Currency Wars: Gambling With Other Peoples’ Money

Politics / Global Debt Crisis 2012 Apr 20, 2012 - 12:28 AM GMTBy: Axel_Merk

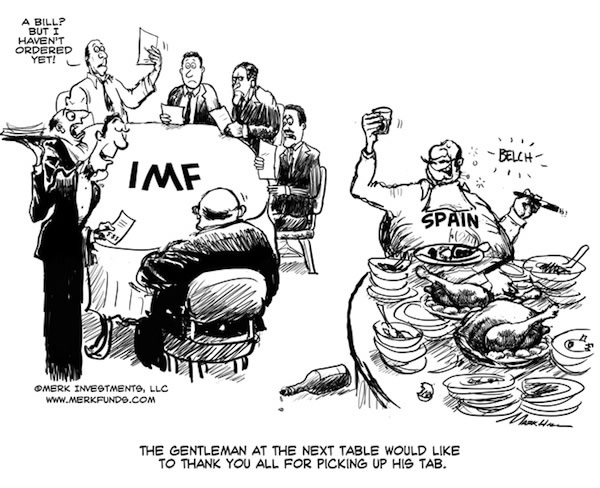

If running out of your own money wasn’t bad enough, policy makers are increasingly spending other peoples’ money to bail their country out. At the upcoming G-20 meeting, finance ministers from around the world will contemplate an increase to the resources of the International Monetary Fund (IMF). At stake for politicians is whether they can continue to do what they know best – to play politics. In contrast, at stake for investors may be whether currencies will retain their function as a store of value.

If running out of your own money wasn’t bad enough, policy makers are increasingly spending other peoples’ money to bail their country out. At the upcoming G-20 meeting, finance ministers from around the world will contemplate an increase to the resources of the International Monetary Fund (IMF). At stake for politicians is whether they can continue to do what they know best – to play politics. In contrast, at stake for investors may be whether currencies will retain their function as a store of value.

Let’s highlight Spain, as the country may be the key to understanding how dynamics may play out. Last November, Spaniards voted for change by electing conservative Prime Minister Rajoy, handing him an absolute majority in parliament, displacing the previous, socialist government. The election may cause former British Prime Minister Thatcher to change her view, that socialism is doomed to fail, as ultimately you run out of other people’s money. It doesn’t take a socialist to run out of money. In the case of Spain, if you run out of your own people’s money, there may always be other peoples’ money.

One of the major concerns is Spain's regional government debt. Spain consists of 17 autonomous regions, whose total debt almost doubled in the past three years, due to economic recession and a housing market collapse. In many ways, Spain reflects a microcosm of how the Eurozone as a whole is structured:

•Spanish regions have the power to issue public debt. The central government has little ability to interfere with regional government spending and is prohibited by Spanish law to bailout regional governments.

•While regions enjoy high autonomy on spending, the central government retains effective control over regional government revenue.

•Spain has its own peripheral problems: the most indebted region, Catalonia, recorded 20.7% debt-to-regional-GDP ratio and 3.6% deficit-to-GDP ratio in 2011. Its 10-year bond yield recently breached 10%, far beyond the yield on 10-year Spanish government bonds, which yield around 6%. In 2011, the total debt of 17 regional governments rose to €140 billion, accounting for 13.1% of Spain's GDP. This number is up from 6.7% by 2008.

•Spanish law forbids the central government from rescuing regional governments (in much the same way that the Maastricht Treaty prohibits bailouts of EU countries). In practice, the central government appears to have implicitly helped Valencia, Spain’s 2nd most indebted region, with a €123 million loan repayment to Deutsche Bank.

More broadly known are Spain’s banking woes. Unlike much of Europe, a housing boom propelled much of Spain’s recent growth, causing Spain’s regional banks, in particular, to become overly exposed to the mortgage sector. Spain’s banks are very dependent on liquidity provided by the European Central Bank (ECB). The recent 3 year long-term refinancing operation (LTRO) by the ECB at first took pressure of the Spanish banking system, but has since been seen more critically, as Spain’s banks may be using the liquidity to buy Spanish government debt, thus increasing inter-dependency and potentially making nationalization of Spanish banks (read: the Spanish government taking on the obligations of its banks) more, rather than less likely.

