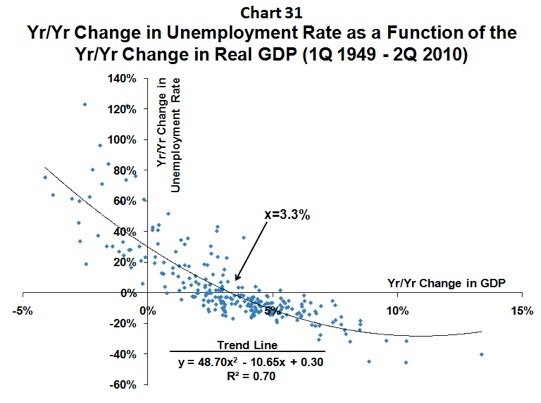

Gary Shilling: Commercial Real Estate and Employment

The next two charts are from good friend Gary Shilling (selected out of about 50 he had). The first shows us that the commercial real estate price index is down almost 40% from its peak. Judging from the graph, it looks like the freefall may be over for now, assuming we do not get into another recession too soon. Is it any wonder that bank lending is down, since so much lending was in commercial real estate and CRE construction?

The last chart shows us the trend line for the relationship between employment growth and GDP. It turns out that you need at least 3% GDP growth to get meaningful employment growth. If growth is slowing down to less than 2%, it is going to be very difficult to really address the unemployment problems.

And now, let’s turn to GaveKal and China.

The Morality of Chinese Growth

We (GaveKal) spend quite a bit of time trying to understand the drivers and fundamentals of Chinese growth. And while we have seen some recent signs of a policy-driven cyclical slowdown (see The Wen Jiabao Put and our latest Quarterly Strategy Chart Book), we remain very optimistic about the Mainland’s structural potential. But up until know, we have not really touched on the more philosophical implications of the Chinese growth story. In that respect, a recent client comment triggered a couple responses we modestly believe could interest the broader readership.

Client Comment: GaveKal’s writings on economics are unmistakably filled with fundamental beliefs regarding human potential, advancement, creativity and the pursuit of knowledge. And even if I did not know your backgrounds, these views appear decidedly French in nature: deeply held beliefs on the rights and dignity of man.

So how does a group of economists focused on the mind and the soul as well as the pocketbook reconcile the sociological challenges presented by modern China? It is undeniable that a country that pulls half a billion people out of subsistence farming in two decades is doing a lot for human decency, no matter how they accomplish it. So maybe I need to throw away my Western lenses when thinking about this. But I really wonder sometimes how you view the authoritarian qualities of 21st century China as it relates to treatment of political rivals, the autonomy of the courts, religious freedoms, control of all forms of media, etc. Should we bend with the breeze and accept that this is the new world?

Charles answers: As I have tried to highlight in a couple of recent documents (see The Way the World Works and Ricardo, Schumpeter & the Cost of Capital), I firmly believe that an overly powerful and extended government is very dangerous. Having said that, I also believe that a total absence of the State is even worse. And since you mention my intrinsic Gallicness, I will turn to the philosophers of the Enlightenment, who happened to often be French, and who showed quite conclusively that human freedom can be exercised in three areas:

1. Political freedom (voting the incompetents out, separation of powers)

2. Social freedom (freedom of worship, sending one’s children to the school of one’s choice, creating a union, etc.)

3. Economic freedom (the ability to create a business, hire or fire employees, etc., regulated by contract law between acting parties).

What the philosophers of the 18th century argued was that the Church had to move out of the political sphere, and the State out of the other two. In Hong Kong, which GaveKal calls home, we enjoy one of the freest societies in the World: we have total social freedom, total economic freedom but yet very little political freedom. Still, I believe this compares extremely well with what we have in France, where the church of Marxism has invaded the State and the educational system, destroying both, while the obese State has invaded the social and economic sphere, leaving entrepreneurs without oxygen. As Tocqueville expected, we have moved towards a strange and benign “molle dictature“.

This brings us to China and your questions. Today, the Chinese government is prepared to increase the population’s economic freedom (far from complete), as well as the social freedom (courts of justice gaining grounds on political cronies, some social rights). But as for political freedom – see you in 20 years. In essence, this is the same deal offered to Singaporeans 30 years ago by Lee Kwan Yew, who now effectively vote for Lee Kwan Yew & sons every time they get a chance!

As a result, and to use Hanna Arendt’s terminology, China is gradually moving from a totalitarian state to an authoritarian state, with a technocratic bias (a la Singapore). To a certain extent, the Chinese government discharges some of its responsibilities pretty well, with some gaping and horrible holes. So while the immediate picture may look ugly, the movement is in the right direction.

Arthur Kroeber answers: Basically I think you need to clarify your questions. Are you surprised that China has been able to deliver high-speed growth while remaining an authoritarian state? If so, there is nothing odd about this. South Korea and Taiwan both achieved their highest sustained growth under brutal dictatorships; Japan achieved its first growth spurt (in the Meiji era) under a benign despotism and its second (post-war) under a one-party state. And of course, most of the modern Western democracies were not really democracies in any modern sense (only landowners could vote, women did not vote…) while they were industrializing. The idea that countries must be liberal democracies in order to achieve high-speed early-stage economic growth is a strange fantasy with no empirical support.

Or is the question that you are worried that China’s path to success means that other countries will follow the same route? Again, the evidence at hand shows that each successful economy, like Tolstoy’s unhappy family, is successful in its own way and that outside models are of limited use (see Dani Rodrik’s One Economics, Many Recipes).

