Currency Wars Massacre in Emerging Markets, Venezuela, Argentina, Turkey...

Currencies / Currency War Jan 25, 2014 - 02:42 PM GMTBy: PhilStockWorld

By Pater Tenebrarum of Acting Man : Both Venezuela (socialist worker's paradise) and Argentina (nationalist socialist paradise) have a problem with their foreign exchange reserves. In both cases it stems from trying to keep up the pretense that their currencies are worth more than they really are. The central banks of both countries are (and have been for some time) printing money like crazy, and inflation is galloping with gay abandon. Their governments publish misleading economic statistics, that inter alia attempt to hide the true extent of the monetary debasement – in short, their inflation statistics are even more bogus than those of other governments (we are leaving aside here that the mythical 'general price level' cannot really be measured anyway).

By Pater Tenebrarum of Acting Man : Both Venezuela (socialist worker's paradise) and Argentina (nationalist socialist paradise) have a problem with their foreign exchange reserves. In both cases it stems from trying to keep up the pretense that their currencies are worth more than they really are. The central banks of both countries are (and have been for some time) printing money like crazy, and inflation is galloping with gay abandon. Their governments publish misleading economic statistics, that inter alia attempt to hide the true extent of the monetary debasement – in short, their inflation statistics are even more bogus than those of other governments (we are leaving aside here that the mythical 'general price level' cannot really be measured anyway).

Since they have maintained artificial exchange rates – coupled with capital controls, price controls and other coercive and self-defeating economic policies – people have of course felt it necessary to get their money out any way they can. This includes making use of every loophole that presents itself, so that e.g. in Venezuela, so-called 'dollar tourism' has developed, whereby citizens travel abroad for the express purpose of using their credit cards to withdraw the allowed limit in dollars at the official exchange rate (and buy some toilet paper while they have a chance to grab a few rolls).

Now the governments of both Venezuela and Argentina have reacted – the former by introducing a 'second bolivar exchange rate' for certain types of exchanges, the latter by stopping to defend the peso's value in the markets by means of central bank interventions.

Bloomberg reports on Venezuela:

“Venezuelan bonds plunged to the lowest in more than two years after the government announced the latest partial devaluation of the bolivar, this time for airlines and foreign direct investment.

Venezuelans traveling abroad, airlines and foreigners sending remittances home must use a secondary exchange rate determined at weekly auctions, Economy Vice President Rafael Ramirez said yesterday. The rate set at the latest auction was 11.36 bolivars per dollar, compared with the official rate of 6.3. Airlines operating in Venezuela fell and one carrier suspended flights.

The partial devaluation comes as the government attempts to halt a hemorrhaging of dollars that has pushed international reserves to a 10-year low. The announcement came on the same day that the country’s largest private food producer, Empresas Polar SA, said it can’t import more raw materials because authorities are delaying the release of dollars.

“The government has done too little and too late to reduce the currency distortions,” Alejandro Grisanti, economist at Barclays Plc said by telephone from New York yesterday. “This partial devaluation means more money printing by the central bank to finance the government.”

[...]

Since taking office in April, President Nicolas Maduro has struggled to boost growth and rein in inflation in a country with the world’s biggest oil reserves. Consumer prices rose 56 percent last year even as government price regulators backed by troops forced more than 1,000 businesses to cut prices on everything from toys to electronics. The country’s international reserves fell to $20.5 billion this month from more than $28 billion a year ago.

Without access to dollars at the official rate, many companies and individuals turn to the illegal black market, where the bolivar weakened from 74 to 79 per dollar after yesterday’s announcements, according to dolartoday.com, a website that tracks the exchange rate on the Colombian border.”

