U.S. Economy Center Cannot Hold, Where Is My Return to the Mean?

Economics / US Economy Dec 18, 2011 - 01:08 PM GMTBy: John_Mauldin

Turning and turning in the widening gyre

Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world,

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.

- The Second Coming, by William Butler Yeats (1865-1939)

This coming week we shall likely see Congress pass an extension of the "temporary" payroll tax cut, first enacted as a stimulus to the economy in January of 2011. As I write, the extension is just for two months. We'll leave aside the politics and look at the economic implications of the extension, and then go on to examine the deficit in the US. That will give rise to some thoughts about Europe and what would have to happen for a country to leave the euro. We'll finally close with some thoughts and graphs about the more controversial part of the tax cut extension, the Keystone XL Pipeline. Just how radical is it to build such a pipeline in the US? And what are the implications for the deficit? I think looking at a few maps might surprise some readers. It should all make for a rather controversial letter, but then controversy is my middle name. (Note, this letter will print longer as there are lots of charts.)

But first, I want to thank one reader for helping to increase my reader base in a rather unusual way. I was sent this bit from a blog by Edward Ream today:

"I came across John Mauldin, http://www.johnmauldin.com, when someone left a printout of his blog in a railway carriage. His ‘Outside the Box' column is free to all.

"I enjoy his column, and I think some of you may enjoy it too. I especially admire his thirst for knowledge and his tolerance of diverse viewpoints. He actively seeks disconfirming evidence and the views of those who disagree with him. Imo, this stance is a model for what politics should be, and isn't :-) – Edward"

Thanks, Edward, and to whomever left the letter on the train. We take expansion of the number of our friends wherever we can find it. And let's see how he feels after this letter.

The Center Cannot Hold

The payroll tax, as a way to pay for Social Security, has been 12.4% since 1990, with half paid by workers and half paid by business. Late last year a temporary payroll tax cut of 2% was enacted. This saved an average family of four about $1,000 per year and affected 160 million taxpayers. It is not peanuts. It also "cost" about $120 billion in revenue (best estimates). This is about 0.8% of GDP. Remember that number.

Let's review the economic implications of tax policy. Depending on which academic study you want to use, tax increases or cuts have a "multiplier" effect of anywhere from 1 times (Harvard and Italy) to 3 times, the latter from Obama's former head of the council of Economic Advisors, Christina Romer, and her husband, both at the University of California Berkeley (not a hotbed of conservatism). Let's use 2 times as an average for our discussion, but you can adjust to suit your favorite academic study (you have read all those papers, haven't you?). Various studies show that spending cuts exert an effect for about 1 year before they are "absorbed" into the economy, and tax cuts take a little longer to have their full effect.

I think it likely that we will see that the US economy grew less than 2% in 2011, and probably closer to 1.5%. If there is a 2 times multiple on tax cuts, then the stimulus was worth anywhere from 1% to 1.6% of growth in 2011 (depending on your favorite academic paper), which is much of (and maybe most of) the growth we had in the US this last year.

As I write early Saturday morning, it looks like the payroll tax cut extension will only be for two months. This would mean that taxpayers may see a roughly $100 per month cut in take-home pay, starting in March. This means that the economy will take a growth hit starting in March. So why not extend it for a year? Or even two? Why not wait until the economy is stronger?

The problem is that the US fiscal deficit is about 8% of GDP. We already have a debt-to-GDP ratio of between 80% to 98%, depending on how you count intergovernmental debt and nonfederal debt. But let's use the lower number.

That means, if we do nothing about the deficit, in three years we are over 100%. We know (Rogoff and Reinhart and the BIS studies) that potential growth decreases above the level of 90% debt-to-GDP. We also know that as the debt grows, so does the cost of interest to pay the debt.

Let's run a thought experiment (for the purposes of simplification) on a country with a large debt of, say, 80% of debt-to-GDP and a deficit of 8%, with interest costs of about 2%. Revenues are 16% from taxes, and expenses are 24%.

