Best Cash ISA Savings Account for New Tax Year 2013-14

Personal_Finance / ISA's Apr 06, 2013 - 12:52 PM GMTBy: Nadeem_Walayat

The new tax year commenced today, which brings a small reprieve for UK savers to at least protect themselves from the 20% to 40% theft (double taxation) on savings interest payments, even though that it is highly unlikely that any accounts will be able to beat the real inflation rate which tends to be about 1.5% above CPI or currently about 4%.

The new tax year commenced today, which brings a small reprieve for UK savers to at least protect themselves from the 20% to 40% theft (double taxation) on savings interest payments, even though that it is highly unlikely that any accounts will be able to beat the real inflation rate which tends to be about 1.5% above CPI or currently about 4%.

This time last year many savers could have picked up an cash ISA account paying as high as 4.5% for a 5 year fix but as the below table shows of the rates offered by the Halifax that the savings rates collapsed directly in response to the Bank of England's Funding for Lending Scheme that was announced in July 2012 that sought to provide the Banks with cheap money to entice lending to the general public that will total an estimated £80 billion over the 18 months of the scheme (that will be extended). The effect of which is that Banks are able to rely on Bank of England / UK Treasury funding for loans instead of Savings and thus savings interest rates crashed.

| Halifax ISA's | May 2012 | Sept 2012 | Nov 2012 | Mar 2013 | % Cut |

|---|---|---|---|---|---|

| Instant Access | 3% |

2.75% |

2.35% |

1.75% |

-41% |

| 1 Year Fix | 2.25% |

2.05% |

2.05% |

-9% | |

| 2 Year Fix | 4.00% |

3.25% |

2.25% |

2.5% |

-37% |

| 3 Year Fix | 4.25% |

3.75% |

2.35% |

3.00% |

-29% |

| 4 Year Fix | 4.35% |

3.80% |

2.40% |

3.05% |

-30% |

| 5 Year Fix | 4.50% |

4.15% |

2.60% |

3.10% |

-31% |

As stated in my last ISA update of September 2012, that I expected the ISA interest rates to improve as the end of the tax year approached -

Therefore the cash ISA savings rates are just so bad that none of the crime syndicate that masquerades as our banks deserves mentioning, instead probably the best strategy is to wait until early next year as the best rates tend to materialise during March and April of each year i.e. to coincide with end of tax years and start of the following years, therefore it maybe better to either wait or opt for an instant access ISA now, in which respect the rates are still catastrophically poor so again not worth mentioning.

Therefore cash ISA savers have perhaps a 4-6 week window to pickup tax free savings accounts before probability favours the rates being cut once more as occurred during 2012 as the Bank of England and government continue to funnel tax payer cash into what still mostly remain bankrupt banks that await the next domino (Slovenia? Spain? Portugal? Italy? Greece? France?) to tip them over the edge once more.

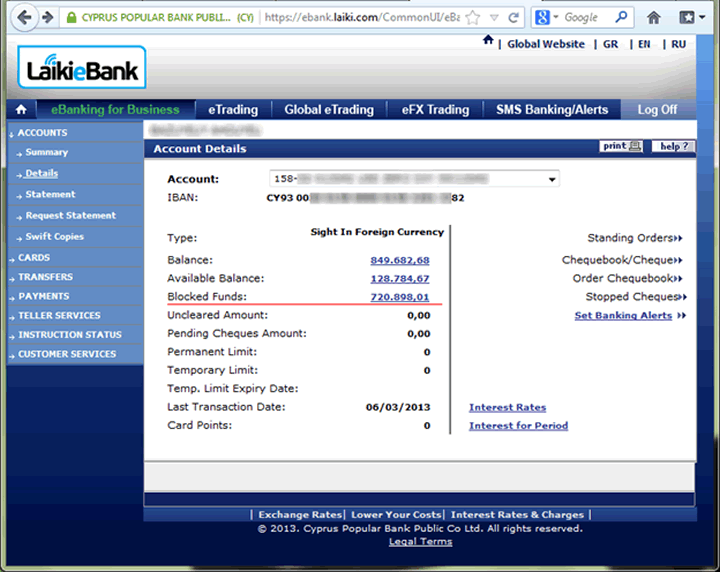

Cyprus Shows Your Deposits are at Risk

Banking crisis shockwave's continue to emanate out of Cyprus as an original 20% hair-cut of depositor funds in the countries two largest banks continues to double, and now triple to at least 60% to be stolen, whilst real life experience of those with bank accounts in Cyprus suggest that the immediate theft is 85%, and maybe they will only get back 20% in 6 or 7 years time as the following real life example illustrates to what amounts to an 85% theft of this customers bank balance at Laiki Bank actually looks like -

