U.S. Economy Flirting with Disaster

Economics / US Economy Jun 19, 2012 - 07:42 AM GMTBy: John_Mauldin

This week I offer a main course, a veritable piece de resistance, for Outside the Box readers, from my friend Rich Yamarone. Rich is Chief Economist for Bloomberg and one really sharp talent. He helps write Bloomberg Brief: Economics, a daily notebook that comes out every business morning with an all-encompassing view of what's happening and will happen.

This week I offer a main course, a veritable piece de resistance, for Outside the Box readers, from my friend Rich Yamarone. Rich is Chief Economist for Bloomberg and one really sharp talent. He helps write Bloomberg Brief: Economics, a daily notebook that comes out every business morning with an all-encompassing view of what's happening and will happen.

I have been on stage with him several times recently and have spent even more time with him over dinners. He keeps reminding me to pay attention to the slow-motion slowdown and eventual (he says) recession that is coming right here to the US. He thinks ten-year bond rates could scare 0.5% (not a typo!) if/when both Europe and China have a simultaneous crisis and the US is seen as a real –and perhaps the last – safe haven (to which I would add: besides gold). Certainly 1% on the ten-year and 2% on the 30-year will be on offer in such a scenario.

I asked him to give us a brief tour, based on some of the graphs in his latest presentation, and it arrived today. If you like, you can subscribe to their regular research by going to bloombergbriefs.com/economics.

But we can't ignore Europe entirely, so for an appetizer I offer this small note from Rob Arnott, founder of Research Affiliates (you may know them as the Fundamental Index guys) and manager of the extremely popular (for good reason) All-Asset Fund at PIMCO. Rob will be with me in about a week in Italy, and I look forward to great evenings over Italian food with friends and family.

Here, Rob looks into the future (something he does with great success in his funds) and walks us backward in time. But I will let him tell his story and then we'll get on to the main course. Quoting:

"On another topic, one of my favorite games as an asset manager is to look past current travails and ask what *must* happen in the years ahead. Then we can turn attention to working backwards, identifying the intervening "path of least resistance." Sometimes, this is *way* more powerful than looking at the near-term decision tree and working forwards.

"The EZ travails lend themselves elegantly to this treatment. What will happen in the months ahead? No one really knows. What will happen in the years ahead? Nations addicted to debt-financed consumption will have to balance their books. All of Europe (and the US and Japan) will be spending no more (or very little more) than their tax receipts, a few years hence. Why? Because – as with any family – debt-financed consumption is ultimately unsustainable.

"Likewise, some years hence, entitlements will need to be on a pay-as-we-go basis, give or take a little wiggle room, in order to not crowd out all other forms of spending. Debt service will need to be part of the nations' spending, crowding out other forms of spending; a 'primary surplus' will be irrelevant.

"When will this transition take place? It's impossible for the status quo to continue more than a few years, though Japan shows that debt-financed government spending can persist far longer than most observers might suppose. And it's impossible for status quo to persist after the capital markets begin looking these few years ahead, which telescopes this transition into the coming handful of years. The more a nation relies on foreign investors to fund its spending, the faster this cliff arrives.

"So, working backwards from these inevitabilities ...

· "Since government spending roughly equals tax receipts, less interest payments, collecting more in taxes is a very dubious path by which to arrive at balance.

· "This leaves us with spending cuts. Entitlement spending roughly equals tax receipts attached to the entitlements. So the same logic applies: entitlement spending will be cut. Age of eligibility, means testing, and rationing are the paths of least resistance; but this will require an evisceration of the public sector and empowering of the private sector, which will in turn require a stark liberalization of regulatory and employment law.

· "*Or* there will be a collapse of GDP, as public spending drops without allowing the private sector to pick up the slack. Increasing global pressure for financial transparency, to facilitate tax collection, will become the norm.

"As we move back closer to the present, the near-term implications are less clear.