First, that means that the debt carries an interest rate cost of about 1.6% of GDP, or around 10% of revenues. If the debt rises to 100% of GDP, then the interest costs will rise to about 2% of GDP, or about 12.5% of revenues. This will force spending cuts or tax increases if the deficit is not allowed to rise.

But wait. If we cut spending (also known in Europe as austerity), then we will see a negative tax multiplier of about 1.5% of GDP over that time period. That means it will be harder to grow our way out of the problem, especially if the economy is growing at less than 2% annually. Debt at the levels we are talking about makes it much harder to grow yourself out of debt.

Let's look at a paragraph from a very recent paper by the Boston Consulting Group entitled "What Next? Where Next?":

"The inability to grow out of the problem is bad news for debtors. Look at Italy, for example: Italian government debt is 120 percent of GDP. The current interest rate for new issues of ten year bonds is 7%, up from 4.7% in April 2011. If Italy had to pay 6% on its outstanding debt , such a high rate would materially increase the primary surplus (That is, the current account surplus before interest expense) that Italy would need to run in order to stabilize its debt level.

"If we assume that Italy's economy grows at a nominal rate of 2% per year, the government would need to run a primary surplus of 4.8% a year of GDP just to stabilize its debt levels; the latest forecast show only a 0.5% surplus for 2011. Any effort to increase the primary surplus through austerity and tax increases runs the risk of creating a downward spiral. When investors start doubting the ability of the debtor to serve its obligations, interest rates rise even further, leading to a vicious circle of austerity, lower growth and rising interest rates."

What if interest costs in our hypothetical country rose to 4%? That would mean that 25% of tax revenues (over time) would be consumed by interest. (Yes, I know, there is a lag effect. I am trying to keep it simple.) That means either further spending cuts or tax increases. Which leads to the vicious circle of austerity that the BCG writes about.

This is why Nouriel Roubini says that Italy is better off simply defaulting on its debt and reducing the overall debt by about 20%. The arithmetic says that Italy would be better off, as the hope of using spending cuts and tax increases (austerity) as their way out of the current problem is rather bleak.

And while we deal with the European problem in Endgame, we also note that the US risks becoming like Italy in a few short years.

Sounds extreme? Here's my reasoning. If you invest in developed-market sovereign debt, it is because you are seeking as close to risk-free returns as you can get. Who buys US debt looking for risk?

The bond market is going to watch the train wreck that is European sovereign debt, and the soon-to-be train wreck that is Japanese debt, and if the US does not show a clear path to a sustainable deficit by 2013, at which time our debt-to-GDP will be closing in on 100% (however you want to calculate it), and then I think the bond market will say, "We have seen how this movie ends in Europe and Japan. We are now watching the same movie in the US. If you don't mind, we'll leave at intermission."

Once rates start to rise, the options faced by the US are not good. Real spending cuts and tax increases in the midst of a crisis? Allowing the Fed (or essentially forcing it) to monetize the debt? There will be no good choices if we do not act.

Whenever the payroll tax cut extension goes away, it will mean an effective tax increase of the same magnitude of the tax cut. In our example, about a 1% to 1.6% hit to GDP. Think the economy is strong enough to handle that without going back perilously close to recession? As states and local governments are raising taxes by about 1% of GDP? As Europe implodes?

These are the headwinds I keep writing about. These tax cuts and increases make a difference in the short, 1-2 year term. Big time difference! Do you in effect hit the economy going into an election? But if not now, when? If we fail to get the deficit under control, we soon become Italy. Can we go another year? Sure. But the longer we wait, the fewer options we have. We are going to have to face the music at some point. Better to control it now!

The only way to do this is an economically rational way is wholesale restructuring of the tax code and restructuring of entitlements. We should consider replacing the payroll tax completely.

No room today to go into these solutions tonight (but we will later!) There are tax cuts and increases that have better multipliers. If you combine or substitute taxes that have bad multiples with those that have benefits, you can partially offset the effect of the spending cuts and tax increases.

There is a way. It will take a level of cooperation we have yet to see, or one party in total control of the process. And then it will take courage.

The US has no easy choices. Our choices now are merely very difficult. If we delay much longer, past 2013, our choices go to bad or very bad. Different in kind from those of Europe but not in difficulty or the quality of outcomes. We are edging closer to the Endgame.

