Fear & Perception - The Speed at Which Investor Sentiment Can Change

Stock-Markets / Financial Markets Nov 01, 2007 - 05:24 PM GMTBy: Doug_Wakefield

“There is truth deep down inside of you that has been waiting for you to discover it, and that Truth is this: you deserve all good things life has to offer . You know that inherently, because you feel awful when you are experiencing the lack of good things. All good things are your birthright!” – The Secret (2007), 41 weeks in top the five NY Times Hardcore Advice List

“There is truth deep down inside of you that has been waiting for you to discover it, and that Truth is this: you deserve all good things life has to offer . You know that inherently, because you feel awful when you are experiencing the lack of good things. All good things are your birthright!” – The Secret (2007), 41 weeks in top the five NY Times Hardcore Advice List

“ Bank of America Corp.'s Michael J. Meyer, head of investment-grade bond trading, is leaving after the company's corporate and investment bank reported a 93 percent decline in third-quarter profit.”

“Stan O'Neal was ousted as chairman and chief executive officer of Merrill Lynch & Co , less than a week after reporting the biggest quarterly loss in the 93-year history of the world's largest brokerage.”

“The slumping U.S. housing market, which cost the world's biggest financial companies more than $30 billion, makes it unlikely UBS's investment bank will return to profit in the fourth quarter, Chief Executive Officer Marcel Rohner said today. Losses at the unit led to the ouster of investment banking head Huw Jenkins and finance chief Clive Standish this month, and outweighed record profit at the wealth management division.”

Either these individuals have yet to find the “truth deep down inside” of themselves, or in the real world, jobs that offer the highest levels of compensation in our economy are not a birthright. As some of the largest financial institutions in the world experience these real and extreme losses, this advice book, which has been at the top of the New York Times best-seller list for over 5 months, seems disconnected from reality. In a similar way, the ever-faster rising world markets look to be propelled more by illusion than reality. The mounting tension, between the real world and what we would want that world to look like, is coming to a head.

In his latest book, The Black Swan: The Impact of the Highly Improbable , Nassim Nicholas Taleb points out that dopamine regulates moods and supplies an internal reward system in the brain, and that higher concentrations of dopamine lowers skepticism. Our innate desire to understand cause-and-effect relationships makes story telling one of the most effective means of communication. For most of us, it is easier to remember and relate to a story than reams of math figures. Eventually, we create our own narrative based on our perception of experiences. As we look back, after we've assigned a cause to an eventual effect, it seems to us that our past should have been much more predictable than it was at the time we experienced it. And, the longer we find information that supports our narrative, we feel more strongly, and are less skeptical, about the validity of our assumptions. And though there is nothing inherently wrong with this, we must be careful as we continuously assess facts and form conclusions.

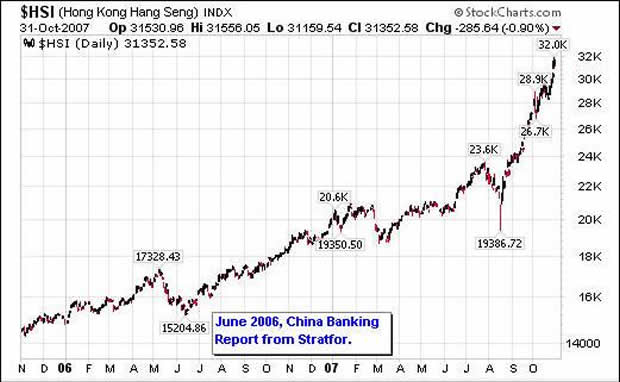

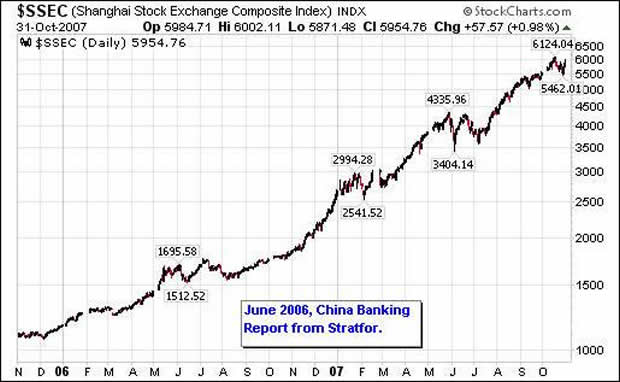

We are watching this unfold in one of the hottest markets in the world today – China. As I was taking some older articles off our website, I stumbled across a June 2006 Stratfor piece on China's non-performing bank loans. Four international financial firms had written of their concerns about China's banks. Fitch comments:

“Estimating a rate of flow of new nonperforming loans is not an easy exercise given Chinese banks' extremely weak historical data and ongoing deficiencies in accounting and disclosure. Few banks report data on NPL flows, and those that do show recent flow rates in the extremely low single digits. We believe these numbers understate the likely level of ultimate credit losses, given what we know to be the slow evolution of a strong credit culture and risk management practices and our suspicion that China's over-reliance on investment-led growth comes at a cost to bank credit quality”

Stratfor concludes: “A turning point has been reached that will be difficult to ignore. Reports from Stratfor are, of course, one thing. Reports from a single credit agency are another. But when a series of reports from highly respected, mainstream analysts all come out within a few days of each other – with each, in their own way, telling the same basic story, it becomes hard for the system to dismiss that. That means that the huge structural imbalance of China, which these debts represent, must be rectified. And that process, as in all such matters, will be painful.”

