Investing in Recession Proof Leading Brands Stocks

Companies / Investing 2013 Jun 06, 2013 - 04:27 PM GMT

The Volatility Is Risk Myth

The Volatility Is Risk Myth

If you were to take the essence of most people’s beliefs and understanding about investing in common stocks, or the stock market for that matter, and turn it into a movie, I believe it would have to be labeled under the category science fiction. In other words, in my experience, most of what people believe about common stocks or the stock market is predicated more on opinion than on fact. But even more importantly, it is predicated on opinions that are driven by strong emotional responses. Consequently, I believe that what most people feel that they know about investing in stocks is based more on myth than truth.

Perhaps the biggest myth of all is the perception that investing in common stocks is a risky endeavor. Whether you are listening to professional or lay investors alike, it is widely accepted that stocks are a risky asset class. Personally, I have found that the true risk of investing in the equity asset class rests more in the attitudes, beliefs and actions of the investors themselves, than it does with the asset class. In other words, how people think about common stocks is actually often more risky than the common stocks actually are. Unfortunately, most people think investing in stocks is risky; I don’t, as long as it’s done intelligently and correctly.

At this point, I should add that I am very compassionate regarding how people feel about their investments. I understand that long-term financial security is one of the most important and sacred issues that people must deal with. The fear of not having adequate resources to fund a secure long-term future is very strong. Our financial nest eggs represent our financial security, especially beyond our working years when we no longer work for money, but instead must depend on our money working for us. More simply stated, we cannot afford to lose what we have, and we are therefore justifiably very emotionally attached to our investment portfolios.

With the above in mind, I believe the biggest myth regarding investing in common stocks is that volatility equals risk. Moreover, in recent history, long-established sound and prudent common stock investing practices has given way to academia, more commonly known as Modern Portfolio Theory (MPT). I have explained this by coining the phrase “Ancient Portfolio Reality has been replaced by Modern Portfolio Theory.” My point being, that MPT has equated volatility with risk. Fancy mathematical formulas such as R squared, the Sharpe ratio, Correlation Coefficients and beta, etc., are all utilized as determinants of risk based on a measurement of volatility.

However, I intend to argue that the true risk of investing in common stocks relative to their volatility is how investors react to the volatility, rather than the volatility itself. I will illustrate later that volatility will only hurt you if you panic and sell, especially if you’re selling a strong business. More often than not, I will demonstrate that this usually causes you to sell a valuable asset for less than it is worth. This is the root idea behind the profound wisdom of Warren Buffett when he advises us to “be greedy when others are fearful, and fearful when others are greedy.”

Moreover, it’s important to understand that volatility is actually a side effect of one of the most salient features of investing in common stocks - liquidity. Therefore, when I see one of my good businesses fall below its intrinsic value, I see this as a temporary illiquid event. I never see it as losing my money, because I believe and understand that my business is worth more than the market is currently pricing it at.

I believe this because I’ve calculated the intrinsic value of the business I own based on its ability to generate cash returns on my behalf. I consider this more relevant and important than what an often fickle and irrational market may be temporarily pricing it at. Consequently, instead of panicking and taking an unnecessary loss, my more intelligent reaction is to look for ways to purchase more now that my great business has gone on sale.

All asset classes have their advantages and disadvantages over each other. I have always believed that the two greatest advantages of investing in common stocks were their unlimited profit potential and their liquidity. I’ve always preferred investing as an owner over behaving as a loaner. In other words, I prefer an equity interest in a good business over lending my money at interest.

Never Fear a Recession Again

At this point, I would like to focus the reader’s attention on the fact that this article is primarily dealing with the volatility risk aspect of investing in common stocks. The unavoidable volatility of stock prices elicits strong emotional responses in people, perhaps more than any other of the myriad risk factors associated with investing. Of course, I’m referring to the primary emotional responses fear and greed. Although both of these can create extreme damage to a person’s portfolio, I contend that fear is the most powerful and dangerous. Moreover, nothing elicits fear in the minds of investors more than the dreaded “R” word - Recession. When the prices of the stocks in their portfolios are dropping like a stone when in the throes of a recession, fear will quickly turn to panic. When panic sets in, terrible mistakes are usually made.

All of my remarks thus far are offered as a prelude supporting my thesis that if you invest in the stocks of the world’s leading brands, you would never need to fear a recession again. This is predicated on the simple reality that a company does not become a world’s leading brand without achieving a high level of business success. Therefore, the companies behind leading brands are almost by definition strong and reliable businesses to invest in. I would also like to remind the reader about my positioning statement in my opening paragraph which suggested that most people’s views about the stock market are founded on opinion rather than fact. Therefore, it is only appropriate that I present facts to support my thesis.

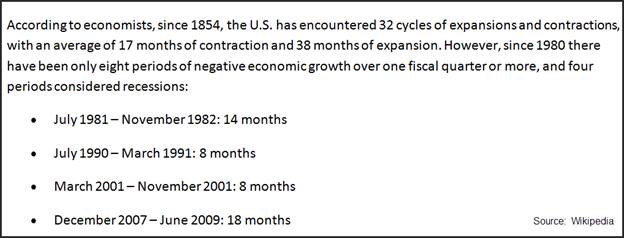

The first fact regarding a recession is that recessions do not imply the end of our economic well-being as we know it. Instead, recessions are temporary interruptions in the business cycle that although difficult to experience, usually end within two years and are followed by strong recoveries. Here are some facts regarding the recessions in the United States according to Wikipedia:

I think it is also appropriate to point out that our last recession, commonly referred to as the Great Recession, was one of the most severe on record. Furthermore, due to its severity and how recent it was, its memory remains very vividly in our minds. In fact, this recession was so severe, that even after four years of recovery, there are many people who are unfortunately still suffering emotionally from its effects. But even more importantly, and as it specifically relates to this article, there were and even continue to be, numerous horror stories told about how people lost their life savings and had their retirements ruined by the declines of their stock portfolios because of the Great Recession.