We must combine the above with policies that create jobs. We must have growth as part of the solution. We can get through this in the US if we choose to. But the sense of urgency needs to get turned up.

Where Is My Return to the Mean?

Much of the Western world has been conditioned to a "return to the mean" paradigm for the past 60 years. Yes, there are recessions, but they are temporary lulls in a prevailing growth dynamic. The growth trend has been more or less inexorable. And we have become accustomed to it. Mainstream economic thought and forecasting are based upon the "past performance" that economic growth will resume. But lately that has not been the case. Economic growth after the credit crisis has been decidedly lackluster.

That return to the mean has gone missing of late. The reason is that we are coming to the end of the debt supercycle. Debt-fueled growth in the "developed" world is coming to an end as the cost of debt rises and the bond markets abandon one country after another, seemingly overnight. One minute debt is easy, the next it is hard to get.

Europe is coming to the make-or-break point rather rapidly. As noted last week, the recent summit did not solve the real problems. The distraction of the British veto served for a while to obscure the lack of any significant solutions. My friend Mohamed El-Erian, who is the CEO and co-chief investment officer of PIMCO, wrote rather alarmingly in this week's Foreign Policy ( http://www.foreignpolicy.com/articles/2011/12/15/downward_spiral) about the choices facing Europe. Remember, this is one of the most thoughtful and influential investors in the world. He knows he is sitting on the world's largest pile of bonds. He is not given to rash analysis (as is so often the case with your humble analyst, who sits on next to nothing). The following is raising eyebrows all over the world (emphasis mine!):

"It is critical for the welfare of billions around the world that Europe get its act together now. The continent faces an increasing probability of having to navigate a fourth potential morphing in the next few months. Should it materialize, this would take one of two forms:

"… either a disorderly and highly disruptive fragmentation of the eurozone, or the establishment of a smaller and less imperfect eurozone that has a different relationship with the rest of the EU.

"Both possibilities involve yet another set of immediate disruptions for Europe and the global economy. As such, the temptation among politicians will be to avoid making any active choices. But that would constitute a huge mistake. It would further reduce their future degrees of freedom due to an even narrower set of possibilities and, with that, erode their ability to influence outcomes.

"As time passes, the option of a smaller and less imperfect eurozone is becoming the only way to ‘refound' a union that would have the chance to stand the test of time and, thus, constitute a key component of medium-term efforts to restore global financial stability, meaningful economic growth, and plentiful jobs. It is not an absolute best, and it would be a messy process involving the risk of collateral damage and unintended consequences. Yet, when judged in terms of feasibility and desirability, it sure dominates the alternative of a full fragmentation."

The High Cost of Leaving

Let's think about what it means for a country to leave the euro (hat tip to Daniel Stetler of the Boston Consulting Group, from the paper I previously mentioned, augmented by a few of my own thoughts).

They would immediately have to impose capital controls. That means closing the border to prevent physical capital flight with piles of cash. And of course it means trade controls, or otherwise any company would rig the books to get as much cash out as possible. Extended bank holidays would be a necessity.

What would be the new official exchange rate? What would be the black market rate? Would euros be somehow marked as the new currency while they waited for the printing presses to spit out the new currency?

How would euro-denominated debt be handled? Not just country debt, which would be relatively easy, but business debt, much of which falls under UK law in Europe. What would it cost to recapitalize the banks? Who runs the stock market and in what currency?

Any sober thought given to exiting the euro, whether by your country or a neighbor, gives one considerable pause. This is what European leaders are so desperate to avoid, yet making the hard choices they now have in front of them is so very difficult. Austerity? That leads to a severe recession at a minimum, and in some countries to a long depression. Defaulting on the debt? That pushes austerity onto the bond holders and banks, which is another form of recession and depression.

How do you pay for those easily promised pensions and health care in such extremes? What about simple basic services? The chaos that will result from exit is more than most people can now imagine. While people may get nostalgic for "their" currency, to go back will not be easy. It will wipe out much of the savings of a generation.

