Stock Market Bottoms Have Two Elements: We’re Still Missing One

Stock-Markets / Stock Markets 2014 Feb 06, 2014 - 01:23 PM GMTBy: PhilStockWorld

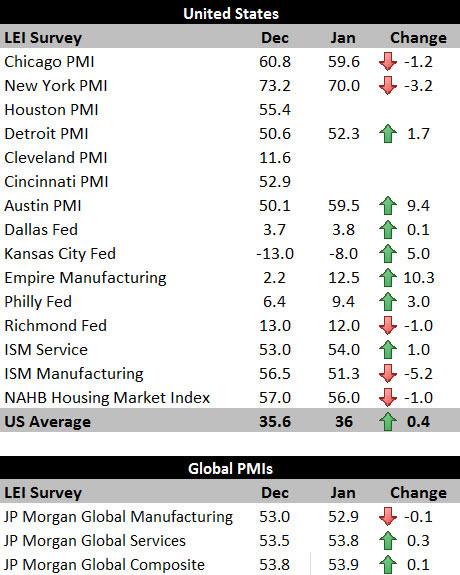

Courtesy of Doug Short: Monday’s ISM wipeout pushed the stock market into deeply oversold territory as fear levels in the market began to surge. The ISM Manufacturing PMI came in at 51.3 versus the estimated 56.0 reading and down from 57.0 for December 2013 and was the biggest miss in years, elevating growth fears. However, while many bears will dismiss pundits blaming the cold weather and see the miss as a sign of things to come, the ISM national PMI is just one survey and it moved opposite to many of the regional Fed manufacturing surveys for January. In fact, when reviewing various PMI readings across the country there were more positive improvements than negative with the average among surveys increasing during the month, as shown below. Note the positive changes in the Austin PMI (+9.4) and the Empire Manufacturing Survey (+10.3) were greater in size than the negative declines. Another encouraging development was a slight uptick in the JP Morgan Global Composite PMI.

Courtesy of Doug Short: Monday’s ISM wipeout pushed the stock market into deeply oversold territory as fear levels in the market began to surge. The ISM Manufacturing PMI came in at 51.3 versus the estimated 56.0 reading and down from 57.0 for December 2013 and was the biggest miss in years, elevating growth fears. However, while many bears will dismiss pundits blaming the cold weather and see the miss as a sign of things to come, the ISM national PMI is just one survey and it moved opposite to many of the regional Fed manufacturing surveys for January. In fact, when reviewing various PMI readings across the country there were more positive improvements than negative with the average among surveys increasing during the month, as shown below. Note the positive changes in the Austin PMI (+9.4) and the Empire Manufacturing Survey (+10.3) were greater in size than the negative declines. Another encouraging development was a slight uptick in the JP Morgan Global Composite PMI.

Source: Bloomberg

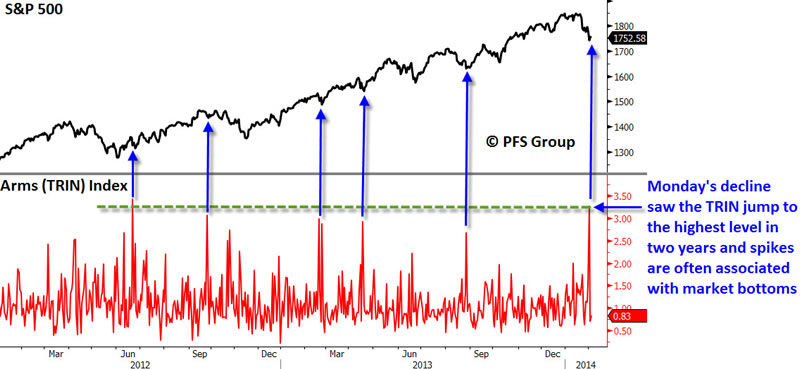

Given these details, the reaction to Monday’s ISM miss appears to be overdone and drove the Arms (TRIN) Index to the highest level in over two years. As shown below, readings north of 2.5 tend to correlate to market bottoms and should at a minimum indicate a pause in the current pullback.