But even sadder yet, at least to my way of thinking, is how all the negative thinking associated with this catastrophic event has caused people to flee and/or avoid investing in America’s greatest businesses. But worse yet, the extreme fear that the Great Recession created caused more damage to people’s portfolios and financial futures than the Great Recession did itself. Fear caused so many investors to sell their stocks at precisely a time that the opportunity for investing in them was the greatest. Consequently, unnecessary losses that devastated so many people’s retirement portfolios should never have occurred.

The antidote to keep these things from happening is knowledge leading to decisions based on facts instead of emotion. Knowledge is power, and what follows is a series of factual information regarding how the stocks of 11 of the world’s leading brands fared during the Great Recession. But more importantly, this leads to an important and critical lesson about successfully investing in common stocks. The lesson is to focus more on the business behind the stock and less on the volatility of its share price. Learn to do this, and investing in common stocks becomes more intelligent, less risky and more profitable.

11 of the World’s Leading Brands

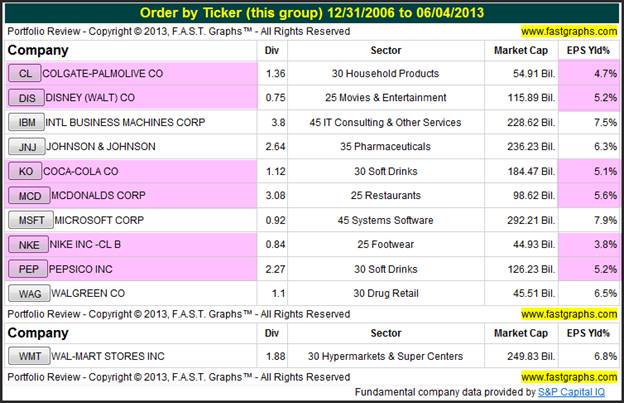

The following portfolio review lists 11 large-cap multinational companies each representing a world’s leading brand. All of these companies are established large-cap companies that pay a dividend. Furthermore, I believe that each of these leading brand companies are worthy of investing in, however, only when they can be purchased at sound valuations. Unfortunately, I believe that 6 of these 11 companies are currently too pricey to buy today (purple highlights on graph). On the other hand, I feel that only Nike (NKE) is so overvalued that it should be sold.

One of the valuation criteria that I personally rely on, is an earnings yield of 6% or higher, and the higher the better. Consequently, there are several names on this list that I believe are also currently buyable; the ones with an earnings yield about 6%. However, this article is not about whether any of these should be bought or sold today. Instead, it is about how they fared through the Great Recession of 2008. I believe these world’s leading brands offer valuable lessons about investing in blue-chip stocks.

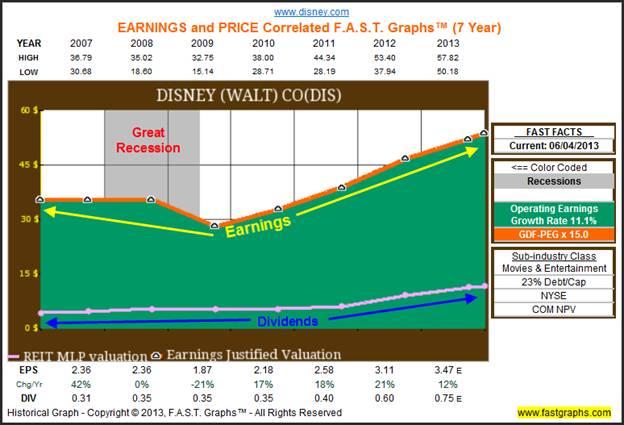

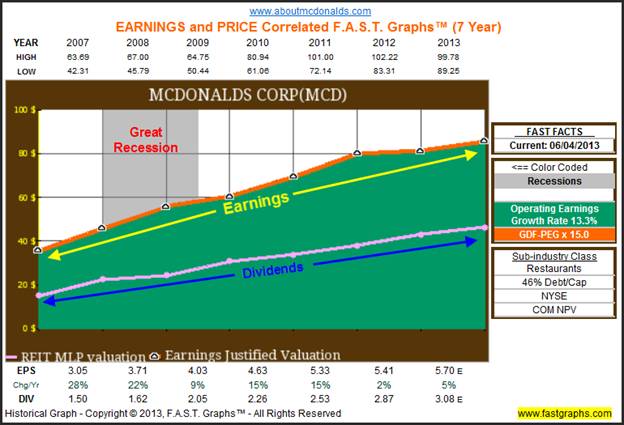

Next I will individually review each of these 11 world’s leading brand companies through the lens of F.A.S.T. Graphs™, the fundamentals analyzer software tool. I will examine the timeframe 2007, one year prior to the recession, to current time. My primary goal is to focus the reader’s attention on how well each of these blue-chip leading brands companies performed as businesses prior to, through and after the Great Recession. If you focus on the earnings (the orange line on each graph) of each of these great businesses, you will see that there was very little damage inflicted by the Great Recession. Only three of them, Disney (DIS), Coca-Cola (KO) and Microsoft (MSFT) experienced a very modest decline in earnings, but in all cases business interruption was very minor.

