Economic Forecasts and Drivers 2014 - The Fed, Inflation-Deflation, Interest Rates, Housing and Speculation

Economics / US Economy Dec 28, 2013 - 02:21 PM GMTBy: John_Mauldin

It's that time of year again, when we begin to think of what the next one will bring. I will be doing my annual forecast issue next week, but my friend Gary Shilling has already done his and has graciously allowed me to use a shortened version of his letter as this week's Thoughts from the Frontline. So without any further ado, let's jump right to Gary's look at where we are and where we're going.

It's that time of year again, when we begin to think of what the next one will bring. I will be doing my annual forecast issue next week, but my friend Gary Shilling has already done his and has graciously allowed me to use a shortened version of his letter as this week's Thoughts from the Frontline. So without any further ado, let's jump right to Gary's look at where we are and where we're going.

Review and Forecast

By Gary Shilling

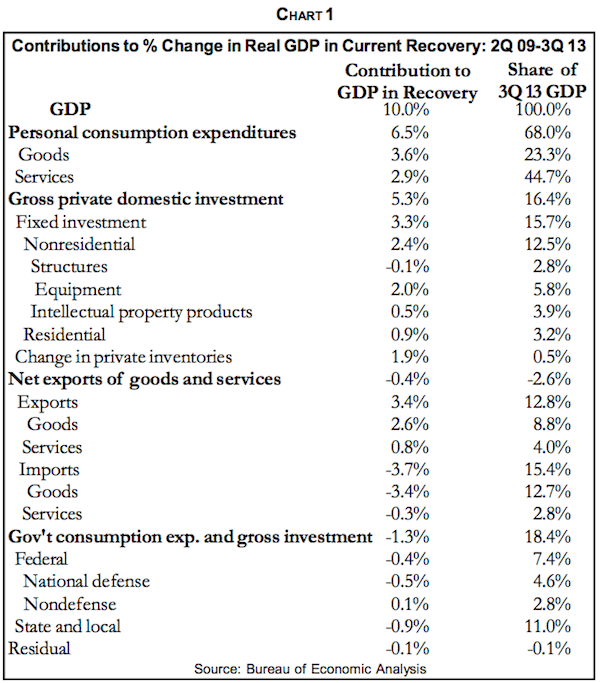

In the third quarter, real GDP grew 2.8% at annual rates from the second quarter. Without the increase in inventories, the rate would be 2.0%, in line with the 2.3% average growth since the economic recovery commenced in the second quarter of 2009.

Furthermore, the step-up in inventory-building from the second quarter may have been unintended, suggesting cutbacks in production and weaker growth in future quarters. Also, consumer spending growth, 1.5% in the third quarter, continues to slip from 1.8% in the second quarter and 2.3% in the first while business spending on equipment and software actually fell at a 3.7% annual rate for only the second time since the recovery started in mid-2009. Government spending was about flat with gains in state and local outlays offsetting further declines in federal expenditures. Non-residential outlays for structures showed strength as did residential building. The 16-day federal government shutdown didn't commence until the start of the fourth quarter, October 1, but anticipation may have affected the third quarter numbers.

The 2.3% average real GDP growth in the recovery, for a total rise of 10%, has not only been an extraordinarily slow one but also quite unusual in structure. Consumer spending has accounted for 65% of that growth, actually below its 68% of real GDP, as shown in the second column of Chart 1. Government spending—which in the GDP accounts is direct outlays for personal and goods and services and doesn't include transfers like Social Security benefits—has actually declined. Federal outlays fell 0.4% despite massive stimuli since most of it went to welfare and other transfers to state governments. But state and local spending dropped 0.9% due to budget constraints.

Residential construction accounted for 9% of the gain in the economy. This exceeds its share of GDP, but still is small since volatile housing normally leaps in recoveries, spurred by low interest rates. But deterrents abound. The initial boost to the economy as retrenching consumers cut imports was later reversed. So net exports reduced real GDP growth by 0.4% in the 13 quarters of recovery to date.

Inventory-building accounted for a substantial 19% of the rise in real GDP, suggesting the accumulation of undesired stocks since anticipation of future demand has been consistently subdued. Nonresidential structures fell 0.1% as previous overbuilding left excess space. Equipment spending contributed 20% of the overall growth, but has failed to shoulder the normal late recovery burst.

Nevertheless, the small intellectual property products component, earlier called software, accounted for 5% of overall growth compared to its 3.9% share of GDP. This reflects the productivity-enhancing investments American business have been using to propel profit margins and the bottom line in an era when sales volume has been weak and pricing power absent.

As we predicted over three years ago in our book The Age of Deleveraging: Investment strategies for a decade of slow growth and deflation, and in many Insights since then, economic growth of about 2% annually will probably persist until deleveraging, especially in the financial sector globally and among U.S. consumers, is completed in another four or five years. Deleveraging after a major leveraging binge and the financial crisis that inevitably follows normally takes around a decade, and since the workdown of excess debt commenced in 2008, the process is now about half over. The power of this private sector deleveraging is shown by the fact that even with the immense fiscal stimuli earlier and ongoing massive monetary expansion, real growth has only averaged 2.3% compared to 3.4% in the post-World War II era before the 2007-2009 Great Recession.