Source: Bloomberg

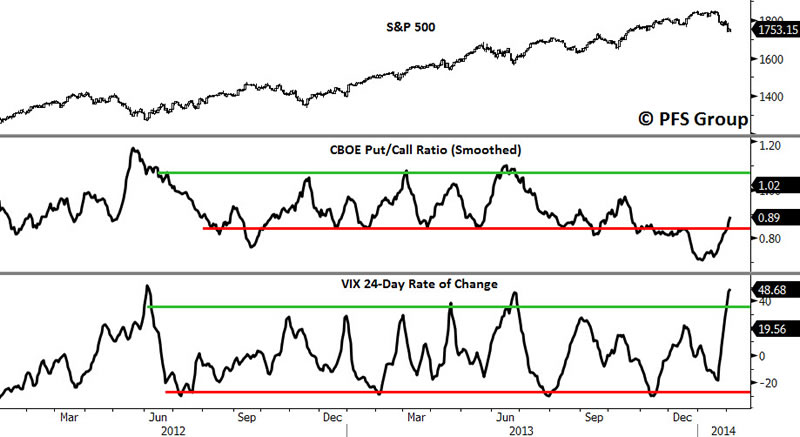

The recent decline has also seen the VIX Index spike with its 1-month rate of change resting at the highest levels since the June 2012 lows and levels associated with prior bottoms. What is discouraging is the lack of put buying to suggest elevated levels of fear associated with bottoms. This means we may need to see a retest of the recent low or slightly lower levels to cause enough fear to put in a sustainable bottom.

Source: Bloomberg

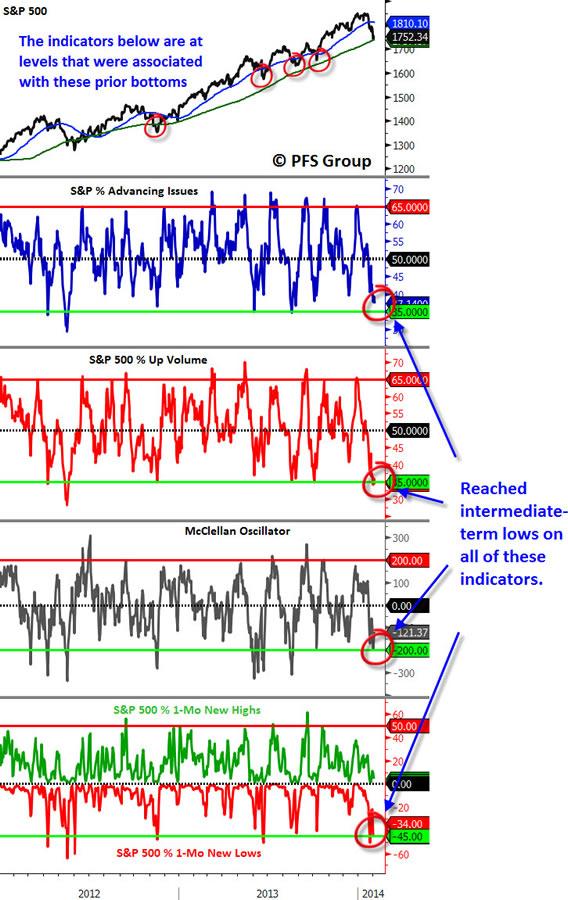

There are two conditions for a market bottom and so far we have one of them, which is a significantly oversold market. As seen below, all four of my intermediate-term indicators have reached oversold territory that has marked prior lows.

Source: Bloomberg

Another set of indicators I track also confirm we’ve reached an oversold condition associated with bottoms (panels 2-5 below). However, what is missing is the second ingredient of a market low, which is a surge of buying to suggest that selling pressure has been exhausted and prices have reached a low enough level to bring out the bulls.

