Gold $1,200 is New Normal

Commodities / Gold and Silver 2011 May 14, 2011 - 06:22 AM GMTBy: The_Gold_Report

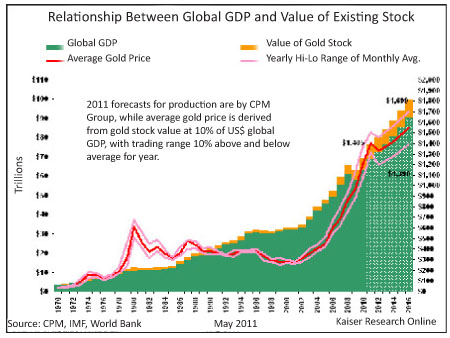

What is good for the U.S. economy is good for gold. John Kaiser, editor of Kaiser Research Online, has proposed a graphic model that relates the value of all above-ground gold stock to global Gross Domestic Product (GDP), thereby explaining why higher real gold prices—even with a recovering American economy—will be the new reality. In this exclusive interview with The Gold Report, he shares his projections about where both gold prices and the U.S. economy could be going in the future.

What is good for the U.S. economy is good for gold. John Kaiser, editor of Kaiser Research Online, has proposed a graphic model that relates the value of all above-ground gold stock to global Gross Domestic Product (GDP), thereby explaining why higher real gold prices—even with a recovering American economy—will be the new reality. In this exclusive interview with The Gold Report, he shares his projections about where both gold prices and the U.S. economy could be going in the future.

The Gold Report: Intel Cofounder Andy Grove wrote an article in BusinessWeek bemoaning the fact that U.S. entrepreneurs in both the hightech and cleantech realm have become inefficient in the return of jobs created per investment dollar basis. He said companies hire fewer employees as more work is done by outside contractors, usually in Asia. He suggested this is a problem not only for low-grade production jobs but also robs the U.S. of its innovation edge, hurting the country's overall economic prospects for the future. Your economic research illustrates this manufacturing decline and shows the value of gold stock values over the last four decades mirroring the U.S. GDP. Why is consolidating manufacturing and research important for U.S. and global growth and how is it linked to the price of gold?

John Kaiser: A lack of physical manufacturing stifles innovation because without access to support facilities, machine shops, test labs and other resources normally associated with a full-scale manufacturing operation, creative people don't see problems, quickly test solutions and have the ability to bring products to scale in a controlled environment. Cut off from manufacturing operations, development stalls.

The American economy is still the largest in the world with a $14.7 trillion dollar GDP followed now by China at nearly $6 trillion. The problem is that the employment structure of the U.S. economy has, in the last 30 years, shifted very much to service jobs in the healthcare, retail, financial and professional sectors, away from making physical goods, that are increasingly imported. We also have a serious oil addiction, which contributes significantly to the trade deficit as we import oil to keep our cars moving. So what are we actually shipping abroad that allows us to offset all the stuff that we import? The jobs we see in the United States today produce less exportable output. That has not hurt economic growth, but it has been achieved through a drawdown of the wealth accumulated during the last century, a drawdown that accelerated during the last decade when a huge debt expansion party bubbled through the economy. But that party ended in 2008. We have now had two rounds of quantitative easing designed to keep the economy from collapsing. In order for the United States to deal with its long-term structural debts and deficits, it needs to demonstrate that there is something American workers can do that is of value to the rest of the world. The core has to be manufacturing.

TGR: Is your argument that we should ignore the lower cost structure we can achieve overseas, bring assembly jobs back to the U.S. and start manufacturing here? Wouldn't the cost of goods go up and spur on inflation at a more rapid pace than we're expecting just because of quantitative easing?

JK: There could be some interim higher costs from bringing manufacturing back to the United States. However, inflation with regard to imported goods due to increasing transportation costs, higher Chinese workspace and emission standards, generally higher wages and the rising value of the Chinese Renminbi is coming anyway. We can't wait to react until we are stuck paying their higher prices with no domestic alternative because we have lost the manufacturing and R&D infrastructure at home. We need to anticipate this higher overseas cost structure and act now.

TGR: Won't those jobs just go to another lower-cost Asian country like Vietnam or Thailand?