Optimists, of course, continue to look for reasons why rapid growth is just around the corner, and their latest ploy is the hope that the effects of individual income tax hikes and reduced federal spending this year via sequestration have about run their course. Early this year when these negative effects on spending were supposed to take place, scare-mongers in and out of Washington predicted drastic negative effects on the economy. But federal bureaucrats apparently mitigated much of the effects of sequestration, and the income tax increases on the rich, as usual, didn't change their spending habits much. So the positive influences on the economy as sequestration fades and income tax rates stabilize are likely to be equally minimal.

Furthermore, small-business sentiment has fallen recently. The percentage of companies that look for economic improvement dropped from -2 in August to -10 in September and -17 in October to a seven-month low. Those expecting higher sales declined from +8 to +2 in October. Most of the other components of the index fell, including those related to the investment climate, hiring plans, capital spending intentions, inventories, inflation expectations and plans to raise wages and prices. Other recent measures of subdued economic activity include the New York Fed's survey of manufacturing and business conditions and industrial production nationwide, which fell 0.1% in October from September.

The New York Fed's Empire State manufacturing survey index for November fell to 2.21%, the first negative reading since May. Every component dropped—orders, shipments, inventories, backlogs, employment, the workweek, vendor performance and inflation.

The ongoing sluggish growth in the U.S. is indeed a global problem. It's true in the eurozone, the U.K., Japan and China. Recently, the International Monetary Fund, in its sixth consecutive downward revision, cut its global growth forecast for this year by 0.3 percentage points to 2.9% and for 2014, by 0.2 percentage points to 3.6%.

It lowered its 2013 forecast for India from 5.6% to 3.8%, for Brazil from 3.2% to 2.5% and more than halved Mexico's to 1.2%. For developing countries on average, the IMF reduced its 2013 growth forecast by 0.4 percentage points to 5%, citing the drying up of years of cheap liquidity, competitive constraints, infrastructure shortfalls and slowing investment. It also worries about their balance of payment woes. For 2014, the IMF chopped its growth forecast for China from 7.8% to 7.3% and from 2.8% to 2.6% for the U.S.

Fed Chairman Bernanke continually worries about fiscal drag. Without question, the federal budget was stimulative in earlier years when tax cuts and massive spending in reaction to the Great Recession as well as weak corporate and individual tax collections pushed the annual deficit above $1 trillion. But the unwinding of the extra spending, income tax increases and sequestration this year and economic recovery—weak as it's been—have reduced the deficit to $680 billion in fiscal 2013 that ended September 30.

From here on, the outlook is highly uncertain with persistent gridlock in Washington between Democrats and Republicans. So far, they've kicked the federal budget and debt limit cans down the road and they may do so again when temporary extensions expire early next year. It looks like many in Congress have no intention of resolving these two problems and may be jockeying for position ahead of the 2014, if not the 2016, elections.

In our many years of observing and talking to Congressmen, Senators and key Administration officials of both parties, it's clear that Washington only acts when it has no alternative and faces excruciating pressure. A collapsing stock market always gets their attention, but the ongoing market rally, in effect, tells them that all is well or at least that it doesn't require immediate action.

