Money Printing, Debt, Dollar Vs Euro

Currencies / US Dollar Aug 24, 2011 - 03:47 PM GMTBy: Axel_Merk

A key reason for recent market turmoil may be the long overdue untangling of important debt-driven interdependencies between the U.S. and Europe. In our analysis, not only has the Federal Reserve’s (Fed’s) ultra-low monetary policy taken away any incentive to engage in meaningful reform in the U.S., but the easy money also spilled far beyond U.S. shores, providing European banks with hundreds of billions of reasons not to shore up their capital bases. With volatility riding high, investors appear to be chasing emotions rather than facts; let’s take a step back, and in an effort to understand where the Fed, the U.S. dollar and the euro might be heading next, let’s focus on facts rather than emotion.

A key reason for recent market turmoil may be the long overdue untangling of important debt-driven interdependencies between the U.S. and Europe. In our analysis, not only has the Federal Reserve’s (Fed’s) ultra-low monetary policy taken away any incentive to engage in meaningful reform in the U.S., but the easy money also spilled far beyond U.S. shores, providing European banks with hundreds of billions of reasons not to shore up their capital bases. With volatility riding high, investors appear to be chasing emotions rather than facts; let’s take a step back, and in an effort to understand where the Fed, the U.S. dollar and the euro might be heading next, let’s focus on facts rather than emotion.

The recent bout of volatility started when fears of renewed tensions in the Eurozone banking system erupted. The cost of funding for select institutions was on the rise. With memories of 2008, fears of a systemic shock, possibly the result of a bank failure, sent stocks plummeting. However, these challenges should not have come as a surprise. As we have learned over and over again, the players in this crisis are primarily motivated to act by market pressure, be that policy makers engaging in fiscal reform or banks bolstering their balance sheets. European banks have had a cozy relationship with their own regulators, as well as U.S. money markets, providing disincentives to get their acts together. Specifically, U.S. taxable money market funds, in search of yield, had been funding European banks by gobbling up U.S. dollar denominated commercial paper issued by these institutions. Only after criticism of this practice could no longer be ignored, including our June 22, 2011, analysis entitled “Euro: Safer than the U.S. Dollar?”, was the practice reduced. Institutional investors dumped their money market fund holdings; in turn, money market fund managers have reduced their holdings of commercial paper issued by European banks. As a reminder, these money market funds were holding massive positions, often substantially in excess of 50% of their net assets, in banks such as BNP Paribas, that in turn have billions of exposure to Greek debt.

Not surprisingly, the cost of funding for those European banks soared after being shunned by U.S. money market funds. The European Central Bank (ECB), as a response, announced on August 4, 2011, that it would once again open its six-month refinancing facility, providing unlimited liquidity to the banking system. What observers failed to realize was that this is not due to new problems, but due to old problems finally being addressed. Very helpful in this context was that the European stress tests released on July 15, 2011, have finally brought unprecedented transparency to the banking system by providing details of sovereign debt holdings of European institutions. It’s not about whether these tests were rigorous enough, but that the market is now able to “encourage” banks to raise more capital by, for example, shunning them from the inter-bank lending markets. Until then, the Fed’s policies have helped to cover up the weaknesses of the European banks affected. In fairness to the Fed, U.S. money market funds are part of what is called the shadow banking system, as money market funds operate outside of the supervision of the Fed. But money market funds have been chasing yields of riskier assets as a result of the low interest rate environment the Fed has imposed on the market; in an environment where Treasuries yield near zero (at times even less than zero), it puts strains even on the most conservative of investors.

Let’s keep in mind, though, that we are not in 2008. Since 2008, the remaining investment banks have converted to banking charters that give them access to central bank lending facilities. As a result, central banks are capable of keeping a banking system afloat, even if it were technically insolvent. All stakeholders should embrace the stress in the markets as an encouragement for further reform. Unfortunately, policy makers on both sides of the Atlantic are utterly slow to engage in urgently needed reform. In the U.S., with a “behaving” bond market, we are not even scratching the surface of what would put the U.S. on a sustainable fiscal path. In Europe, it’s perfectly understandable that Germany is pushing back against writing blank checks to bail out weaker countries, but we need more than speeches on closer fiscal integration. But don’t despair: the market will not wait. Think about it this way: any country that has asked for help from the IMF or the Eurozone had to give up sovereign control over their budgeting. Isn’t that exactly what German Chancellor Merkel and French President Sarkozy are calling for? The difference between what the market is imposing and policy makers are calling for is one of process: stressful periods are less stressful if sound institutional processes are in place. But even in the absence of such processes, the reform movement continues. It just happens to be a rather ugly and painful affair with plenty of political minefields.

Talking about these minefields: many have warned that policy makers might be voted out of office, potentially jeopardizing policies. Indeed, policy makers may lose their jobs, but that won’t change bond vigilantes: the language of the bond market is the only language policy makers appear to listen to. As a result, kick out one government and the primary consequence is that a new government now owns the same problem. In Spain, early national elections have been called for in November; odds are that the opposition will sweep to power, giving the new government, well, a way to accelerate reform.