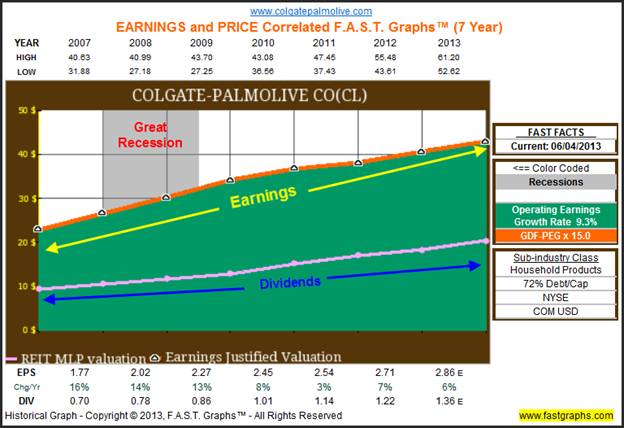

In order to get the maximum benefit out of each of the individual F.A.S.T. Graphs™, a few words of explanation as to what you’re looking at are in order. The first graph plots operating earnings (the orange line) which also represents the intrinsic value of the company. The green shaded area represents a mountain chart of all the earnings, and the pink line plots the company’s dividends over this time. The key take away from the first graph is to illustrate how strong each of these companies’ businesses were prior to, through and after the Great Recession. The pink line plotting dividends simply reinforces the strength underpinning each of these businesses.

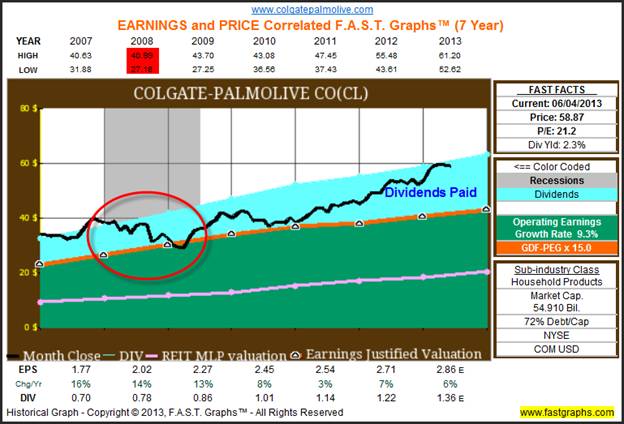

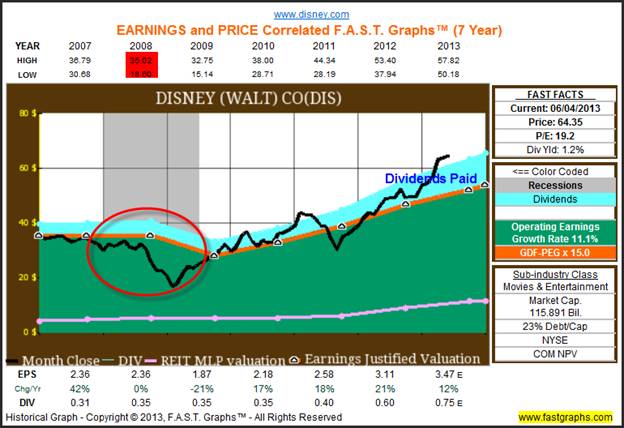

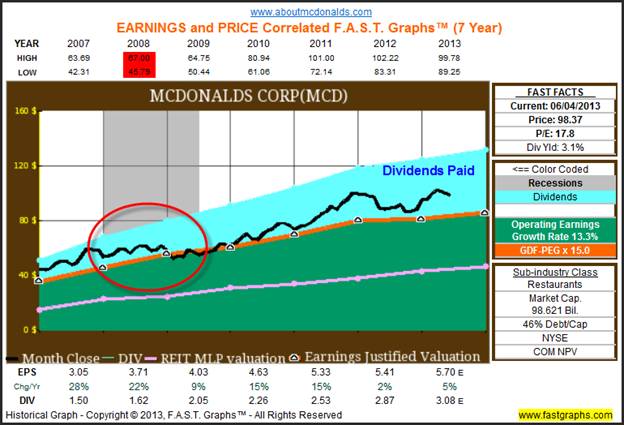

With the second graph, monthly closing stock prices (the black line) and the dividends paid out (the blue shaded area) are added to provide a perspective on how truly irrelevant the temporary price drops (price volatility) were. Although some of the price drops are significant on a percentage basis, the reader should also note how quickly they recovered based on the underlying strength of the businesses behind the stock price. I’ve highlighted the high and low prices in 2008 to illustrate the severity of the price drops during the recession. But the reader should also note that each of these companies is trading at new all-time highs currently.

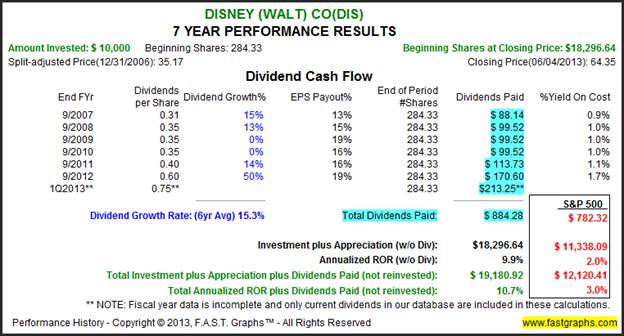

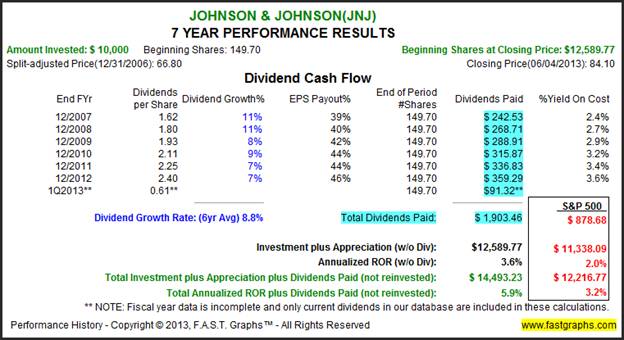

The performance graph associated with the 2007 to current time period illustrate how good an investment each of these world’s top brand companies were even during the recession. As long as you didn’t sell when the price originally dropped, your long-term rewards were clearly exceptional in each case. Capital appreciation was significantly better than the S&P 500, and no shareholders of any of these great businesses would have experienced a cut in their income. In fact, if these 11 names represented a retirement portfolio, the owner would have actually received an increase in pay each year.

