Gold for Preserving Wealth Not Creating Wealth According to Warren Buffett

Commodities / Gold and Silver 2012 Apr 15, 2012 - 07:56 AM GMTBy: Brian_Bloom

The link below will take the reader to a summary of a report by Warren Buffet to shareholders of Berkshire Hathaway. In it, he implicitly makes the point that investors may be regarding gold with too much emotional attachment. http://www.businessinsider.com...

The link below will take the reader to a summary of a report by Warren Buffet to shareholders of Berkshire Hathaway. In it, he implicitly makes the point that investors may be regarding gold with too much emotional attachment. http://www.businessinsider.com...

I think that the most significant point Mr Buffett makes is that “wealth creation” is a function of building businesses that satisfy market needs/demands. Businesses are living, breathing multi-cellular organisms that create value regardless of what the stock market is doing.

From my perspective he is not saying that gold is “bad”. He is saying that if you want to “preserve” wealth, then gold is okay but if you want to “create” wealth then sitting on a pile of gold won’t help you do that. Another observation, if I understood him correctly, was that too many people are buying gold nowadays because they are motivated to “add” to their wealth. Too many people are buying gold because they think a “greater fool” will pay them a higher price than they paid.

I agree with this observation. It’s a mindset issue. If, for the sake of argument, gold was merely a commodity and not a currency then, when it outperforms commodities, that excess performance would flow partly from speculation and partly from relative demand/supply forces. But “real” (volume) demand for gold seems likely to slow over the coming years as less real wealth is created in a slowing global economy (i.e. less real wealth will be available to invest in gold) and supply is likely to keep growing as new mines open. That, essentially, is why I think that the gold price is due for a strong correction. Have a look at the relative strength chart below, courtesy stockcharts.com (Gold divided by commodities). Since 2006, a sort of hysteria has been building and the “ratio” has almost quadrupled – from slightly over 150 to slightly less than 600.

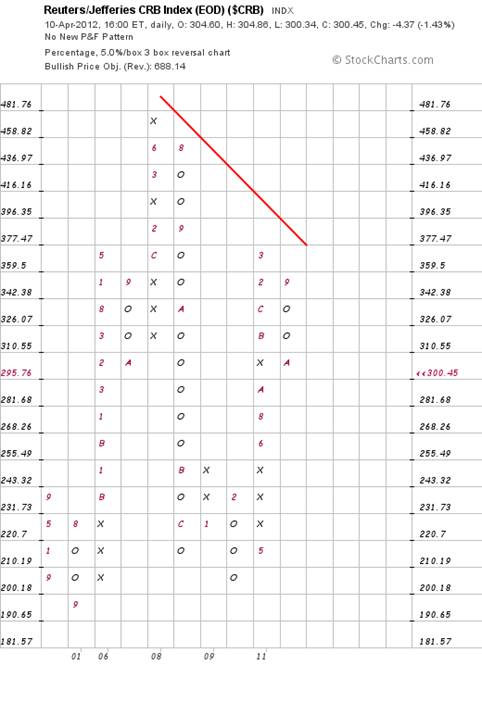

Based on the “pure” commodity chart below (courtesy stockcharts.com), the commodities index has risen in price since 2001 from 231 to 304 – that’s a compound growth rate of 2.5% p.a. and the lower growth rate probably flowed from “relative” abundance, as will be examined later in this article.

Now let’s look at the counter argument in relation to gold:

If, for the sake of argument, gold was a “currency” then it should “hold” its value against paper currencies – i.e. as the volume of paper currencies rise, so the gold price should rise proportionally.

The fact is that M2 money supply in March 2001 was $5 trillion, and in Feb 2012 it was $9.8 trillion. (source: http://www.federalreserve.gov/releases/h6/hist/h6hist1.htm )That’s a compound growth rate of 6.3% p.a.

Whilst the stock of money has been rising at a higher compound growth rate than commodity prices, production of commodities has also been compounding – so, from a “demand” perspective, more money has been chasing more goods. That’s one reason why the prices of commodities have not kept pace with money supply. Another is that because of greater productivity, we need a lower quantity of commodities to do the same job as before. For example, cars nowadays get a higher number of kilometres per litre of fuel.

