Bond Insurers Failures to Break 200 Year Old System - The Great Credit Unwind of 2008

Interest-Rates / Credit Crisis 2008 Jan 30, 2008 - 01:18 PM GMTBy: Mike_Whitney

"The current crisis is not only the bust that follows the housing boom, it's basically the end of a 60-year period of continuing credit expansion based on the dollar as the reserve currency. Now the rest of the world is increasingly unwilling to accumulate dollars.'' ' George Soros, World Economic Forum in Davos, Switzerland. `

"The current crisis is not only the bust that follows the housing boom, it's basically the end of a 60-year period of continuing credit expansion based on the dollar as the reserve currency. Now the rest of the world is increasingly unwilling to accumulate dollars.'' ' George Soros, World Economic Forum in Davos, Switzerland. `

Global market turmoil continued into a second week as stock markets in Asia and Europe took another tumble on Monday on growing fears of a recession in the United States. China's benchmark index plummeted 7.2% to its lowest point in six months, while Japan's Nikkei index slipped another 4.3%. Equities markets across Asia recorded similar results and, by midmorning in Europe, all three major indexes---the UK FTSE “Footsie”, France's CAC 40, and the German DAX---were all recording heavy losses. It's now clear that Fed Chairman Bernanke's 'surprise' announcement of a 75 basis points cut to the Fed Funds rate last Tuesday has neither stabilized the markets nor restored confidence among jittery investors.

At the time of this writing, the storm clouds are swiftly moving towards Wall Street where markets are likely to be roiled on the very day that President Bush will give his farewell State of the Union speech.

In Monday's Financial Times, Harvard economics professor, Lawrence Summers, made an impassioned plea for further government action in addition to the Fed's rate cuts and Bush's $150 billion “stimulus plan”. Summers believes that steps must be taken immediately to mitigate the damage from the sharp downturn in housing and persistent troubles in the credit markets. He suggests a “global coordination of policy”, which is another way of admitting that the Fed has lost control of the system and cannot solve the problem by itself.

Summers is right, although it's easy to wonder why he remained silent while the markets were soaring and the investment banks were reaping trillions of dollars in profits on a “structured investment” swindle which has left the global financial system teetering on the brink of catastrophe. Now that the US economy is sliding towards recession; Summers is calling for “transparency”. How convenient.

“Financial institutions are holding all sorts of credit instruments that are impaired but are difficult to value, creating uncertainty and freezing new lending. Without more visibility, the economy and financial system risk freezing up as Japan's did in the 1990s.”

Right again. The banks are “capital impaired” because they are holding nearly $600 billion in mortgage-backed assets which are declining in value every month. This is forcing many banks to conceal their real condition from investors while they scour the planet for the extra capital they need to continue operations. As long as the banks are in distress, consumer and business lending will dwindle and the economy will continue to shrink. The main gear in the credit-generating mechanism is now broken. The rate cuts can provide liquidity, but they cannot bring insolvent banks back from the dead. Summers is expecting too much.

The United States has led the world into the greatest credit bust in history, and yet, few people even know what has transpired. The US massive current account deficit (nearly $800 billion) has been recycling into US Treasuries and securities from foreign investors. Up to this point, American markets were an attractive place to put one's savings. The dollar was strong, and the stock market had a proven record of profitability and transparency. But since President Bill Clinton repealed Glass-Steagall in 1999, the markets have been reconfigured according to an entirely new model, “structured finance”. Glass-Steagall was the last of the Depression-era bulwarks against the merging of commercial and investment banks. As a result banking has changed from a culture of “protection” (of deposits) to “risk taking”, which is the securities business.

