Reasons Why The U.S. Government Is Destroying The Dollar

Currencies / US Dollar Jan 08, 2014 - 05:21 AM GMTBy: Dan_Amerman

Overview

Overview

The United States government has six interrelated motivations for destroying the value of the dollar:

-

Creating money out of thin air on a massive basis is all that stands between the current state of hidden depression, and overt depression with unemployment levels potentially rivaling those seen in the Great Depression of the 1930s.

-

It is the most effective way to not just pay down current crushing debt levels using devalued dollars, but also to deal with the rapidly approaching massive generational crisis of paying for Boomer retirement promises.

It creates a lucratively profitable $500 billion a year hidden tax for the benefit of the US government - a tax which is not understood by voters or debated in elections.

It creates a second and quite different form of hidden taxation by way of generating artificial market highs, which while non-existent in inflation-adjusted terms, do create artificial investment profits that are fully taxable and highly profitable for the US government.

It is the weapon of choice being used to wage currency war and reboot US economic growth; and

It is an essential component of political survival and enhanced power for incumbent politicians.

In this article we take a holistic approach to understanding how individual short, medium and long-term pressures all come together to leave the government with effectively no choice but to create a significant rate of inflation that will steadily destroy the value of the dollar over time.

If you have savings, if you rely on a pension, if you are a retiree or Boomer with retirement accounts - any one of these six fundamental motivations is by itself a grave peril to your future standard of living. However, it is only when we put all six together and see how the motivations reinforce each other, that we can most effectively seek personal solutions.

Reason One: The Political Interests Of Self-Serving Politicians

Even after the major tax increases of about $400 billion a year that took effect at the end of 2012, almost 5% of the US economy is still currently funded by deficit spending. From a political perspective, this approximately $750 billion a year in borrowed money is "free money" that politicians often get to disburse on a political district and favored special interest group basis. In other words, roughly $650 per month per above-poverty line American household can be used to reward friends - and can be withheld from enemies - with personal credit being taken by the benevolent politicians for this never-ending largess.

In past decades, politicians were restricted to spending perhaps $200 or $300 per month per household over and above what the government was collecting in taxes, with the difference being borrowed in the bond market. Anything above that would require the unpleasantness of raising taxes, which might put individual politicians in danger of actually losing their position and privileged lifestyle if he or she weren't in a "safe" district. However, in the current climate all limitations are gone, the pork is rolling out on a historically unprecedented basis, and the politicians are wielding unprecedented power.

So why do the limitations usually exist on at least some level, and why are they gone now? Historically, the US government had directly created money out of thin air on a massive basis to fund deficit spending during the Civil War, and also during the Revolutionary War. There is a very good reason such governmental actions are so rare: the value of the US dollar was rapidly destroyed in both instances. So, this spending without limit would not ordinarily be a sensible path. Unless, from the government's perspective, there were other dangers that were considered a greater threat, and that could be addressed only through destroying the value of the dollar.

Reason Two: To Hide A Depression

(I have written numerous articles about various aspects of Reasons Two through Six for some years now, and my long-term readers and subscribers have been well aware of the building pressures. While the emphasis of this article is on the interweaving of the short, medium and long-term relationships between the six reasons, we will first set the stage by taking a few paragraphs each to briefly review the individual government motivation, with a link to a full length article that covers the problem in more depth.)

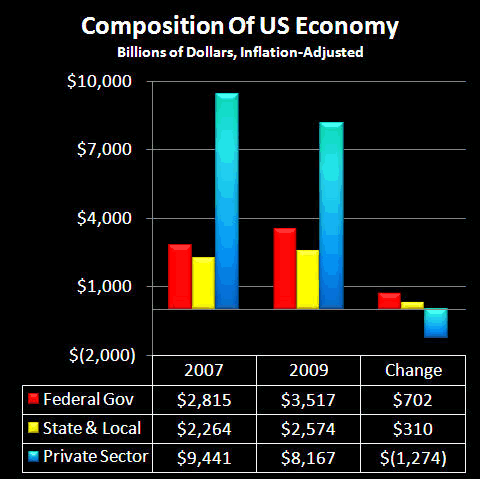

While you wouldn't know it from government press releases or media headlines, there has been a gaping hole in the US economy since 2008, as illustrated below:

During the first round of the Financial Crisis in 2008 and 2009, the US private sector nearly collapsed, threatening to send the US economy straight into deep depression. We're talking about a $1.3 trillion private sector collapse that was contained only by the government fantastically increasing the money it spent, even while tax revenues were falling. Indeed, the creation of huge government deficits has been all that has maintained even a facade of semi-normalcy. Remove that mechanism, and it is straight to official Great Depression-level unemployment in months.

