Gold Long-term Irreversible Forecast Trend to $10,000

Commodities / Gold and Silver 2013 Apr 10, 2013 - 05:46 PM GMTBy: Nick_Barisheff

The long-term “irreversible” trends I’ve discussed in detail in my upcoming book, $10,000 Gold, continue to develop. Many of the trends, such as debt creation and the movement away from the U.S. dollar, are accelerating and their consequences are appearing globally. Today we will interpret how these developments will likely affect the price of gold over the coming year and beyond.

The long-term “irreversible” trends I’ve discussed in detail in my upcoming book, $10,000 Gold, continue to develop. Many of the trends, such as debt creation and the movement away from the U.S. dollar, are accelerating and their consequences are appearing globally. Today we will interpret how these developments will likely affect the price of gold over the coming year and beyond.

Perhaps the most prevalent indication that something is amiss with the world’s economy is a sense of malaise that many have been experiencing—a distrust in the financial system and the government. A U.S. Gallup poll, completed at the end of November 2012, found politicians to be the second least trusted individuals in society next to car salespeople. Sharing bottom marks were bankers, journalists, business executives, state governors and insurance salespeople. By contrast, nurses were the most trusted.

This level of distrust is global. Ask any Greek what he or she thinks of bankers and politicians who, through their complex bond deals, have destroyed the country’s economy. Ask the people of Iceland, who ignored the bankers’ demands for more money and instead threw them in jail. Such distrust is a tangible indication that the 41-year-old experiment in a global fiat currency system is failing.

At this stage, it is no surprise to see that those who benefited from this system are stepping up their PR campaign. Their goal is to bolster trust in paper currencies. Such campaigns are broad-based. As James Rickards, author of Currency Wars pointed out, the world is in the midst of an economic war between countries, currencies and gold. Developing countries are challenging the U.S. dollar’s de facto reserve currency status, and many in the East are turning to physical gold. The Western financial media insists on supporting the status quo with their positive messages of imminent economic recovery, but many are not buying it and the global appetite for physical gold is the best indication of this.

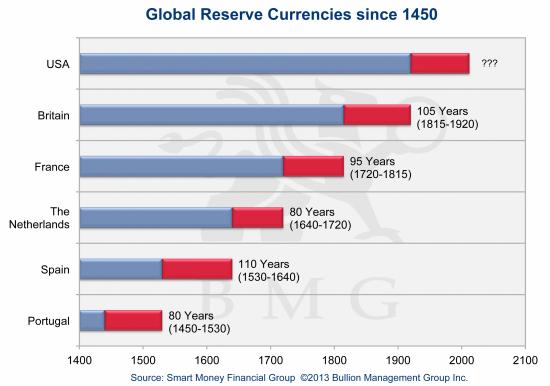

It should come as no surprise that the U.S. petrodollar is facing challenges. Reserve currencies go through cycles that last about a century as can be seen from the reserve currency chart. They usually end when the country that has this exalted privilege creates too much currency and goes too deeply into debt, just as the United States is demonstrating.