Through “financial innovation” the investment banks created myriad structured debt instruments which they sold through their Enron-like “off balance” sheets operations (SIVs and Conduits) Now, trillions of dollars of these subprime and mortgage-backed bonds---many of which were rated triple A---are held by foreign banks, retirement funds, insurance companies, and hedge funds. They are steadily losing value with every rating's downgrade. Here is a graph which illustrates how the scam works. http://bp2.blogger.com/_nSTO-vZpSgc/R5VesXtCUwI/AAAAAAAAB50/gUcUZpYFey8/s1600-h/Model-For-Fraud.png

Summers, of course, understands the enormity of the swindle that has taken place beneath the noses of US regulators, but chooses not to hold any of the main actors accountable. Instead, he draws our attention to a little known part of the market which will probably lead the way to a stock market crash and a system-wide meltdown.

Here's Summers: “It is critical that sufficient capital is infused into the bond insurance industry as soon as possible. Their failure or loss of a AAA rating is a potential source of systemic risk. Probably it will be necessary to turn in part to those companies that have a stake in guarantees remaining credible because they have large holdings of guaranteed paper. It appears unlikely that repair will take place without some encouragement and involvement by financial authorities. Though there are many differences and the current problem is more complex, the Long-Term Capital Management work-out is an example of successful public sector involvement.”

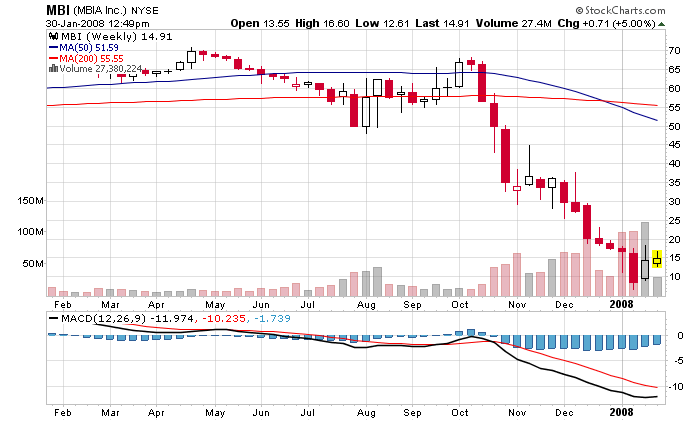

Some of the largest bond insurers are are currently unable to cover the losses that are piling up from the meltdown in mortgage-backed securities (MBS) and collateralized debt obligations (CDO). Their business model is hopelessly broken and they will require an immediate $143 billion bailout to maintain operations. The largest of the bond insurers is MBIA.

"MBIA's total exposure to bonds backed by mortgages and CDOs was disclosed to be $30.6 billion, including $8.14 billion of holdings of CDO-squareds (eds note; pure garbage). MBIA was being priced as a weak CCC-rated credit when it issued its bonds last week; it is now being priced for a bankruptcy. MBIA's stock, which traded just under $68 per share last October, dropped another $3.50 this morning to under $10.00 per share.” (Stock analyst Michael Lewitt, quoted in Bloomberg)

Barclay's estimates that the investment banks alone are holding as much as $615 billion of structured securities guaranteed by bond insurers. If the insurers default, hundreds of billions will be lost via downgrades.

So, in practical terms, what does it mean if the bond insurers go under?

It means that the system will freeze and the stock market will crash. Here's how TV stock guru Jim Cramer summed it up last week in an interview with MSNBC's Chris Matthews: “But, Chris, there is something I would urge all the candidates to think about and our Treasury Secretary, which is that there are a group of insurance companies which insure all these bad mortgages and, Cris, I think they are all about to go belly-up, and that will cause the Dow Jones to decline 2,000 points. They've got to be shut down and the insurance given to a New Resolution Trust. This is going to happen in maybe two or three weeks, Chris, it going to on the front of every newspaper and no one in Washington is even willing to admit it.

Chris Matthews: “So who are you including in these mortgage companies that are going to go belly-up; give me a description?

