Beware of Floating Interest Rates

Interest-Rates / US Interest Rates Oct 26, 2011 - 11:07 AM GMTBy: Neeraj_Chaudhary

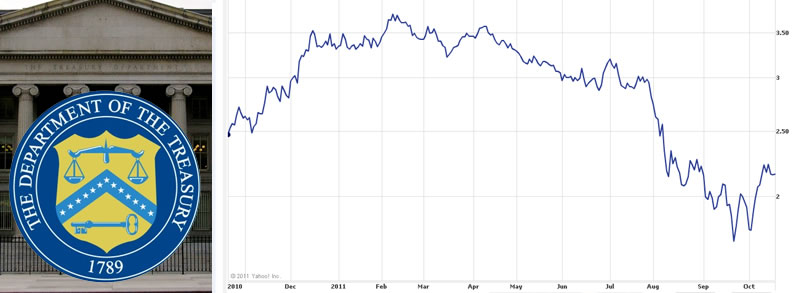

According to US government figures, the yield on the 10-Year US Treasury note reached a record low of 1.72% last month. Thus, despite the fact that government debt has exploded at a rate of more than $1 trillion per year, and the fact that S&P recently downgraded US debt, it appears that market demand for long-term US debt is nearly insatiable.

According to US government figures, the yield on the 10-Year US Treasury note reached a record low of 1.72% last month. Thus, despite the fact that government debt has exploded at a rate of more than $1 trillion per year, and the fact that S&P recently downgraded US debt, it appears that market demand for long-term US debt is nearly insatiable.

But in order to explain this seemingly irrational demand, some economists have suggested that bond buyers are preparing for a decade's long Japan-style deflationary era here in the US. In Japan, rates have been stuck below 2% for the better part of a generation. In such an environment, where economic malaise sucks the life out of stocks and other investments, ultra low interest rates are not enough to dissuade safety-seeking investors.

And yet, behind the scenes, private buyers may not be planning for lower long-term rates. Instead, they may be concerned that instead of falling, US interest rates will rise. If they do, investors who buy in at current levels, especially for longer maturity debt, could realize significant losses in their bond portfolios. That's because existing low yielding bonds fall in price when yields rise.

In February of this year, the Treasury Borrowing Advisory Committee (TBAC) - a group of banks that deals directly with the Fed, which includes JP Morgan Chase, Goldman Sachs, Bank of America, and other major financial institutions - asked the US Treasury to offer floating rate notes. This month - while US interest rates hovered near all-time lows - the Treasury agreed to consider the Committee's proposal.

Floating rate debt instruments reset periodically (often quarterly) in response to market rates. As a result, they can offer enhanced yield in a rising interest rate environment, which should provide greater price protection to buyers.

All things being equal, governments have no motive to offer floating rate notes. They would rather simply keep costs low by issuing a bond at current market rates, and then pay back the interest and principal on the agreed-upon schedule. Locking in low interest rates is one of the best incentives for governments to maintain a healthy balance sheet. It is the buyers of debt, who - concerned about the possibility for portfolio losses - seek to impose additional conditions before they are willing to loan.

So although the US government can at present issue 10-year notes at record low interest rates, private buyers are discreetly pushing for protection against rising interest rates. These buyers may be indicating their deep concern about the government's finances, and the distinct possibility that rates will in fact rise.

Incidentally, these are not just any buyers. In addition to buying government debt for their own accounts, TBAC members represent other major buyers such as banks, insurance companies, and pension funds, and also foreign investors who in recent years have bought as much as 50% of US debt.

In our 200+ year history - including the periods of World Wars One and Two, the Great Depression, and the inflationary period of the 1970s - the US Treasury has never offered floating rate notes. The mere fact that the US may go down this road should send a chill. Such an outcome should not inspire confidence in the world's largest bond issuer.

It is no accident that the governments in recent history that have been forced to issue floating rate paper read like a Who's Who of fiscal mismanagement and hyperinflation: Argentina during the mid-80s, Brazil during the mid-90s, Mexico and Thailand in the late 1990s, Venezuela throughout the 1980s and 1990s, etc. In fact, during the 1980s (in the wake of the Third World Debt Crisis), there was a period during which more than one in three new issues in the international bond market were of the floating rate variety.

Low US interest rates have lulled some into a false sense of complacency, believing that these yields indicate clear sailing in the US bond market. But even the most casual observer of economic conditions must acknowledge that no one - not an individual, a business or a government - can borrow nearly 10% of his income every year forever without any consequences.

We continue to believe that the United States is going down a path that will end in a bond market and currency crisis. And unless we change course, the consequences for every American citizen and every foreign holder of US debt may be severe.

Source: Yahoo Finance. CBOE Interest Rate 10-Year T-Note from October 2010 - October 2011.

For full access to the remaining articles in The Euro Pacific Global Investor Newsletter, please click hereto subscribe. For an in-depth look at the prospects of international currencies, download Peter Schiff's and Axel Merk's Five Favorite Currencies for the Next Five Years. Be sure to pick up a copy of Peter Schiff's just-released economic fable, How an Economy Grows and Why It Crashes. Click here to learn more and order.

Neeraj Chaudhary is an Investment Consultant with Euro Pacific Capital. Opinions expressed are those of the writer and may or may not reflect those held by Euro Pacific Capital, or its CEO, Peter Schiff.

Copyright © 2011 Euro Pacific Capital, Inc.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.