(emphasis added)

Here are a few relevant charts showing the situation in Venezuela:

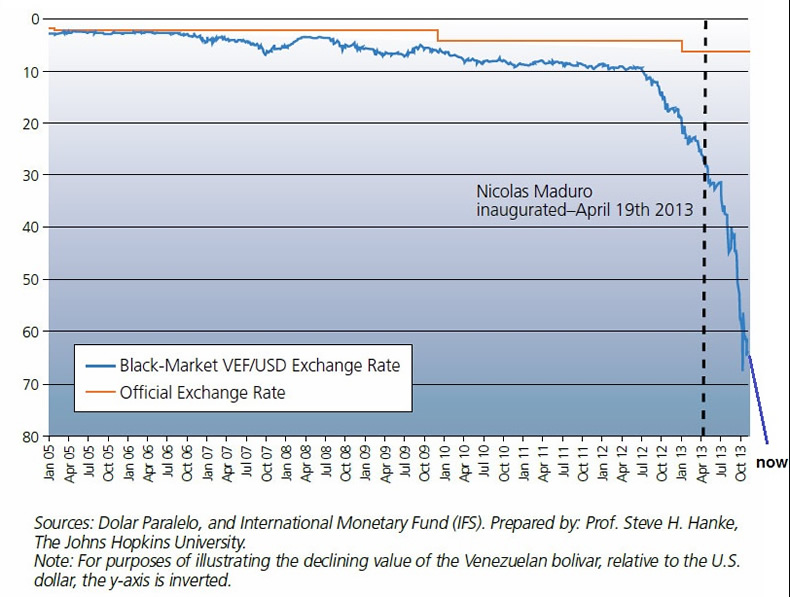

The Venezuelan bolivar, official vs. black market rate (inverted) – we have drawn in the most recent plunge of the black market rate by hand – click to enlarge.

We once said that Venezuela was a catastrophe waiting to happen, but over the past year or so it would be fair to state that the catastrophe is well underway. As incredible as that may sound, Maduro has actually managed to make things even worse after Chavez joined his ancestors in the eternal hunting grounds. Of course he merely continued where his former boss left off, with not the slightest attempt at reforming this ongoing massive economic failure. Not surprisingly, not even the workers like their worker's paradise anymore according to a recent Economist article.

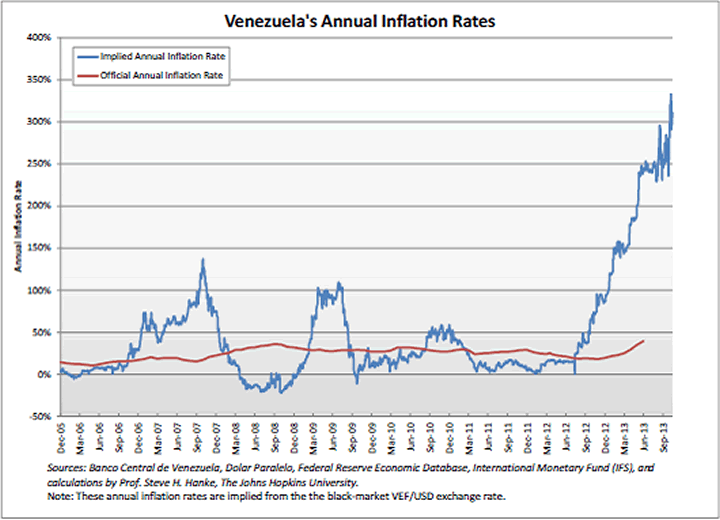

Venezuela's official inflation rate vs. its actual inflation rate (as calculated by Prof. S. H. Hanke) – click to enlarge.

Here is what happened in Argentina:

“Argentina devalued the peso the most in 12 years after the central bank scaled back its intervention in a bid to preserve international reserves that have fallen to a seven-year low.

The peso has plunged 12.7 percent over the last two days to 7.8825 per dollar at 3:45 p.m. in Buenos Aires, after falling to as low as 8.2435, according to data compiled by Bloomberg. The decline in the peso marks a policy turn for Argentina, which had been selling dollars in the market to manage the foreign-exchange rate since abandoning a one-to-one peg with the U.S. dollar in 2002.