By contrast, gold production hasn’t gown as quickly as that of other commodities so, relative to paper currency, its price had to rise more than other commodities. But, as I understand Mr. Buffett, he thinks that the gold price has run too far. If he is correct (and I think he is) then gold must correct in price WITHIN THE CONTEXT OF A CONTINUING BULL MARKET FOR AS LONG AS GOVERNMENTS CONTINUE TO PRINT MONEY.

(Author note: Because the US Dollar has been the default international currency, I have used US M2 statistics as a proxy index for global statistics. Of course, this is not necessarily true but it is the principle on which the reader needs to focus. )

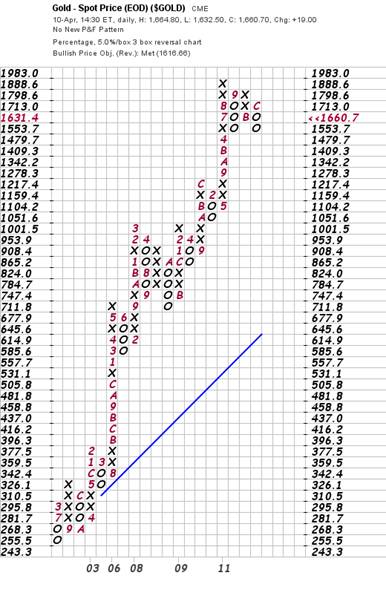

In fact, the gold price has risen from about $300 an ounce to $1660 an ounce in the same time period. That’s a compound growth rate of 16.76% p.a.

By contrast, if gold was rising in price to compensate for actual growth rate of the money supply at 6.3% p.a. then it should have risen from $300 to $591 an ounce. But let’s not jump to conclusions. Arguably, the market is looking forward and is anticipating a compound growth rate of money supply that is much higher than it has been historically. But even if the growth rate in future is (say)10% p.a. and, looking backwards, had been 10% p.a. from 2001, then the price today would only have been $855.

For gold to fall to the technical target level of $1109 (as is being indicated by the 3% X 3 box reversal Point-And-Figure chart shown in my article of last week), this implies that money supply growth rate will need to accelerate to a level where compound growth rate from 2001 will have been 12.62% p.a.

Based on these numbers, there has clearly been an element of speculation – flowing from the assumption that the world is heading back towards a gold standard; and that gold will become the world’s currency of last resort with all existing paper money backed by some ratio of gold. Frankly, for reasons that I have articulated many times, I think that such an outcome is not practical. It is an expectation that is based on theoretical reasoning that does not take reality into account. The reality is that industrial demand for gold will grow over time and, relatively speaking, gold will become even scarcer.

Financial authorities cannot dictate that gold may not be used for industrial purposes. What if the growth in the amount of available gold (available for currency purposes after industrial demand has been satisfied) slows down to be lower than growth in population? Will that mean that money supply per capita will shrink? Are we aspiring to build “deflation” into our economic management toolbox? All this talk about gold being a currency of last resort is, in my view, nonsense. But it doesn’t follow that gold is not valuable. It merely means that the gold price is currently in a bubble (that may or may not expand further; i.e. the “risks” are growing) and it needs to correct – within the confines of a continuing bull market.

So, after it corrects to wash out the speculative element, if governments are predisposed to continue inflating the money supply – which is what the Fed has been doing – then gold will allow you to stand still without having to get on a treadmill. But Mr. Buffet’s point is that no-one got rich by standing still. Ergo, you need to already have wealth to aspire to own gold.

