U.S. Dollar and Assets - America’s ‘Exorbitant’ Privilege Will Continue

Currencies / US Dollar Apr 19, 2013 - 10:28 PM GMTBy: Richard_Mills

In July 1944, delegates from 44 nations met at Bretton Woods, New Hampshire - the United Nations Monetary and Financial Conference - and agreed to “peg” their currencies to the U.S. dollar, the only currency strong enough to meet the rising demands for international currency transactions.

In July 1944, delegates from 44 nations met at Bretton Woods, New Hampshire - the United Nations Monetary and Financial Conference - and agreed to “peg” their currencies to the U.S. dollar, the only currency strong enough to meet the rising demands for international currency transactions.

Member nations were required to establish a parity of their national currencies in terms of the US dollar, the "peg", and to maintain exchange rates within plus or minus one percent of parity, the "band."

What made the dollar so attractive to use as an international currency was each US dollar was based on 1/35th of an ounce of gold, and the gold was to held in the US Treasury. The value of gold being fixed by law at 35 US dollars an ounce made the value of each dollar very stable.

The US dollar, at the time, was considered better then gold for many reasons:

- The strength of the U.S. economy

- The fixed relationship of the dollar to gold at $35 an ounce

- The commitment of the U.S. government to convert dollars into gold at that price

- The dollar earned interest

- The dollar was more flexible than gold

There’s a lesson not learned that reverberates throughout monetary history; when government, any government, comes under financial pressure they cannot resist printing money and debasing their currency to pay for debts.

Lets fast forward a few years…

The Vietnam War was going to cost the US $500 Billion. The stark reality was the US simply could not print enough money to cover its war costs, it’s gold reserve had only $30 billion, most of its reserve was already backing existing US dollars, and the government refused to raise taxes.

In the 1960s President Lyndon B. Johnson's administration declared war on poverty and put in place its Great Society programs:

- Head Start

- Job Corps

- Food stamps

- Medicaid

- Funded education

- Job training

- Direct food assistance

- Direct medical assistance

More than four million new recipients signed up for welfare.

During the Nixon administration welfare programs underwent major expansions. States were required to provide food stamps. Supplemental Security Income (SSI) consolidated aid for aged, blind, and disabled persons. The Earned Income Credit provided the working poor with direct cash assistance in the form of tax credits and welfare rolls kept growing

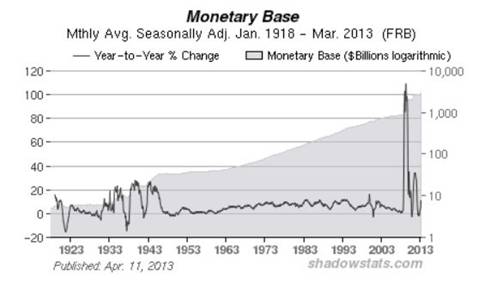

Bretton Woods collapsed in 1971 when Nixon severed (known as the Nixon Shock because the decision was made without consulting the other signatories of Bretton Woods, even his own State Department wasn’t consulted or forewarned) the link between the dollar and gold – the US dollar was now a fully floating fiat currency and the government had no problem printing more money. With gold finally demonetized the US Federal Reserve (Fed) and the world’s central banks were now free from having to defend their gold reserves and a fixed dollar price of gold.

The Fed could finally concentrate on achieving its mandate - full employment with stable prices - by employing targeted levels of inflation. The Fed’s ‘Great Experiment’ had begun – the objective being a leveling out of the business cycle by keeping the economy in a state of permanent boom - gold's "chains of fiscal discipline" had been removed.

But there was a problem - because of the massive printing of the US dollar to cover war and welfare reform costs Nixon worried about the strength of his country’s currency – how do you keep the U.S. dollar as the world’s reserve currency, how do you keep demand strong, if one you remove gold’s backing and two print it into oblivion?

Recognizing that the US, and the rest of the world, was going to need and use more oil, a lot more oil, and that Saudi Arabia wanted to sell the world’s largest economy (by far the US) more oil, Nixon and Saudi Arabia came to an agreement in 1973 whereby Saudi oil could only be purchased in US dollars. In exchange for Saudi Arabia's willingness to denominate their oil sales exclusively in U.S. dollars, the United States offered weapons and protection of their oil fields from neighboring nations.

Nixon also abolished the International Monetary Fund’s (IMF) international capital constraints on American domestic banks. This allowed Saudi Arabia and other Arab producers to recycle their petrodollars into New York banks.

Global oil sales in U.S. dollars caused an immediate and strong global demand for US dollars – the ‘Petrodollar’ was born.

By 1975 all OPEC members had agreed to sell their oil only in US dollars in exchange for weapons and military protection.