President Cristina Fernandez de Kirchner, who said May 6 that the government wouldn’t devalue the peso, is struggling to hold onto dollar reserves which have fallen 31 percent to $29.4 billion amid annual inflation of more than 28 percent. Reserves are the government’s only source to pay foreign creditors. Since changing her economy minister, cabinet chief and the head of the central bank on Nov. 18, the peso has fallen 25 percent, the most in the world, according to data compiled by Bloomberg.”

(emphasis added)

If memory serves, Argentina's 'official' inflation rate is reported to be somewhere around 10% and economists in the country who dare to say otherwise can expect to be fined up to $100,000 per utterance (even worse punishments have been mooted).

It is quite funny to hear the government arguing that 'free markets' have been in charge – if only for a single trading day:

“Cabinet Chief Jorge Capitanich told reporters earlier today the government isn’t intervening in the peso’s decline, allowing the market, which is mostly closed to buyers of dollars, to adjust prices.

“It wasn’t a devaluation induced by the state,” Capitanich said. “For the lovers of free markets, supply and demand was expressed in the capital markets yesterday.”

[…]

Since her re-election in 2011 when capital flight almost doubled to $21.5 billion, Fernandez has put into effect more than 30 measures to keep money from leaving the country. Her policies have included blocking most purchases of foreign currencies, taxing vacations abroad and online purchases, banning units of foreign companies from remitting dividends, and restricting imports.

The controls cut the total amount traded last year in the local foreign-exchange market in half from 2010, according to data compiled by Argentina’s Mercado Abierto Electronico automated trading system. Banned from purchasing dollars for savings to protect against inflation, Argentines have turned to an illegal currency market, where the price per dollar soared to a record 12.75 per dollar, according to Buenos Aires-based newspaper Ambito.

(emphasis added)

It is a glorious 'free market' with 30 different measures restricting the free flow of capital. This would perhaps be a good moment to remind Mr. Rogoff and other economists sharing his persuasions (many of which infest the IMF), that such measures always backfire and make the situation worse (we urge readers not to take the mainstream fairy tale of Iceland's 'success' at face value). A number of these luminaries have lately indicated that capital controls should be considered by the bankrupt governments of Europe as well. Governments everywhere rarely hesitate to impose regulations curtailing the economic freedom of their citizens if a big enough 'emergency' can be used as a pretext to justify their actions, but these always and everywhere are solely benefiting the ruling class and its immediate circle of cronies, but never the citizens whose liberties are taken away.

We have unfortunately not been able to find a chart of the black market rate of the Argentine peso, but since it was never a 'fixed', but merely a heavily manipulated exchange rate, the charts of the hitherto manipulated market rate are also quite instructive:

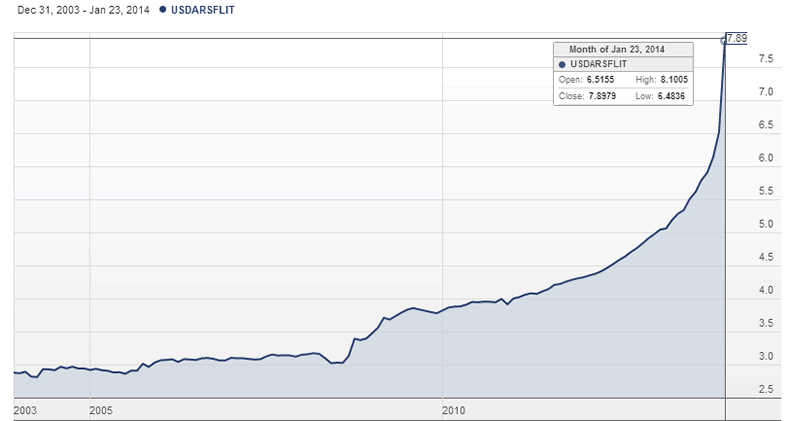

The Argentine peso vs. the dollar over the past 10 years. Ms. Kirchner and the people she chose to head the central bank have made a mess of the economy which is at least partly expressed in the peso's collapse (add about 5 pesos to arrive at the black market rate, i.e., the real rate) – click to enlarge.