So, what have millions of investors done since this information was presented since this June 2006 report? See for yourself.

In January of 2006, investors opened an average of 2,708 brokerage accounts per day. By August of 2007, the average had grown to 450,000 individuals accounts opened per day. Is the difference comprised of individuals who are thoroughly investigating companies' economic fundamentals and the sustainability of their stock prices? Are they seeking to understand when these historic leaps will end, or are they looking for any story that supports the view that China's markets will only go up?

One would have to have lived on another planet not to realize the public's changing views of real estate as an investment over the past two years. And yet, since China is the land of unlimited investment possibilities, I'd not be surprised if many of these same people have funds in the Asian markets. It reminds me of the condo flippers a couple years ago, who knew that real estate was a bubble, but were going to get out before the decline started. With the Hang Seng exploding upwards another 33 percent in the last two months, have the concerns that surfaced in June 2006 been cleaned up, or has the pressure from these real financial issues only grown more intense?

No matter how smart we think we are or how large a following we have garnered by pouring tons of other peoples' money into any market that is exploding skyward, until these manic tendencies breakdown, we would do well to ask the following question. As the dollar's devaluation propels markets higher and bullish and bearish sentiments hit historic extremes, what is my exit strategy? Am I aggressively looking for an exit, or am I looking for more stories to support why I am on the right side of the trend?

As a derivatives expert with over 25 years of experience at the highest levels of the global capital markets, in his new book, Traders, Guns & Money , Satyajit Das reminds us how fast public behavior and prices can change. He points out that while Long Term Capital Management watched its star rise, it used leverage of up to 25 times its capital base. But, with returns in excess of 40 percent in 1995 and 1996, the amount of leverage was not a concern. And though the returns were lower in 1997, Merton and Scholes, two of the men at the helm of the hedge fund, received the Nobel Prize for Economics that October. For most people, this solidified their story of successful investing. They had chosen the right strategies and were investing with the elite. How many investors could boast of such an impressive story!

However, by the fall of the next year, the real bond market, the real Russian economy, and the real government in Indonesia had become increasingly unstable. By September of 1998, LTCM had lost 92 percent of its capital, which increased its leverage to over 100 times its capital. Even so, Meriwether, the head of LTCM, stated, “We've had a serious markdown buy everything's fine with us.” On October 18 th of 1998, LTCM's principal broker, Bear Sterns (which still seems to be having a hard time remembering the history of highly leverage hedge funds) was rumored to have frozen the fund's cash account following a huge margin call. After ever possibility of a buyer was exhausted, the New York Federal Reserve facilitated a recapitalization of LTCM and 14 banks invested $3.6 billion in return for 90 percent stake in LTCM.

After the Federal Reserve quickly cut interest rates in early October of that year, the story of LTCM became buried in the roar of the bull run that took the markets into early 2000. Even today, I wonder how many investors, depending on buy and hold strategies, know the dozens of similarities between 1998 and the events that have been unfolding since July of 2007.

With the enormous increase in leverage since 1998, the vastly more complex array of exotic financial products, and the technology that allows large trades to move much faster than the fall of 1998, should investors, advisors, and traders, be waiting for reports from the few individuals who have been invited to private weekend meetings? [See recent MLEC developments] Or, should we prepare our finance and business strategies before we read the various explanations of what went wrong, which will be based on erroneous cause and effect relationships?

Those who are sure that human psychology and crowd behavior is different this time, and that the “dollar will only go down and most other investments will only go up,” should be asking, “what happens after the dollar collapses?” Because of the dollar decline of the last few years, we have come to believe in a linear narrative of a “dollar collapse.” But, a study of history reveals cycles, forcing us to ask, “what will happen when this trend changes?” Lest we forget what happens when markets start to correlate, let me close with these words from another Nobel Laureate for Economics, Merton H. Miller:

“The question …is whether the LTCM disaster was merely a unique isolated event, a bad drawing from nature's urn; of whether such disasters are the inevitable consequences of the Black-Scholes formula itself and the illusion it may give that all market participants can hedge away all their risks at the same time .” [Italics mine]

If you're interested in what various experts, from a variety of disciplines, have to say about finance, you should consider becoming a part of The Investor's Mind and benefiting from the research and views of some of the most experienced individuals in the world of money. To get a feel for the educational material we've presented to our readers since January of 2006, click here . We continue to gain recognition for our 154-page industry paper on short selling, Riders on the Storm: Short Selling in Contrary Winds , which can be obtained with a subscription to The Investor's Mind. To learn more about our mission, as well as our educational and advisory services, visit our website .

Sources:

- The Black Swan: The Impact of the Highly Improbable (2007), Nassim Nicholas Taleb

- Traders Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006), Satyajit Das

- When Genius Failed: The Rise and Fall of Long-Term Capital Management (2000), Roger Lowenstein

By Doug Wakefield with Ben Hill

President

Best Minds Inc. , A Registered Investment Advisor

Copyright © 2005-2007 Best Minds Inc.

Best Minds, Inc is a registered investment advisor that looks to the best minds in the world of finance and economics to seek a direction for our clients. To be a true advocate to our clients, we have found it necessary to go well beyond the norms in financial planning today. We are avid readers. In our study of the markets, we research general history, financial and economic history, fundamental and technical analysis, and mass and individual psychology.

Doug Wakefield Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.