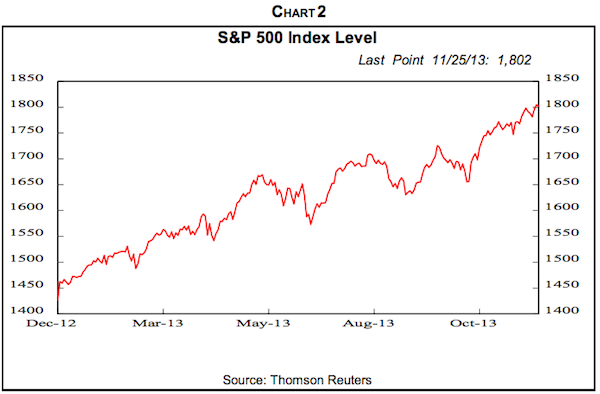

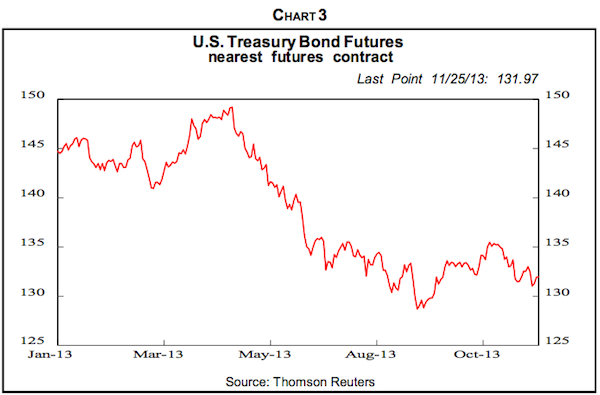

With muted economic growth and risks on the downside, distrust in the abilities or willingness of Congress and the Administration to right the ship, and falling consumer and business confidence, the burden of stimulating the economy remains with the Fed. Janet Yellen, the likely next Chairman, seems even more committed than Bernanke to continuing to keep monetary policy loose. The Fed plans to reduce its buying of $85 billion per month in securities but the negative reactions by stocks (Chart 2), Treasury bonds (Chart 3) and many other securities to Bernanke's hints in May and June that purchases would be tapered and eliminated by mid-2014 made a strong impression on the Fed. Similarly, the release of the minutes of the Fed's October policy meeting— which again said officials looked forward to ending the bond-buying program "in coming months" if conditions warranted—resulted in an instant drop in stock and bond prices.

The Fed is trying to figure out how to end security purchases without spiking interest rates, to the detriment of housing, other U.S. economic sectors and developing economies. It's moving toward "forward guidance," more commitment to keep the short-term interest rate it controls low than its present pledge to keep it essentially at zero until the current 7.3% unemployment rate drops to 6.5% and its inflation rate measure climbs to 2.5% from the current 1.2% year-over-year.

The hope is that a longer-term commitment to keep short-term rates low will retard long rates as well when the Fed tapers its asset purchases. This strategy appears to be having some success. Treasury investors are switching from 10-year and longer issues to 2-year or shorter notes. This is known as the yield-steepening trade as it pushes short-term yields down and longer yields up. As a result, the spread between 2-year and 10-year Treasury obligations has widened to 2.54 percentage points, the most since July 2011. Banks benefit from a steeper yield curve since they borrow short term and lend in long-term markets. But borrowers pay more for loans linked to long-term Treasury yields. There's a close link between the yield on 10-year Treasury notes and the 30-year fixed rate on residential mortgages.

The Fed has already signaled that it may not wait to raise short rates until the unemployment rate, a very unreliable gauge of job conditions as we've explained in past Insights, drops below 6.5%. Bernanke recently said that "even after unemployment drops below 6.5%, the [Fed] can be patient in seeking assurance that the labor market is sufficiently strong before considering any increase in its target for the federal funds rate." At that point, the Fed will consider broader measures of the job market including the labor participation rate. If the participation rate hadn't fallen from its February 2000 peak due to postwar baby retirements, discouraged job-seekers and youths who stayed in school since job opportunities dried up with the recession, the unemployment rate now would be 13%.

The Fed is well aware that other than pushing up stock prices, its asset-buying program is having little impact on the economy. In a recent speech, Bernanke said that while the Fed's commitment to hold down interest rates and its asset purchases both are helping the economy, "we are somewhat less certain about the magnitude of the effects on financial conditions and the economy of changes in the pace of purchases or in the accumulated stock of assets on the Fed's balance sheet." We wholeheartedly agree with this sentiment, as discussed in detail in our October Insight. Tapering Fed monthly purchases only reduces the ongoing additions to already-massive excess member bank reserves on deposit at the Fed.

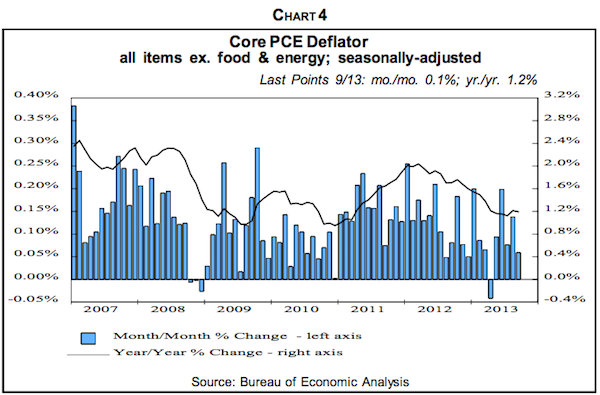

Inflation has virtually disappeared. The Fed's favorite measure of overall consumer prices, the Personal Consumption Expenditures Deflator excluding food and energy (Chart 4), is rising 1.2% year-over-year, well below the central bank's 2.0% target and dangerously close to going negative.

There are many ongoing deflationary forces in the world, including falling commodity prices, aging and declining populations globally, economic output well below potential, globalization of production, growing worldwide protectionism including competitive devaluation in Japan, declining real incomes, income polarization, declining union memberships, high unemployment and downward pressure on federal and state and local government spending.

With the running out of 2009 federal stimulus money and gas tax revenues declining as fewer miles are driven in more efficient cars, highway construction is declining and construction firms are consolidating and reducing bids on new work even if their costs are rising. Highway construction spending dropped 3.3% in the first eight months of 2013 compared to a year earlier. Also, states are shifting scarce money away from transportation and to education and health care. We've noted in past Insights that aggressive monetary and fiscal stimuli probably have delayed but not prevented chronic deflation in producer and consumer prices.