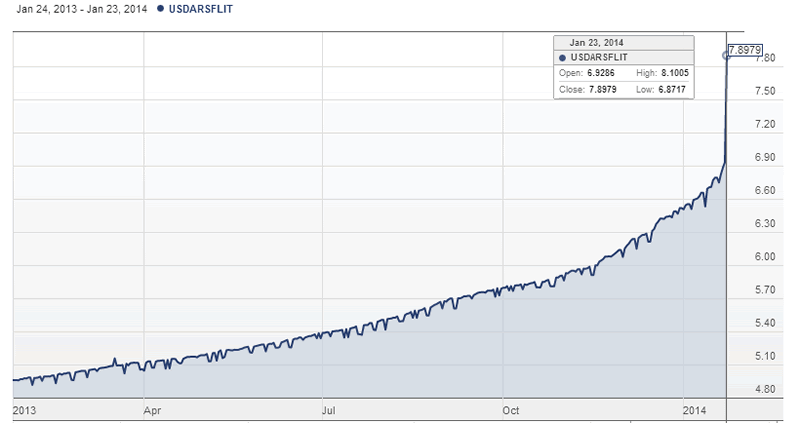

A close-up of the past three years shows the plunge of the past few days more clearly – it also shows that the decline previously took the shape of a 'managed' low-volatility devaluation. As soon as the central bank stopped intervening, it accelerated.

The Argentine peso over the past year. In the past two trading days the collapse has accelerated markedly – click to enlarge.

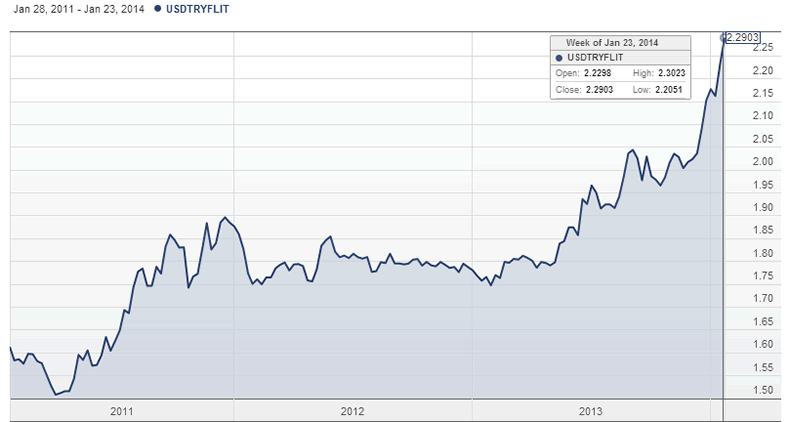

Turkey Joins the Fun

“Turkish Intervention Fails to Stem Lira Sell-Off” as the WSJ informs us. Turkey has big problems on a number of fronts right now, from political scandals and growing unrest to a burgeoning current account deficit that has left foreign lenders exposed to the tune of $350 billion (see this recent article at Zerohedge for details. Here is a link to achart showing the risk exposure disaggregated by type). The central bank has tried to intervene to slow the decline of the currency, but apparently the markets have decided to simply ignore its efforts. That is usually a sign that the 'crisis point' has arrived.

“Turkey's central bank resorted Thursday to direct currency sales for the first time in two years to prop up the lira, but the currency kept on spiraling to record lows amid a broad-based investor exodus from emerging markets.

Policy makers in Ankara started selling dollars in the European morning as the dollar jumped to 2.2973 against the lira, according to traders familiar with the transaction. The lira bounced back somewhat in response, but plunged again within hours. That drew in the central bank for a second time, traders said, but again the lira quickly sank, with the dollar soaring above 2.30 to the lira.