· "Nothing in this end-point *requires* that countries leave the EZ. Greece can simply slash public-worker salaries or head count to be fully covered by tax receipts. Likewise, Spain, Italy, Portugal, France (!).

· "If any country does exit, its banking sector must rebuild from scratch. The domino effect here is obvious: countries exiting en masse becomes a possibility. Italy and France are not assured to remain in the EZ in this circumstance. So, it's implausible that one, and only one, country exits.

· "All of this means that EZ exits may prove to be too messy to be allowed to happen, in which case defaulting countries will simply default, then cut spending to balance their budgets ... and then move on, with sharply diminished public sectors and GDP."

And back with John. It all sounds so simple when he explains it. But we will lurch from crisis to crisis in Europe, and then Japan will enter the picture in a big way. Hopefully we in the US can learn a lesson and deal proactively with our very similar problems, about which I will write this week.

And now I have to go to my next meeting, although it will be a pleasant one over a low-cholesterol dinner. Have a great week. The next time you hear from me I will be in Madrid on my way to Italy. So adios and ciao for now.

Your ready for a little downtime and conversation analyst,

John Mauldin, Editor Outside the Box JohnMauldin@2000wave.com

Flirtin' with Disaster

Rich Yamarone Chief Economist, Bloomberg

I'm travelin' down the road and I'm flirtin' with disaster I've got the pedal to the floor and my life is running faster I'm outta money outta hope it looks like self destruction Well how much more can we take with all of this corruption

Molly Hatchet

The U.S. economy is flirting with disaster. Traditionally policy makers adopt a monetary-fiscal policy mix that is targeted to the ailing economy; unfortunately for the U.S. those policies today are either impotent or contractionary.

Recently released economic data confirm the end of the strong patch; the lack of real disposable personal income has resulted in a slump in the primary driver of aggregate demand, consumer spending. In what seems like an annual event, economists are once again returning to their models for downward revisions to GDP growth estimates. Anecdotes contained in the Bloomberg Orange Book have identified all of the current underlying influences in the economy including a paradigm shift in the retail sector and the temporarily positive economic consequences of a warmer than historical spring. Both of these factors imply deteriorating activity.

A sinking economy requires stimulus from two agents, the Federal Reserve and the government. There are periods throughout history when monetary policy prescriptions from the Fed have a better influence on the economy than the government's fiscal responses. Sometimes the government's actions rule the day. Ultimately, the economy is righted by some combination of these two sources.

Today, monetary policy is rendered impotent since the U.S. economy is mired in a liquidity trap, and the Fed's actions have been as effective as "pushing on a string." Part of the reason for monetary policy's impotence is related to cyclical factors, while structural factors in the economy account for the other part and may take decades to sort out.

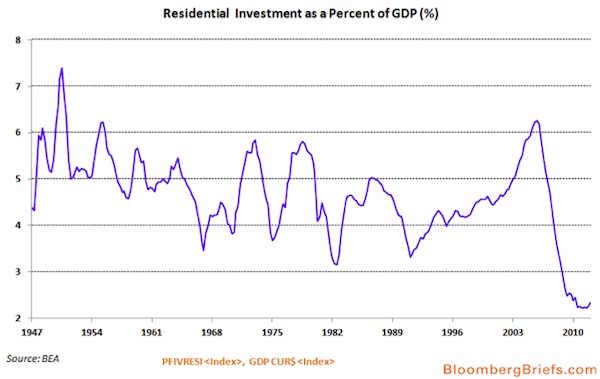

Extremely easy monetary plans have failed to boost aggregate demand and engender a desirable pace of job creation. By lowering interest rates – the primary policy tool of the central bank – the intent is to influence the two most interest rate sensitive sectors, housing and manufacturing. Housing – generally one of the biggest contributors of overall economic health in the economy – is barely advancing from its bottom registered two years ago. Sales of homes have flat-lined, the MBA Purchasing Managers Index is locked in a sideways trend, and employment in this industry is a far cry from encouraging. This sector is a lowly fraction of its former self. What used to comprise over 5 percent of GDP now lingers at an all-time low 2.3 percent.