Why does the Fed clearly fear deflation? Steadily declining prices can induce buyers to wait for still-lower prices. So, excess capacity and inventories result and force prices lower. That confirms suspicions and encourages buyers to wait even further. Those deflationary expectations are partly responsible for the slow economic growth in Japan for two decades.

With the Fed likely to continue to hold its federal funds rate close to zero, other short-term interest rates will probably remain there too. So the recent rally in Treasury bonds may well continue, with yields on the 10-year Treasury note, now 2.8%, dropping below 2% while the yield on our 32-year favorite, the 30-year Treasury "long bond," falls from 3.9% to under 3%. Even-lower yields are in store if chronic deflation sets in as well it might. Ditto for the rise in stocks, which we continue to believe is driven predominantly by investor faith in the Fed, irrespective of modest economic growth at best. "Don't fight the Fed," is the stock bulls' bellow. Supporting this enthusiasm has been the rise in corporate profits, but that strength has been almost solely due to leaping profit margins. Low economic growth has severely limited sales volume growth, and the absence of inflation has virtually eliminated pricing power. So businesses have cu t labor and other costs with a vengeance as the route to bottom line growth

Wall Street analysts expect this margin leap to persist. In the third quarter, S&P 500 profit margins at 9.6% were a record high but revenues rose only 2.7% from a year earlier. In the third quarter of 2014, they see S&P 500 net income jumping 14.9% from a year earlier on sales growth of only 4.7%. But profit margins have been flat at their peak level for seven quarters. And the risks appear on the downside.

Productivity growth engendered by labor cost-cutting and other means is no longer easy to come by, as it was in 2009 and 2010. Corporate spending on plant and equipment and other productivity-enhancing investments has fallen 16% from a year ago. Also, neither capital nor labor gets the upper hand indefinitely in a democracy, and compensation's share of national income has been compressed as profit's share leaped. In addition, corporate earnings are vulnerable to the further strengthening of the dollar, which reduces the value of exports and foreign earnings by U.S. multinationals as foreign currency receipts are translated to greenbacks.

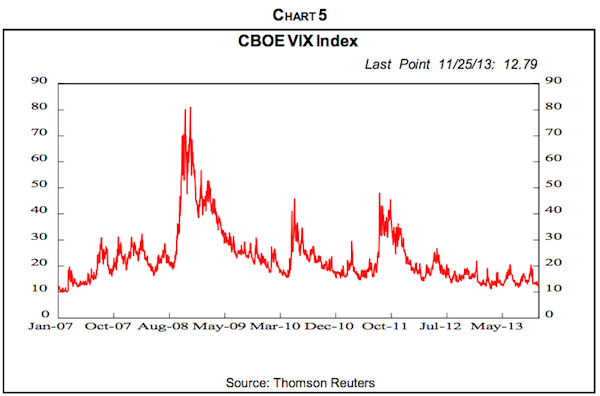

Driven by the zeal for yield due to low interest rates and the rise in stock prices that has elevated the S&P 500 more than 160% from its March 2009 low, a degree of speculation has returned to equities. The VIX index, a measure of expected volatility, remains at very low levels (Chart 5). Individual investors are again putting money into U.S. equity mutual funds after years of withdrawals. "Frontier" equity markets are in vogue. They're found in countries like Saudi Arabia, Nigeria and Romania that have much less-developed—and therefore risky—financial markets and economies than Brazil and Mexico.

The IPO market has been hot this year. The median IPO has been priced at five times sales over the last 12 months, almost back to the six times level of 2007. And many IPOs have used the newly-raised funds to repay debt to their private equity backers, not to invest in business expansion. Through early November, IPOs raised $51 billion, the most since the $62 billion in the comparable period in 2000. Some 62% of IPOs this year are for money-losing companies, the most since the 1999-2000 dot com bubble. Some hedge fund managers are introducing "long only" funds with no hedges against potential stock price declines.

The S&P 500 index recently reached an all-time high but corrected for inflation, it remains in a secular bear market that started in 2000. This reflects the slow economic growth since then and the falling price-earnings ratio, and fits in with the long-term pattern of secular bull and bear markets, as discussed in detail in our May 2013 Insight.

High P/E

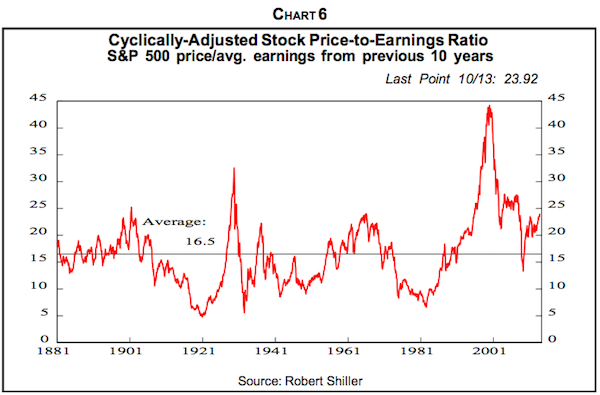

Furthermore, from a long-term perspective, the P/E on the S&P 500 at 24.5 is 48% above its long run average of 16.5 (Chart 6), and we're strong believers in reversions to well-established trends, this one going back to 1881. The P/E developed by our friend and Nobel Prize winner, Robert Shiller of Yale, averages earnings over the last 10 years to iron out cyclical fluctuations. Also, since the P/E in the last two decades has been consistently above trend, it probably will be below 16.5 for a number of years to come.

