U.S. Economy Half Year Review, We Should Be OK, Except...

Economics / US Economy Jul 02, 2011 - 02:35 PM GMTBy: John_Mauldin

We are halfway through the year, and what a ride it has been. Today I will share my thoughts on what the next six months could look like, and endeavor to keep it short and simple, as we have a holiday weekend. There will be more than a few charts. What does the end of QE2 mean? What can we expect from Europe? Is a commodity bubble getting ready to burst? Is it really a bubble? There is a lot to cover.

We are halfway through the year, and what a ride it has been. Today I will share my thoughts on what the next six months could look like, and endeavor to keep it short and simple, as we have a holiday weekend. There will be more than a few charts. What does the end of QE2 mean? What can we expect from Europe? Is a commodity bubble getting ready to burst? Is it really a bubble? There is a lot to cover.

I recorded a PBS show a month or so ago, and it is airing this weekend on a number of stations around the country, so look for details at the end of the letter. Now let's jump in.

We Should Be OK, Except...

The economy should be in Muddle Through range (around 2% growth), absent any shocks. For instance, today we had the June ISM number, which was stronger than most analysts expected, at 55.3. There was a lot of whispering that it could dip below 50. Some of the internal components were a little soft, though. New Orders were barely above 50. And Backlogs fell below 50. Exports fell to the lowest level in two years (more on that below). Of the 18 industries surveyed, only 12 reported growth.

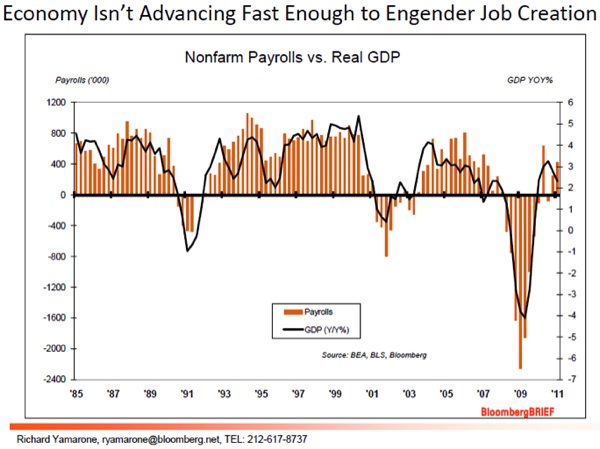

But Muddle Through is not going to allow us to really cut into the unemployment problem. We need at least 3% and most economists think we need to see 3.5% to result in some real strong jobs numbers for several months in a row. That just doesn't seem to be in the cards. Richard Yamarone at Bloomberg is calling for a recession by the end of the year, and he sent me a rather vivid PowerPoint of his latest thoughts. Let me share a few of those slides with you.

The following chart shows what I mean by Muddle Through not being enough to really cut into unemployment. As GDP seems to be slowing rather than picking up, the correlation between employment and growth is not encouraging. And if you look at the NFIB (National Federation of Independent Businesses) data, small businesses are not really back in the hiring game, and that is where the action needs to happen. We will see a new survey next week, but I doubt we will see a major jump in expectations.

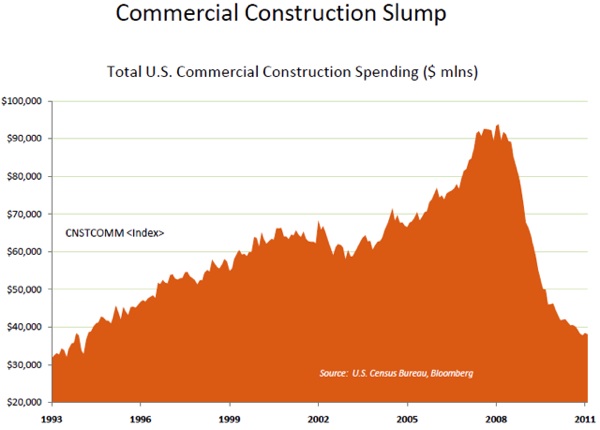

About two years ago I wrote a rather lengthy piece about why unemployment would be a problem until at least the middle of the decade. When you lose 8 million jobs, with about 2-3 million of those jobs permanently gone, it is tough to dig out of the hole. We can't look to housing construction to be the driving force that it once was for another 3-4 years, and commercial construction is falling.