Even as the true gravity of the situation is hidden from the general public, so too is the true cost of the grossly irresponsible short-term "band-aid" that is being used to cover the hole in the US economy. The destruction of the value of savings in general, as well as the impoverishment of Boomers and retirees in particular, is explained in my article linked below, "Hiding A Depression: How The US Government Does It."

Reason Three: A Desperate Attempt To Escape Depression By Waging Currency War

The US government has been waging currency war since September of 2010. Simply put, the US would have great difficulty emerging from depression so long as the US dollar were "strong", because a strong dollar translates to "expensive" US workers who have difficulty competing for market share even in the US economy, let alone abroad. So one reason for a nation intentionally slashing the value of its currency is that its workers become relatively cheaper, enabling them to not only better defend their domestic market share, but to begin to take market share in foreign economies as well. However, when a major player goes on the currency offensive, many trading partners will counterattack in the attempt to defend their own economies, not by making their own currencies stronger, but by weakening them- so that their domestic workers remain relatively inexpensive and will be better able to compete for market share.

To successfully maintain and increase the power of this currency offensive while negating attempted counterattacks, the Federal Reserve chose a radical weapon in the form of QE3 - which began with the public announcement that it would be directly creating money on a massive scale equal to 6% of the US economy indefinitely, with the proceeds going to purchase US government debt and mortgage-backed securities in the secondary markets. Ultimately, the only protections for a symbolic currency such as the US dollar are the policies deployed by the Central Bank to maintain that value. And when the nation's chief central banker directly threatens to use his power to destroy the symbol, rather than preserve it - the threat is extraordinarily effective.

QE3 has been highly successful in reducing the value of US currency relative to both Europe and China. However, Japan has counterattacked with the new Abenomics, a particularly potent form of quantitative easing which has been quite successfully pushing down the value of the yen versus the rest of the world, thereby ratcheting up Japanese export profits.

There is no free lunch, however. While the US government is insisting to the world-at-large that it is not engaged in currency warfare, in order to maintain the plausible deniability that is essential to diplomatic doublespeak, it is also hiding the heavy cost from its own citizens. The US standard of living since the late 1990s has been based on having a "strong" dollar and huge trade deficits - meaning we haven't actually been able to pay for what we consume for a long time. Therefore, even as jobs and the real economy grow, there is a drop in the overall standard of living, which is not evenly weighted, but is disproportionately borne by savers, Boomers and retirees.

A deeper exploration of how this works, including the specific ways that older citizens are - and will continue to be - the primary victims, can be found in my article linked below, "Bullets In The Back: How Boomers & Retirees Will Become Stimulus, Bailout & Currency War Casualties".

Article Link

These second and third components of hiding a depression and waging currency war are tightly interwoven, and could even be called "killing two birds with one stone". The money doesn't exist to keep the US from openly plunging into depression, it simply isn't there for a fiscally responsible government. And covering the economic hole by creating money out of thin air at a rate equal to 6% of the total US economy is so fiscally irresponsible, that few nations dare a counterattack of such magnitude. So for now, massive monetary creation allows the US to not only cover over the current hidden depression, but also to wage all-out currency war to try to emerge from that depression.

While boosting employment is an important motive behind currency warfare, to better understand the agenda of the US government, we'll next explore the greatest financial problem of all, and how destroying the value of the dollar is the intended solution.

Reason Four: Dodging National Bankruptcy

Sometimes households reach the unfortunate point where when they add up the credit cards, mortgage payments, and second mortgage payments - they realize that they will never be able to pay their bills. They know they are bankrupt and there is no way of dodging it. But instead of reducing their spending - they may actually ratchet it up, until all the lines of credit are maxed out, and the bills are all in arrears. Because once bankruptcy is inevitable anyway, why slash your standard of living before you absolutely have to? Partying it up for another few months won't change the destination, so why not?

Fortunately, relatively few ordinary people are so irresponsible as to think that way. There is ample evidence, however, that a good number of politicians hold that mindset when it comes to budget deficits that appear impossible to repay, at least in the conventional manner.

There is a pervasive myth that is being frequently repeated, which is that our children and grandchildren will be slaving away for decades to pay back the money that we've been borrowing to fund this reckless deficit spending. The assumption behind the myth is that were it not for the current spending, the nation would be fine, and therefore increased taxes will be needed to pay back these borrowings over the decades to come.

Except that the nation wouldn't be fine. For like most other major developed nations in the world, the United States has been effectively bankrupt for quite some time, with a day of reckoning that is approaching fast - with or without the current outrageous level of deficit spending.