The housing industry has historically been a major macroeconomic driver though employment – purely domestic since they cannot be off-shored – and through endless retail and spending channels.

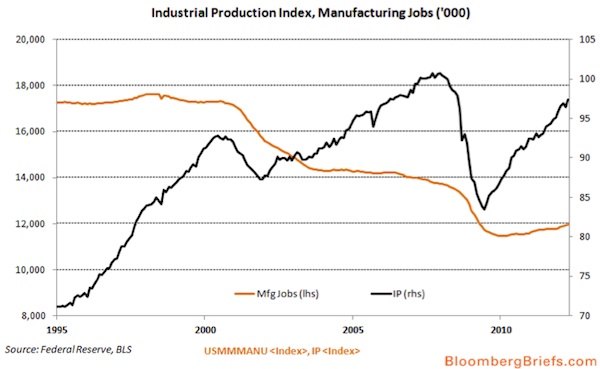

Manufacturing output has picked up sharply, with a brilliant V-shaped recovery. Unfortunately, there has been little-to-no job creation due to exponential gains in productivity in this sector.

The fruitless economic response to record low interest rates are proof positive that Fed policies are not inciting a desired response– you can lead a horse to water, but you can't make it drink.

On the fiscal front, intensifying restrictive policies are impeding economic activity, and may send the economy into a tailspin before the arrival of the "Fiscal Cliff" in January 2013.

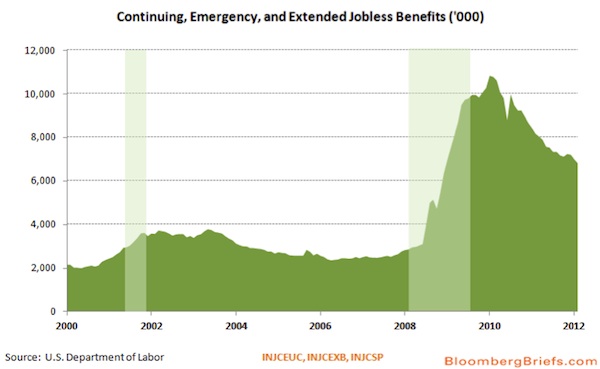

Contrary to popular belief, we never had a legitimate fiscal stimulus – what we got was largely an extension of unemployment benefit insurance. This, as most economists will remind you, is nothing more than a disincentive to look for a job. For many out-of-work Americans, particularly those with limited skills and education, it is best to sit on the couch, watch Oprah and eat Bon-Bons. Don't get me wrong, I like Bon-Bons. But sending a check to a depressed, out-of-work individual is not a way to get the economy back on its feet.

There is nothing stimulative about unemployment benefit insurance – it is a safety net for those that have fallen. In my longer than 25 year history on Wall Street I have collected unemployment benefits on seven occasions. [Finance is a very cyclical industry, and the economist is usually the first to be jettisoned when tough times surface. So, if you are a good economist – and I am – you know when you're about to get fired.]

Those checks didn't boost consumption activity in my household, and they certainly didn't get the economy back on its feet. At best it keeps some percentage of the labor force above water; at worst it exacerbates the growing chasm between the haves and the have-nots and stirs civil unrest through movements like Occupy Wall Street.

Sadly, the American public is led to believe that the cure can be found though a political right wing vs. left wing fight. It cannot. The U.S. economy is bigger and more powerful than any tax cutting Republican or transfer payment-issuing Democrat. We experienced a depression in 2007-2009– a prolonged period of contracting economic activity associated with a steep decline in employment. Not the severity of the Great Depression, but certainly more harsh than any recession since. The only way out of a depression is to adopt an incredibly easy-money Fed policy – which we did –combined with bold expansionary fiscal policy – which we did not.