That crisis will come to the shores of the US, and will reduce our GDP. I think it does so next year, pulling us into recession. That means revenues are down and costs are up. The deficit gets larger, not smaller. The costs of not dealing with the problem will mount with every passing month, here just as they do in Europe. Europe has kicked the can down the road, but it is coming to the end of that road. We are going down the same path unless we make the hard choices. The longer we wait, the harder the choices. Again:

"As such, the temptation among politicians will be to avoid making any active choices. But that would constitute a huge mistake. It would further reduce their future degrees of freedom due to an even narrower set of possibilities and, with that, erode their ability to influence outcomes."

Must we wait until a crisis forces the hands of politicians? Not just in the US, but throughout the developed world?

I fear, as Yeats wrote in 1919, that "the center cannot hold."

Some Quick Thoughts on the Keystone XL Pipeline

Given what we have discussed above, the need for economic growth is going to become imperative in the Western world in general and the US in particular, as we strive to overcome our massive debt burdens. And while we are thinking of unintended consequences, it is useful to remind ourselves that for a country (the public sector) to balance its budget while at the same time its private sector is deleveraging, it is necessary to reduce the trade deficit or even run a surplus. While I go into this in great detail in Endgame, the basics are simple. Quoting myself briefly:

"The desire of every country is to somehow grow its way out of the current mess. And indeed that is the time-honored way for a country to heal itself. But let's look at yet another equation to show why that might not be possible this time. It is yet another case of people wanting to believe six impossible things before breakfast.

"Let's divide a country's economy into three sections: private, government, and exports. If you play with the variables a little bit you find that you get the following equation. Keep in mind that this is an accounting identity, not a theory. If it is wrong, then five centuries of double-entry bookkeeping must also be wrong.

"Domestic Private Sector Financial Balance + Governmental Fiscal Balance - the Current Account Balance (or Trade Deficit/Surplus) = 0

"(By Domestic Private Sector Financial Balance we mean the net balance of businesses and consumers. Are they borrowing money or paying down debt? Government Fiscal Balance is the same: is the government borrowing or paying down debt? And the Current Account Balance is the trade deficit or surplus.)

"The implications are simple. The three items have to add up to zero. That means you cannot have surpluses in both the private and government sectors and run a trade deficit. You have to have a trade surplus." (You can read more about this in my letter at ( http://s.tt/133tk) or in the book Endgame, in chapter 3.)

Thus the problem of Greece, with its massive trade deficit and huge fiscal deficit. They have no choices but default or depression.

The US has two main sources of its trade deficit: energy and China, in roughly equal proportions. If we reduce our energy dependence, we can get the trade deficit below 2% of GDP.

The China problem is not simply one of reducing our trade deficit with China, as much of what China makes and sells to the US is sourced in countries outside of China. While the final manufacture is perhaps in China, the bits and pieces come from other parts of Asia. The true cost of a product from China is less than 20% actual Chinese value added. An example is the Apple iPhone, which is assembled in China but whose most costly components come from elsewhere in Asia. Direct Chinese costs are less than 4%, but the entire amount is "attributed" to China in calculating the trade deficit. See http://voxeu.org/index.php?q=node/6335.

The real problem is the demand in the US for cheaper goods. If the US were to pass a tariff on Chinese-manufactured goods, then production and buying would shift to other countries without the tariffs. Markets look for the lowest-price source. For a tariff to be truly effective, it would have to be on the product and not the source country. And the only way to do that is to start a trade war. That is typically not a good way to promote free markets and general prosperity. Think Smoot-Hawley in the 1930s.

On the other hand, the US can do something about its energy dependence. We are blessed with abundant energy, if we simply exploit it in a responsible manner. And doing so would directly create hundreds of thousands of jobs, many of them quite high-paying, and many more hundreds of thousands of jobs servicing those employed and their companies.