[…]

In a one-sentence emailed statement after the first intervention, the central bank said it was taking this action because of "unhealthy price developments." A spokesman declined further comment and the policy makers haven't provided an update.

"The central bank has wasted precious foreign-exchange reserves today on what was—and would always be in the absence of meaningful rate hikes—a futile intervention effort," said Peter Kinsella, senior foreign-currency strategist at Commerzbank in London. "The move higher shows no signs of stopping and unless we see aggressive countermeasures from the central bank, there could be a more aggressive run on the currency in the coming weeks."

(emphasis added)

To be fair, quite a few emerging market currencies as well as the currencies of developed countries that are large commodity exporters have been under pressure for some time. The Indonesian rupiah has basically crashed, the South African Rand and the Brazilian real have fallen to their weakest levels since the 2008/9 crisis sell-off, and even the Canadian and Australian dollar look a bit frayed around the edges these days.

We cannot help thinking that all this upheaval is the prelude to a more serious denouement down the road – perhaps sooner than most people currently think. Let us take a look at the Turkish lira and at Turkey's stock market. Interestingly, although the weak lira provides some support to stock prices, the stock market has also lost nearly one third of its value from last year's high. It is still trading at a fairly high level though, as there was a huge boom in Turkey in recent years (naturally, financed with lots of cheap credit).

The Turkish lira over the past three years. Its plunge has accelerated since early 2013 – click to enlarge.

Turkey's main stock market index has been under severe pressure since reaching an all time high in May of 2013 – click to enlarge.

It should be pointed out that the foreign lenders with the biggest exposure to Turkey are actually Greek banks. We kid you not, the bailed-out remnants of the Greek banking system are right in the line of fire again. That's definitely one from the 'you couldn't make this up' department. It should also hasten the deployment of Super-Mario's 'QE-bazooka'.

On Thursday, a number of stock markets, from Japan's Nikkei to the US stock market incidentally had quite a bad hair day. Although most press reports identified the fact that China's manufacturing PMI came in slightly lower than expected as the culprit, it seems to us that there is perhaps a more profound problem boiling under the up until recently tranquil surface.

One of the sources of all this recent trouble is quite possibly Japan's decision to inflate with the help of a generous dose of 'QE' and deficit spending. Although the yen's anticipatory move lower could so far not really be justified by actual money supply growth, the fact remains that it did decline rather sharply. This in turn has put pressure on Japan's competitors in Asia, which in turn has put pressure on their suppliers in commodity-land and has altered capital flows, etc.

Recall that the Asian crisis of the late 1990s was preceded by a devaluation in China, after which the yen started weakening rather precipitously as well. Of course the situation was different in that many of the countries hit by the crisis had their currencies pegged to the dollar at the time, but the point remains that a weakening yen preceded the event. A parallel is that there are once again quite a few countries that sport large current account deficits and have experienced major credit and asset booms. In short, there are many balloons waiting for a pin.

- Phil

Philip R. Davis is a founder of Phil's Stock World (www.philstockworld.com), a stock and options trading site that teaches the art of options trading to newcomers and devises advanced strategies for expert traders. Mr. Davis is a serial entrepreneur, having founded software company Accu-Title, a real estate title insurance software solution, and is also the President of the Delphi Consulting Corp., an M&A consulting firm that helps large and small companies obtain funding and close deals. He was also the founder of Accu-Search, a property data corporation that was sold to DataTrace in 2004 and Personality Plus, a precursor to eHarmony.com. Phil was a former editor of a UMass/Amherst humor magazine and it shows in his writing -- which is filled with colorful commentary along with very specific ideas on stock option purchases (Phil rarely holds actual stocks). Visit: Phil's Stock World (www.philstockworld.com)

© 2014 Copyright PhilStockWorld - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

PhilStockWorld Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.