This can be seen by a lack of MACD buy signals on the S&P 500 over the last few days. A strong surge of MACD buy signals by the 500 members within the S&P 500 over a short time period (10 days) is often the final seal needed to mark a bottom, with readings north of 15% typically seen after a market bottom is in (see panel 6 below).

Source: Bloomberg

Given the lack of fear seen in the put/call ratio and lack of a surge in MACD buy signals in the S&P 500 members, I believe at best we will see a weak rally attempt until we get the jobs data on Friday. Should the report disappoint we will likely see a retest of the recent lows and likely a further drop down to the 200d MA on the S&P 500 currently at 1709. However, if the jobs data confirms the economy is on solid footing we may get the surge in buying that we are missing to call a market bottom and end the current pullback.

What can’t be stressed enough is that even if the recent low of 1737.92 gets breached on the S&P 500 we are still likely experiencing an overdue correction in an ongoing bull market. This current correction may turn out to be deeper than your average 5% correction since 2013 was such an atypical year for consistent stock returns.

To put things in perspective, consider the following: Going back all the way to 1928 on the S&P 500 shows an average of three 5%+ corrections each year. Outside of last year, since 1961 there have been only three years when the market didn’t have more than one 5%+ correction. Suffice to say, volatility is the norm, not the exception, with this current one clearly overdue.

While some noted bears have taken this recent pullback as an opportunity to warn of a major crash (again), don’t be so quick to jump ship as we still find many supports for this being another pullback, as I’ll identify below. For example, most bear markets are associated with recessions and the chance of recession on the horizon still remains remote. Our recession probability model assigns only a 4% chance the U.S. is slipping into a recession. For the recessionary alarm bells to ring we need to see readings north of 20%, which we are still far away.

Source: Bloomberg

Also arguing against a coming recession is the Philadelphia Fed’s State Leading Index survey, which measures the leading economic indicators for all 50 states. We just received the December readings this week and the survey shows that 47 of the 50 states are expected to grow over the next six months. When 94% of the nation is expected to show positive growth over the next half year, talk of a coming recession is highly premature.

Source: Philadelphia Fed

The Philly Fed constructs a national index based on the 50 state indexes and the national index is projected to grow 1.65% over the next six months. As shown below, typically we see the national index deteriorate well before the stock market peaks and typically falls below 0% just as a recession starts. We currently rest near the highs seen since the recovery began and why a recession occurring in the near-term is highly unlikely.

Source: Bloomberg

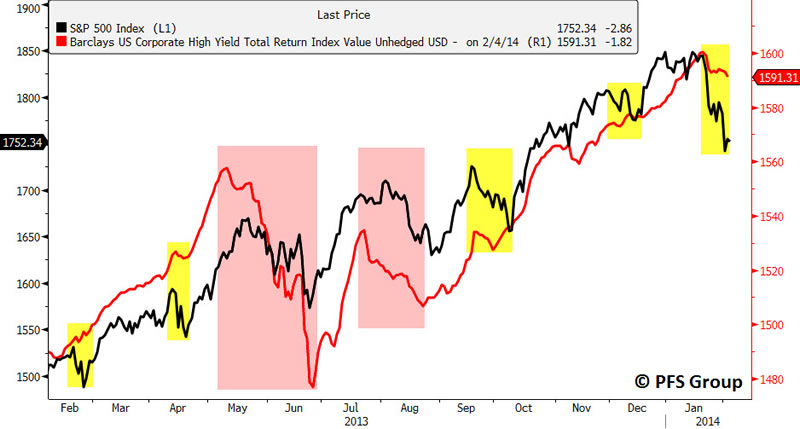

Outside of economic indicators, looking at market signals for a read on the state of the stock market also shows healthy developments. An example is looking at the credit market, specifically the junk bond market, as you often see major signs of financial stress arise there before the stock market.