This index is trading at 19 times its companies' earnings over the past 12 months, well above the 16 historic average. This year, about three-fourths of the rise in stock prices is due to the jump in P/Es, not corporate earnings growth. Even always-optimistic Wall Street analysts don't expect this P/E expansion to persist in light of possible Fed tightening. Those folks, of course, are paid to be bullish and their track record proves it. Since 2000, stocks have returned 3.3% annually on average, but strategists forecast 10%. They predicted stock rises in every year and missed all four down years.

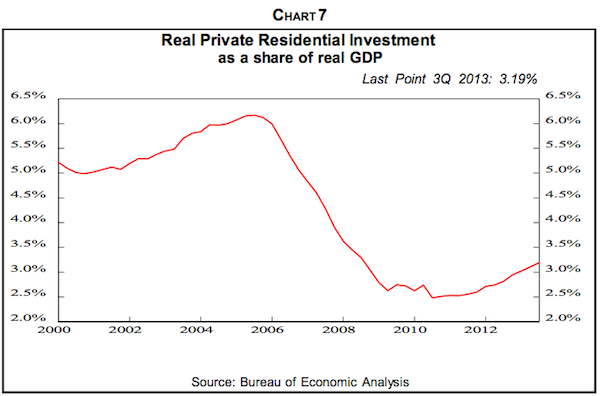

Residential construction is near and dear to the Fed's heart. It's a small sector but so volatile that it has huge cyclical impact on the economy. At its height in the third quarter of 2005, it accounted for 6.2% of GDP but fell to 2.5% in the third quarter of 2010 (Chart 7). That in itself constitutes a recession, even without the related decline in appliances, home furnishings and autos.

Furthermore, the Fed can have a direct influence on housing. Monetary policy is a very blunt instrument. The central bank only can lower interest rates and buy securities and then hope the economy in general will be helped. In contrast, fiscal policy can aid the unemployed directly by raising unemployment benefits. But by buying securities, especially mortgage-related issues, the Fed can influence interest rates and help interest-sensitive housing. The rise in 30-year fixed mortgage rates of over one percentage point last spring probably has brought the housing recovery to at least a temporary halt. Each percentage point rate rise pushes up monthly principal and interest payments by about 10%.

Of course, many other factors besides mortgage rates affect housing and have been restraining influences. They include high downpayment requirements, stringent credit score levels, employment status and job security and the reality that for the first time since the 1930s, house prices have fallen—by a third at their low.

Many hope that record levels of corporate cash and low borrowing costs will propel capital spending. And spending aimed at productivity enhancement, much of it on high-tech gear, has been robust as business concentrates on cost-cutting, as noted earlier. But the bulk of plant and equipment spending is driven by capacity utilization, and while it remains low, there's little zeal for new outlays.

That's why capital spending lags the economic cycle. Only after the economy strengthens in recoveries do utilization rates rise enough to spur surges in capital spending. And as our earlier research revealed, it's the level of utilization, not the speed with which it's rising, that drives plant and equipment outlays. So this is a Catch-22 situation. Until the economy accelerates and pushes up utilization rates, capital spending will remain subdued. But what will cause that economic growth spurt?

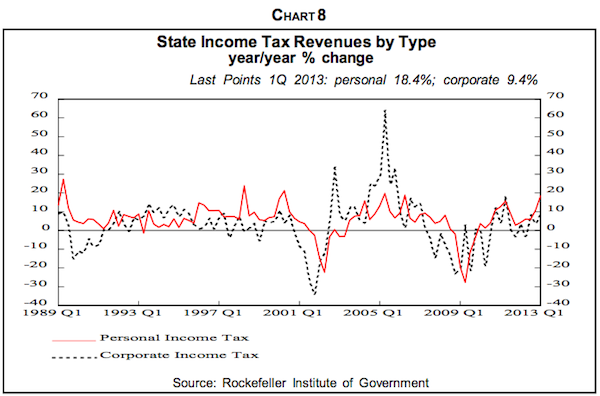

It's unlikely to be government spending. State and local outlays used to be a steady 12% or so of GDP and a source of stable, well-paying jobs. But no more. State tax revenues are recovering (Chart 8), but the federal stimulus money enacted in 2009 has dried up, leaving many states with strained budgets.

Pressure also comes from private sector workers who are increasingly aware that while their pay has been compressed by globalization and business cost-cutting, state and local employees have gotten their usual 3% to 4% annual increases and lush benefits. As a result, those government people have 45% higher pay than in the private sector, 33% more in wages and 73% in additional benefits. Oversized retiree obligations have sunk cities in California and Rhode Island and pushed Illinois to the brink of bankruptcy. Hopelessly-underfunded defined benefit pensions are a major threat to state and local government finances.