What should have happened, and perhaps looking ahead, may be the only effective government response, is a direct work relief program like in the 1930s. Is this politically popular or desirable? Of course not. But it may be the only choice. Cutting taxes haven't helped; it's not exactly clear how reducing a tax burden on an underemployed individual or on a business that has fewer people passing through its doors will employ more people? You may get more hiring of minimum wage retail workers; again, not the type of job creation to get the economy back on a path of prosperity.

Adherents of Adam Smith and Free Marketeers should welcome a bold government move like this since it was outlined in their bible, The Wealth of Nations. Smith promoted the government's maintenance of "good roads and communications," whereby they benefit the whole society. Smith thought it to be one of only a few reasons for governments to intervene – the others being education, defense, and the administration of justice. If we had shovel ready, boots-to-the ground jobs like we were promised in 2008 rather than extended benefits (food stamps, jobless benefits, tax credits, etc.) we'd have employed a good portion of those idled construction workers, manufacturers, machinists, etc. They would have fixed our dilapidated highways, bridges, tunnels, railways, ports, electrical grid, and airports (that can't land the newest planes.) Like FDR's New Deal works program, we'd have a legacy after it was all over.

My great grandfather was a sculptor (Lee Lawrie, sculpting Atlas in Rockefeller Center.) He was paid by the government to do that project. Then, after the Great Depression ended, there was a legacy. We had stuff to brag about, and people had jobs, and felt good about themselves. [No wonder FDR was the only president elected to more than two terms.]

Today our legacy consists primarily of roughly three times the historical average of unemployed workers receiving unemployment benefit insurance...

Now with a burgeoning budget deficit, expansionary fiscal policy is considerably more difficult to implement – but not impossible. Ending some benefits and tax cuts could pave the way for the necessary financing of a major public works program.

The lone saving grace is, if the United States has to borrow a boatload of money, and it does, it is best to do it during a low real interest rate environment. Assuming an inflation rate of 2.7 percent and a yield on the U.S. 30-year bond of 2.68 percent, the government is effectively borrowing real money for thirty years free.

Consumer Spending

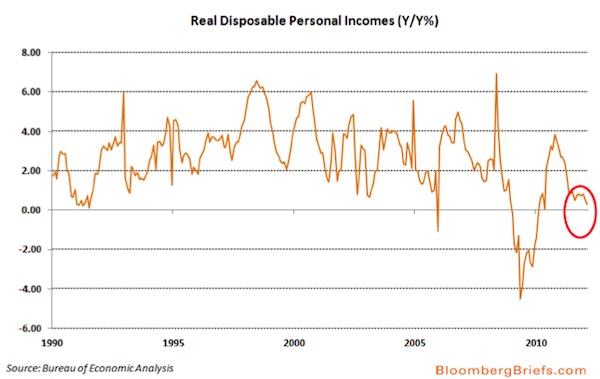

What's it take to get consumers (upwards of 72 percent of the U.S. economy) to spend? As George Harrison said, "...it's gonna take money a whole lotta spending money. It's gonna take plenty of money to do it right child." Unfortunately the labor dynamics in the country are not inducing a sufficient pace of real income and wage growth.

Keep in mind that current labor market conditions are grossly different than they were a few years ago. As I mentioned back in early February, most of the jobs that have been created have been in industries generally not atop the income spectrum: administrative and waste services, food services and drinking places, retail department stores, arts, entertainment, and spectator sports – this also includes employment at museums, historical sites, and amusement parks, and membership associations and organizations.

Real disposable personal incomes – income available after adjustments for taxes and inflation – are up a lowly 0.6 percent over the last year. This is the amount of money that consumers have available to spend.

Bloomberg Orange Book Revelations

Several companies in the Bloomberg Orange Book – a compilation of macroeconomic anecdotes gleaned from comments CEOs and CFOs make on quarterly earnings conference calls – have made mention of the downward trend in incomes. Lowe's Corp. said, "We believe future uncertainties are still weighing heavily on the consumer. For instance, there is no meaningful area of strength in personal income data. So while spending has been strong up to this point in the year, it will likely level off without real income growth."

