The Myth that Japan is Broke: The World’s Largest “Debtor” is now the Largest Creditor

Interest-Rates / Japan Economy Sep 09, 2012 - 11:22 AM GMTBy: Ellen_Brown

Japan’s massive government debt conceals massive benefits for the Japanese people, with lessons for the U.S. debt “crisis.”

Japan’s massive government debt conceals massive benefits for the Japanese people, with lessons for the U.S. debt “crisis.”

In an April 2012 article in Forbes titled “If Japan Is Broke, How Is It Bailing Out Europe?”, Eamonn Fingleton pointed out the Japanese government was by far the largest single non-eurozone contributor to the latest Euro rescue effort. This, he said, is “the same government that has been going round pretending to be bankrupt (or at least offering no serious rebuttal when benighted American and British commentators portray Japanese public finances as a trainwreck).” Noting that it was also Japan that rescued the IMF system virtually single-handedly at the height of the global panic in 2009, Fingleton asked:

How can a nation whose government is supposedly the most overborrowed in the advanced world afford such generosity? . . .

How can a nation whose government is supposedly the most overborrowed in the advanced world afford such generosity? . . .

The betting is that Japan’s true public finances are far stronger than the Western press has been led to believe. What is undeniable is that the Japanese Ministry of Finance is one of the most opaque in the world . . . .

Fingleton acknowledged that the Japanese government’s liabilities are large, but said we also need to look at the asset side of the balance sheet:

[T]he Tokyo Finance Ministry is increasingly borrowing from the Japanese public not to finance out-of-control government spending at home but rather abroad. Besides stepping up to the plate to keep the IMF in business, Tokyo has long been the lender of last resort to both the U.S. and British governments. Meanwhile it borrows 10-year money at an interest rate of just 1.0 percent, the second lowest rate of any borrower in the world after the government of Switzerland.

It’s a good deal for the Japanese government: it can borrow 10-year money at 1 percent and lend it to the U.S. at 1.6 percent (the going rate on U.S. 10-year bonds), making a tidy spread.

Japan’s debt-to-GDP ratio is nearly 230%, the worst of any major country in the world. Yet Japan remains the world’s largest creditor country, with net foreign assets of $3.19 trillion. In 2010, its GDP per capita was more than that of France, Germany, the U.K. and Italy. And while China’s economy is now larger than Japan’s because of its burgeoning population (1.3 billion versus 128 million), China’s $5,414 GDP per capita is only 12 percent of Japan’s $45,920.

How to explain these anomalies? Fully 95 percent of Japan’s national debt is held domestically by the Japanese themselves.

Over 20% of the debt is held by Japan Post Bank, the Bank of Japan, and other government entities. Japan Post is the largest holder of domestic savings in the world, and it returns interest to its Japanese customers. Although theoretically privatized in 2007, it has been a political football, and 100% of its stock is still owned by the government. The Bank of Japan is 55% government-owned and 100% government-controlled.

Of the remaining debt, over 60% is held by Japanese banks, insurance companies and pension funds. Another chunk is held by individual Japanese savers. Only 5% is held by foreigners, mostly central banks. As noted in a September 2011 article in The New York Times:

The Japanese government is in deep debt, but the rest of Japan has ample money to spare.

The Japanese government’s debt is the people’s money. They own each other, and they collectively reap the benefits.

Myths of the Japanese Debt-to-GDP Ratio

Japan’s debt-to-GDP ratio looks bad. But as economist Hazel Henderson notes, this is just a matter of accounting practice—a practice that she and other experts contend is misleading. Japan leads globally in virtually all areas of high-tech manufacturing, including aerospace. The debt on the other side of its balance sheet represents the payoffs from all this productivity to the Japanese people.

According to Gary Shilling, writing on Bloomberg in June 2012, more than half of Japanese public spending goes for debt service and social security payments. Debt service is paid as interest to Japanese “savers.” Social security and interest on the national debt are not included in GDP, but these are actually the social safety net and public dividends of a highly productive economy. These, more than the military weapons and “financial products” that compose a major portion of U.S. GDP, are the real fruits of a nation’s industry. For Japan, they represent the enjoyment by the people of the enormous output of their high-tech industrial base.

Shilling writes:

Government deficits are supposed to stimulate the economy, yet the composition of Japanese public spending isn’t particularly helpful. Debt service and social-security payments — generally non-stimulative — are expected to consume 53.5 percent of total outlays for 2012 . . . .

