Currency Cross Signals - Unwinding of Yen Carry Trades Leads to Temporary Dollar Rally Against Long-term Devaluation

Currencies / Yen Carry Trade Nov 15, 2007 - 12:31 PM GMTBy: Jim_Willie_CB

In the last several weeks, tremendous movement and change has occurred in foreign currencies. Almost all foreign currencies have made multi-year highs against the crippled US Dollar. The United States suffers from wretched finances and a banking system teetering on seizures. In progress is the gradual dismantling of large tinkertoy structures within its vast network of bond risk management. Its entire business of structured finance is under siege and revaluation.

In the last several weeks, tremendous movement and change has occurred in foreign currencies. Almost all foreign currencies have made multi-year highs against the crippled US Dollar. The United States suffers from wretched finances and a banking system teetering on seizures. In progress is the gradual dismantling of large tinkertoy structures within its vast network of bond risk management. Its entire business of structured finance is under siege and revaluation.

The banking & bond woes cannot be blamed on just the subprime mortgages, those mispriced collections of slime used in considerable export to those very friendly parties who supply the necessary $2.1 billion in daily US capital. No, the USDollar can be identified as a ‘subprime currency' slowly enduring recognition as such. The buck is badly mispriced, offering a yield under half of the true price inflation rate of 10.4%, falsely rated as ‘AAA' under coercion, supported by broad statistical lies, exported widely to foreign institutions, and wrecking havoc in economies who peg their currencies to the US$. How shallow can any denial be?

As one peruses the various currencies and their exchange rates, multi-year highs can be seen across the spectrum. Two key currencies stand out in prominence, the Swiss franc and the Japanese yen. Furthermore, two key crosses are significant in their own right. The cross of the swissy with the euro, and the cross of the euro with the yen each delivers a powerful message of profound change.

The November Hat Trick Letter covers the currency chess game, but also the most powerful currency on the planet, the Canadian Dollar. Goldman Sachs shot it down after extended gains to the 110 level. Soon outgoing central banker David Dodge made some defensive painful comments in mid-October when the loonie had reached the 103.5 level following boastful commentary of deserved loonie strength. With John Thain appointed as the new CEO at Merrill Lynch, the parade continues of former GSax executives taking control of powerful Western financial organizations. See the US Dept of Treasury, US Dept of Energy, World Bank, the Bank of Canada, the central bank of Italy , and now Merrill Lynch. Maybe Goldman Sachs should take control of all regulatory bodies and debt rating agencies and indexed funds and currency controls and financial news media?

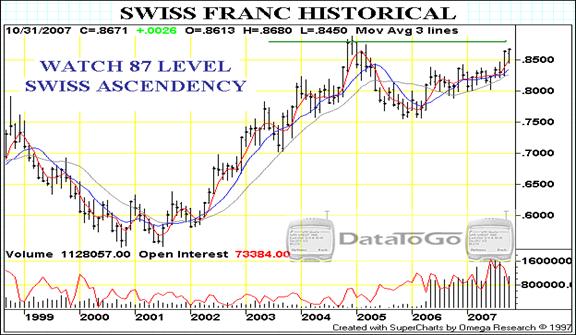

SWISS FRANC STEPS FORWARD

In the last couple months, much attention has come to the euro. It hit 147, after being 110 in the summer of 2003 when the late great Kurt Richebächer sipped coffee on his veranda with me, discussing how euro warrants were the centerpiece to his estate. He wanted to bequeath to his children large sums based on designed bets against the USDollar. The European Union economy has a juggernaut within it, Germany , whose export business per capita exceeds even that of Japan , a little known fact passed from Dr Kurt. The Euro Central Bank feels behind the curve with an official 4.0% interest rate, now stuck due to the US problem. The Swiss franc is the real story on the currency front in Europe though. It soon will register a multi-decade high.

Some crucial comments are warranted on the Swiss, from a geopolitical standpoint. As a preface, former USFed Chairman Alan Greenspan took a paycheck from the Swiss bankers. Its size is unknown, so one must wonder if it was indeed larger than his US-based paycheck. A suspicious person (it pays to be suspicious these days) might regard Greenspan as having worked a second hidden agenda, to restore banking power back to Switzerland after sixty years. The Swiss quietly resent the Americans, who after World War II wrested banking power as the spoils from war. They see the US bankers and economists and politicians and war machine as having essentially destroyed the global banking system. The Swiss want power to return to central Europe . Recall that the owners of the US Federal Reserve are reported to reside in both Switzerland and London , in more control of US monetary policy (if not political leaders) than people realize. One signal of power restored to Switzerland can be interpreted as the Swiss franc making decade highs, in order to confirm prominence in its quintessential power center, banking. Notice the increase in trading volume in the last 18 months.