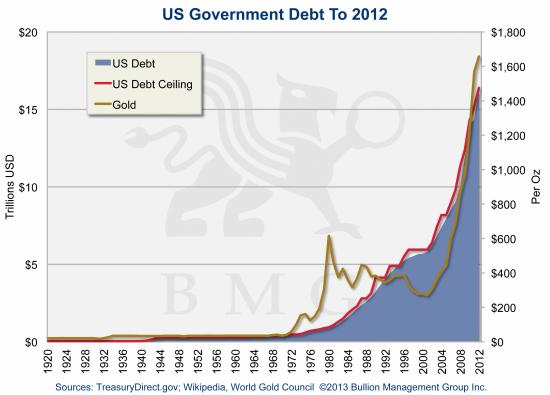

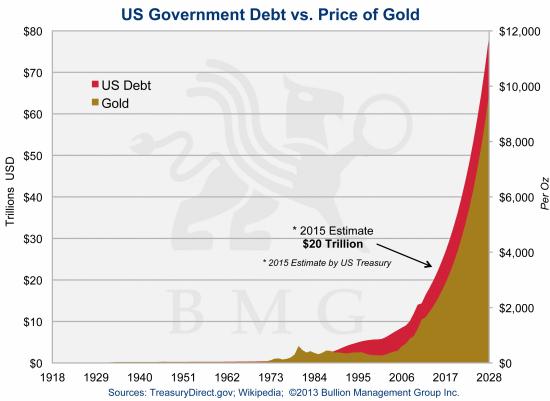

As in any war, “Truth is the first casualty,” but how do we distill the truth from so much complex and contradictory financial information? The answer is simple: by changing perspective; by using gold as our measure for financial assessment. The gold vantage point is more comprehensive. It allows us to see the hidden influences of inflation, for example. It helps us to understand why governments are doing what they are doing, despite their words to the contrary. `The fiat experiment officially began on August 15, 1971, the day President Nixon broke the U.S. dollar’s final international peg to gold. This allowed governments to create unrestricted amounts of currency with none of the safeguards that gold backing otherwise demanded. Consequently, the debt is now so large it is impossible to pay back. In the words of Congressman Ron Paul, the United States is “technically bankrupt.” So let’s start by looking at the most important influence on the price of gold—global government debt. Global DebtGovernment debt creation through currency debasement causes paper currencies to lose purchasing power against the more stable economic standard of gold. In fact, there is a direct relationship between debt and the price of gold. The Relationship to Gold and U.S. Debt chart, which was the centerpiece of last year’s Outlook for Gold, shows the gold price rising in near lockstep with rising U.S. debt over the past decade.

|

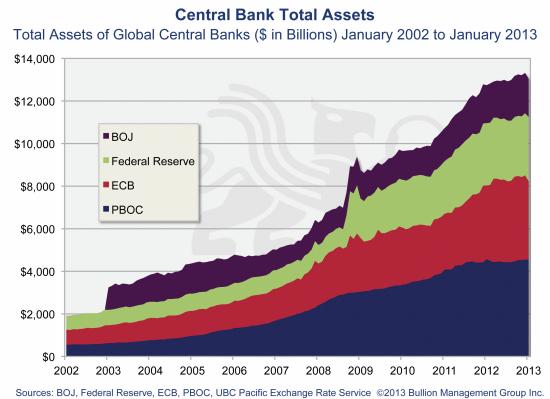

The increase in central bank assets is a good indicator of how this debt is growing.

|

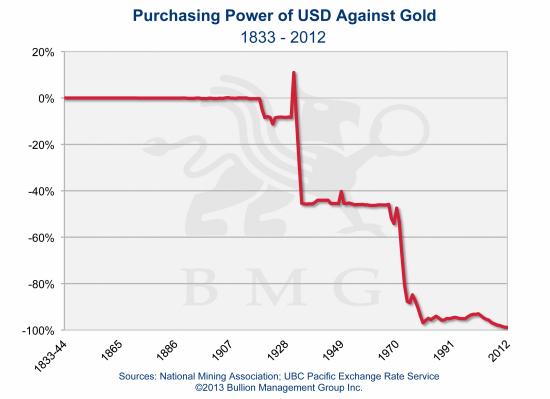

Between 2007 and 2012 Bank of England reserves increased by 362 percent, and the U.S. Fed’s increased by 223 percent. Unfortunately, as the people of Greece have discovered, most of the bailout cash stays in the hands of banks, even though the taxpayer is expected to repay the lenders. Although all the major currencies have lost purchasing power against gold, the chart shows the dramatic demise of the U.S. dollar. Being the world’s de facto reserve currency, it is by far the largest and most important, and the reason we give so much attention to the financial health of our southern neighbour. We can see that while backed with gold the dollar maintained purchasing power. In 1934 it lost its domestic peg to gold and then, in 1971, its international peg. The dollar has now lost 98 percent of its purchasing power since 1934.