Since a picture is worth 1000 words, I’m going to let the graphs speak for themselves. As you review each company, notice how their earnings held up, which allowed their stock prices to recover even after dropping during the panic of the Great Recession. Also, spend some time reviewing the performance results, taking special note of the dividends paid column. Do this thoroughly, and I believe the only rational conclusion that can be made is that if you own the right businesses, you never have to fear another recession again.

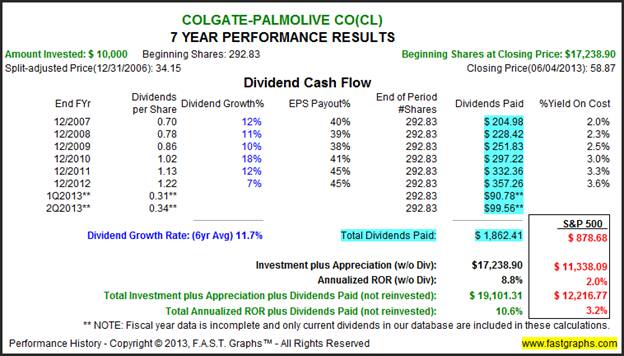

Colgate-Palmolive Co (CL) Est. 1806 – 207 Years

Earnings never missed a beat during the Great Recession. Consequently the company increased its dividend every year.

During the Great Recession the stock price fell from $40.99 to $27.18, a 33.7% drop. Today Colgate trades at an all-time high price of $58.87.

Disney (Walt) Co (DIS) Est. 1923 – 90 Years

Earnings did drop in fiscal 2009, but soon recovered. The company’s dividend was temporarily frozen, but began rising again in 2011.

During the Great Recession the stock price fell from $35.02 to $18.60, a 47% drop. This would have only hurt you if you panicked and sold, as Disney currently trades at an all time high of $64.35.

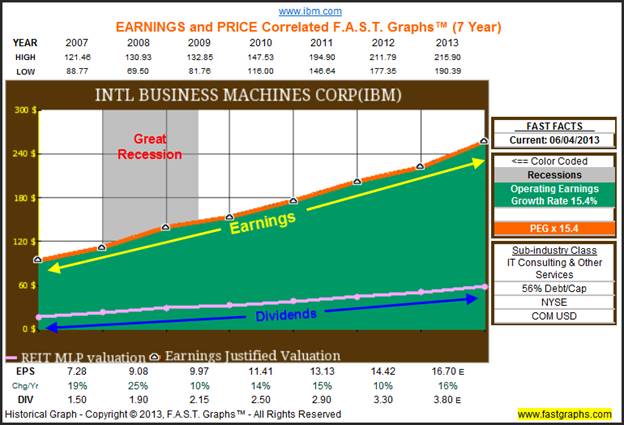

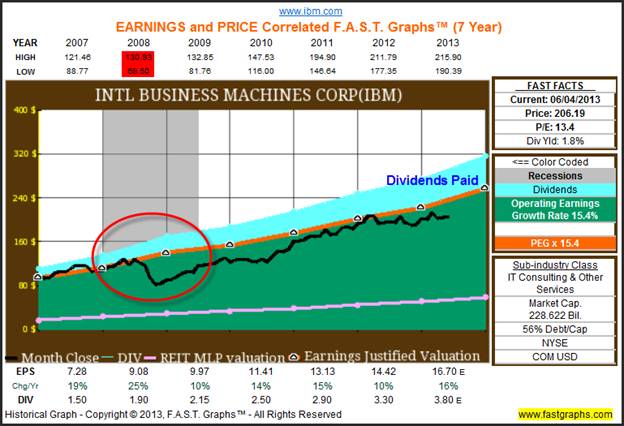

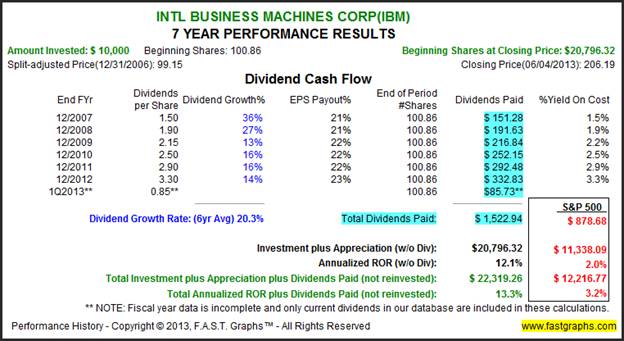

International Business Machines Corp (IBM) Est. 1911 – 102 Years

IBM had one of its best years in recent history during the Great Recession as earnings grew over 25% in fiscal 2008. Regarding IBM’s business results, there was no Great Recession.

Inspite of IBM’s great operating results, its stock price fell from $130.93 to $69.50 during fiscal 2008 equallying a 47% drop. However, the drop was temporary as IBM currently trades at an all time high of $206.19.