“In a nutshell, any country that wants to purchase oil from an oil producing country has to do so in U.S. dollars. This is a long standing agreement within all oil exporting nations, aka OPEC, the Organization of Petroleum Exporting Countries. The UK for example, cannot simply buy oil from Saudi Arabia by exchanging British pounds. Instead, the UK must exchange its pounds for U.S. dollars…

This means that every country in the world that imports oil—which is the vast majority of the world's nations—has to have immense quantities of dollars in reserve. These dollars of course are not hidden under the proverbial national mattress. They are invested. And because they are U.S. dollars, they are invested in U.S. Treasury bills and other interest bearing securities that can be easily converted to purchase dollar-priced commodities like oil. This is what has allowed the U.S. to run up trillions of dollars of debt: the rest of the world simply buys up that debt in the form of U.S. interest bearing securities.” Christopher Doran, Iran and the Petrodollar Threat to U.S. Empire

As developed economies grew and prospered, as developing economies took center stage with their massive urbanization and infrastructure development plans their need for oil grew, and so too did the need for new U.S. dollars, as demand grew the currency strengthened. The U.S. Dollar quickly became the currency for global trades in almost every commodity and most consumer goods, it wasn’t used just for oil purchases anymore. Countries all over the world bought, had to buy, more and more dollars to have a reserve of currency with which to buy oil and ‘things.’ Countries began storing their excess US dollar capacity in US Treasury Bonds, giving the US a massive amount of credit from which they could draw.

There’s no disputing the U.S. greenback is the world's currency - the dollar is the currency of denomination of half of all international debt securities and makes up 60 percent of countries foreign reserves.

The Petrodollar replaced the Gold Standard

Currently the only source of backing for the U.S. dollar is the fact that oil is priced in only U.S. dollars and the world must use the Petrodollar to make their nation’s oil purchases or face the weight of the U.S. military and economic sanctions. Many countries also use their Petrodollar surplus for international trade - most international trade is conducted in U.S. dollars.

It’s very obvious that the United States economy, and the global economy, are both intimately tied to the dollar's dual role as the world’s reserve currency and as the Petrodollar.

“Trade between nations has become a cycle in which the U.S. produces dollars and the rest of the world produces things that dollars can buy; most notably oil. Nations no longer trade to capture comparative advantage but to capture needed dollar reserves in order to sustain the exchange value of their domestic currencies or to buy oil. In order to prevent speculative attacks on their currencies, those nations’ central banks must acquire and hold dollar reserves in amounts corresponding to their own currencies in circulation. This creates a built-in support for a strong dollar that in turn forces the world’s central banks to acquire and hold even more dollar reserves, making the dollar stronger still.” Harvey Gold, Iran’s Threat to the U.S. – Nuclear or the Demise of the Petrodollar?

It’s also very obvious that if global Petrodollar demand were ever to crumble the use of the U.S. dollar as the world’s reserve currency would abruptly end.

The consequences:

- Energy costs would rise substantially. American’s, because their dollar is the world’s reserve currency and they control it, have been buying oil and gasoline for a fraction of what the rest of the world pays.

- There would be substantially less demand for dollars and U.S. government debt. All nations that buy oil and hold U.S. dollars in their reserves would have to replace them with whatever currency oil is going to be priced in - the resulting sell-off would weaken the U.S. currency dramatically.

- Interest rates will rise. The Federal Reserve would have to increase interest rates to reduce the dollar supply.

- Foreign funds would literally run from U.S. stock markets and all dollar denominated assets.

- Military establishment collapses.

- There would be a 1930s like bank run.

- Dollar exchange rate falls. The current-account trade deficit would become unserviceable.

- The U.S. budget deficit would go into default. This would create a severe global depression because the U.S. would not be able to pay its debts.

Why some might think the Petro dollar is history, consider:

- Several countries have attempted to, or have already moved away from the petrodollar system – Iraq, Iran, Libya, Syria, Venezuela, and North Korea.

- Other nations are choosing to use their own currencies for inter country trade; China/Russia;China/Brazil;China/Australia;China/Japan;India/Japan;Iran/Russia; China/Chile; China/The United Arab Emirates (UAE);China/Africa Brazil/Russia/India/China/South Africa (the new BRICS are plus S.A.).

- Countries began storing their excess US dollar capacity in US Treasury Bonds, giving the US a massive amount of credit from which they could draw. But by keeping interest rates excessively low for so long a period of time, and with no relief in sight, the rate of return on U.S. interest bearing securities has been so low it’s not worth holding them to generate any kind of return for your U.S. foreign reserves, the very same reserves you want to hold to buy oil.

- The U.S. does not need its Arab Petrodollar partners as much since the invasion of Iraq with its immense oil resources (second largest in the world) and discovery of how to obtain oil from unconventional sources – shale oil, oil sands etc. Saudi Arabia and other OPEC countries in the region might be less needy for U.S. protection now that Iraq has been neutralized and Iran is in the crosshairs.

- Russia is the number one oil exporter, China is the number two consumer of oil and imports more oil from the Saudis then the U.S. does. Chinese and Russian trade is currently around US$80 billion per year. China has agreed to lend the world’s largest oil company, Russia’s Rosneft, two billion dollars to be repaid in oil.