Mort Zuckerman, CEO of Boston Properties noted, "The income numbers are very weak. The retail sales numbers are very weak when you boil it down to what it – take out food and fuel. The overall GDP growth is weak."

The spending side of the equation isn't that promising either. Real consumption expenditures are only 2.1 percent higher than year ago levels. And as Mr. Zuckerman said, purchases on necessities like food and fuel are growing in importance to a retailer that has its back against the wall.

It's no secret that there is a great transformation underway in the retail sector. Consumers have adopted a multi-channel buying process whereby the would-be buyer will browse bricks and mortar stores to try on sizes, feel styles, materials, colors, etc. Then, when satisfied, they head back to the internet (on their laptops or mobile applications) and order it free of delivery charges and in many instances, free of taxes.

This process had decimated many sellers of ubiquitous items like books, electronics, and household items. As a result, businesses like Circuit City, Borders, and Linen's & Things have all been forced to file for bankruptcy protection. This is a trend that may continue to negatively affect other stores that refuse to change. Macy's is trying to work around these changes in consumer behavior; "We are also beginning to be able to satisfy online demand with store inventory when the distribution center runs out of a particular item. It is really very exciting to watch. We now have over 80 stores equipped to fulfill orders from other stores or from online demand, and by the holiday season, we'll have over 290 store fulfillment locations. We think the sales potential from this omni-channel approach is enormous."

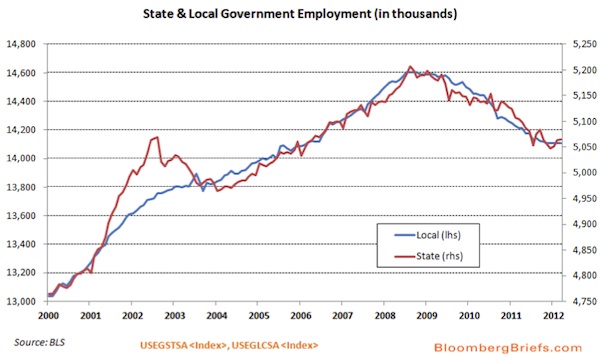

There are several disconcerting issues with this trend. Obviously, the diminished need for bricks and mortar stores has resulted in widespread mall vacancies, which are lingering near all-time highs. This reduces employment opportunities. In addition, it hurts state and local governments. The reduction of commercial tax revenues – combined with losses in the residential and income tax base – as well as lost sales tax revenues force local municipalities to make cuts. This is best identified by the ongoing job cuts by governments.

Similarly, several Big Box retailers like Wal-Mart and Best Buy are experimenting with smaller-sized stores. If consumers are only going to come in to browse, why possess so much space? It can be costly heating and cooling 50,000 square feet. Another developing trend is that many retailers are expanding their food and beverage presence. Wal-Mart continues to perform much better in the grocery aisle than in its apparel and footwear section. They are very much aware of how critical grocery items are to the consumer. In its last quarterly earnings conference call, Wal-Mart mentioned, "As we move into the second quarter, we remain mindful of potential challenges for our customers. The overall economy is still our customers' main concern. In particular, they remain concerned about job security or the availability of jobs, followed by gas and energy prices and rising food costs. Food is consistently the top monthly expense outside of housing and vehicle payments."

Dollar Tree's CEO Bob Sasser said, "Our expansion of frozen and refrigerated product continues. We installed freezers and coolers in 127 stores in the first quarter and now offer frozen and refrigerated product in 2,345 stores. We are planning approximately 325 installations for the full year. This important category is extremely productive. It serves the current needs of our customers, drives traffic into our stores and provides incremental sales across all categories."

