Is the "Fiscal Cliff" a Threat to the U.S. Economy?

Economics / Taxes Sep 16, 2012 - 08:23 AM GMTBy: Frank_Shostak

The US Congressional Budget Office (CBO) said on August 22, 2012, that scheduled tax increases and spending cuts in 2013 would reverse the current modest economic recovery. The CBO and other experts are of the view that large government spending cuts and tax hikes will cause severe economic slump.

The US Congressional Budget Office (CBO) said on August 22, 2012, that scheduled tax increases and spending cuts in 2013 would reverse the current modest economic recovery. The CBO and other experts are of the view that large government spending cuts and tax hikes will cause severe economic slump.

Experts hold that without action by Congress to avoid a "fiscal cliff" Americans should expect a significant recession and the loss of some 2 million jobs. The CBO predicts that the real GDP could shrink by 0.5 percent next year while the unemployment rate could climb to around 9 percent.

Experts hold that without action by Congress to avoid a "fiscal cliff" Americans should expect a significant recession and the loss of some 2 million jobs. The CBO predicts that the real GDP could shrink by 0.5 percent next year while the unemployment rate could climb to around 9 percent.

The "fiscal cliff" refers to the impact of around $500 billion in expiring tax cuts and automatic government-spending reductions set for 2013 as a result of successive failures by Congress to agree on some orderly alternative method of reducing budget deficits.

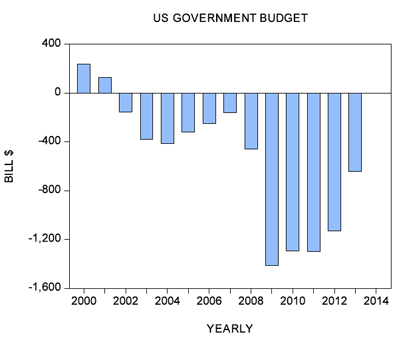

According to the CBO projection the budget deficit could fall to $641 billion in 2013 from $1.128 trillion in 2012.

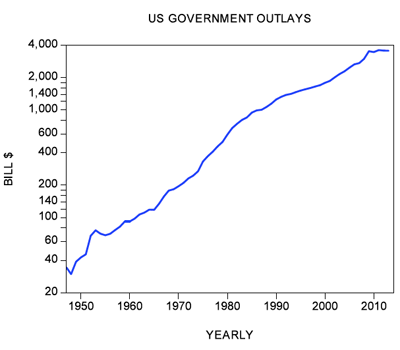

We suggest that the goal of fixing the budget deficit as such could be an erroneous policy. Ultimately what matters for the economy is not the size of the budget deficit but the size of government outlays — the amount of resources that government diverts to its own activities. Note that, because the government is not a wealth-generating entity, the more it spends, the more resources it has to take from wealth generators. This means that the effective level of tax here is the size of the government and nothing else.

For instance, the government outlays are $3 trillion, and the government revenue is $2 trillion — the government has a deficit of $1 trillion. Because government outlays have to be funded, the government would have to secure some other sources of funding, such as borrowing or printing money, or new forms of taxes. The government is going to employ all sorts of means to obtain resources from wealth generators to support its activities. What matters here is not the deficit of $1 trillion but that government outlays are $3 trillion. If government revenue from higher taxes were $3 trillion, then we would have a balanced budget. But would this alter the fact that the government takes $3 trillion of resources from wealth generators?

According to the CBO data, government outlays are expected to fall in 2013 by $9 billion to $3.563 trillion after a projected decline of $40 billion in 2012.

Given that there is a time lag between government outlays and their effect on economic activity, it strikes us that it is the cut of $40 billion this year rather than the cut of $9 billion next year that should be of concern to various worried commentators.

We hold that an increase in government outlays sets in motion an increase in the diversion of real savings from wealth-generating activities to non-wealth-generating activities. It leads to economic impoverishment.

So in this context is it really bad news for the economy if on January 1, 2013, we have an automatic cut in government outlays? Most commentators such as the IMF and the CBO are of the view that cutting government outlays could inflict severe damage to the real economy.

We suggest that a cut in government outlays should be seen as great news for wealth generators. It is of course bad news for various artificial forms of life that emerged on the back of increases in government outlays.

What about the fact that we will also have an increase in taxes as a result of the expiration of the Bush tax cuts? To the extent that government outlays are going to be curtailed the increase in taxes should be regarded as a monetary withdrawal from the economy. In this sense it is like a tight monetary policy. A tighter monetary stance in this respect should be seen as positive for wealth generators since it weakens various bubble activities that sprang up on the back of past loose monetary policies.

(Conversely, a reduction in taxes while government spending goes up is not a tax reduction as such but should be viewed as loosening in the monetary stance. Again, an increase in government amounts to an increase in effective tax. The government has to divert resources from wealth generators to support the increase in spending.)

Note that the CBO projection of the future state of the US economy is in terms of GDP. Given that GDP is in fact monetary turnover, its ultimate course is going to be dictated by the rate of growth of the money supply. The more money that is pumped, the stronger GDP is going to be.

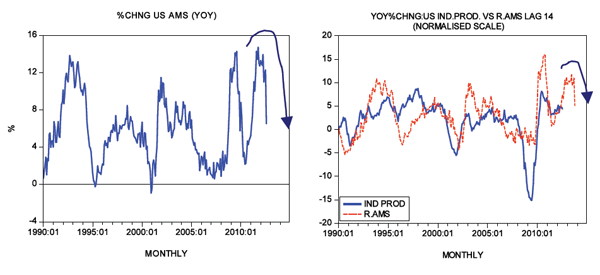

Contrary to the CBO and most commentators, we suggest that what is likely to undermine the growth momentum of GDP next year is the current visible decline in the growth momentum of money supply. In the week ending August 13 our monetary measure, AMS, fell by $70.9 billion from July. The yearly rate of growth of AMS fell to 6.5 percent from 12.3 percent in July. Observe that in October last year the yearly rate of growth stood at 14.7 percent.

As a result the yearly rate of growth of real AMS (AMS adjusted for CPI inflation) fell to 5.1 percent in mid-August from 10.9 percent in July. Based on the lagged-by-14-months yearly rate of growth of real AMS, we can suggest that the growth momentum of industrial production is likely to weaken sharply from the second half of next year.

The growth momentum of industrial production and real GDP could be in trouble from the second half of next year, but the underlying economy should start strengthening. The demise of bubble activities will be good news for wealth generators.

Against the background of a still-weak labor market, we suspect that Fed officials are likely to introduce another massive pumping in a few months' time. Given the current time-lag structure, it is unlikely however that more pumping can avoid a decline in the pace of economic activity in terms of GDP from the second half of next year.

Summary and Conclusions

According to the US Congressional Budget Office, scheduled tax increases and spending cuts in 2013 (the so called "fiscal cliff") could reverse the current economic recovery. We suggest that a cut in government outlays is actually going to be good news to wealth generators. It is, however, going to be bad news for various nonproductive activities that emerged on the back of increases in government outlays. In the meantime, a serious threat to economic activity in terms of GDP is posed by a visible fall in the growth momentum of money supply. We suggest that the present fall in the growth momentum of money supply is likely to undermine the GDP rate of growth from the second half of next year.

Frank Shostak is an adjunct scholar of the Mises Institute and a frequent contributor to Mises.org. He is chief economist of M.F. Global. Send him mail. See Frank Shostak's article archives. Comment on the blog.![]()

© 2012 Copyright Frank Shostak - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.