The Effects of Freezing the Fed Balance Sheet

Interest-Rates / Central Banks May 20, 2011 - 10:22 AM GMTBy: Frank_Shostak

By the end of June, the expansion of the Federal Reserve's balance sheet is expected to come to an end. According to economic commentators, Fed officials are expected to initially hold the central bank's balance sheet steady — currently at $2.75 trillion — by reinvesting the proceeds from maturing Treasuries and mortgage bonds. Thereafter, these commentators believe, as economic activity starts to gain strength, Fed officials are likely to shrink the size of the balance sheet by selling assets.

By the end of June, the expansion of the Federal Reserve's balance sheet is expected to come to an end. According to economic commentators, Fed officials are expected to initially hold the central bank's balance sheet steady — currently at $2.75 trillion — by reinvesting the proceeds from maturing Treasuries and mortgage bonds. Thereafter, these commentators believe, as economic activity starts to gain strength, Fed officials are likely to shrink the size of the balance sheet by selling assets.

Most experts and Fed officials are of the view that freezing and thereafter reducing the size of the balance sheet won't generate much of a disruption to economic activity as long as the economy is on a sustained growth path. Most experts are also of the view that we are currently on such a path.

Note that for most economists the key is the strength of economic activity. Also note that the pace of economic activity mustn't be too strong in order to avoid igniting inflationary expectations and in turn the rate of inflation.

These economists attribute an economic swing, i.e., a boom-bust cycle, to various mysterious factors such as a sudden weakening in overall consumer spending and its subsequent effect on businesses' economic activity. As long as the economy is on a sustained growth path, various disruptive factors that cause boom-bust cycles can be contained — so it is held. This means that what is required here are capable Fed policy makers who will be able to successfully steer the economy toward the growth path of economic stability. It hasn't occurred to most commentators that the alleged defender of the economy — the Fed — is perhaps the main source of economic instability.

We suggest that the key to boom-bust cycles is the Fed's monetary policy. The so-called economy of Fed experts' models is nothing more than monetary turnover that (once deflated by a dubious price index) is labeled as real economic activity or real gross domestic product. As long as the pace of monetary pumping is accelerating, the so-called real economy follows suit. Once, however, the pace of pumping slows down, the pace of the economy's so-called expansion also declines (after a time lag).

Now as long as the state of the pool of real savings is still OK, i.e., as long as there are enough wealth generators to support wealth and nonproductive activities (bubble activities), Fed policy makers can get away with the impression that they are helping the economy. (Again, note that the more they pump, the larger the monetary turnover and hence GDP becomes.) Once the pool of real savings becomes stagnant — or worse, starts shrinking — the underlying real economy (the true real economy) follows suit. In this case it doesn't matter how aggressive the Fed's policies are: the economy cannot be revived. On the contrary, loose monetary policies will only make things much worse by diverting real funding from wealth-generating activities to nonproductive bubble activities.

Given the importance of real savings in the revival of the true real economy, it is astounding that most experts, including Nobel laureate Paul Krugman, are of the view that there is a need for QE3 to keep the economy going.

We suggest that once Fed policy makers freeze the balance sheet of the US central bank it will slow down the growth momentum of the Fed's balance sheet. Consequently, this is going to exert downward pressure on the growth momentum of the money supply. Note that ultimately it is fluctuations in the growth momentum of the money supply that set in motion fluctuations in the pace of formations of bubble activities. As a result, various bubble activities that emerged on the back of the rising growth momentum of the money supply will come under pressure — an economic bust will be set into motion.

Obviously it is possible to have a situation where commercial banks' expansion of lending "out of thin air" counters the freezing of the Fed's balance sheet. It remains to be seen whether this is going to be the case in the months ahead. For the time being, the Fed's balance sheet continues to expand at a rapid pace.