JK: Those countries have considerably smaller populations and without super-automation they don't have the capacity to absorb a large-scale influx of manufacturing capacity. If the solution is super-automation, then you are reducing labor costs anyway so why not do it in the U.S. and avoid the political upheaval that could disrupt the production? Two outcomes of the 30-year decline in U.S. manufacturing are that the power of labor unions has diminished, and much of the legacy manufacturing infrastructure has disappeared. To a large degree American legacy production methods were simply shifted overseas where there was an abundance of cheap and willing labor. If manufacturing is to make a comeback in the U.S. it will be in a highly automated form with newly trained employees drawn from the younger generation, not the current boomer generation or their near-retirement parents. If boomers hope to receive their entitlements when they retire, it cannot be paid for by taxing young workers doing little more than fulfilling those entitlement expectations through service jobs.

TGR: Is supply chain and geopolitical security part of what's driving this consolidation of research and the manufacturing?

JK: Yes. Long term, as China becomes stronger, it will flex its muscles. It's just refurbished an old Soviet aircraft carrier so that it can park itself in the South China Sea and exert its military presence. If the United States ceases to produce anything, it will become irrelevant and lose influence anywhere in the world.

TGR: Are major companies bringing manufacturing back based on the reasons you just outlined?

JK: Yes, one example is Boeing, which is way over budget and delivery deadline on its new generation of composite materials-based 787 Dreamliner airplanes. Because the company had outsourced construction of every component, including design, the pieces didn't fit during the assembly process in Seattle. It didn't work. The company is now looking at changing its outsourcing strategy by developing a centralized industrial park in which its subcontractors will be required to have a physical presence. That way engineers can see first hand if a piece fits.

TGR: Does that mean consolidation of design and manufacturing domestically will be driven by private enterprise operating in their best long-term interest rather than the government mandating it though trade tariffs?

JK: Yes. Protectionism in the old style is not going to fly. Instead, individuals and companies will have to voluntarily adopt total cost accounting. Instead of just looking for a cheap price, consumers will have to consider all the costs associated, including safety standards, environmental factors and sustainability. By adding in the costs that have literally been dumped on somebody else, we do the responsible thing. We have to stop being parasites, hurting others for our own cheap goods. This total cost view will create jobs and make the country stronger in the long run.

From a corporate perspective, the opportunity cost posed by supply chain disruptions needs to be factored into the cost-benefit analysis before they happen, not just ignored and then suffered when natural disasters or political upheavals happen overseas such as recently happened in Japan. If we stop assuming eternally cheap transportation costs, building and operating factories close to destination markets starts to make sense. It's also time to ditch the narrow-minded self-interest of the libertarian school and borrow a page from Henry Ford's book of enlightened self-interest: if you want consumers to buy your product, they need to pay with money earned through productive jobs, not entitlement spending.

TGR: While we're talking about consolidation and the global shift, please comment on the Barrick Gold Corp. (TSX:ABX; NYSE:ABX)/Equinox Minerals Ltd. (TSX:EQN; ASX:EQN) deal. You predicted gold in the thousands last year. Why do you think Barrick Gold purchased Equinox Minerals, a copper play in Chile, when gold is at an all-time high right now?

JK: First, gold is not at an all-time high in inflation-adjusted terms, which would be about $2,300 using the $850 peak in 1980 as a base. It is only two-thirds of the way to an all-time high. But if we use $400 where gold settled in 1980 as a base, the inflation-adjusted price is about $1,024. That means today's gold price of $1,500 is about 50% higher than in 1980 in real price terms. But rather than look at the gold price, I look at the value of the above-ground gold stock. About 3.2 billion ounces (Boz.) existed in 1980; today that number is about 5.8 Boz. It is remarkable that during a 30-year period the mining industry nearly doubled a gold stock, which had taken several thousand years to build. This was possible because between 1970 and 1980 gold underwent a tenfold price increase. That equaled a 500% real increase for a mining industry locked in a $35/oz. mindset. Once gold was released from its monetary prison, it established a new relationship to the value of the global economy expressed in U.S. dollars, which I have graphed.