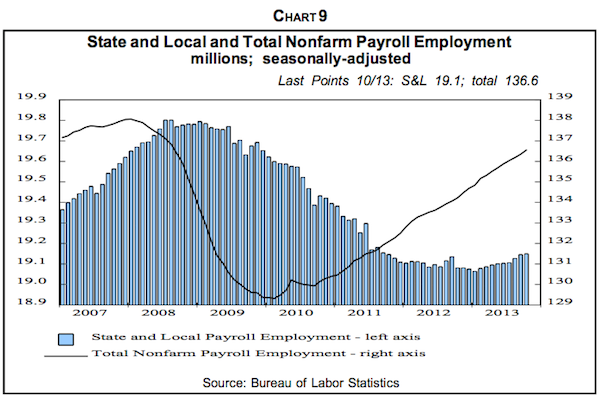

Municipal government employment is down 3.3% from its earlier peak compared to -0.2% for total payroll employment (Chart 9). And since these people are paid 1.45 times those in the private sector, two job losses is the equivalent of three private sector job cuts in terms of income. Real state and local outlays have fallen 9.5% since the third quarter of 2009.

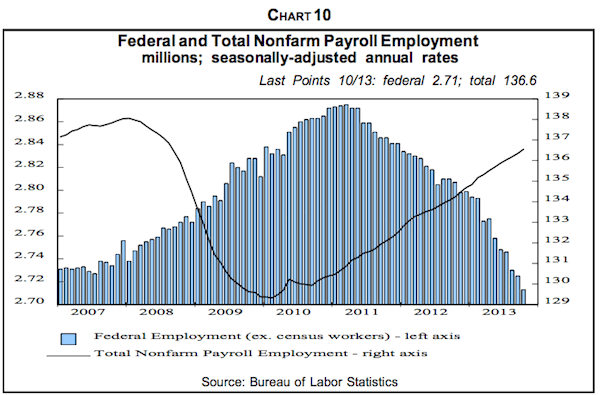

Federal direct spending on goods and services, excluding Social Security, Medicare and other transfers, has also been dropping, by 7.2% since the third quarter of 2010. Both defense and nondefense real outlays are dropping, and this has occurred largely before the 2013 sequestration. At the same time, federal government civilian employment, civilian and military, has dropped 6% from its top (Chart 10).

The U.S. labor market remains weak and of considerable concern to the Fed. Recent employment statistics have been muddled by the government's 16-day shutdown in October and the impasse over the debt ceiling. Initially, 850,000 employees were furloughed although the Pentagon recalled most of its 350,000 civilian workers a week into the shutdown.

The unemployment rate has been falling, but because of the declining labor participation rate. We explored this phenomenon in detail in "How Tight Are Labor Markets?" (June 2013 Insight). As people age, their labor force participation rates tend to drop as they retire or otherwise leave the workforce. With the aging postwar babies, those born between 1946 and 1964, this has resulted in a downward trend in the overall participation rate—but it doesn't account for all of the decline.

The irony is that participation rates of younger people tend to be higher than for seniors, but are declining. For 16-24-year-olds, the rate has declined sharply since 2000 as slow economic growth, limited jobs and rising unemployment rates have encouraged these youths to stay in school or otherwise avoid the labor force.

Meanwhile, the participation rates for those over 65 have climbed since the late 1990s as they are forced to work longer than they planned. Many have been notoriously poor savers and were devastated by the collapse in stocks in 2007-2009 after the 2000-2002 nosedive, two of only five drops of more than 40% in the S&P 500 since 1900.

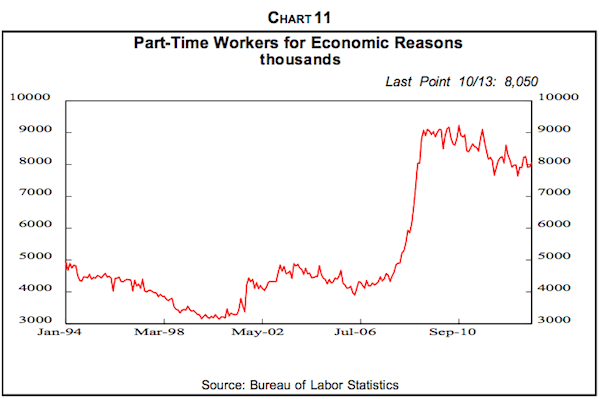

An additional sign of job weakness is the large number of people who want to work full-time but are only offered part-time positions—"working part-time for economic reasons" is the Bureau of Labor Statistics term (Chart 11)—and these people total 8 million and constitute 5.6% of the employed. This obviously reflects employer caution and the zeal to contain costs since part-timers often don't have the pension and other benefits enjoyed by full-time employees.