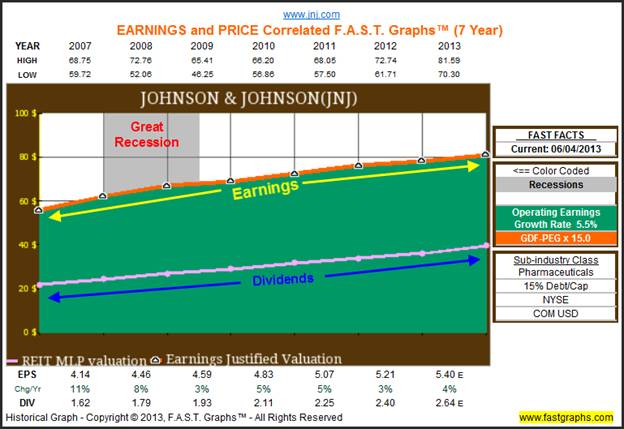

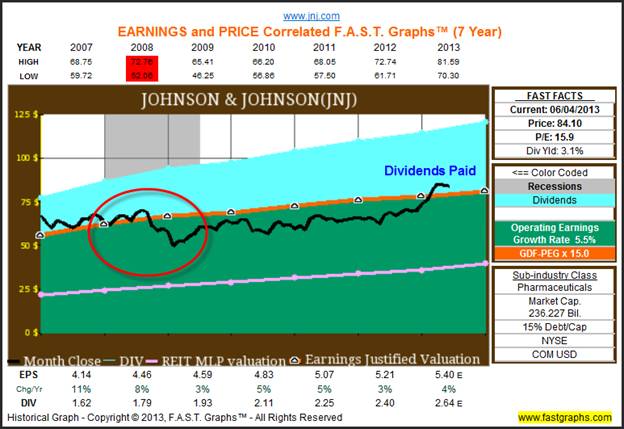

Johnson & Johnson (JNJ) Est. 1886 – 127 Years

Johnson & Johnson’s earnings held up extremely well during the Great Recession with very little impact. Consequently, the company was able to continue increasing its dividend each year.

Johnson & Johnson’s stock price did fall from $72.76 to $52.06, representing a temporary 28% drop. However, its stock price did recover and currently trades above its 2008 high.

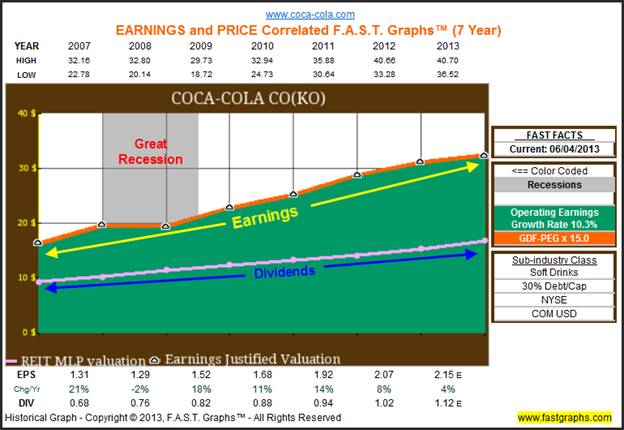

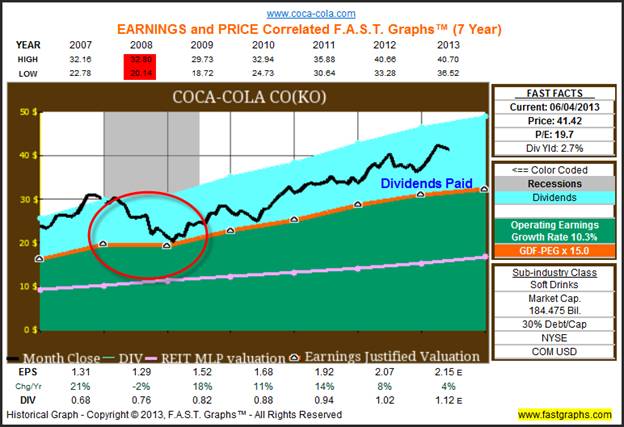

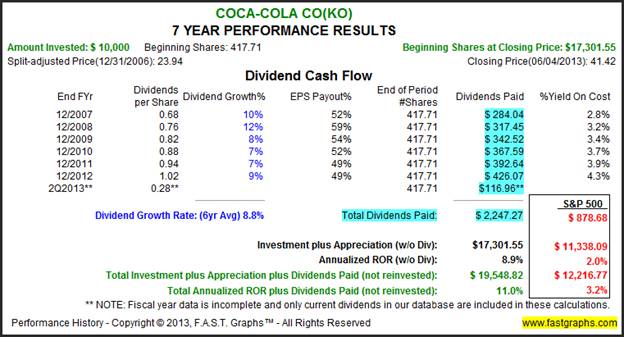

Coca-Cola Co (KO) Est. 1886 – 127 Years

Coca-Cola’s earnings did flatten a little during the Great Recession, but have recovered at an above-average rate ever since. Consequently, Coca-Cola raised its dividend each year.

Coca –Cola’s stock price fell from $32.80 to $20.14, representing a 38.6% drop. However, it should be noted that Coca-Cola’s stock price was technically overvalued at the beginning of 2008. Nevertheless, the current stock price of $41.42 exceeds its 2008 high. Once again, price volatility would have only hurt those that panicked and sold in spite of Coca-Cola’s premium valuation just prior to the recession.

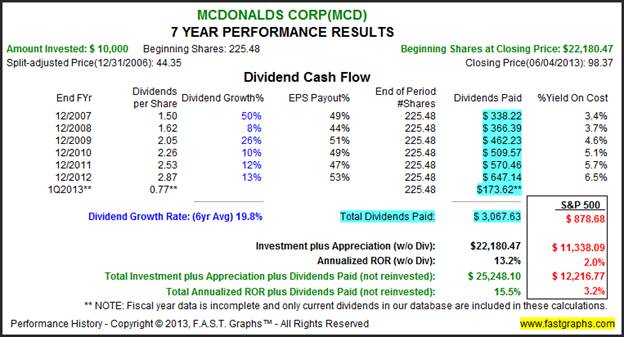

McDonalds Corp (MCD) Est. 1940 – 73 Years

There was no Great Recession for McDonald’s business. Nevertheless, McDonald’s dividend growth rate in 2008 was lower than normal, perhaps indicating prudent behavior by management.

Interestingly, McDonald’s stock price did fall from $67.00 to $45.79, representing a 31.6% drop. However, by looking at the graph it could be argued that this price drop was more related to beginning overvaluation in 2008 than to the Great Recession.