Models are based on each country's GDP converted into U.S. dollars. While a 50% devaluation of the U.S. dollar should not change the nominal U.S. GDP, the U.S. dollar GDP of all other countries would rise, boosting global U.S. dollar GDP sharply to $110 trillion without any real growth. That would translate into a $2,100/oz. gold price if the gold stock stays valued at 10% of global GDP. Of course, the cost of everything would increase correspondingly and gold companies would be no better off than they are now at $1,500 gold. The model also accounts for the inflation of the gold stock through mine supply. A higher real price will boost gold production, which CPM Group projects as growing from 83 Moz. in 2011 to 103 Moz. by 2016.

I took the above-ground stock of gold that existed in each year and multiplied it by the average price of gold during that year to get the value of all the gold that existed in each year. Then I divided it by the nominal GDP of the world for each corresponding year. That produces an interesting chart. It shows gold going from about 3% of GDP in the 1970s to a peak of 20% during the 1980 bubble and then crashing all the way back down to 4% in 2002 at the bottom of the gold market. Now it is 10%, which is about halfway to what you might regard as a bubble peak. I think gold will stabilize at these levels and go up as GDP grows.

The International Monetary Fund is predicting that our $62 trillion GDP from last year will be almost $90 trillion globally by 2016. So, if you take 10% as the norm, gold should be stable within a $1,400/oz. to $1,700/oz. range over the next six years. That's a sustainable price assuming the world is growing. Growth would also result in increased copper demand. Barrick is diversifying its revenue base and treating both gold and copper as commodities. Copper, because it is mined to serve as a means to an end rather than as an end in itself as is the case with gold, does not have the arbitrary price volatility of gold. If suddenly the world decided it didn't need the gold anymore and wanted to convert it into some other form of asset, it would be worth a lot less. Because copper is useful for construction, there is a limit as to how low it can go. Barrick sent a signal that it thinks the global economy is going to grow, that we are not dealing with either a looming depression or hyperinflation. I welcome that because it means gold and copper will have a strong future for the next five years.

TGR: Do you foresee more mergers and acquisitions in precious metals? Is this the start of a trend?

JK: Yes. As companies focus on advancing projects, it will take large capital investment. It will be difficult for a stand-alone project to raise $500M+ without being absorbed by a bigger company that already has production in place and is generating cashflow. This is an opportunity for large, liquid companies to acquire these assets without paying a big premium, particularly if it uses its paper as currency. It is a one plus one equals three situation because as the acquiring company diversifies its revenue base, its catastrophe risk declines. As the market gets more comfortable with gold at current levels, we will see mergers and acquisitions step up and more money coming into the market.

TGR: So, you see economic growth as price drivers for both gold and copper?

JK: In the case of gold, yes. In the case of copper, the question is whether $4 copper is the new reality on which we can base mine development decisions, given a low inflation scenario. The key thing that has happened in the last decade is that China has become a significant economic force. It has now displaced Japan as the second-largest economy with a billion-plus population base and relatively low per-capita GDP. It could grow substantially and eventually become larger than the U.S. economy. But, China is still an unusual political entity; it is a hybrid communist-capitalist country. As they get stronger, we have no idea how they will behave on the global stage. Therefore, people are shifting capital into gold as part of their long-term security plans. As GDP grows, it will probably grow faster than the ability to bring new gold supply on stream. Therefore, gold will rise in price as it tracks the strength of the global economy.

TGR: If you're expecting the price of gold to track nominal GDP, which is growing 2% to 4%, won't you see money coming out of gold and going into equities that would probably represent a higher potential return?

JK: All the gold in the world is about 5.3 Boz., worth about $8 trillion. That's really a fraction of the estimated net worth of all other assets, which is about $130 trillion. Most gold is held as a long-term asset. So even if the crazy gold bugs start selling to buy stocks, they are a small minority and won't make a huge difference. I believe the value of gold stock as 10% of GDP is a reasonable level. Make it a lot higher and gold owners will look to convert it into other assets such as land, buildings, resources and dividend- or interest-yielding instruments capable of generating a cash flow as opposed to a capital gain. What would the new owner's reason be for buying? The only return generated by gold is psychological stress relief. However, if gold prices surge to 20% of GDP as it did in 1980, it will be because of an unstable global situation. Under such conditions, gold ownership is not likely to offer much stress relief, especially if government confiscation or a breakdown of law and order become risks. At 20% of GDP, the value of the gold stock would imply a price of about $2,400 in real terms (as opposed to a price rise generated by excessive inflation or a major devaluation of the U.S. dollar against other currencies). In 1980, when gold was 20% of GDP, some thought the United States had reached the end of the line. But the United States survived that crisis and went on to win the Cold War, unleash globalization and accelerate time through the Internet communications revolution. Short of a calamitous collapse in China, I see the center of gravity for global economic and military power gradually shifting away from the United States during the coming decades. On the other hand, I do not see the value of the gold stock dropping back to 5% of GDP because this would require a major decrease in our uncertainty about the future global order.