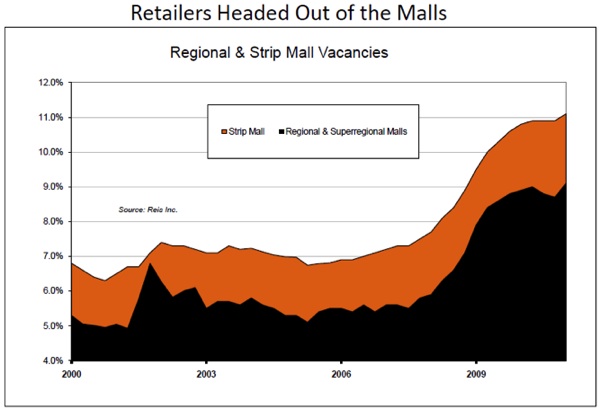

I was talking to a friend yesterday who is a director on two local bank boards. He pointed out that while the government wants banks to lend, the regulators (the Fed) are basically saying they can do development loans without very large equity components. They want 50% loan-to-value of very-reduced valuations. Let's look at two charts from Rich. One shows commercial construction and the other shows regional and strip mall vacancies. Construction spending for May 2011 fell 0.6% below its revised level in April, and is 7.1% below its May 2010 level. This is not the stuff that makes real estate moguls want to part with their cash. Nor does it bode well for construction jobs.

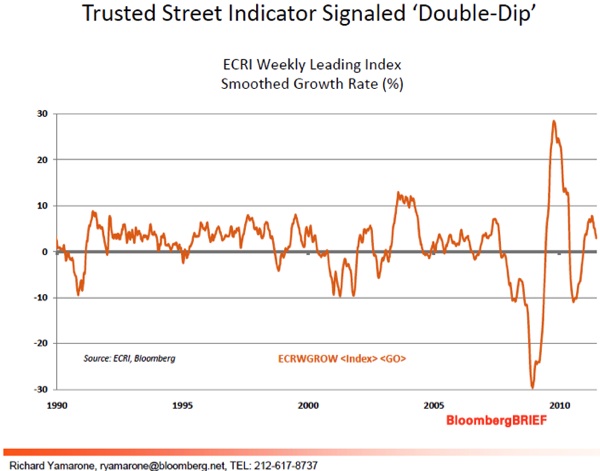

OK, only two more charts from Rich (Over My Shoulder subscribers can see the whole thing. More on that below.) The first is the smoothed ECRI (Economic Cycle Research Institute) index over the last 20 years. We can see it turning over. The ECRI weekly leading index decreased to 126.4 for the week ending June 24, from an unrevised 127. The smoothed, annualized growth rate fell to 2% from an unrevised 2.9%. The ECRI WLI has been consistently losing momentum in recent months, adding to concerns about the sustainability of the recovery.

The ECRI itself points out that their index is simply signaling a weakening economy but does not signal a recession. And you can see that there have been similar downturns in the past without a recession or even a recovery. But the recent trend is disconcerting and must be watched.

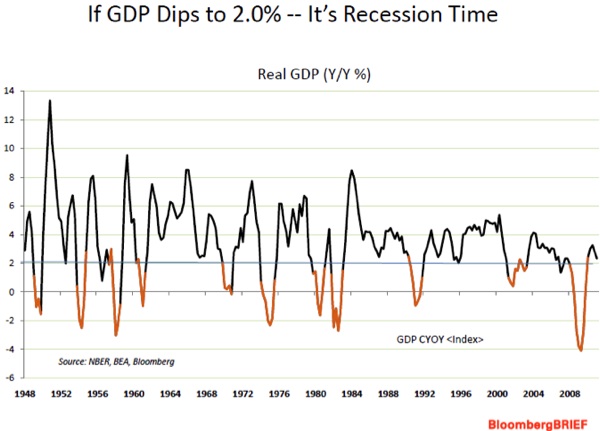

And the last chart is one I had not seen before, and is interesting. Rich notes that if year-over-year GDP growth dips below 2%, a recession always follows. It is now at 2.3%.

Growth is clearly decelerating. Look at the growth numbers from the St. Louis Fed website for the last six quarters:

2009-10-01 13019.012 2010-01-01 13138.832 2010-04-01 13194.862 2010-07-01 13278.515 2010-10-01 13380.651 2011-01-01 13444.301

It will be very interesting to see, at the end of the month, what the numbers are for the second quarter. Another quarter like the first quarter and we should either be close to or actually dip below 2%.

What Happens if There Is a Shock?

The problem with a slow-growth economy that is basically at stall speed is, if there is any type of "exogenous" shock, the economy can easily tip over into recession. There are several potential sources of a shock coming from the outside the US.

The first is from Europe. I have been writing about this for a very long time. It is the number one thing in my worry closet. We have dodged a short-term bullet with Greece and Europe coming to terms this week, but in late July they will have to find AT LEAST €50-70 billion more euros in loans and rollovers, and then more next year. Without projected asset sales it could reach €100 billion very easily. And willpower is waning on the part of creditor countries. Opposition against throwing good money after bad is increasing, as recent polls in Finland, Germany, the Netherlands, and Slovakia have shown. How long Merkel can hold her coalition together in the face of growing discontent is not clear. Powerful, authoritative voices in Germany are starting a daily chorus of chanting "no" to more bailouts.