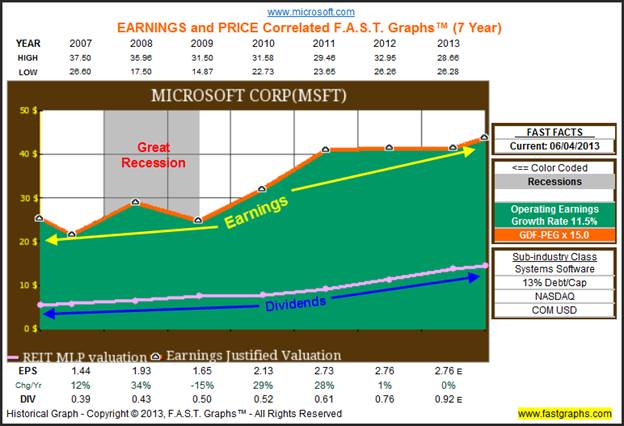

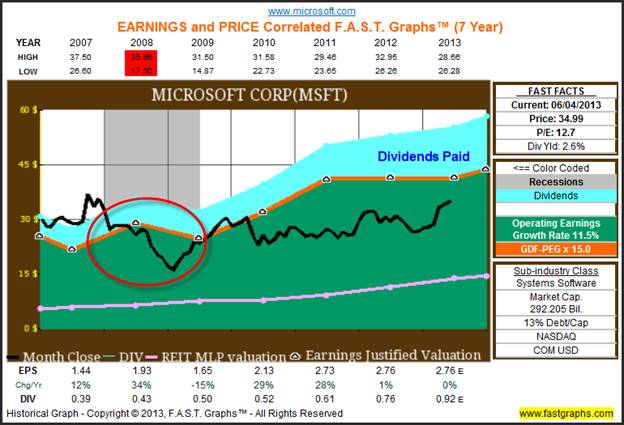

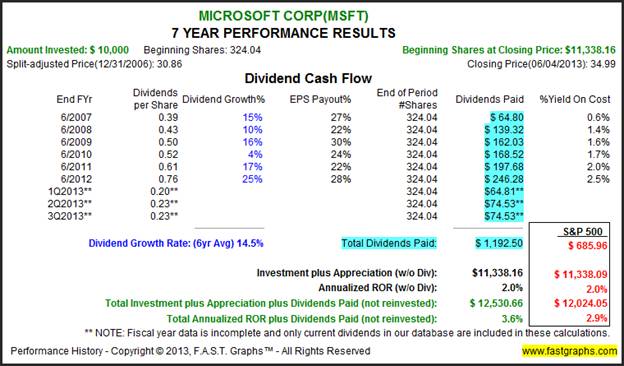

Microsoft Corp (MSFT) Est. 1975 – 38 Years

The Great Recession did impact Microsoft’s earnings in fiscal 2009. However, fiscal 2010 and 2011 recovered strongly as they came off of a low base.

Although Microsoft saw its stock price fall over 50%, from $35.96 to $17.50, it could be argued that there were other factors besides the Great Recession involved. First was overvaluation in the fall of calendar year 2007, then we saw an earnings drop in fiscal 2008 as a result of the Great Recession. However, Microsoft’s stock price has recovered to $34.99 at the close on June 4, 2013.

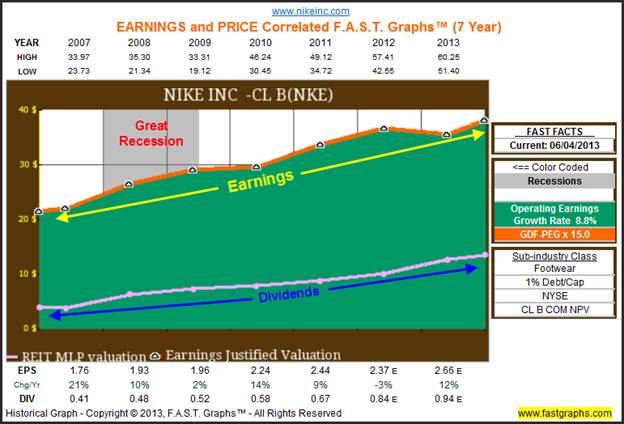

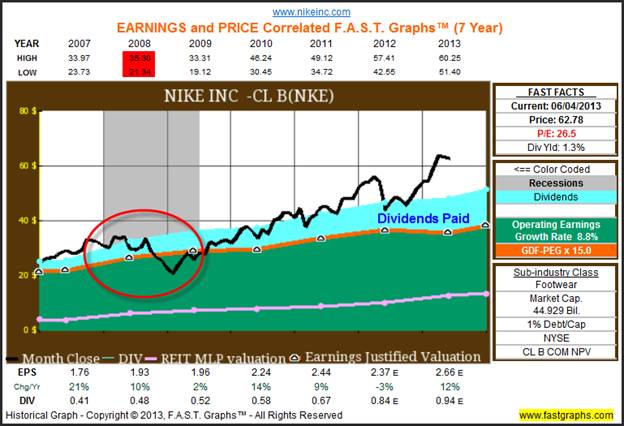

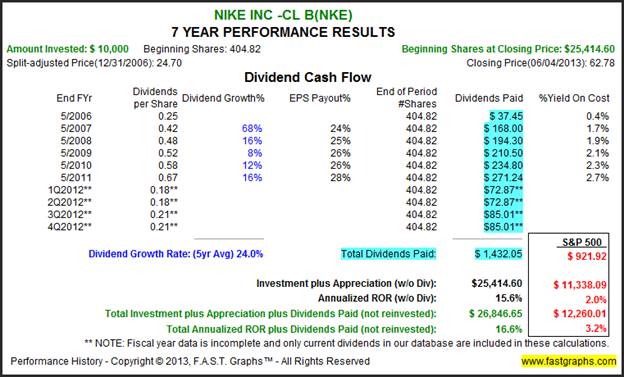

Nike Inc (NKE) Est. 1964 – 49 Years

Nike only experienced a flattening of earnings during the Great Recession. Consequently, they were able to raise their dividend each year.