|

U.S. federal debt is now growing exponentially. In his first term, President Obama added more debt than was added since the United States declared its independence from Britain in 1776. Another milestone: In Obama’s first term, the U.S. debt to GDP ratio passed 100 percent. At the present time, U.S. national debt is $16.4 trillion and GDP is $15.5 trillion. Interest payments on the debt were $454 billion in 2011. The U.S. Treasury "balance sheet" does not include the unfunded liabilities of Medicare, Social Security and other outsized and very real obligations. The actual liabilities of the federal government—including Social Security, Medicare, and federal employees' future retirement benefits—already exceed $86.8 trillion, or 550 percent of GDP. These figures are kept from the public eye and are not listed on official balance sheets. They can be found in obscure documents like the annual Medicare Trustees' report. Some estimates put total U.S. unfunded liabilities at well over $200 trillion. In 1984, in what might have been the last serious attempt of the U.S. government to address the problem of the rising debt, President Reagan’s Grace Commission report stated that: “With two-thirds of everyone's personal income taxes wasted ((on government excess)) or not collected (because of underground economy)), 100 percent of what is collected is absorbed solely by interest on the Federal debt and by Federal Government contributions to transfer payments. In other words, all individual income tax revenues are gone before one nickel is spent on the services which taxpayers expect from their Government.” It is safe to say that most of what this 1984 report warned against—that trillion-dollar federal debts would become reality if action was not taken immediately—has become reality. Political Options to Counter Debt To address the issue of runaway debt, politicians have five choices:

One: Grow out of it through increased productivity and increased exports. This is highly unlikely, as Western economies, and even China, are poised for recession. Two: Introduce strict austerity measures to reduce spending. This has the unwanted short-term effect of increased unemployment, lower tax revenues and reduced GDP, resulting in even higher deficits. And the voting public hates it. The U.S. government has shown no willingness to take this path. Three: Default on the debt. This will make it difficult to raise future bond issues at any reasonable level of interest rates. Four: Issue even more debt, and have the central bank in question simply create whatever amount of currency is required. Five: Follow a program of “financial repression.” The four main pillars of financial repression are:

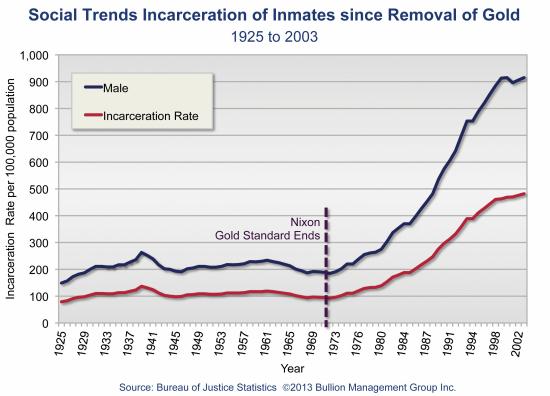

Obviously, governments around the world have chosen to fight this currency war and their ballooning debt with options four and five. The fiscal cliff fiasco of December 2012 proved that the majority of U.S. politicians will not risk their careers by implementing the more direct, more responsible option two or three. Financial Repression and Negative Real Interest RatesThis is a topic for a more in-depth presentation, but as 2012 confirmed, financial repression has become the unmistakable policy of governments worldwide. We will be hearing much more about this policy over the coming years. According to Bridgewater, the frequency of protests, strikes, and social unrest increases sharply as soon as annual public spending is cut by more than 3 percent of GDP. This unrest is appearing globally. In Greece, where the government has attempted to implement austerity measures, there is 20 percent unemployment in the 30 to 50 age group, and 58 percent youth unemployment. Greece’s homeless rate has risen 25 percent since 2009, with 20,000 people living in the streets of Athens. Suicide rates, violent crime and HIV infections are all rising quickly. This is what happens when society begins to break down because of debt. Youth unemployment is exceptionally high in most countries, especially the United States, which further burdens its young people with crippling student loans. Rising crime rates are another symptom of the increased stress currency devaluation causes. This chart on Social Trends Incarceration of Inmates since the removal of gold we can see the rapid rise in crime since 1971.

|

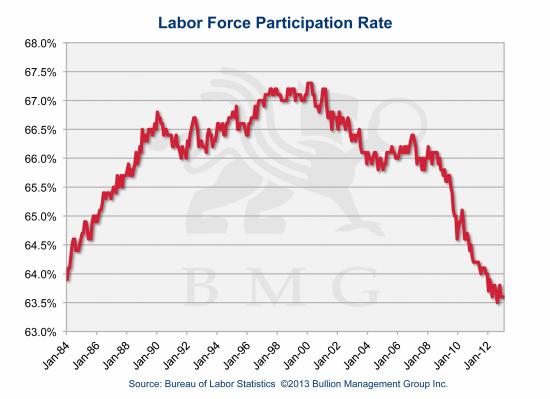

Despite the government job reports that put unemployment at 7.8 percent, those who have stopped looking for work after years of failing go uncounted. As soon as unemployment benefits run out, a job seeker is no longer registered as unemployed by the official figures. We can see that the job participation in the United States is plummeting, due in large part to the aging population and outsourcing.