So says conventional theory, but social security and interest paid to domestic savers actually do stimulate the economy. They do it by getting money into the pockets of the people, increasing “demand.” Consumers with money to spend then fill the shopping malls, increasing orders for more products, driving up manufacturing and employment.

Myths About Quantitative Easing

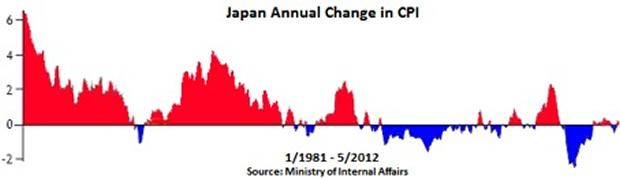

Some of the money for these government expenditures has come directly from “money printing” by the central bank, also known as “quantitative easing.” For over a decade, the Bank of Japan has been engaged in this practice; yet the hyperinflation that deficit hawks said it would trigger has not occurred. To the contrary, as noted by Wolf Richter in a May 9, 2012 article:

[T]he Japanese [are] in fact among the few people in the world enjoying actual price stability, with interchanging periods of minor inflation and minor deflation—as opposed to the 27% inflation per decade that the Fed has conjured up and continues to call, moronically, “price stability.”

He cites as evidence the following graph from the Japanese Ministry of Internal Affairs:

How is that possible? It all depends on where the money generated by quantitative easing ends up. In Japan, the money borrowed by the government has found its way back into the pockets of the Japanese people in the form of social security and interest on their savings. Money in consumer bank accounts stimulates demand, stimulating the production of goods and services, increasing supply; and when supply and demand rise together, prices remain stable.

Myths About the “Lost Decade”

Japan’s finances have long been shrouded in secrecy, perhaps because when the country was more open about printing money and using it to support its industries, it got embroiled in World War II. In his 2008 book In the Jaws of the Dragon, Fingleton suggests that Japan feigned insolvency in the “lost decade” of the 1990s to avoid drawing the ire of protectionist Americans for its booming export trade in automobiles and other products. Belying the weak reported statistics, Japanese exports increased by 73% during that decade, foreign assets increased, and electricity use increased by 30%, a tell-tale indicator of a flourishing industrial sector. By 2006, Japan’s exports were three times what they were in 1989.

The Japanese government has maintained the façade of complying with international banking regulations by “borrowing” money rather than “printing” it outright. But borrowing money issued by the government’s own central bank is the functional equivalent of the government printing it, particularly when the debt is just carried on the books and never paid back.

Implications for the “Fiscal Cliff”

All of this has implications for Americans concerned with an out-of-control national debt. Properly managed and directed, it seems, the debt need be nothing to fear. Like Japan, and unlike Greece and other Eurozone countries, the U.S. is the sovereign issuer of its own currency. If it wished, Congress could fund its budget without resorting to foreign creditors or private banks. It could do this either by issuing the money directly or by borrowing from its own central bank, effectively interest-free, since the Fed rebates its profits to the government after deducting its costs.

A little quantitative easing can be a good thing, if the money winds up with the government and the people rather than simply in the reserve accounts of banks. The national debt can also be a good thing. As Federal Reserve Board Chairman Marriner Eccles testified in hearings before the House Committee on Banking and Currency in 1941, government credit (or debt) “is what our money system is. If there were no debts in our money system, there wouldn’t be any money.”

Properly directed, the national debt becomes the spending money of the people. It stimulates demand, stimulating productivity. To keep the system stable and sustainable, the money just needs to come from the nation’s own government and its own people, and needs to return to the government and people.

Ellen Brown developed her research skills as an attorney practicing civil litigation in Los Angeles. In Web of Debt, her latest book, she turns those skills to an analysis of the Federal Reserve and “the money trust.” She shows how this private cartel has usurped the power to create money from the people themselves, and how we the people can get it back. Her earlier books focused on the pharmaceutical cartel that gets its power from “the money trust.” Her eleven books include Forbidden Medicine, Nature’s Pharmacy (co-authored with Dr. Lynne Walker), and The Key to Ultimate Health (co-authored with Dr. Richard Hansen). Her websites are www.webofdebt.com and www.ellenbrown.com.

Ellen Brown is a frequent contributor to Global Research. Global Research Articles by Ellen Brown

© Copyright Ellen Brown , Global Research, 2012

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.