Nike’s stock price fell 40% from $35.30 to $21.34 during the Great Recession. However, as the graphic illustrates, emotions towards Nike’s stock subsequently went from negative to euphoric.

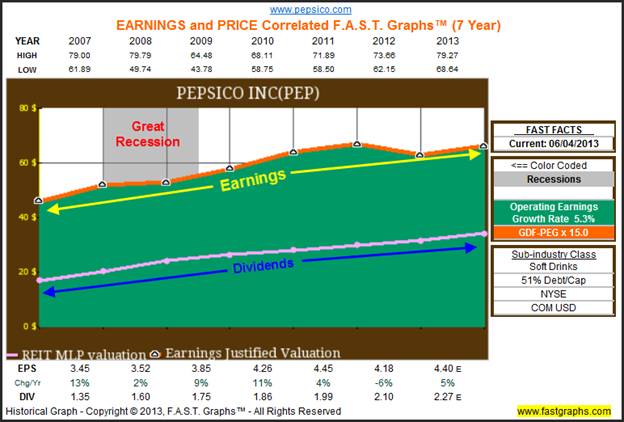

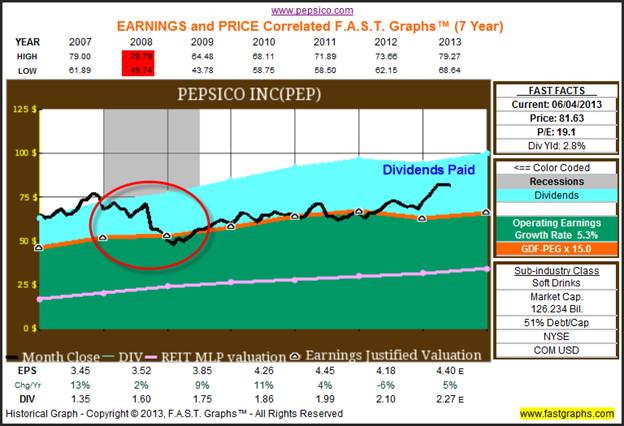

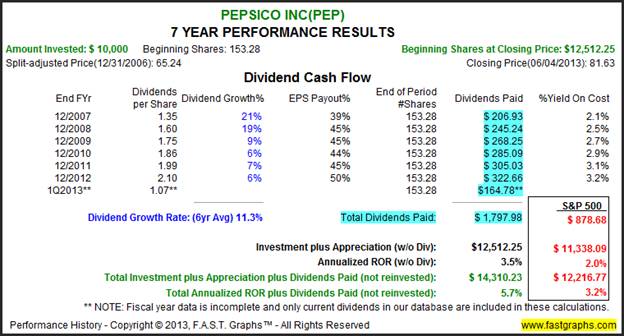

PepsiCo Inc (PEP) Est. 1965 – 48 Years

PepsiCo also experienced a minor flattening of earnings during the Great Recession. Nevertheless, they still increased their dividend every year.

PepsiCo’s stock price fell 38% from $79.79 to $49.74 in 2008, however, note the premium valuation that was on the shares at the time. Nevertheless, they raised their dividend each year, and price is now moving back to its typical premium valuation.

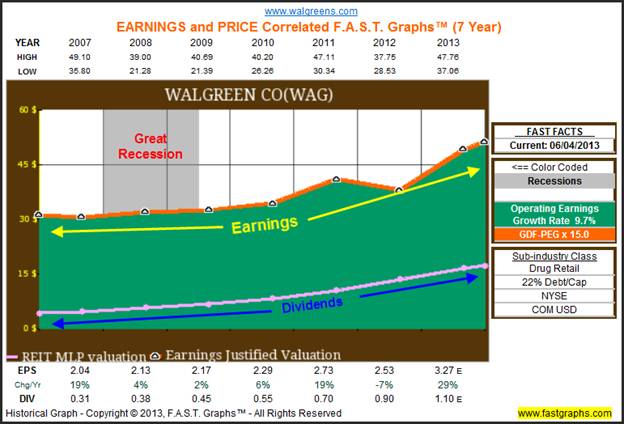

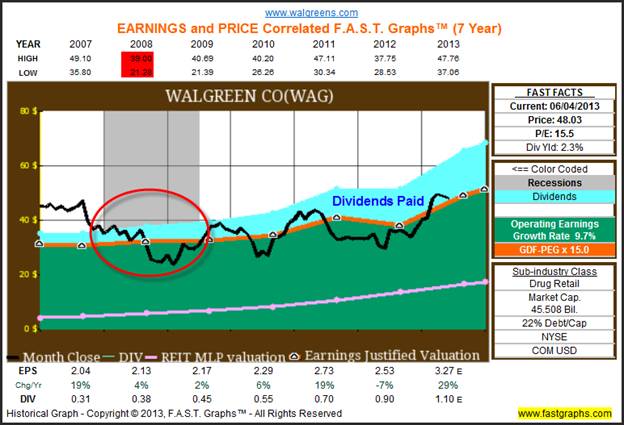

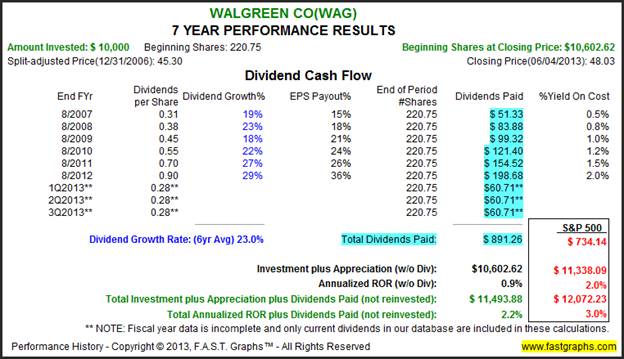

Walgreen Co (WAG) Est. 1901 – 112 Years

Walgreens remained profitable during the Great Recession although growth did slow a bit. Nevertheless, they raised their dividend each year.