TGR: What does this mean for silver? Both gold and silver had a setback recently.

JK: Silver has been the worst performing metal for decades. What it's doing now is a bit of a catch up. Although most of the above-ground silver stock of 46 Boz. is fabricated into some useful form, unlike gold, silver is gaining popularity, especially in emerging economies. The above-ground silver stock value went from 1.5% of GDP in 1970 to a peak of 6% in 1980. But by 2002 the silver stock was worth only 0.5% of GDP. Right now it's between 2% and 3%. I believe silver can parallel gold's role as a hedge against the uncertainty associated with the long-term relative decline of the United States and the gradual disappearance of the U.S. dollar as the world's reserve currency. If we assume the silver stock will establish a value as 3% of global GDP, the price will base out in the $30–$40 range this year, which will grow to $47–$57 by 2016. If it goes to $100/oz., that would indicate a bubble reflecting the inflation-adjusted equivalent of the $50 peak in 1980. Because the recent price growth looks exponential, the markets have fought back and a bear attack is pushing silver back down. But I believe $30–$50/oz. will be the new long-term reality, which opens up some good buying opportunities among silver companies in the next couple of months.

TGR: Since the pullback is happening right now and it has been pretty dramatic, wouldn't the buying opportunity be now? What will be different in two months?

JK: I'm not a big fan of catching falling knives and anvils. I like to see them bounce around first so I know they're not going to hurt me. Especially this time of year, it might be best to see where silver and gold stabilize.

TGR: What do all these new economic drivers mean for gold, copper and silver mining companies? And what companies could capitalize on these changes?

JK: Well, the pessimism embedded in the market right now about the U.S. economy and, ultimately, the global economy that still very much depends on the U.S. economy, has discouraged the market from taking current metal prices seriously. If you plug in $1,500/oz. gold and $4/oz. copper into the discounted cash-flow models for these development projects, you get some very sexy numbers compared to what the stocks are trading at. For example, take Geologix Explorations Inc. (TSX:GIX). It has the Tepal Project, a copper/gold play. It's not super high grade or very large. But, right now the stock's trading below $0.50. Conservative numbers like $2.75/lb. copper and $1,100/oz. gold result in a value of about $1.10 a share, which is not very exciting. But plug in current prices, $4/lb. copper and $1,500/oz. gold, and the target blossoms into the $3/lb.–$4/lb. range.

We see this across the board, an unwillingness to plug current metal prices into the valuations because of an assumption that we're going to see copper back below $2/lb. or gold back to $1,000/oz. And, yes, if we end up in a global depression we will certainly see the metal prices go back down. But I see the global economy trending upward, causing gold and copper to stay strong, thereby leading to an inflection point when the market realizes this pessimistic attitude is all wrong. Then the market will take these prices seriously and put capital into mining projects to mobilize new metal supplies. The problem with mine development is it takes three to five years to realize. That is why we need to start going after these huge profit margins now instead of perpetually waiting for signs of an enduring recovery. The irony of the inflation we are seeing in raw material prices today, which threaten to destabilize emerging market economies, is that it is due to the reluctance of capital markets to take the IMF GDP growth projections seriously and deploy capital to mobilize new mine supply.

TGR: What companies are making those investments today?

JK: Sandspring Resources Ltd. (TSX.V:SSP) is an example. It started off as an alluvial gold operation in Guyana. The company ended up going public and raising capital to focus on the bedrock potential, thereby developing a large gold resource with a minor copper credit. Sandspring just completed a preliminary economic assessment using current pricing that suggests the project is worth about $900M. Yet the market valuation is about $300M. That gives you three to five times upside potential if there are no glitches in the pre-feasibility study and current metal prices get nailed to the wall.