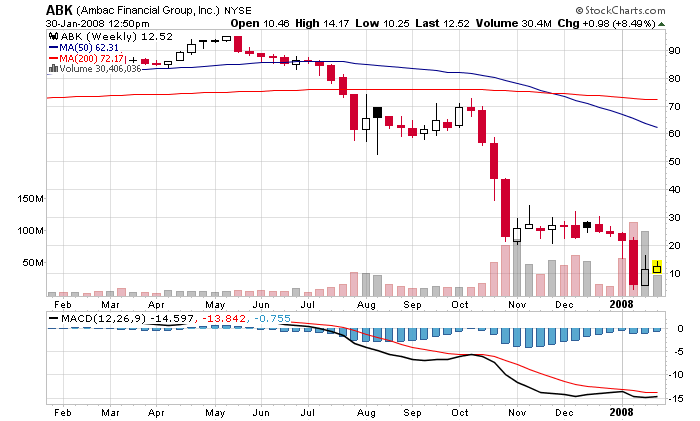

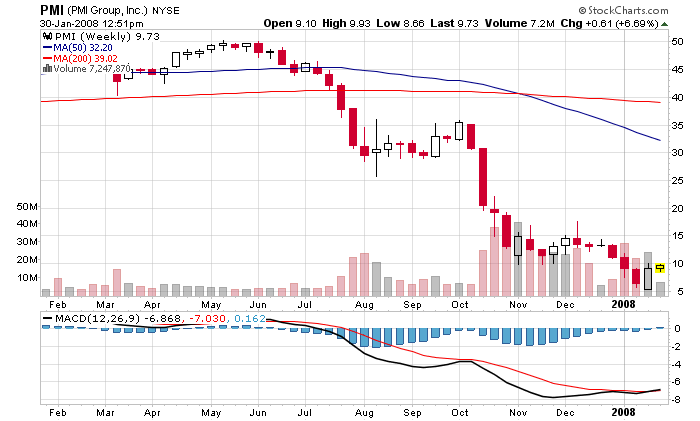

These are MBIA and Ambac remember the companies that Merrill Lynch and Citigroup wrote down a lot of stuff the other day? All these companies are relying on insurance to save them. The insurers don't have the money. There's also personal mortgage insurance; that's PMI, is one company; MGIC is another. Chris, I am telling you that these companies do not have the capital to “make good”. And when they do fall, and I believe it is when---if the government does not have a plan in action; you will not be able to open the stock market when they collapse.” No one is even talking about the fact that these major insurers, who insure $450 billion of mortgages are all about to go under.” (See the whole video: http://www.crooksandliars.com/Media/Play/25486/1/hardball_cramer_recession_011808.wmv/ )

Cramer is correct in assuming that the market won't open. And yet, so far, nothing has been done to avert the disaster which lies just ahead. Maybe nothing can be done?

So, how did things get so bad, so fast? How could the world's most resilient and profitable markets be transformed into a carnival sideshow peddling poisonous “mortgage-backed” snake-oil to every gullible investor?

Author and stock market soothsayer Pam Martens puts it like this: “How could a layered concoction of questionable debt pools, many of dubious origin, achieve the equivalent AAA rating as U.S. Treasury securities, backed by the full faith and credit of the U.S. government, and time-tested over a century of panics, crashes and the Great Depression?

How did a 200-year old "efficient" market model that priced its securities based on regular price discovery through transparent trading morph into an opaque manufacturing and warehousing complex of products that didn't trade or rarely traded, necessitating pricing based on statistical models?” (The Free Market Myth Dissolves into Chaos, Pam Martens, counterpunch)

How, indeed?

The answer to all these questions is “deregulation”. The financial system has been handed over to scam-artists and fraudsters who've created a multi-trillion dollar inverted pyramid of shaky, hyper-inflated, subprime slop that they've sold around the world with the tacit support of the ratings agencies and the US political establishment. (wink, wink) Now that system is about to collapse and there's nothing that the Federal Reserve can do to stop the Great Credit Unwind of '08.

As economist Ludwig von Mises said: "There is no means of avoiding the final collapse of a boom brought on by credit expansion. The question is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved."

By Mike Whitney

Email: fergiewhitney@msn.com

Mike is a well respected freelance writer living in Washington state, interested in politics and economics from a libertarian perspective.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.