SWISS-EURO CROSS REVERSES

During the brief correction in midweek last week, a very important event occurred. The Swiss franc hardly budged, not correcting much at all. Many regard the swissy as a currency-based insurance policy in the volatile FOREX trading pits. The swissy often is overlooked in the central bank interventions, where the USDollar, euro, and yen dominate. This Monday when the euro, pound sterling, Canadian dollar fell by well over 100 basis points each, the swissy remained steady. We probably have seen yet another one-day USDollar bounce. The beleaguered buck suffered multiple slow bleed down days in the last couple weeks, but only one fleeting day with a powerful corrective bounce upward.

In the last month, the Swiss franc has reversed its position relative to the euro currency. While the euro has risen, the swissy has risen more. As the euro has corrected very moderately, the swissy has not corrected much at all. The call is early, but the long two-year slide for the Swiss franc relative to the euro appears to have halted. Two weeks ago, a powerful reversal occurred, one in continuation. The ratio swept past the 20-week moving average easily. Let's see if the ratio moves past the 50-wk MA. Let's also see if the 20-wk MA crosses above the 50-wk MA to flash a strong bullish signal. The Swiss franc might be working to take back its position of prominence, where for over a century it stood firm as the true primary investment currency.

Both the Swiss franc and the Japanese yen are important to monitor during these crisis times. Europe is taking a lead role in currency adjustment, setting the euro as a defacto dual standard for a world reserve currency. They feel pain for that lead role, as ECB head Trichet calls the adjustment brutal. Asia is taking a lead role in currency management, setting the pathway for diversification away from the USDollar AND for the management of Sovereign Wealth Fund. The SWFs are rendered controversial by the secrecy and confrontational positions to energy and mineral dominance. The US Congress mulls over options to regulate foreign billion$ in a truly laughable toothless display of helpless weakness. They want more disclosure like with Norway 's SWF. In the background is the Persian Gulf group of nations, threatening to loosen their tight peg with the USDollar, but succumbing to US pressures. They possess no military. However, back to the yen and its cross.

JAPANESE YEN REFLECTS ITS CARRY TRADE

The most watched currency cross in the last several months, for its indication on global speculative finance, has been the euro over the Japanese yen ratio. Both currencies are rising, but the yen is rising faster. The 91.5 level is crucially important from a technical standpoint. The correction in August 2005 (to hit the 20-week moving average) and in the May 2006 spike when the Bank of Japan began its ultra slow motion interest rate hike sequence, these set the resistance levels which are soon to be broken.

Notice the crossover of the 20-wk MA above the 50-wk MA in September, a siren call warning in the currency world. In fact, the powerful reversal since June-July 2007 from the 80-81 level coincides with a gradual unwind of the grandest carry trade phenomenon in the history of the modern world. The Yen Carry Trade profits from borrowing cheap Japanese yen and investing in higher yielding USTreasury Bonds, with a currency risk inherent. It is unwinding. The impact not only to speculative investment, but to baseline structural investment, is enormous and given little emphasis. The correlation between the S&P500 stock index in the US and the Japanese yen is strong. The linkage has been apparent to me for over a year. The implication is that the Yen Carry Trade might govern the US stock market. Its unwind governs the selloff in the largest among US stocks. The November Hat Trick Letter provides further crystal clear, if not shocking evidence of linkage.

EURO-YEN CROSS BREAKS DOWN

With little tested history, the euro is the product of an amalgam of currencies in loose association from a European continent attempting to unify once again. Some call the euro-yen cross the most important currency related signal to monitor appetite for risk. The yen is a suppressed currency, kept down with US blessing and brute force. The yen appears to be awakening after a decade or more of slumber. In my view, the emergence of China makes the yen awakening unavoidable. China has become the most important focal point in Asia , so Tokyo had better acknowledge this change, and show respect with a bow. The Bank of Japan has continued its hawkish tone, threatening to hike interest rates, but holding back. They show deference to the USFed. The double top failure in this euro-yen cross indicates clearly that the Japanese yen currency is to continue its rise. In the process, the global finance system will be forced to endure shock waves. The Yen Carry Trade is unwinding at the same time that the US financial structure of risk management is being dismantled. These two corners of the globe are extraordinarily important. By contrast, Europe seems quiet, staid, and boring, with a task of leading in the currency adjustment process. Soon the yen will share that burden.