Exeter Resource Corp. (TSX:XRC; NYSE.A:XRA; Fkft:EXB) is another example. The company discovered the Caspiche deposit in Chile. It has a large copper resource. It also has a low-grade gold-oxide resource on top. The copper resource is too big for Exeter to develop on its own and in view of the capital cost escalation being suffered by similar large deposits bought out before the 2008 crash and the skepticism that $3–$4 copper is the new reality, Exeter will have a hard time attracting a buyout by a major in the near term. So, to create value while it bides time, the company is now focusing on developing a gold-oxide leaching operation to take advantage of the 1.4 Moz. resource sitting on top of this system.

TGR: Any other companies that could take advantage of the new pricing reality either in the gold, the copper or the silver area?

JK: Grade is very important in the gold sector. Last year Osisko (TSX:OSK) took over Brett Resources Inc. (TSX.V:BBR) and its Hammond Reef Deposit in Ontario, which is just under 1 g/t and about 7 Moz., at about $4. Now that the market is getting more comfortable with the idea of gold north of $1,200/oz., other similar low-grade projects are looking attractive.

Northern Gold Mining Inc. (TSX.V:NGM) is an example. The company's 700 Koz. Garrcon Project wasn't very interesting when gold was below $1,000/oz. But, at current prices, the company has an incentive to do step out drilling and lower the cutoff grade in an effort to boost that resource to a 2 to 4 Moz. Open pit mineable. This $40M market cap company could undergo a fivefold increase if Northern Gold triples the resource and delivers a positive prefeasibility study.

TGR: Are you saying that whether we are in a depression as some believe or a recovery as you have outlined, we've already seen the floor of $1,200/oz. for gold and these companies are a low-risk return investment?

JK: Not exactly. In the scenario where gold rises because the American economy is in a death spiral, the solution is to pursue a hyperinflation strategy that results in costs rising in conjunction with the price of gold. So, that is of no benefit to the companies. If the alternative is to just curl up in a fetal position and suck one's thumb and prepare for the end, that will result in gold prices going down. The best alternative for resource juniors is if the world avoids both a deflation-linked depression and hyperinflation scenarios, the American economy gets back on track with a revival of manufacturing on U.S. soil and the global economy continues to grow. That will be good for raw material demand and gold and silver prices.

TGR: Thanks, John. Enlightening as always.

John Kaiser, a mining analyst with over 25 years' experience, is editor of Kaiser Research Online. He specializes in high-risk speculative Canadian securities and the resource sector is the primary focus for an investment approach he developed that combines his "bottom-fishing strategy" with his "rational speculation model." Kaiser began work in January 1983 as a research assistant with Continental Carlisle Douglas, a Vancouver brokerage firm that specialized in Vancouver Stock Exchange listed securities. In 1989 he moved to Pacific International Securities Inc., where he was research director until April 1994 when he moved to the United States with his family. He launched the Kaiser Bottom-Fishing Report (now Kaiser Research Online) as an independent publication in October 1994 and developed it into an online commentary and information portal. He has written extensively about the junior resource sector, is frequently quoted by the media, and is a regular speaker at investment conferences. Since 2008 he has developed a focus on security of supply issues and how they relate to critical metals such as rare earths.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

DISCLOSURE:

1) Brian Sylvester of The Gold Report conducted this interview. He personally and/or his family own the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Timmins.

3) Ian Gordon: I personally and/or my family own shares of the following companies mentioned in this interview:Timmins Gold, Golden Goliath, Millrock and Lincoln. My company, Long Wave Analytics is receiving payment from the following companies mentioned in this interview, for receiving mention on my website, Golden Goliath, Millrock and Lincoln Gold.

The GOLD Report is Copyright © 2011 by Streetwise Inc. All rights are reserved. Streetwise Inc. hereby grants an unrestricted license to use or disseminate this copyrighted material only in whole (and always including this disclaimer), but never in part. The GOLD Report does not render investment advice and does not endorse or recommend the business, products, services or securities of any company mentioned in this report. From time to time, Streetwise Inc. directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.