|

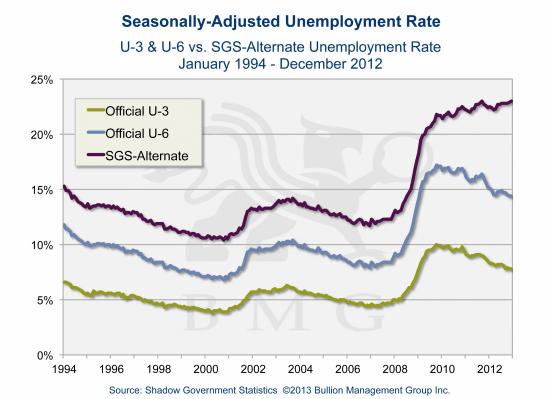

When we take into account the lack of participation, as the Shadow Stats figures show, we see real unemployment in the U.S. is over 20 percent.

|

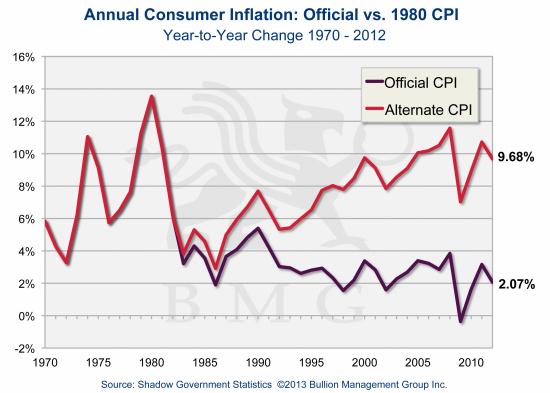

Financial repression involves restrictions on bank lending practices, which dries up available financing and stifles economic growth and development. This is a subtle form of nationalization, as it discourages investment abroad. A more obvious form of nationalization comes as restrictive trade laws. One example is the U.S.’s Foreign Account Tax Compliance Act (FATCA), enacted in 2012 with the cooperation of fifty countries. This makes it much more difficult for Americans to hold investment funds based outside of the United States. Larger government and further nationalization of industry are aspects of financial repression policy. In the United States, distressed financial institutions, automakers and healthcare are coming under the control of government, especially under the Obama presidency. Most of the new jobs created are government jobs, with five hundred thousand U.S. government employees making over $100,000 per year (twice that of the average U.S. workers’ salary). Financial repression is becoming a global policy as the currency war amongst countries like China, Russia and the United States accelerates. China has been using financial repression since 2000, with official inflation pegged at 0.72 percent from 2002 to 2009. This creates negative real interest rates of -7.2 percent, which gives China some of the lowest real interest rates in the world and explains why it is such a large gold buyer. Negative real interest rates can be determined by subtracting real inflation from official inflation or Real Interest Rate = Nominal Interest Rate - Inflation (Expected or Actual). There is a direct correlation between gold buying and negative real interest rates that are encouraged by financial repression. Negative real interest rates, despite governments’ incessant promises of economic recovery, will likely be with us for years to come. This policy rewards borrowers, but punishes savers. Currency debasement, which results from creating too much currency and is one of the elements of financial repression, is surreptitious in that the public is less aware of the damage. Inflation caused by currency creation is the “hidden tax”. Everyone who eats, drives, heats their home or sends their children to college is aware that life is becoming more costly by the day. Yet government continues to issue inflation figures that show the cost of living is stable. They have achieved this deception since the days of Bill Clinton through “creative” accounting, such as removing food and energy from the “basket of goods” used to measure inflation and the CPI. Before 1995, the CPI measured a “fixed standard of living” with a fixed basket of goods. Today it measures the cost of living with a constantly changing basket of goods, measured with metrics that are themselves constantly changing. Fortunately, economist John Williams of ShadowStats.com keeps track of the original basket and his figures show inflation at a more realistic level. |