This group will no doubt leap when Obamacare is fully implemented in 2015, according to its current schedule. Employers with 50 or more workers have to offer healthcare insurance, but not to those working less than 30 hours per week. When these people and those who have given up looking for jobs are added to the headline unemployment rate, the result, the BLS's U-6 unemployment rate, leaped in the Great Recession and is still very high at 13.8% in October.

The weakness in the job market is amplified by the fact that most new jobs are in leisure and hospitality, retailing, fast food and other low-paying industries, which accounted for a third of the 204,000 new jobs in October. Manufacturing, which pays much more, has added some employees as activity rebounds but growth has been modest.

With all the downward pressure on labor markets, real weekly wages are falling on balance. The folks on top of the income pile have recovered all their Great Recession setbacks and then some, on average. The rest, perhaps three-fourths of the population, believe they are—and probably still are—mired in recession due to declining real wages, still-depressed house prices, etc. Consequently, the share of total income by the top one-fifth, which has been rising since the data started in 1967, has jumped in recent years. The remaining four quintile shares continue to fall, although falling shares do not necessarily mean falling incomes.

The average household in the top 20% by income has seen that income rise 6% since 2008 in real terms and the top 5% of earners had an 8% jump. The middle quintile gained just 2% while the bottom 29% are still below their pre-recession peak. A study of household incomes over the 2002-2012 decade shows that the top 0.01% gained 76.2% in real terms but the bottom 90% lost 10.7%. In 2012, the top 1% by income got 19.3% of the total. The only year when their share was bigger was 1928 at 19.6%.

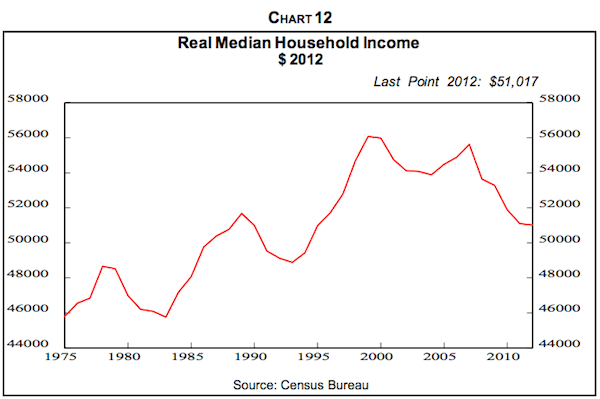

Real median household income, that of the household in the middle of the spectrum, continues to drop on balance, only leveling last year from 2011 (Chart 12). In 2012, it was down 8.3% from the prerecession 2007 level and off 9.1% from the 1999 all-time top. Americans may accept a declining share of income as long as their spending power is increasing, but that's no longer true, a reality that President Obama plays to with his "fat cat bankers" and other remarks.

Households earning $50,000 or more have become increasingly more confident, according to a monthly survey by RBC Capital Markets, but confidence among lower-income households stagnated, created a near-record gap between the two. Of the 2.3 million jobs added in the past year, 35% were in jobs paying, on average, below $20 per hour in industries such as retailing and leisure and hospitality. Since the recession ended, hourly wages for non-managers in the lowest-paying quarter of industries are up 6% but more than 12% in the top-paying quarter. These income disparities are reflected in consumer spending. In the first nine months of this year, sales of luxury cars were up 12% from a year earlier but small-car sales rose just 6.1%.

With housing, capital spending, government outlays and net exports unlikely to promote rapid economic growth in coming quarters, the only possible sparkplug is the consumer. Consumer outlays account for 69% of GDP, and with falling real wages and incomes, the only way for real consumer spending to rise is for their already-low saving rate to fall further.

Even the real wealth effect, the spur to spending due to rises in net worth, is now muted. In the past, it's estimated that each $1 rise in equity value boosted consumer spending by three cents over the following 18 months while a dollar more in house value led to eight cents more in outlays. But now the numbers are two cents and five cents, respectively.

True, the ratio of monthly financing payments to their after-tax income has been falling for homeowners, freeing money for spending. Those obligations include monthly mortgage, credit card and auto loan and lease payments as well as property taxes and homeowner insurance. Nevertheless, for the third of households that rent, their average financial obligations ratio has been rising in the last two years as rents rise while vacancies drop.

Declining gasoline prices have given consumers extra money for other purchases, and are probably behind the recent rise in gas-guzzling pickup truck and SUV sales. Furthermore, the automatic Social Security benefit cost-of-living escalator will increase benefits by 1.5% in 2014 for 63 million recipients of retirement and disability payments. Still, with low inflation in 2013, the basing year, that increase is smaller than the 1.7% rise last year and the lowest since 2003, excluding 2010 and 2011 when there were no increases due to a lack of inflation. Social Security retirement checks will rise $19 per month to $1,294, on average, starting in January.