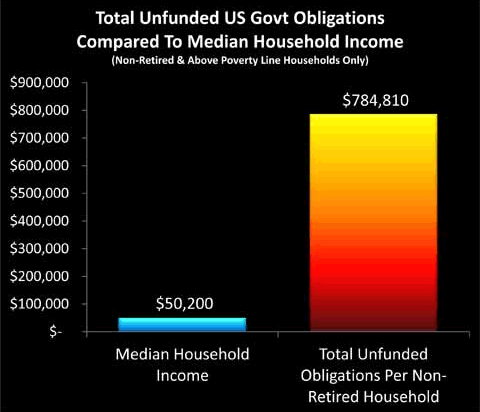

The graph below is from my article, "Six Layers Of Deficit Impossibilities Mean Retirement Catastrophe".

As developed step by step in "Six Layers", when we add up current and future federal deficits, as well as unfunded Social Security, Medicare and other unfunded government promises, the total comes to over $785,000 per non-retired household over the coming years that has an above-poverty line income. And this actually isn't even the total cost - it is the excess cost over and above current estimated tax receipts, with those estimated receipts being based on the assumption of a healthy and growing economy. When we drop the assumption of an economy growing at the same rates of the last 50 years, then the shortfall goes far higher - perhaps to over $200 trillion for Social Security and Medicare alone by some recent estimates. That would raise the total shortfall to over $2 million per non-retired and above-poverty-line household.

If taxes can't pay (and it's ludicrous to think they can), and the US doesn't declare bankruptcy, then just how do we cover the gap?

Short answer: pay in full, but make the dollar worth five cents. This drops the per household cost for everything from almost $800,000 down to about $40,000. Painful, but manageable over a period of 20-30 years.

Merely make a dollar worth five cents, and those seemingly impossible government promises become quite payable. The problem with this "solution", however, is that it also requires making most people's life savings worth five cents on the dollar.

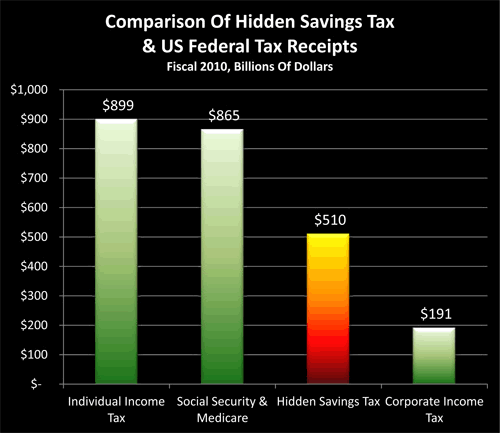

Reason Five: Create A Massive Hidden Tax

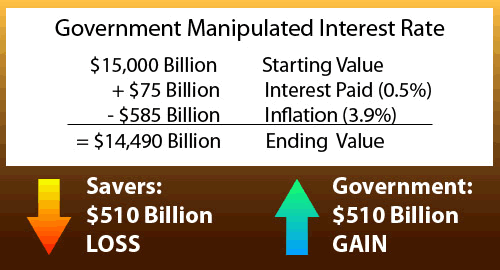

The Federal Reserve effectively controls short, medium and long-term interest rates in the United States, and this means that it controls the borrowing costs of the United States government. As developed in my article linked below, "Hiding A $500 Billion Tax On Savings: How The Government Deceives Millions", by forcing interest rates below the rate of inflation, the Federal Reserve creates about a half trillion dollar per year "windfall" gain for the federal government.

This is not "free money", far from it - for every dollar that the government takes in from interest rate manipulations comes directly out of the pockets of savers. That is, for the government to come out ahead by $500 billion per year requires savers and pension funds to come up short by $500 billion per year. This makes it a tax - in all but name. It is also essential to note that two elements have to come together to make this hidden tax work: 1) there have to be low interest rates, and 2) there also has to a substantive real rate of inflation (which can be quite different from the official rate).

From a politician's perspective, this massive tax - almost three times the size of federal corporate taxation - is a "dream tax". Half a trillion dollars a year is available to spend without overtly raising taxes or increasing deficits! Sure, there is a cost, which is the entirely deliberate destruction of retirement dreams and promises for tens of millions of US workers and retirees - particularly Boomers - as well as pushing forward the insolvency of state and local government pension funds around the country. But the deliberate bankrupting of a generation is a long-term problem with no clear accountability and almost no voter understanding, which means it is more or less irrelevant for how political decisions are made today.

Reason Six: Taxing Inflation As Income

Let's consider three market scenarios when viewed from a governmental tax collection perspective.

1) Falling Markets. If investment markets such as the stock market are falling - then on average, rather than generating taxes for the government, they result in tax deductions, as investors write off their losses. Falling asset values are disastrous for government budgets, because falling investment markets act to reduce government tax collections.

2) Level Markets. If markets are on average neither rising nor falling but going sideways - then while tax deductions are not being generated on a net basis, neither are total tax collections. While this is a better scenario for the government than falling markets, it is still quite problematic for tax collection in general, because one of the primary sources of tax revenues - particularly from the more affluent portion of the population - ceases to exist.