Where I am predisposed to disagree with Mr. Buffett is that this central bank predisposition to deliberately create monetary inflation is a “growth” oriented approach to building an economy. His thought processes are geared to inflation – as are the thought processes of the gold bugs. In my mind, the world economy will not survive in the longer term if it continues to be “growth” focussed. As climate change is demonstrating, there is a new dynamic out there. The “environment” is not the benevolent cornucopia that it once was. We need to stabilise global population numbers (which might take 20-30 years), and, in doing so we need to start thinking in terms of a stable economy where people can improve their standards of living only if they add value. An implication of this is that speculative trading will become irrelevant and those who do not add value will remain poor, because the gross size of the pie will not grow. On the other hand, the net size of the overall pie will likely keep growing because costs will fall through improved productivity and greater efficiency in usage. Therefore, overall standards of living can continue to grow – for those who add value.

Of course, if the gold price was being suppressed in the years leading up to 2001, then the target price (fundamentally) of gold might be higher than the range of $591 - $855 that is discussed above. For example, if the starting number “should have” been (say) $600 (for ease of discussion) then the current number should be somewhere between $1200 and $1700. Either way, further upside in the gold price is limited

In my mind, both the charts and the fundamentals are in alignment. The charts are (subtly) calling for a correction in the price of gold and I believe them. Warren Buffett’s logic only served to reinforce my view that gold should not be thought of as a “currency”. It is a commodity that will grow significantly in fundamental value over time.

In my forthcoming factional novel, The Last Finesse, I suggest how gold might play an important contributory role in a new era of financial discipline. Via the book’s storyline, the rationale of how gold can form part of a solution (but not the entire solution) is laid out for even the lay person to understand. A long term “real” price of around $2,000 an ounce seems reasonable to me, but the gold price might churn at around these levels for up to a decade.

In closing, there are some who will remember that Mr Buffett bought a large quantity of silver some years ago and will argue that, therefore, he is speaking with a forked tongue. I think the reason he bought silver was, quite simply, that he thought it was underpriced. It should be born in mind that at the time that he bought it he paid somewhere around $5 an ounce and it is now trading at over $30 an ounce. Things change and our thinking needs to adjust to the reality of that change.

In all my published articles – and in both my books – my main thrust has been this: Precisely because life is dynamic, one needs to avoid “dogma” in all decision making – not only in financial decision making. I have recently been reading an article on “wisdom” in corporations, and here is a relevant quote (Source: http://econpapers.repec.org/... ):

“Embeddedness is an important systems principle: problems cannot be isolated from the systems in which they are located, or embedded; the system, itself is nested within a larger context that must also be understood and, perhaps, changed for viable problem resolution (Devine,2005; Keating et al, 2001.). This explains why holistic approaches to problem analysis and intervention are more likely to succeed in complex environments than formulaic ones (Clayton and Gregory, 2000; Sice and French, 2006) while also accepting that problem diagnosis or analysis is more challenging”

The bottom line is this: The world in which we live is a highly complex system of which the economy is a complex subsystem. The mountain of global debt is one symptom (there are other symptoms) of imbalances in both the system and the subsystem. Honing in on a gold standard as the way to redress these imbalances is a formulaic approach which has a low probability of success. To solve our problems, we need a holistic approach, not sound-bite cleverness, or even the charisma to sell facile, clever sounding, sound-bite solutions. In short: We need “wisdom”.

Personally, I am prepared to accept that the world’s most successful investor has a modicum of that wisdom. When he expresses a view on something as important as the gold price, I am prepared to stop and listen carefully to what he is saying. Warren Buffett is not a stupid man.

Brian Bloom

Author, Beyond Neanderthal and The Last Finesse

In the global corridors of power, a group of faceless men is positioning to usurp control of one of the world’s primary energy resources. Climate change looms large. Can the world be finessed into embracing nuclear energy? Set in the beautiful but politically corrupt country of Myanmar, The Last Finesse, through its entertaining and easy-to-read storyline, examines the issues of climate change, nuclear energy, the rickety world economy and the general absence of ethical behaviour in today’s world. The Last Finesse is a “prequel” to Beyond Neanderthal, which takes a right-brain, visionary look at possible ways of addressing the same challenges. The Last Finesse takes a more “left brain” approach. It is being published in all e-book formats.

Copyright © 2012 Brian Bloom - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Brian Bloom Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.