The tensions between Spanish regions and its national government are nothing new. And that’s really the main lesson here: it’s business as usual in Spain! As of late, Rajoy’s government appears to be reining in regional control over budgets in earnest. However, Spaniards are used to eternal debates on where subsidies should come from, how to stop regions from spending, and – conversely - how to find ways around restrictions. In brief, Spaniards are pros at this battle. Not surprisingly, when there’s a threat of market headwinds, Rajoy is publicly committing to reform. The moment the pressure abates, it appears those promises are forgotten. Spain is proof that the only language policy makers may be listening to is that of the bond market.

As painful as it is, volatile markets are necessary to keep policy makers focused. Whenever Spanish bonds come under pressure, Spain moves further from talk and closer to action, with respect to implementation of more austerity measures, as well as the pursuit of structural reforms. Spain – like so many developed countries – has rigid bureaucracies aimed at protecting the old (companies and employees) at the cost of preventing the new, stifling innovation and fostering massive youth unemployment. Structural reform is politically painful. What is striking about Spain is that it has an enviable position of a government with an absolute majority. Yet, even such a seemingly strong government is dragging its feet in implementing reform. In the process, political support is eroding, thus making it increasingly difficult to pursue reforms as the economic environment worsens.

Politicians always appear to consider the cost of acting versus the cost of inaction. As long as more money is lined up: be that from the central government for the regions; be that from a European stability fund for the government; or be it from the IMF, incentives for reforms are taken away. In many ways, Catalonia should be getting the message that its budget is unsustainable, but with help on the way from Madrid, the region may continue its bad habits.

As Europeans have convinced themselves that they have done plenty of the heavy lifting, the next stop is the IMF, where member countries are expected to pledge billions more. The critics may be forgiven for pointing out that Europe could be doing more before tapping into purses of other, less affluent countries. Unfortunately, politicians treat this as politics rather than a serious debate about money. The good news here may be that we don’t think this is a European problem. The bad news is that this is a global problem. Spain is not unique. In the U.S., we have many of the same challenges, but we have a bond market that has allowed policy makers to get away with spending ever more money. Different from the Eurozone, the U.S. has a significant current account deficit. As such, should the bond market impose austerity on U.S. policy makers, it may have far more negative implications on the U.S. dollar than it has had on the Euro to date.

In the meantime, as policy makers around the world continue to hope for the best, but plan for the worst, expect monetary policy to be most accommodating: the U.S., Eurozone, UK and Japan all have eased in some form or another in recent months. Beneficiaries in the medium term may be precious metals and commodity currencies. For now, those currencies have been held back by a generally somber mood about global growth. What has done well – and we expect will continue to do well – are the currencies of countries that realize such policies will foster inflationary pressures. Singapore should be praised in this context, as the Singapore Monetary Authority tightened monetary policy last week, allowing the Singapore Dollar to appreciate. Those countries that can afford to are taking note that all this easy money may have significant side effects and are taking action to combat it. However, such countries are few and far between. We have long argued that there may not be such a thing anymore as a safe asset and investors may want to take a diversified approach to something as mundane as cash.

Please subscribe to our newsletter to be informed as we provide food for thought about the relationship between gold and currencies. We will also discuss what investors may want to do in a world that has moved further and further away from the gold standard. Subscribe to Merk Insights by clicking here. Also, please click here to register for the Merk Webinar: Quarter 1 Update on the Economy and Currencies which will take place on Thursday, April 19th at 4:15pm EF / 1:15pm PT. We manage the Merk Funds, including the Merk Hard Currency Fund. To learn more about the Funds, please visit www.merkfunds.com.By Axel Merk

Manager of the Merk Hard, Asian and Absolute Return Currency Funds, www.merkfunds.com

Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. Axel Merk wrote the book on Sustainable Wealth; order your copy today.

The Merk Absolute Return Currency Fund seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes.

The Merk Asian Currency Fund seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand.

The Merk Hard Currency Fund seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability.

The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses.

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Axel Merk Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.