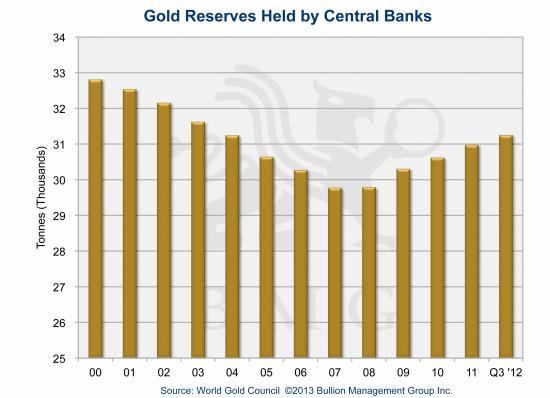

Further ConsequencesMovement away from petrodollarLast year saw several important BRICS and ASEAN agreements that exclude the U.S. dollar. In March 2012, Brazil, Russia, India, China and South Africa (BRICS) agreed to development banks that will allow these countries to trade amongst themselves without using U.S. dollars. In 2012, China also signed important trade agreements with Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Singapore, Thailand, Vietnam and the Philippines, which are members of the ASEAN alliance. They will trade in yuan rather than U.S. dollars. China and India are rumoured to be circumventing Iranian trade sanctions by trading gold for Iranian oil. The foreign appetite for U.S. Treasuries is also waning and the Fed is subsequently being forced to buy United States’ debt. It is expected to buy up to 90 percent of new debt created in 2013. This situation creates restriction on available Treasuries, which will continue to push down absolute yields. The developing world has had enough of the U.S. economic domination that has been in force since the 1944 Bretton Woods agreement. OPEC’s backing of the U.S. dollar in 1973, which required oil to be traded only in U.S. dollars, stopped the greenback’s rapid slide that began when the gold peg was removed two years earlier. As the developing world continues to find ways around this petrodollar arrangement, the U.S. dollar will find itself in serious trouble as its weak fundamentals, rather than its reserve currency status, are used for valuation. The Federal Reserve currently holds about 18 percent of the U.S. GDP on its books, a number that could bulge to 28 percent a few years out depending on the continuation of or increase in current programs, and growing distrust in U.S. fiscal responsibility. Increased Preference for Physical Gold over Paper GoldPrivate investors are pulling out of the markets and are even showing distrust in gold proxies such as gold shares and ETF shares in favour of the most trusted asset—physical bullion. By one estimate, physical demand will likely exceed ETF demand by five times. This is almost a complete reversal from a few years ago, when ETFs accounted for 80 percent of demand. “Backwardation” occurred in the gold price in 2012, which means the physical price exceeds the futures price. This indicates a stronger interest in physical over paper gold. Backwardation is a rare event in gold, as physical gold is one of the most liquid forms of money. Much of the world’s gold still exists and is available at the right price. Last year, 2012, began with slow gold coin sales; however, November saw the greatest volume in fourteen years, probably influenced heavily by Obama’s election, which guaranteed more spending and more debt. Central Banks are Buying GoldPerhaps the most significant consequence of runaway debt is that central banks have been net buyers of gold for the past three years, beginning in 2009. According to GFMS, in 2012, net official sector gold purchases totalled 536 metric tons. This is up 17.4 percent on the year. These figures do not include China’s central bank buying, which in the past occurred secretly through Chinese sovereign wealth funds that do not require the same degree of transparency central banks do. We know that China, as a country, bought more gold by August than the European Central Bank’s (ECB) entire 501 tonnes of holdings. This past year saw significant central bank buying from countries like Brazil, Iraq, Mexico, Thailand, South Korea and the Philippines, as well as by established buyers like Turkey, China, India and Russia. In fact, central banks bought more gold in 2012 than they have since 1964. German Repatriation of GoldGermany’s call for repatriation of some it’s gold from the United States and France is another indication of the monetary role central bankers are anticipating for gold in the coming years. Some gold watchers, like James Sinclair, feel this is a game-changing event and another example of loss of confidence in the U.S. government. When Venezuela demanded the return of its 160 tonnes of gold from the United States, it took only a few months to acquire. Why does Germany have to wait seven years for the U.S. Fed to deliver 300 tonnes? One obvious answer is the gold is not available at this time. Japan’s Monetization as Forerunner to U.S. MonetizationAlthough the United States is monetizing its debt through the Fed’s purchase of Treasuries, Japan is even further along this road and we can learn about the future of the U.S. economy by looking at Japan’s example. Japan, which has the worst balance sheet of any of the world’s developed nations, has survived partly because it is self-funded and is less dependent on foreign bond purchases. Japan’s death rate now exceeds its birthrate. The population is aging and retiring and therefore the Japanese public are becoming bond redeemers rather than bond buyers. As well, Japan’s relationship with China has soured significantly over the Japanese government’s decision to “nationalize” the Senkaku islands, which the Chinese claim as their own. The Japanese auto industry has suffered significantly. Japan has still not recovered from the Fukushima Daiichi nuclear disaster caused by the 2011 tsunami. Because of these developments, Japan’s central bank will buy 56 percent of the country’s issued treasury bonds this year. |