Coming into 2008, Walgreen’s stock price was significantly overvalued. In calendar year 2008, Walgreen’s stock price fell from $39.00 to $21.28, a 45% drop. Nevertheless, Walgreen’s continued profitability allowed them to raise their dividend.

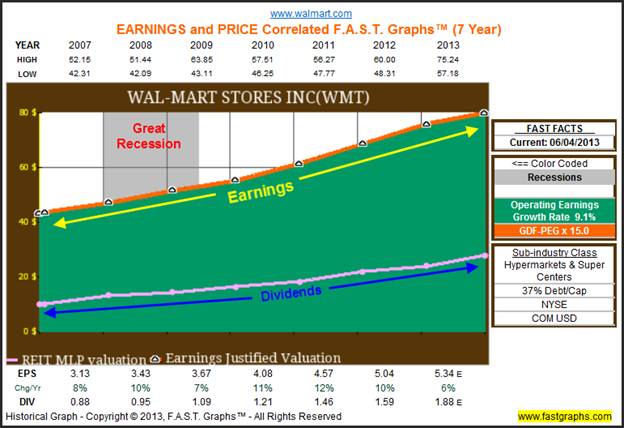

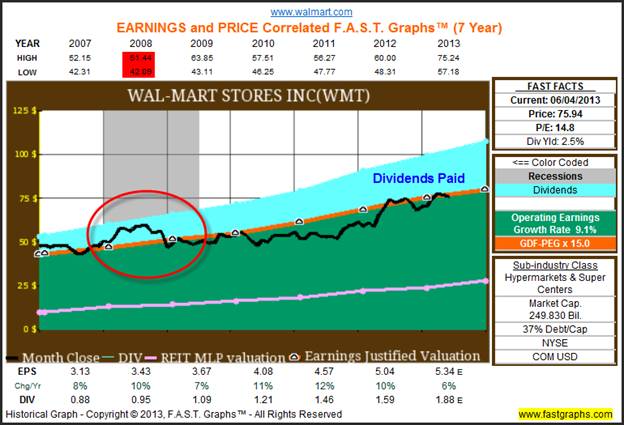

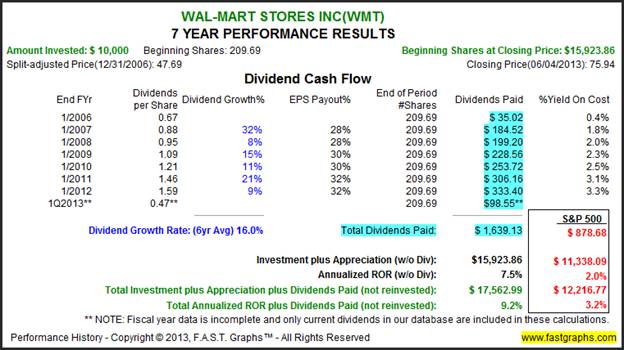

Wal-Mart Stores Inc (WMT) Est. 1962 – 51 Years

It could be argued that the Great Recession was actually a positive for the world’s leading low-cost retailer. Both earnings and dividends increased during the Great Recession as if it never happened.

The strength of Wal-Mart’s business even protected it share price. In 2008, Wal-Mart’s stock fell from a high of $51.44 to $42.09, representing a modest 18% drop relative to other companies. Consequently, they continued to raise their dividend at a double-digit rate.

Summary and Conclusions

The primary thesis behind this article is that volatility does not necessarily equate to risk. Instead, how a person reacts to volatility is quite often where most of the risk of investing in equities actually rests. Moreover you’ll notice that none of these companies cut their dividend, however, Disney did freeze theirs for a couple years. The point being that, retirees depending on these companies for the income they produced would not have been affected by the Great Recession at all in the long run.

The hardest lesson, but also perhaps the most important lesson, is that it’s more rational, reliable and profitable to focus more on the business behind the stocks you own than it is to focus on the day-to-day volatility of their prices. Stock prices are often pathological liars, and therefore, decisions based on price movement will often lead investors astray. In other words, a rising price can engender greed causing the investor to buy when they should be selling, and conversely a falling price can engender fear causing the investor to sell when they should be buying.

I also want to point out that it’s important to recognize that this article is focused on companies representing some of the world’s best brands. As I previously pointed out, this also implies companies that are best-of-breed and/or blue-chip dividend paying stalwarts. In other words, these are the crème de la crème of companies that this article is written about. My point being that not all companies were able to perform as well as these blue-chips did during the Great Recession. However, I also contend that only choosing impeccable companies for your retirement portfolios is a very wise strategy. It’s much easier to ride out the storms, when the foundational structures underpinning your portfolios are the strongest available.

On a final note, it’s also important to invest in even the best of companies, only when their prices are sound and reflective of economic value. On the other hand, although most of the companies in this group were reasonably priced at the beginning of 2007, a few were actually technically moderately overvalued. Colgate-Palmolive, Coca-Cola, Pepsi and Walgreens were the most overvalued. Johnson & Johnson, McDonald’s, Microsoft and Nike were fully valued but not over. Disney, IBM and Wal-Mart were all fairly valued at the beginning of 2007. Nevertheless, each of these companies performed for their shareholders based on the strength of their businesses. Therefore, every company on this list represented equity investments that enabled their owners to sleep well at night, as long as they understood what they owned.

Disclosure: Long CL, JNJ, KO, MCD, MSFT, NKE, PEP at the time of writing.

By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm. Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2013 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Chuck Carnevale Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.