Highlighted below is the Barclays US Corporate High Yield (Junk) Total Return Index relative to the S&P 500. The two pullbacks we had in 2013 were associated with declines in the High Yield Index (red shaded regions) but anytime there was a market selloff not associated with a sizable decline in the High Yield Index the market tended to regain its footing and take its cue from the junk bond market (yellow boxes). Of note is that we have only seen a tiny decline in the junk bond index while the S&P 500 has taken quite a hit and suggests the selloff in the stock market is overdone.

Source: Bloomberg

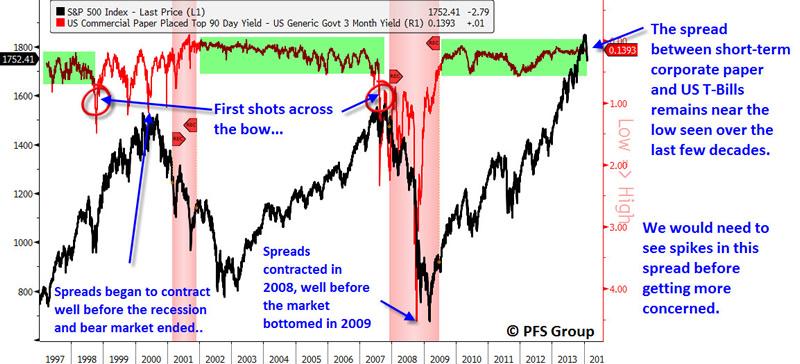

Other signals from the credit markets suggest this is likely a pullback and not indicative of a major top. One of my favorite credit measures is the yield spread between corporate short-term commercial paper and US T-bills, which measures the relative default risk between corporate America relative to the US Treasury. During economic expansions the yield spread between the two should be low while as we begin to slip into recession and corporate earnings near a peak, investors begin to price greater default risk on corporations relative to the Treasury by requiring higher yields to invest in commercial paper.

The spread begins to spike as the market discounts a coming recession, with the initial spike serving as a major red flag (see red circled areas below). These initial spikes occurred well before both prior recessions and market tops and they also served as early warnings of a coming bear market.

Source: Bloomberg

Note that the spikes in the spread began to diminish in 2001-2002 and returned to normal levels before the market bottomed. Also of note, the spread peaked in late 2008 several months before the market bottomed in March 2009. The fact that commercial paper and T-Bill spreads rest near multi-decade lows should give the bulls out there plenty of conviction this is just a decline and not the early innings of a bear market.

Summary

Currently the market is at an oversold condition similar to what we’ve seen at all of the significant bottoms over the last few years. However, we’ve yet to see clear evidence of exhaustion in selling followed by a surge in enthusiastic buying, which is the final evidence of a market bottom. So far we have a tepid rally attempt as buyers are likely waiting on the sidelines heading into the big payroll report this Friday that has the potential to send the market flying in either direction. Should the jobs report come in ahead of expectations we may finally see the surge in buying to declare a market bottom. On the other hand, if we get another disappointment in Friday’s labor report like Monday’s poor ISM PMI reading, we are likely to breach the recent lows and head further south towards the 200 day moving average on the S&P 500 (1709 currently).

Even if the labor report comes in weak and the market declines further, given the above we are likely only experiencing a correction in an ongoing bull market rather than a full blown bear market.

- Phil

Philip R. Davis is a founder of Phil's Stock World (www.philstockworld.com), a stock and options trading site that teaches the art of options trading to newcomers and devises advanced strategies for expert traders. Mr. Davis is a serial entrepreneur, having founded software company Accu-Title, a real estate title insurance software solution, and is also the President of the Delphi Consulting Corp., an M&A consulting firm that helps large and small companies obtain funding and close deals. He was also the founder of Accu-Search, a property data corporation that was sold to DataTrace in 2004 and Personality Plus, a precursor to eHarmony.com. Phil was a former editor of a UMass/Amherst humor magazine and it shows in his writing -- which is filled with colorful commentary along with very specific ideas on stock option purchases (Phil rarely holds actual stocks). Visit: Phil's Stock World (www.philstockworld.com)

© 2014 Copyright PhilStockWorld - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

PhilStockWorld Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.