We are not suggesting that these reforms will all be implemented to everyone’s, or even anyone’s satisfaction. However, we believe that the drama playing out in the Eurozone is one of process, an ugly process in which challenges are primarily expressed in the bond spreads in the Eurozone. In this environment, the Euro may strive, despite or possibly because of, all the pain, because less money is being spent than in the U.S.

There is also far less money printing in the Eurozone versus the U.S. In the U.S., we have no exit from “QE2”: all the money that has been printed remains in the system. What has changed is that words may count again, highlighted by the latest initiative by Fed Chair Bernanke. Since 2007, U.S. monetary policy has become ever more expensive, as rate cuts were followed by emergency rate cuts, followed by printing billions, then trillions. With the commitment to keep interest rates low until mid 2013, Bernanke has managed to depress interest rates with a statement rather than the printing press. While we strongly disagree with the policy, we must acknowledge this a major development. In many ways, Bernanke has doubled down on the Fed’s credibility. However, given that the Fed has rarely ever been accused of being too far sighted, I interpret the latest policy as just that: a policy for now, subject to change. Importantly, the Fed may continue to play with the “size and composition” of its balance sheet; if further action takes place, the Fed may first re-invest proceeds of securities it holds into longer-dated securities, to further depress the long-end of the yield curve. However, the most likely scenario, in our view, is that Bernanke will explain his recent actions rather than announce major new initiatives when he speaks at the annual gathering of global central bankers in Jackson Hole later this week.

By talking down interest rates, Treasury securities appear to offer unattractive returns to rational investors: negative real interest rates are being priced into the market. Similar to quantitative easing, this may provide further negative dynamics for the U.S. dollar, as investors are not getting properly compensated for the risks they are taking on. Bernanke, in our assessment, is employing the U.S. dollar as a monetary policy tool. Remember: Bernanke has even testified that going off the gold standard during the Great Depression, i.e. debasing the U.S. dollar, helped the U.S. recover faster from the Great Depression than other countries that held on to the gold standard for longer.

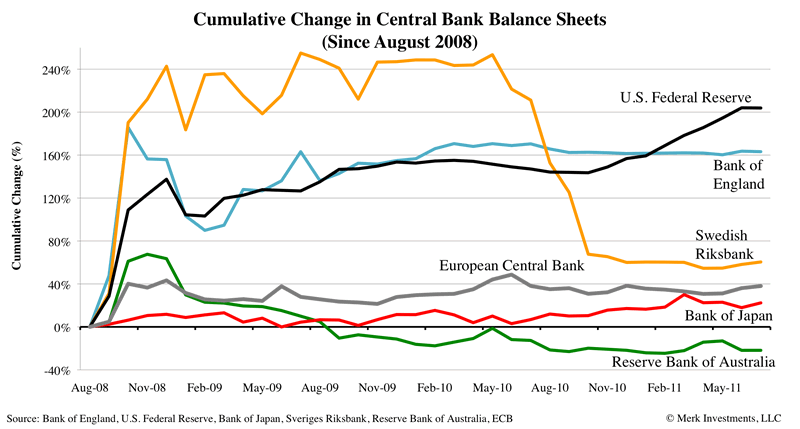

It’s in this context that we are negative on the dollar and positive on the euro: the Eurozone is on the other side of Bernanke’s version of the Great Depression trade. Indeed, while there’s been plenty of lamenting about ECB policy, the European Central Bank has printed a fraction of the money that the Fed has; the chart above depicts the growth of balance sheets (a proxy for the money that has been printed by the respective central bank) relative to August 2008.

And as far as the “behaving” bond market in the U.S. is concerned? The time may come when U.S. bond vigilantes will demand fiscal reform. The difference to the European experience is that the U.S. has to finance a current account deficit; as a result, the U.S. dollar may be far more at risk than the euro; in the Eurozone, the current account is roughly in balance. As the Japanese experience has shown, countries that don’t rely on foreigners to finance their deficits may experience strong currencies on the backdrop of economic stagnation.

In a nutshell, the U.S. is leading the developed world at spending and printing money. As a result, there may be no such thing anymore as a safe asset and investors may want to take a diversified approach to something as mundane as cash. Investors may be over-exposed to the U.S. dollar and may want to consider managing the currency risk of their investments more actively. We manage the Merk Absolute Return Currency Fund, the Merk Asian Currency Fund, and the Merk Hard Currency Fund; transparent no-load currency mutual funds that do not typically employ leverage. To learn more about the Funds, please visit www.merkfunds.com. Please sign up to our newsletter to stay in the loop as this discussion evolves.

By Axel Merk

Manager of the Merk Hard, Asian and Absolute Return Currency Funds, www.merkfunds.com

Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. Axel Merk wrote the book on Sustainable Wealth; order your copy today.

The Merk Absolute Return Currency Fund seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes.

The Merk Asian Currency Fund seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.

The Merk Hard Currency Fund seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability.

The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses.

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Axel Merk Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.