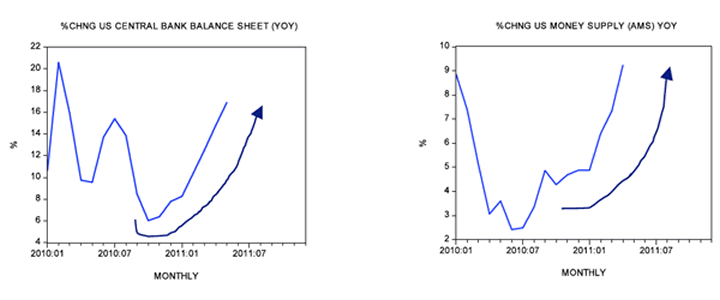

So far in May, the yearly rate of growth of the Fed's balance sheet stood at 16.9 percent against 14.8 percent in April. Also, the growth momentum of our monetary measure AMS displays a visible strengthening. Year on year, its rate of growth stood at 9.2 percent in April against 7.4 percent in the month before.

Now, we suspect that the difficulty the Fed has had in meaningfully "reviving" the economy so far could indicate that the state of the pool of real savings or the pool of real funding is in trouble. This means that even if the growth momentum of lending does currently show some strengthening (see chart) it is highly unlikely that, with the weakening of bubble activities on account of the Fed's freezing its balance sheet, commercial banks will pursue an aggressive expansion of credit out of thin air. Also, it is quite likely that with the freezing of the balance sheet, Treasuries will come under pressure, and the growth momentum of banks' holdings of Treasuries will weaken. This in turn will exert downward pressure on the growth momentum of total bank lending, which includes lending to the government.

Now, a visible strengthening in the growth momentum of the consumer price index (CPI) and the core price index (CPI less food and energy) may prevent Fed officials from introducing QE3 as suggested by some experts.

The yearly rate of growth of the CPI shot up from 2.7 percent in March to 3.2 percent in April. The pickup in the rate of growth of the CPI is yet to concern Fed officials, including Bernanke, who are of the view that this increase is of a temporary nature.

Some other experts have labeled the strengthening of the growth momentum as tame; they believe it shouldn't be of much concern. In fact most commentators are of the view that a little bit of inflation is great news, because it provides a buffer against deflation, which they regard as a terrible thing.

Most experts blame the increase in the CPI on oil prices and various other components of the price index, which they believe exert a temporary effect on the CPI. Nothing however has been said about the lagged effect of past monetary pumping by the Fed.

Remember that a price is the amount of money paid for a good. Hence, all other things being equal, it is not possible to have a general increase in prices without an increase in money supply. Based on this we can suggest that the yearly rate of growth of the CPI is likely to strengthen further in the months ahead.

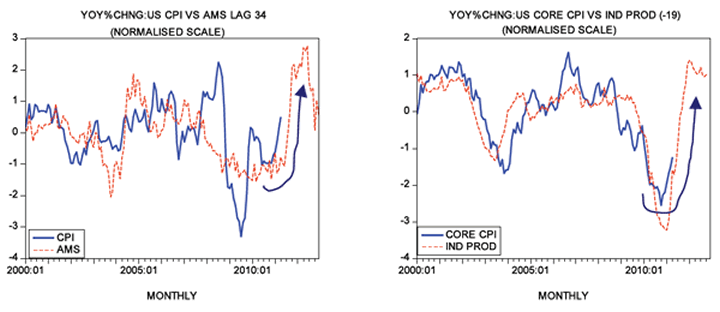

It will not surprise us if the yearly rate of growth shoots up to around 5 percent by year end. Now even in terms of the so-called core CPI, the rate of growth is showing visible strengthening. The yearly rate of growth stood at 1.3 percent in April this year against 0.9 percent in April last year.

We suggest that by year end the rate of growth could easily surpass the unofficial target of 2 percent (see chart).

Conclusions

Most experts and Fed officials are of the view that freezing and thereafter reducing the size of the US central bank's balance sheet is not going to generate much of a disruption to economic activity. We suggest that the key to boom-bust cycles is the Fed's monetary policy.

We suggest that once Fed policy makers freeze the balance sheet of the US central bank, the growth momentum of the money supply will slow down. As a result various bubble activities that emerged on the back of the rising growth momentum of the money supply will come under pressure. A visible strengthening in the growth momentum of the CPI may prevent Fed officials from introducing QE3 as suggested by some experts.

Frank Shostak is an adjunct scholar of the Mises Institute and a frequent contributor to Mises.org. He is chief economist of M.F. Global. Send him mail. See Frank Shostak's article archives. Comment on the blog.![]()

© 2011 Copyright Frank Shostak - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.