The China model could work in China because of a specific set of historical and institutional factors that are not replicable elsewhere.

These include a 1,500-year history of centralized bureaucratic rule, which set the template for the current governance system of bureaucratic authoritarianism; an almost equally long history of active commerce and preindustrial capitalism which set the template for private sector activity once the state decided to get out of the way; and the presence of Hong Kong, which meant that China could make full use of modern Western institutions (such as a reliable legal system, property rights, efficient services, etc) without having to go through the cumbersome decades-long political hassle of building these at home. (On this latter very important point see the opening chapter of Yasheng Huang’s Capitalism with Chinese Characteristics).

Or is your concern that China has been able to have a dynamic economy while doing nothing to reform its political system, and will continue to be able to do so ad infinitum? Here the perception that China has made no political reform is specious. There is a gigantic difference between China in the 1970s and China today in terms of freedom of expression, breadth of political discourse, personal liberty and property rights.

Through the end of Mao’s rule, China was a totalitarian dictatorship ruled by individual caprice, with generally disastrous results (30-40mn deaths in the 59-62 famine, 10s of millions more in the Cultural Revolution, etc.). Since then it has transformed itself into a bureaucratic authoritarian state with very imperfect but generally increasing accountability of government. This is a massive political transformation. (And Huang, cited above, makes the important point that this “directional liberalism” — this confidence that things were getting durably better — was very important in encouraging China’s entrepreneurs to start work in the 1980s, despite the absence of what we would consider clear property rights).

If we judge China not by how far it has to go but by how far it has come, the change has been dramatic, and we can reasonably expect the political system to continue to evolve in the coming decades, though not necessarily in linear or predictable ways.

Or is your concern that we in the West somehow have to render moral judgment on China, which requires some calculus along the lines of X amount of economic progress is worth Y amount of political repression, so if repression = y-1 then China is “good” and if y+1 then China is “bad”? Here I will wax philosophical and distinguish myself from Charles somewhat. Unlike him (and strangely, since I am generally considered the house Communist), I am not a Marxist, as I strongly believe that it is a society’s underlying political bargains that tend to shape economic activity, not the other way round.

As Isaiah Berlin pointed out, societies grapple with the problem that there are lots of good things – justice, wealth, individual liberty, social stability, security, equity – and we cannot maximize all of them at once. Trade-offs among these ultimate values must be made and that is what politics is about. Societies create a set of trade-offs by negotiation (and by the way democratic elections are not in themselves a mechanism for making these trade-offs; they are simply a mechanism for transmitting information to the agents who are negotiating the trade-offs; so it is a fallacy to presume as many do that only via democratic elections can a society achieve a “true” bargain) and the ultimate bargain configures the playing field on which economic actors operate.

Among the societies we describe as democratic capitalist there are vast differences in the bargains and hence in the nature of economic activity. America tolerates levels of instability, crime, inequality and pernicious religious zealotry that Europeans and Japanese consider absurd, but it gets in return a much more dynamic entrepreneurial system of wealth creation. Japanese willingly accept levels of social conformity that Westerners consider bizarre, but achieves a high level of social stability and tremendous success in economic areas (such as high precision manufacturing), where self-disciplined social cohesion is a plus.

China, like all societies, is working out its bargain. It is still very much a work in progress but the process is dynamic, not static.

We Americans have a strange utopian tendency to assume that among all possible social bargains there is one perfect bargain out there (probably ours) and that it is our job to judge how well other people are keeping on the path to that bargain, any straying from which necessitates perdition for them and gnashing of teeth for us. But maybe we should just stop worrying about it. China will become what it will become and hopefully whatever it becomes will produce good results both materially and spiritually for most Chinese. As long as our society continues to do the same for us, it does not much matter whether the two societies wind up looking a lot or a little like each other. Chacun son gout!

Another Birthday? What Happened to My Year? Athens and the Barefoot Ranch

I turn 61 next Monday. All the kids are coming into town to celebrate with Dad. I am really looking forward to it. But I really have a hard time believing that it’s time for yet another birthday. I am sure it was just last month we celebrated my 60th. Thankfully I don’t feel like I am 61.

It has been a great year on both a personal and business level. Italy with the family was a highlight, and not just of the last year. We are going back to Tuscany next year. I am so grateful that my business is growing and that we are finding new opportunities. Thank you for your support this last year.

And yes, I am going to Athens next week. Athens, Texas, that is. There is a rather large ranch/lodge called the Barefoot Ranch near Athens, where Kyle Bass of Hayman Advisors has invited some 50 people to gather and discuss the markets and the world at large for three days. Fund managers, writers, politicians, historians, and a fairly wide variety of interesting people. That is in the mornings and evenings. In the afternoon we relax. There are lots of things to do. One of the more interesting things will be to shoot sniper rifles under the tutelage of a fairly famous Navy Seal (I understand you are never an ex-Seal).

While I will be presenting, I expect that I will learn a lot more than I impart. It should make for a very interesting letter next week.

And speaking of Athens, I got a text from good friend Prieur du Plessis. Greece, he says, from the island beaches, is clearly not in crisis. But more close observation is needed. As I get on my plane I will pull out my latest International Living and dream about a little R&R.

And it is time to hit the send button. The conference is almost over and I will need to run to the airport and catch a plane back to Dallas and see my kids. It is going to be a good weekend. I see movies and Mimosas and grandkids in my future. I think brunch is set for 14. Have a great week!

Your still feeling like a kid analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.