Which brings us to the rather strange case of the Keystone XL Pipeline project. For non-US readers, this is to be a 1,700-mile pipeline designed to connect Canada's oil production in the province of Alberta with the US Gulf Coast. The various government agencies of the current US administration approved the project, after exhaustive environmental impact analyses. President Obama overruled his subordinates, postponing a decision until 2013, after the next election. Even though labor unions (normally thought of as Democratic and Obama allies) actively supported the project (as it means lots of jobs), various environmental lobbies were against it, and Obama apparently gave into them. (That is not just my opinion, but widely assumed, even by Democratic supporters.)

This issue has raised a few questions from international readers, wanting to know why so many people (the large majority of US voters, if polls are right) are seemingly willing to hurt the environment simply for the purpose of transporting oil. Wouldn't a new pipeline create a whole new host of environmental dangers? What were we thinking?

As it turns out, a new pipeline is not all that radical. If you drive in the US, you cannot go ANYWHERE for any length to time without crossing dozens of pipelines that already exist, especially in the corridor where they want to build the Keystone XL pipeline.

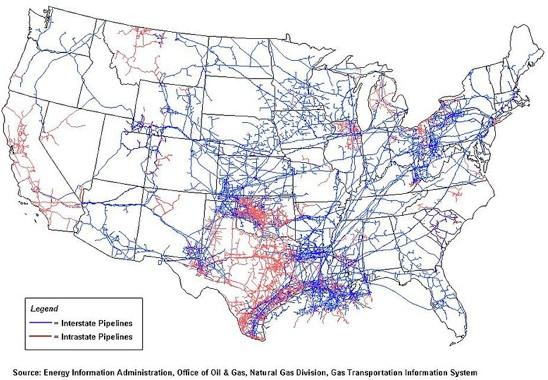

Let's look at two maps. The first is a map of natural gas pipelines in the US. To say it looks worse than your grandmother's varicose veins is no exaggeration. It is hard to find a state that does not have a natural gas pipeline. Without them the US would simply come to a grinding halt. (The source for this map is a governmental agency, the US Energy Information Administration.)

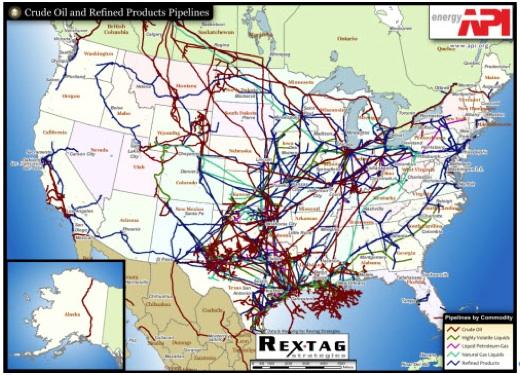

The next map is just the major oil pipelines. If you were to add in all the small (8-inch or less) lines connecting minor oil fields, you could not distinguish between the lines in certain areas, as we will see in the third chart.

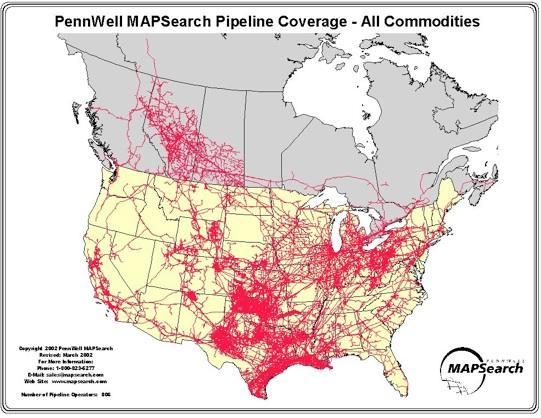

This next chart I throw in because it also shows the rather extensive pipeline system in Canada. This chart combines commodity pipelines of all kinds. The point is that we have the technology to build pipelines safely and in an environmentally reasonable way. When was the last time you heard of a serious pipeline disaster, or even a small one? Yes, the BP oil rig certainly comes to mind, but that was human error and not the fault of technology. Just as the large majority of airplane accidents are pilot error, you do everything you can to minimize the impact, and require safety procedures. But people screw up every now and then.