Source - So, What's It Like To Have a Business in Cyprus Right Now?

Writes the account owner:

"Most circulating assets on our business Current Account are blocked. Over 700k of expropriated money will be used to repay country's debt. Probably we will get back about 20% of this amount in 6-7 years.

I'm not Russian oligarch, but just European medium size IT business. Thousands of other companies around Cyprus have the same situation.

The business is definitely ruined, all Cypriot workers to be fired. We are moving to small Caribbean country where authorities have more respect to people's assets."

In respect of which UK depositors must stick to the £85,000 FSCS guarantee and ensure you have limited exposure to euro-zone banks.

My overall strategy remains as I have voiced in several ebook's (FREE DOWNLOADS) and hundreds of articles over the past 5 years of the financial crisis which is to leverage my wealth to the unfolding exponential inflation mega-trend as illustrated by the below graph.

To be in receipt of ongoing strategies on how to protect your wealth from ongoing Inflation theft, ensure you remain subscribed to my always FREE newsletter.

Best Cash ISA?

Baring in mind the ongoing systemic fraud perpetuated against savers, the following will seek to represent the least loss of purchasing power against an estimated real inflation rate of 4% that at least protects against the 20-40% tax on savings.

Another point to consider is that most instant access ISA's taken out a year ago will likely be seeing their 12 month bonuses end, so this is a good time to review and plan to move existing ISA's ahead of expiry of bonus rates.

Given the abysmal rates on offer at the moment many people may be questioning if its worth opening an ISA at all, in which respect I suggest savers focus on the long-game which is to get as much of your bank deposits into tax free accounts as possible with a view to fixing them at a later date for multiple years as I repeatedly advocated doing in the 6 months leading upto the financial crisis of October 2008 -

08 Oct 2008 - UK Interest Rate Forecast 2009

Savers - To reiterate what I have been saying over the last 6 months, savers still have a a golden opportunity to lock in high fixed savings rates which in the UK are above 7% . These rates won't stay around for much longer, were talking perhaps in the days rather than weeks or months. So the time for action is now ! - Yes, banks can go bankrupt but savings are protected which includes accumulated interest. In the UK the protection is for the first £50k per banking group.

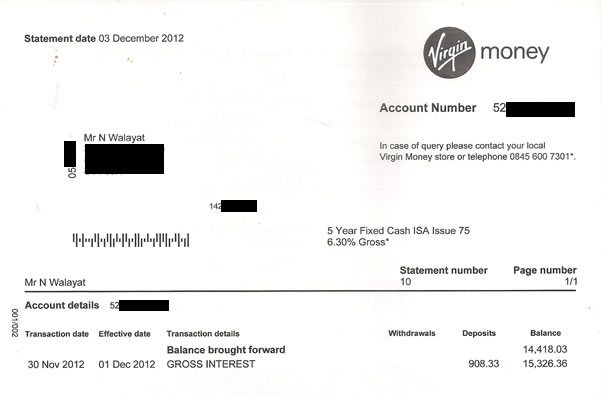

In which respect I am still personally in receipt of rates of as much as 6.3% per annum on fixed rate cash ISA's taken out during 2008 (non ISA accounts tended to pay 1% more interest per annum), though all of these are set to mature this year as illustrated below (Northern Rock ISA- taken over by Virgin):

So where cash ISA's are concerned, play the long-game and wait for savings rates to rise then lock them in for as long as possible to beat both inflation and the tax man. Remember that rates can only remain low as long as the Bank of England retains control of the bond market, which as the euro-zone illustrates that confidence is always fragile i.e. it does not take much to tip bond investor perceptions from low risk to extreme high risk especially as UK, US, German and Japanese bond markets ARE in the mother of all bubbles.