Target is also well along the way of the expanded grocery presence. In its latest conference call, CEO Gregg Steinhafel noted, "We also completed more than 100 remodels, resulting in nearly 1,000 general merchandise stores that we've either opened or remodeled in the last four years. This means that even though we've reduced new store growth in response to the recession and resulting slowdown in commercial development, our store base is much fresher than before the recession began. Guests in these stores respond to the appealing environment by spending more at Target, as we capture more of their shopping trips. While the most visible change to these stores is the addition of a broader food assortment, including an edited assortment of perishable items, guests also respond to enhanced navigation, compelling visual elements, and our latest thinking in beauty, shoes, home, apparel, and baby. As we look ahead to the remainder of 2012, we remain confident in our strategy and operational plan but cautious about the macro-environment. We believe the current economic recovery will continue to be slow and uneven."

What to Watch

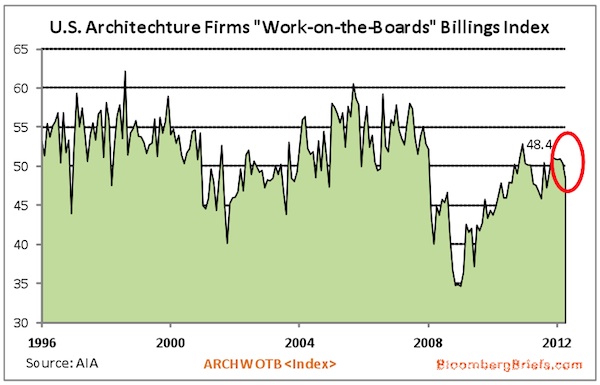

One key indicator to keep a keen eye on is the Architectural Billings Index (ABI) assembled by the American Institute of Architects. In the past Johnson Controls, U.S. Concrete, and even Alcoa have made mention of the importance of the Architectural Billings Index as an indicator of things to come. In the latest quarterly earnings season, two companies cited its trend.

A.O. Smith: "New construction...we look at as light commercial and light industrial for our product lines. You can see the Architectural Billing Index. That's the leading indicator that we look at and it's coming up a little bit, but we're expecting it to be flat."

United Rentals: "And the Architectural Building Index which has remained above 50 for the commercial and industrial sector for seven straight months and this morning the ABI reported that the March index for our sector was 56. So as you know we felt good about 2012 going into this year and we're just as bullish now and even more confident about our outlook."

The ABI fell two points in April to 48.4 – any reading below 50 implies contraction.

Weather

The 'Word of the Quarterly Earnings Season' in the latest edition of the Bloomberg Orange Book must be "Weather." Nearly every company made some mention of the record high temps and talked about the influences on their respective earnings performance. Retailers like Urban Outfitters, warned "We believe the early, usually warm weather in the first quarter may steal some sales from the second quarter." Essentially all apparel and footwear retailers noted a sizeable increase in demand for spring apparel. Restaurants benefited by an early opening of patio and outdoor dining.

Not everyone saw the sunny skies and warmer climate as favorable. Food producers felt a sting at traditional winter travel destinations; Sysco said: "...we were hurt in areas where you would expect winter to be beneficial. So the big ski areas in Colorado and Utah and Florida, you know, we did not do as well in those areas and so I'm not going to say it netted out, but it wasn't a totally positive thing from a weather standpoint."

Better than expected conditions caused the rails to take it on the chin due to lesser demand for raw materials. Norfolk Southern claimed "Chemicals volume was flat for the quarter, as gains in plastics and crude oil from the Bakken and Canadian oilfields offset declines in rock salt for highway treatment due to the mild winter." Meanwhile, Union Pacific said "...volume decline in our Energy business during the quarter was largely the result of a dramatic weakening of demand for coal, driven by a near perfect storm of very mild winter weather and low natural gas prices..."

Interestingly, in this rather gloomy assessment of the U.S. economic situation, not a single mention was made of the U.K. recession, Europe, the possible break-up of the euro, Spain's housing and banking crisis, Japan's third lost decade, or the harder than initially expected Chinese landing – issues revealed on several occasions in the Orange Book. Cumulatively, they can't possibly be good for the U.S. economic situation.

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.