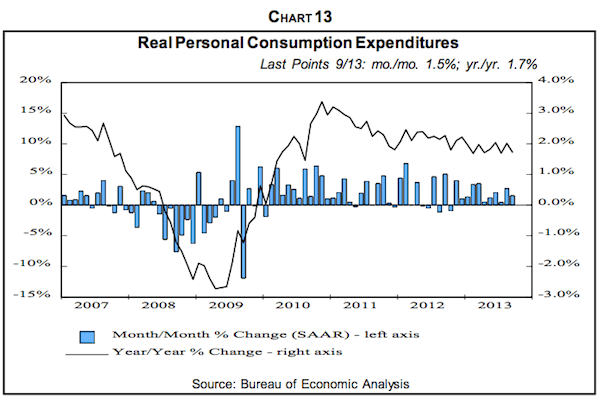

In any event, retail sales growth is running about 4% at annual rates recently, about half the earlier recovery strength (Chart 13). And a lot of this growth has been spurred by robust auto sales, allegedly driven by the need to replace aged vehicles.

Insight readers know we've been waiting for a shock to remind equity investors of the fundamental weakness of the economy, and perhaps push the sluggish economy into a recession. With underlying real growth of only 2%, it won't take much of a setback to do the job.

Will the negative effects of the government shutdown and debt ceiling standoff, coupled with the confusion caused by the rollout of Obamacare, be a sufficient shock? The initial Christmas retail selling season may tell the tale, and the risks are on the down side. Besides the consumer, we're focused on corporate profits, which may not hold up in the face of persistently slow sales growth, no pricing power and increasing difficulty in raising profit margins.

Nevertheless, we are not forecasting a recession for now, but rather more of the same, dull, slack 2% real GDP growth as in the four-plus years of recovery to date.

If you like what you read and would like to keep up with Gary for the next year, you can subscribe to Gary Shilling's Insight for one year for $335 via email. Along with 12 months of Insight you'll also receive a free copy of his full report detailing why he believes it will be "advantage America" in the coming years and a free copy of Gary's latest book, Letting Off More Steam. To subscribe, call 1-888-346-7444 or 973-467-0070 between 10 am and 4 pm Eastern time or email insight@agaryshilling.com. Be sure to mention Thoughts from the Frontline to get the special report and free book in addition to your 12 months of Insight (available only to new subscribers).

Dubai, Saudi Arabia, Canada, and Auld Lang Syne

(For a little mood music, you can listen to James Taylor croon "Auld Lang Syne." Or here's the Beach Boys’ version.)

I am home for the holidays until January 8, when I leave for Dubai and then Riyadh for a week. There is the potential for a day trip to Abu Dhabi to meet with Maine fishing buddy Paul O'Brien. Then I am back home for a week before I fly to Vancouver, Edmonton, and Regina for a three-day speaking tour at those cities' respective annual CFA forecast dinners. A note from a reader in Edmonton pointed out that it is already -30 there. I am actively hunting for my thermal underwear.

Oddly enough, my calendar then shows me home for four weeks before I head to Laguna Beach, CA, for a speech and then hop a plane to Miami. You would think that someone who flies as much as I do would have done a cross-country flight more than a few times, but this will be my first time ever to fly coast to coast in the US.

As noted last week, all my kids will be in town tonight, and we will celebrate our "official" family Christmas tomorrow. The poor grandchildren have had to wait three extra days to open their presents, but I keep telling them that waiting builds character. I get looks back from them that say they're not sure what character is but they want nothing to do with it.

I have always enjoyed this time of year as an interlude for contemplating the future. For whatever reason, since I was in college I have paused as the new year approached to think about where I wanted to be in five years. Given that I'm 64, that means I've gone through this process some 42 times and seen the completion of 37 five-year planning cycles.

My batting average to date is 0 for 37. I never end up where I thought I was going to be, although there are times when I at least get the direction right, and fortunately there even a few times when the new midcourse correction means things turn out even better than planned.

Next week I write my 2014 forecast, for which the theme will be "Uncertainty." Yet even in the face of overwhelming uncertainty, I will still come up with a personal five-year plan. Given the rather unique set of opportunities that have been presented to me in the past year, the plan is rather ambitious. And I expect it to change a lot. Among other projects, I expect to be announcing several new letters in the coming months that will be specifically directed to strategic portfolio planning. Right now our plan is to make these letters more or less freely available.

But the one thing that will hopefully not change is that I will be writing this letter to you, as together we try to make sense of the world. As the year draws to a close, I want to thank you for being part of my family of readers. And may the coming year surpass all your most wildly optimistic plans.

Your hearing "Auld Lang Syne" analyst,

John Mauldin

subscribers@MauldinEconomics.com

Like Outside the Box?

Sign up today and get each new issue delivered free to your inbox.

It's your opportunity to get the news John Mauldin thinks matters most to your finances.

© 2013 Mauldin Economics. All Rights Reserved.

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.MauldinEconomics.com.

Please write to subscribers@mauldineconomics.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.MauldinEconomics.com.

To subscribe to John Mauldin's e-letter, please click here: http://www.mauldineconomics.com/subscribe

To change your email address, please click here: http://www.mauldineconomics.com/change-address

Outside the Box and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin's other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRA, SIPC, through which securities may be offered . MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at http://www.MauldinCircle.com (formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.