A powerfully important dynamic requires attention. The entire commodity investment bull market, precious metals, energy, and base metals, depends on continued easy money from Japan AND a yen currency which does not continue to rise. The yen is rising from the weakness of the USDollar, a shaky US banking system resisting seizures, and the likelihood of further USFed rate cuts, more than from the prospect of a series of BOJ rate hikes. The USDollar weakness is profound enough to jeopardize financial investment flow of Japanese funds for the commodity bull market itself. And that bull market trend is leveraged by USDollar weakness. Talk about a paradox!!!

On November 13, the Bank of Japan held steady on interest rates, keeping their official cost of money at the insane 0.5% rate. Their credibility is not as firm as the Euro Central Bank. BOJ Governor Fukui voted to hold steady on interest rates, citing a reduced economic growth estimate, a construction downturn, export risk from the US housing & mortgage problems, and hardship to small businesses from higher energy costs. The combined effects of higher energy costs, US woes, rising yen currency, and Japanese stock market breakdown enable the BOJ to salute the US Federal Reserve and hold steady. More details are in my November report. Do other people grow uncomfortable when the two leading Japanese names are Fukui ad Fukuda? Do such names pass the political correct test? Japanese Prime Minister Yasuo Fukuda refused to dismiss the possibility of formal interventions so as to keep the yen currency from rising too much too fast. The Nikkei stock index in Japan is showing distress.

CONCLUSION

The November Hat Trick Letter contains a frightening list of relevant important quotes regarding the developing dire situation with the USDollar. In focus is the US$ as world reserve currency, the global banking system stability, foreign accumulation of reserves, lost sovereignty of US policy, imminent breakdown of the PetroDollar standard, and palpable US vulnerability. In the last few years those leaders subjugated under USDollar policy dictated to them have been actively resisting, if not revolting. The fall of the USDollar from grace amounts to a tectonic shift in the global hierarchy.

This time, the US currency is on the clear defensive. A description of hegemony (abused dominance) applies. Recent chapters center on the ascendance of China and India, growing confidence in the European common currency, record American deficits, the challenge by London over New York as a financial center, the ongoing housing recession in the US, the mortgage banking debacle, the export of mortgage bond fraud, and the gradual seizure of the US banking system. Prominent economists are raising the specter that the USDollar status as the world reserve currency is no longer dominant. For the first time, Treasury Secy Paulson has been on the defensive in the face of stated concerns of the USDollar role as a reserve currency, as in during G7 Meeting of finance ministers.

The falling USDollar is a hidden mechanism for importing price inflation. The tremendous money supply growth guarantees the continued falling exchange rates for the USDollar versus other currencies. As the USEconomy finds increasing obstacles and backfires to exporting its inflation, the end result will be more price inflation within the United States as it cannot escape so easily. Refer to the reaction by foreigners to bond fraud in subprime mortgages, and refer to trade sanctions planned against China . The growth in US$ money supply is shocking, reminiscent of Weimar Times in pre-WW2 Germany . The M3 annual growth of US$ money supply is at a 36-year high, running at 14.7% and adding pressure to the USDollar. A global currency war is underway. Foreign central banks will ramp up their own money supply growth rates so as to defend themselves and prevent their currencies from rapid appreciation. The round robin game to undermine currencies is precisely what lifts the gold price to the heavens . Eventually, people will call into question the value of paper.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“Your newsletter caught my attention when the Richebacher report ended. Yours has more depth and is broader in coverage for the difficult topics of relevance today. You pick up where he left off, and take it one level deeper, a tribute.” - (JoeS in New York )

“Great Hat Trick Letter in September, very informative. I have been in the metals since the 1970's. You are right on with these issues that we all face today.” - (BillB in California )

“My subscription is worth double what I pay. Once for the economic analysis, and once for the education in wordsmithing! I am coming to value the second one the most, as your alliteration and parable-esque style keeps me smiling even as you write about the walls crashing down!” -(MichaelH in Georgia )

“I am currently subscribed to over 60 paid newsletters. Your analysis is by far the most accurate every time. The most impressive characteristic of your thought processes is your ability to think in multi-factorial terms. You are one of the few remaining intellectuals with such capacity intact.” - (Gabriel R in Mexico )

By Jim Willie CB

Editor of the “HAT TRICK LETTER”

www.GoldenJackass.com

www.GoldenJackass.com/subscribe.html

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise like a cantilever during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by heretical central bankers and charlatan economic advisors, whose interference has irreversibly altered and damaged the world financial system. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy. A tad of relevant geopolitics is covered as well. Articles in this series are promotional, an unabashed gesture to induce readers to subscribe.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 24 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.