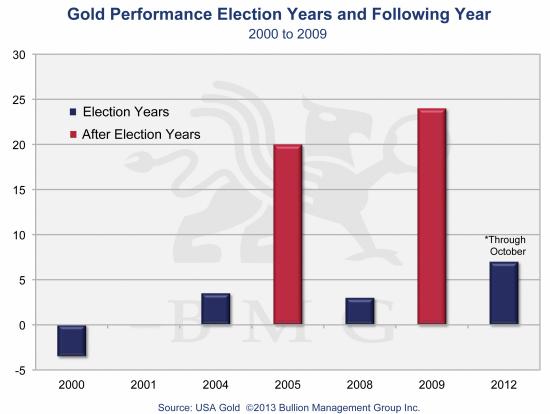

Complexity, Obfuscation and ScandalThis past year was also one of unprecedented complexity, obfuscation and scandal. These are symptoms of the final days of an economic system. There was the successful prosecution of a countrywide interest-rate rigging scandal that affected all fifty states, known as the Municipal Bond Scandal, or more specifically United States of America v. Carollo, Goldberg and Grimm. Then there was an even larger interest rate scandal, one that affected the entire world. Prosecutions in the Libor scandal, which was uncovered in July 2012, have already begun. Last year banks paid $10.7 billion in fines for such transgressions. White-collar corruption has never been so apparent, yet regulators seem to be no more interested in bringing this to the public’s attention than are the compliant media. Despite the blatant flaunting of the law during the subprime crisis, no major player has gone to jail or even been prosecuted. MF Global’s robbery of money from its client accounts, in broad daylight, not only went unprosecuted, but in January 2013 a judged nixed customers’ attempts to depose MF Global’s infamous CEO Jon Corzine. Mr. Corzine, of course, is the former head of Goldman Sachs and a former senator then governor of New Jersey. He is also a major fundraiser for President Obama. Wall Street alumni continue to make their way into political positions as the relationship between Wall Street and Washington becomes even more intimate. With the fox guarding the henhouse, there is little chance of this trend changing course. What Could Make Gold Prices Stop Going Up?With an endless stream of “green shoots” reports coming out of the mainstream financial media, gold continues to climb a “wall of worry”. This means that gold is still far from its exponential phase when people start lining up for miles to buy gold as they did in 1980, and despite temporary, healthy interruptions to its price ascent. However, many are still asking what will cause the price of gold to stop going up. Some mention U.S. resurgence after the much-ballyhooed shale oil fracking program that releases natural gas from shale and is supposed to make the U.S. energy independent. The United States did increase domestic oil production by 766,000 barrels per day during 2012, which resulted in the highest domestic production in fifteen years. Foreign oil now supports just 41 percent of American demand, down from 60 percent seven years ago. Fracking is a dangerous and expensive practice that is unpopular with environmentalists and primarily provides natural gas, which cannot be stored as oil is stored. It will also require decades of infrastructure development. U.S. debt problems are systemic and, as the recent fiscal cliff stalemate indicated, the country may not have decades or even years to right its economic ship. Negative real interest rates would have to turn positive. Yet for every one percent of official inflation, the United States would have to add approximately $160 billion to its federal debt as indexed pensions and other inflation-sensitive obligations would become much more expensive, as would borrowing to meet these costs. Raising interest rates in this environment will be almost impossible due to the massive amounts of global debt. In 1981 when Fed chief Paul Volcker raised interest rates as high as 21.5 percent, with official inflation at 7.5 percent, it stopped the flow of currency into gold. This could never happen today, as the United States owes far too much debt to make high interest rates viable. A deep recession in countries like India and China that are major gold buyers could negatively impact the price of gold. However, history shows that such harsh economic conditions in countries that believe so strongly in gold may have the opposite effect and cause even more capital to flee to the protection gold offers. People become even more serious about wealth preservation in times of crisis. Little, short of discovering how to make gold from salt water, will change the primary direction of gold, which for the coming years is upward on its way to $10,000 an ounce and beyond. Where is gold heading in 2013?This year, 2013, will likely be a more positive year for gold than 2012, if history is a reliable indicator. Over the past decade, since gold began to regain its stature as money, U.S. election years have been lacklustre for gold and the following year has shown a significant rise in price. |