And it is not just Greece. After Greece is dealt with, the Eurozone must deal with Ireland and Portugal. And the market is increasingly suggesting there is more risk there than the area can handle. Look at the graph below, which shows the steady rise of interest rates for Ireland and Portugal. This looks like Greece not so long ago. And Portugal now has higher rates than Ireland. This means that both countries are effectively cut out of the private market. (www.ifre.com)

Both countries keep saying they are not Greece, but the bond markets are not buying it. And as I noted last week, when Greece defaults, and they will at some point, the contagion to other countries will be quick and severe. And Spain will be included. The Italian bank index has been in free fall of late.

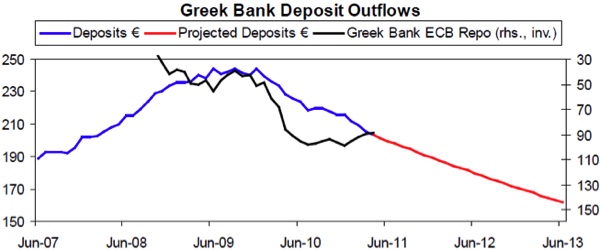

Money is flying out of Greek banks. Indeed, deposits in all the peripheral countries are falling. It is quite possible we get a credit or banking crisis in Europe before we get a sovereign default crisis. The longer Greece waits, the more they try and kick the can down the road, the worse it gets for their banks. And Greece has NO money to bail out its banks. Look at this graph from Bridgewater:

And quoting Bridgewater (one of the more brilliant sources of information in the world):

"While the focus is for the moment on the question of bridging Greece's immediate funding need, it's important not to lose sight of the bigger picture, which is that indebtedness is not the periphery's only problem, and is in many way only a symptom of the structural imbalances (extremely negative current account and budget deficit) that plague it. No amount of funding will change the fact that the periphery continues to be extremely uncompetitive; that in order to become competitive, it needs to become much cheaper; and that as long as it continues to be a member of the euro, the only way to achieve this is through sustained wage cuts and deflation that would need to be dramatically more extreme than the adjustments they've experienced thus far."

This could put Europe into a recession. And that is not good for US exports or for China. China is already in tightening mode. A hard landing is still too far away to call, but things could get softer, which will definitely affect commodity prices, which are already rolling over.

And Then There Was No QE

And as of today, the only QE will be that of the Fed taking the drawdown on its mortgage book and using it to buy Treasuries, which it has been doing. The markets are going to have to come up with $50 billion in bond purchases, and the recent auctions have not been all that good. I know the markets liked the ISM numbers, but a lot of the rise this week was quarter-end gaming by mutual funds and money managers. Let's see if there is follow through in July. The last time QE was stopped the markets swooned. That is only a data point of one, but it's all we have.

I think this is a very risky next six months. Maybe we avoid a crisis somewhere that affects the US and thus the world. If we do, if Europe can kick the can down the road another six months, then while a slowdown seems to be in the data, it is not yet suggesting a recession. I would be very careful about any long-only trades, whether it be stocks or commodities or bonds. We just don't know - there is less certainty than at almost any time I can remember.

"Endgame" Program

"ENDGAME: The End of the Debt Supercycle and How It Changes Everything," a program I recorded with McCuistion TV of Dallas, will air on Sunday, July 3, at 12:30 PM on KERA, Channel 13, Dallas, and also on other PBS stations around the country. You can also view the entire episode next week on the McCuistion website.

Tulsa for the 4th

My twins, Abigail and Amanda, live in Tulsa; and this year they have demanded that Dad come to them. It was their birthday last Thursday, so we will celebrate their 26th. Fireworks on the 3rd after the birthday dinner! For whatever reason, I do like a great fireworks display. Always have.

It seems like just a few months ago that we went to the Dallas Airport and saw them for the first time, at six months old. They grew up so fast. The picture below is from the cover of Twins magazine, sometime in 1987, I think.

Too cute, yes? And they grew up into such beautiful young ladies, both inside and out. One was Homecoming Queen and the other Senior Queen. One of the most touching moments in my life was when one of them won Homecoming Queen and the other just glowed with love and affection for her sister. Not a hint of jealously. I caught it in a picture, one of the few times that Dad actually had the camera in the right place at the right time. And Dad maybe had a moist eye or two. Dad is proud, and justifiably so.

As it turns out, my good friend Louis Gave of GaveKal married an Oklahoma girl, and her family lives about 90 minutes away from Tulsa on a lake somewhere in Oklahoma, where he visits his in-laws for month every year, with their four kids in tow. Brave man that he is, he has invited my clan to come over on the 4th for lake time and BBQ, and there was an enthusiastic "Yes" from the five of my kids who will be in Tulsa, plus spouses and other friends! So the Mauldin horde will descend on the Gave tribe and see just how much food they really have stored up for invasions.

Have a great 4th of July if you are in the US or celebrating as an expat in some remote locale. It promises to be a good one for Dad, and getting to spend time with Louis is a bonus. He is simply one of the smartest financial minds I know.

Your betting there are fireworks (hopefully not financial) in my future analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.