This is not to dismiss the problems and environmental concerns of drilling for petroleum products, or mining for various minerals. There needs to be strict controls on all such activities, with real penalties. You can see from the maps that my home state of Texas has a lot of pipelines and wells. The problems with pollution in the early development phase here in Texas were well-known. Now there is a very aggressive and popular regimen of control of drilling and transportation of oil and gas. We have to live next to the wells and pipelines. No one wants their water or land destroyed.

Now, let's circle back to the Keystone Pipeline. We started this section with a reference to trade deficits. And this is Canadian oil, not US oil. So it does not help our trade deficit directly, although a large portion of US dollars that go to Canada come back to the US. Canada is far and away our largest trading partner and major energy supplier.

The problem is that the opposition is mainly of the "I don't like any carbon-based energy" variety. Whether it is coal or oil or natural gas, it is not as "clean" as solar or wind.

The problem is that solar and wind simply cannot produce enough energy without huge government subsidies, at least with current technology (although that will change over time). In the meantime, if we want to balance our budget in the US (and we must!), we are going to have to become energy independent as one part of the solution. In the short term (10-15-20 years), that means carbon-based energy. If we can produce our energy in the US, and we can, then why not create the jobs here rather than elsewhere, if jobs are our #1 political concern, as they seem to be, according to the polls? Further, in the short term, as Mexican production is falling rather fast, we are going to need that Canadian oil if prices are not going to rise.

(Note: in my book, I actually call for a slowly rising energy tax on gasoline usage, to be solely used for rebuilding our decaying infrastructure, so I am not against higher prices per se. I just want the reason for higher energy costs not to be shortages. But that's another story for another day.)

In the "payroll tax cut" bill that will be passed in a few days here in the US, Congress will require the President to make a decision by the end of February on whether to allow the Keystone project. I hope they do pass it, and I hope he does decide to allow it.

But let's not think that this one more pipeline is going to destroy the environment of the US. It might create competition for some US producers, but if you can't live with competition then you're in the wrong country.

The US is in a very deep hole. We need to stop digging and start figuring out a way to climb out. The world is sadly going to see what happens when Europe has to resolve its current crisis, one way or another, and what that will mean for world GDP growth. Then, I am afraid, Japan will be the next crisis in waiting.

The world can ill afford for the US to be the third major economy to implode. The world is far too connected to shrug off such problems.

Look Over My Shoulder for Forecast 2012

I have started to seriously research my annual forecast issue, which I will do the first Friday of January. I read more for this issue than any other single piece. This last year, I have offered a new service called Over My Shoulder. Subscribers get access to 5-10 (sometimes more) pieces I read each week that I think are particularly thoughtful and important – material that is not usually available through your normal sources.

For the next few weeks, I am going to post most of what I read as I research my forecast issue. You can look Over My Shoulder for $39 a quarter. Where else can you get someone to read for you, and filter what he reads, and let you know what's important. From sources you won't see in most places. You can learn more and subscribe at http://www.johnmauldin.com/overmyshoulder/recent/ .

LA, NYC, Hong Kong, and Singapore

"When sorrows come, they come not single spies, but in battalions."

The last few weeks have been a little more stressful than normal. These times come and go, of course, and eventually I return to my own mean. I really am an optimist at heart. Yet, perhaps the tumult of the time is why my letter may be more bearish than usual tonight. But events do give one pause for introspection, and an acknowledgement that whatever control we think we have is transitory and illusory.

But even as I work through my "stuff," I look around at people who are dealing with so much more and realize I am so very lucky, the most blessed of men. Family, friends, and a meaningful life. A really well-made sandwich. What more can one ask?

But whatever, I leave in a few hours for LA, where I will be with Rob and Marina Arnott at their boat-parade-watching party in Newport Beach. And Jay Abraham is going to come, as well. I will see lots of friends and gain some insight into what matters. And then it's on to New York and meetings and more friends, then back home until the 10th of January, when I am off to Hong Kong and Singapore for 11 days.

It is late and past time to hit the send button. I have to get up in just a few hours and need some sleep. Have a great week. And take some time to spend with those who mean the most to you. Don't let the sturm and drang of the holidays make you miss what is important.

Your dealing with the drama analyst,

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.