3) Rising Markets. There is nothing like a good bull market to rapidly increase government tax collections. Investors all across the country are ratcheting up their tax payments, and rising markets also tend to generate frequent short-term trading, which means that many of those tax collections will be at the lucrative (for the government) short-term bracket level. It is no coincidence that the only US government surpluses in recent decades occurred at the height of the tech stock bubble, with the often frenetic short-term trading (at short-term tax rates) that was a part of it.

If governments didn't have a means for turning level or falling markets into rising markets - this three-part relationship could be a huge problem, particularly with a struggling economy.

Fortunately for the government - and very unfortunately for investors - there is a very powerful weapon which can turn falling or level markets into rising markets, while radically increasing investment tax revenues. This weapon is inflation, the destruction of the value of the dollar, and it has generated enormous hidden tax revenues for the US government ever since the United States went off the gold standard in 1933.

While these hidden inflation taxes are very well understood by governments and economists, the average voter and investor is not even aware of their existence. To help address this knowledge gap, I have prepared two resources, linked below.

" Could Misleading Theory And Jargon Threaten Your Net Worth?" is an easy to follow, illustrated tutorial which shows how the destruction of the value of money can be used to cover over the destruction of the value of assets - even while generating substantial false "income", which is fully taxable even though it doesn't exist in after-inflation form.

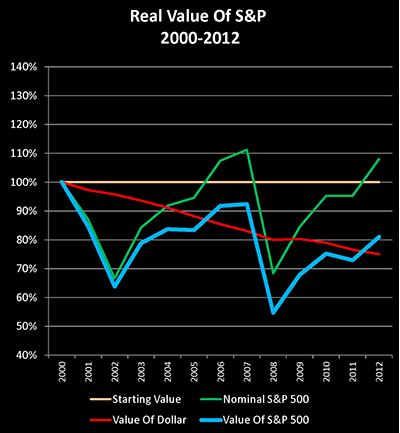

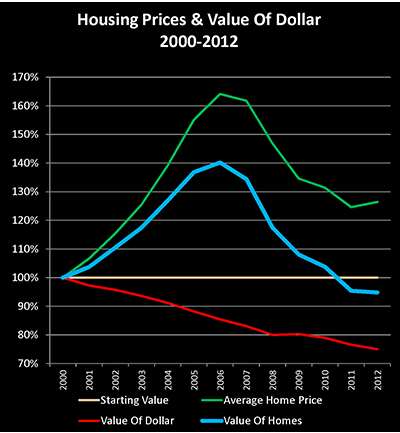

As developed in the article, when it comes to the largest components of household net worth for American households, for the 22 out of 40 years analyzed - the destruction of the purchasing power of assets was being (successfully) hidden from the public.

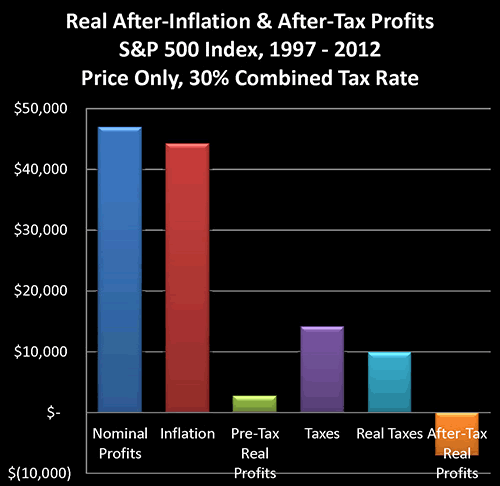

As shown in the graph above, and developed in my article, " Stealth Taxes Consume Stock Gains & Retirement Plans", about 94% of taxes paid on stock price gains held between 1997 and 2012 weren't actually paid on real income - but rather on inflation. That is, for every $1 of taxes on "real" or after-inflation income, the government was collecting $17 in taxes on phantom income - which had been created by the rate of inflation.

It is difficult to overstate the importance of inflation to the government when it comes to both the level and the reliability of investment tax collections. With no inflation in the mix, it all comes down to the economy and the luck of the markets. And in any given year, falling markets could generate increased tax deductions that could cripple government revenues.

Even a moderate annual rate of inflation, then (whether included in official government inflation estimates or not), is enough to skew investment tax returns strongly in the government's favor. And of course the higher the rate of inflation, the more powerful the financial advantages to the government of this long-standing tax, which as the US government knows quite well from eight decades of experience - most voters don't understand.

The Convergence Of The Six Overwhelming Governmental Motivations

The second half of this article takes a look at the intertwined relationships between the six reasons over the short, medium and long term, and how the six-way motivation to create inflation is far stronger than with any one reason in isolation.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2014 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.