Currently, it takes very little for short-term optimism about gold to turn bearish. This is further indication that gold has much further to rise. Each time a hedge fund or government intervention causes a precipitous drop such as we saw twice in December, gold sentiment becomes weaker. Mark Hulbert of Hulbert Gold Newsletter Sentiment Index, or HGNSI, had this to say about negative sentiment towards gold: “. . .of the last three decades has shown that, at the 95% confidence level that statisticians often use to assess whether a pattern is most likely genuine, gold tends to do better in the wake of low levels of bullish sentiment (like now) than in the wake of excitement and enthusiasm”. - Mark Hulbert This past year, 2012, showed a strong negative bias amongst most sentiment indicators such as the Hulbert Survey and Market Vane. This is a strong contrarian signal for the coming year. The Gold and Debt over the next decade chart shows the projection of U.S. debt, assuming gold will continue the same close relationship with debt as demonstrated in the historical gold and debt chart discussed earlier. |

ConclusionGold’s price is directly proportionate to the massive amount of debt that is being created to keep the current fiat system alive. This will likely continue until a crisis, such as a severe global recession or hyperinflation, strikes one of the major developed economies. Either event will be bullish for the gold price, but for different reasons. The price is being driven by the physical market in the developing countries, especially India and China. China has to continue buying as much physical gold as possible if they expect to eventually compete for world reserve currency status. Some estimates state the Chinese hope to have at least 10,000 tonnes to out-rank their main competitor for gold holdings—the United States. In 2012, the world mined gold production was approximately 2,700 tonnes. Of which India and China bought nearly 2,000 tonnes between them. Over the past five years, emerging markets accounted for 70 percent of gold demand. The question of who actually owns the United States’ gold is debatable and made particularly opaque by complex, highly secretive gold lease agreements. The increased calls for gold repatriation and for audits of Fort Knox and the U.S. Federal Reserve could shed light on this issue in the coming years. This is the perfect time to hold gold and silver for wealth protection. Fund redemptions, negative institutional sentiment, financial repression and the raging currency war ensure gold will continue its climb towards $10,000 an ounce. I expect that gold will end 2013 between $1,900 and $2,000 an ounce, and silver between $40 and $45 an ounce. In a world where financial and geopolitical certainty is evaporating, no one knows what Black Swan event could cause an explosion in the gold price. Some have suggested it will be the failure of a major bank through derivative exposure, or a Middle East war. A major downgrade of U.S. bonds might also be the catalyst. In 2013, as has been the case since 2001, the best policy for wealth protection remains to simply buy and hold uncompromised bullion until we are once again on solid economic footing. Thank you, |

In my new book, $10,000 Gold: Why Gold's Inevitable Rise is the Investor's Safe Haven, published by John Wiley and Sons and to be released in May, I discuss the long-term and irreversible trends that will lead to $10,000 gold. The book looks more deeply at the issues discussed above. It also describes how investors can protect their wealth through precious metals ownership, just as many in the developing nations have been doing methodically for the past decade.

Each week BMG presents a free newsletter called the BullionBuzz that is a compilation of articles, charts and videos that follow the developing trends that will lead to $10,000 gold.

By Nick Barisheff

Nick Barisheff is President and CEO of Bullion Management Group Inc., a bullion investment company that provides investors with a cost-effective, convenient way to purchase and store physical bullion. Widely recognized in North America as a bullion expert, Barisheff is an author, speaker and financial commentator on bullion and current market trends. He is interviewed monthly on Financial Sense Newshour, an investment radio program in USA. For more information on Bullion Management Group Inc. or BMG BullionFund, visit: www.bmginc.ca .

© 2012 Copyright Nick Barisheff - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.