In the meantime Richard Branson's Virgin continues to pay me 6.3%, which is about triple the rate being offered to new Virgin Cash ISA customers.

Best Instant Access ISA

| Financial Institution | Interest Rate | Minimum £ | Comments |

| Santander | 2.5% | £2,500 | Direct ISA - Includes a 2% bonus for 12 months for balances less than £10k, allows transfers is. |

| NS&I | 2.25% | £100 | Does not allow transfers in, rate completely variable i.e. could be dropped within a month! - 100% Safe. |

Best Notice ISA

| Financial Institution | Interest Rate | Minimum £ | Comments |

| Coventry BS | 2.6% | £1 | 60day notice account. Includes a 0.6% bonus for 12 months. No transfers in. Note a month ago Coventry was paying 2.8%. |

Best Current Fixed Rate ISA's (1 Year)

All of the 1 year accounts are rubbish, in terms of interest rates offered you would be better off with an instant access account.

Best Current Fixed Rate ISA's (2 Year)

| Financial Institution | Interest Rate | Fixed Period | Minimum £ | Comments |

| Santander | 2.8% | 2 years | £1 | Boosted to 3% if you hold a 123 current account. Allows transfers in. You have until 30th May 2013 to add to the account. Extra bonus of 0.10% possible if Rory McIlroy wins at Golf. |

| Halifax | 2.5% | 2 Years | £500 | Allows transfers in. Early withdrawals allowed subject to 180days loss of interest. |

Best Current Fixed Rate ISA's (3 Year)

| Financial Institution | Interest Rate | Fixed Period | Minimum £ | Comments |

| Halifax | 3% | 3Years | £500 | Allows transfers in. Early withdrawals allowed subject to 270days loss of interest. |

Summary of ISA Rules & Benefits

- The ISA accounts are TAX FREE, and do not have to be entered onto any tax returns. The equivalent taxable return on a 3% cash ISA for standard rate tax payers is 3.6%. For higher rate tax payers it is 4.2%.

- The income from tax ISA's does not count against many mean tested benefits such as Tax Credits.

- The Allowance for 2013-14 is £11,520, £5,760 for cash and £5,760 for shares ISA's or the whole £11,520 into a shares ISA.

- You can only open ONE New cash ISA per tax year, and you can add new monies to One Cash ISA per tax year (see transfers). Similarly you can open only one new Shares ISA per tax year.

- You do not have to open a Cash ISA with your existing provider, i.e. you can open an account at different providers every year.

- Most providers allow for transfers in. And ALL should allow you to transfer out.

- Once you withdraw from a Cash ISA you cannot then then re-deposit into. The £5,760 limit refers to total deposited, and not maximum account balance. So if you deposit £5,760, and withdraw £1000, then you cannot re-deposit that £1000 in the same tax year as you have used up your £5,760 deposit limit.

- To maximize your tax free interest, it is best to open your account at the start of the tax year.

- The Financial Services Compensation Scheme (FSCS) guarantees the first £85,000 (Euro 100,000) per person, per banking licence . Those with sizable savings that total more than £85,000 should ensure that their institutions really are separate, especially given the banking crisis forced mergers.

- There is the facility to transfer Cash ISA monies into Shares ISA's but NOT from Shares ISA's to Cash ISA's .

- Next years Cash ISA allowance (2014-15) will increase inline with CPI inflation to around £5,880.

Source and Comments: http://www.marketoracle.co.uk/Article39827.html

Nadeem Walayat

Copyright © 2005-2013 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved.

Nadeem Walayat has over 25 years experience of trading derivatives, portfolio management and analysing the financial markets, including one of few who both anticipated and Beat the 1987 Crash. Nadeem's forward looking analysis focuses on UK inflation, economy, interest rates and housing market. He is the author of four ebook's in the The Inflation Mega-Trend and Stocks Stealth Bull Market series.that can be downloaded for Free.

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 600 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 600 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Nadeem Walayat Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.