- U.S. federal debt is close to 17 trillion dollars and is 90 percent of GDP. The deficit is a horrendous 7 percent of GDP. Political infighting and bickering has made cooperation nearly impossible and effective measures just aren’t being taken. The Federal Reserve is increasing its reserves by over a trillion dollars a year, the Fed is out of tools, its measures are not working. The ‘recovery’ is false, jobs are scarce and 6.2 million Americans have dropped out of the workforce.

Exorbitant Privilege

Valéry Giscard d'Estaing referred to the benefits the United States has due its own currency being the international reserve currency as an "exorbitant privilege."

“Reserve currency status has two benefits. The first benefit is seigniorage revenue—the effective interest-free loan generated by issuing additional currency to nonresidents that hold US notes and coins... The second benefit is that the United States can raise capital more cheaply due to large purchases of US Treasury securities by foreign governments and government agencies…The major cost is that the dollar exchange rate is an estimated 5 to 10 percent higher than it would otherwise be because the reserve currency is a magnet to the world's official reserves and liquid assets. This harms the competitiveness of US exporting companies and companies that compete with imports...

There is no realistic prospect of a near-term successor to the dollar. Although the euro is already a secondary reserve currency, MGI finds that the eurozone has little incentive to push for the euro to become a more prominent reserve currency over the next decade. The small benefit to the eurozone of slightly cheaper borrowing and the cost of an elevated exchange rate today broadly cancel each other. The renminbi may be a contender in the longer term—but today China’s currency is not even fully convertible.” McKinsey Global Institute,An exorbitant privilege? Implications of reserve currencies for competitiveness

The Alternatives

There has lately been a lot of talk about the demise of the Petrodollar. Fortunately, or unfortunately (depends what side of the debate your on) there exists no viable alternative to the U.S. dollar, not today, not tomorrow, not for a very long time.

The EU is a waste land, will the deeply flawed Euro even survive?

“The euro’s major weakness comes from its political base. If the entire 27-country strong European Union (EU) were backing the euro, its long-term international standing would be considerably enhanced. With only half of the E.U countries backing it, the euro zone is vulnerable in the future to a possible dissolution under the pressures of economic hardships. This is more so since the statutes of the European Central Bank are unduly rigid, not only freezing exchange rates between member states, which is OK, but also de facto freezing their fiscal policies, while the central bank itself has the goal of fighting inflation as its only objective. It seems that the objective of supporting economic growth was left out of its statutes, with the consequence that it may be unable to ride successfully future serious economic disturbances.” Prof Rodrigue Tremblay, Nothing in Sight to Replace the US Dollar as an International Reserve Currency

Well what about China you ask?

One of the preconditions of reserve currency status is relaxing capital controls so foreigners can reinvest their accumulated yuan back into a countries markets. China has strict capital controls in place. If they were to be relaxed to the level needed then market driven money flows, not China’s Communist leaders, would drive exchange and interest rates. Communist leaders would be facing the thing they fear the most – instability because they lose control over two of their main economic levers.

China has well over US$3.2 trillion in its foreign reserves. They’ve accumulated this massive amount of money over the years by maintaining the yaun’s semi fixed peg to the dollar.

Think about it; the euro-crisis makes the US dollar the preferred safe-haven, this lowers US borrowing costs. This in turn means China has to continue to lend to the US in order to hold-up the value of its current reserves, pushing down US borrowing costs.

A massive shift as many envision – China out of the U.S. dollar - would destroy the dollar and cause the instability the Communist Party fears so much. Why would China deliberately destroy its own wealth and why would Chinese communist leaders set themselves up for discord among its citizens?

“China, itself as a country, has a very limited moral international stance. It is still a totalitarian, authoritarian and repressive state regime that does not recognize basic human rights, such as freedom of expression and freedom of religion, and which crushes its linguistic and religious “minority nationalities. It is a country that imposes the death penalty, even for economic or political crimes…Only a fundamental political revolution in China could raise this country to a world political and monetary status. This is most unlikely to happen in the foreseeable future and, therefore, no Chinese currency is likely to play a central role in financing international trade and investment.” Prof Rodrigue Tremblay, Nothing in Sight to Replace the US Dollar as an International Reserve Currency

Conclusion

U.S. assets are free from default risk, free from political risk, the U.S. has never imposed capital controls and has only frozen funds once – Iran’s in 1978.

Fact; the United States of America, and only the United States of America, controls the fate of the Petrodollar. Not communist China, not Russia or Saudi Arabia or the EU.

The questionable ‘exorbitant’ privilege (the interest-free loans, U.S. Treasury purchases by foreign governments versus the loss of business competitiveness and all that entails) bestowed upon America for having the world’s reserve currency is going continue for the for-seeable future. This fact, and what it means to the U.S. and the world, should be on all our radar screens. Is it on yours?

If not, maybe it should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including:

Wall Street Journal, Market Oracle, SafeHaven , USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2013 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Richard (Rick) Mills Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.