The Shocking Deals Behind Bankster Fines, The Real Reason No One Goes to Jail

Politics / Banksters Feb 20, 2014 - 12:04 PM GMTBy: Money_Morning

Shah Gilani writes: Headline news about banks settling charges for violating rules, regulations, and laws - and announcements of the fines they agree to pay - appears every day...

Shah Gilani writes: Headline news about banks settling charges for violating rules, regulations, and laws - and announcements of the fines they agree to pay - appears every day...

Rarely - if ever - do they reveal how much money is really being paid or where it's going...

They also seldom explain what kinds of settlements are reached...

Or how banks negotiate what they'll actually pay and to whom... or how they negotiate tax deductibility of fines... or how they get "credits" for fines they never pay... or how insurance covers some of it...

This is not one of those stories... this is about what really happens behind the banksters' doors.

The details are shocking...

These Massive Penalties Are Quieted to Protect "Us"

First of all, some settlements never see the light of day. They can be deemed "confidential" by regulators settling with a miscreant bank.

Why are some settlements confidential? Because bank lawyers argue their clients are exposed to "reputational risk" and details of their "alleged" wrongdoing, which they typically "neither admit nor deny," could impact the health of the bank. Of course, that could create "systemic risk," they argue, due to the damage to the public's perception of trust in their banking institutions.

The FDIC, the Federal Deposit Insurance Corporation, is one agency that thinks keeping settlements confidential will keep folks from withdrawing money from law-breaking banks. They believe it protects the agency from having to bail out remaining depositors if those banks eventually fail.

Last year, for example, the FDIC, ignoring the Federal Deposit Insurance Corp. Improvement Act of 1991 that mandates settlements be made public, fined Deutsche Bank $54 million for packaging and selling bad mortgage-backed securities to a failed bank, but no one heard about it.

According to E. Scott Reckard, who reported on the confidential settlement for the Los Angeles Times, "The deal might have made big headlines, given that the bad loans contributed to the largest payout in FDIC history, $13 billion. But the government cut a deal with the bank's lawyers to keep it quiet: a 'no press release' clause that required the FDIC never to mention the deal 'except in response to a specific inquiry.'"

Also last year, according to the Financial Times, Wells Fargo "quietly settled" with the Federal Housing Finance Agency "for allegedly misleading disclosures on mortgage securities" it sold to Fannie Mae and Freddie Mac. The FT went on to say, "unlike deals with UBS and JPMorgan, Wells' settlement, which is believed to be worth less than $1 billion, is governed by a confidentiality agreement."

The Real Reason No One Goes to Jail

Of course, whether their settlements are confidential or not, too-big-to-fail banks have only faced civil charges, for which they have to pay fines. There have been no criminal prosecutions of any banks or banksters. That's because of the doctrine: too-big-to-fail and too-big-to-jail.

None of the agencies that bring civil actions against the big banks can pursue them criminally. If a bank's actions are so egregious that they warrant a criminal investigation, the agency passes along their files to the Department of Justice.

But, the DOJ hasn't pursued any criminal action against any bank or bankster.

Why? Because as Lanny Breuer, who was chief of the Criminal Division of the DOJ from April 2009 to March 2013, explained in a 2012 speech to the New York City Bar Association, "To be clear, the decision of whether to indict a corporation, defer prosecution, or decline altogether is not one that I, or anyone in the Criminal Division, take lightly. We are frequently on the receiving end of presentations from defense counsel, CEOs, and economists who argue that the collateral consequences of an indictment would be devastating for their client. In my conference room, over the years, I have heard sober predictions that a company or bank might fail if we indict, that innocent employees could lose their jobs, that entire industries may be affected, and even that global markets will feel the effects."

Lanny Breuer left the DOJ last year to return, for a reported $4 million a year, to his old white-collar criminal defense firm Covington & Burling, who represents Morgan Stanley, Bank of America, and others. Attorney General Eric Holder is also a Covington alumni.

Besides not being pursued criminally, when banks and banksters are caught breaking laws they are slapped on the wrist and gifted with Deferred Prosecution Agreements (DPAs) and Non-Prosecution Agreements (NPAs). These consistently handed out agreements, in the 20 years since their emergence as an alternative to indictments, are, in the words of the Harvard Law School, "a mainstay of the U.S. corporate enforcement regime, with the U.S. Department of Justice (DOJ) leading the way."

According to the Harvard Law School Forum on Corporate Governance and Financial Regulation, "These types of agreements have achieved official acceptance as a middle ground between exclusively civil enforcement (or even no enforcement action at all) and a criminal conviction and sentence. DPAs and NPAs allow companies and prosecutors to resolve high-stakes claims of corporate misconduct - often the subject of sizable media attention - through agreements to obey the law, cooperate comprehensively with the government, adopt or enhance rigorous compliance measures, and often pay a hefty monetary penalty."

You'll Be Surprised Where the Fine Money Lands

So, how does the DOJ and how do attorneys general, and the SEC and CFTC, and the FHFA and FREC and any and all of the other alphabet soup of regulators overseeing the Lords of the Banking Underworld determine what settlement fines banks have to pay?

They negotiate them, of course, with the banks.

Before they get to any settlement amounts, the banks first negotiate their DPAs and NPAs (deferred and non-prosecution agreements) and confidentiality, if they can get it.

They always want to "neither admit nor deny" allegations, and usually get that, although the SEC recently changed its longstanding settlement policy and now requires "admissions of misconduct in cases where heightened accountability and acceptance of responsibility by a defendant are appropriate and in the public interest." The first settlements under the new policy just came in actions against Philip A. Falcone and his firm, Harbinger Capital Partners, and JPMorgan Chase & Co.

At the same time the banks are negotiating how much they will pay, they are negotiating who they will pay what to, whether they will pay in cash, make restitution in some other way, or get credit for costs and systems to be put in place to help the harmed or not commit the same violations again.

It's important to negotiate who gets paid. The banks don't like paying the federal government. Why? Because federal law prohibits deducting fines and other penalties paid to the government, but allows write-offs for non-federal entities.

To be sure, the federal government wants to extract its pound of flesh. Why? Because monies paid (wired directly) to the Department of Treasury help reduce the deficit. Some people call that government extortion, and it may be, but the banks wouldn't have to pay "get out of jail" money if they weren't guilty of violations and crimes in the first place.

State attorneys general get money for their state, which is passed through the Treasury, which puts it in the state's "fund."

The Securities and Exchange Commission extracts large fines too. Before the passage of the Sarbanes-Oxley Act in 2002, the SEC usually sent civil monetary penalties to the Treasury. Now, a provision in Sarbanes-Oxley known as "Fair Funds" lets the SEC add civil penalties to ill-gotten gains, put them in a Fair Fund, and return all of the money to victims. If there are no ill-gotten gains disgorged, the penalty goes to the Treasury.

In some cases the SEC has added $1 in disgorgement to civil penalties so that fines paid by companies can be used to compensate investors.

In any event, the regulatory agencies don't get to keep any of the civil monetary penalties they extract from banks, which would make sense if they could use fines to offset federal budget outlays that fund the agencies.

For example, the CFTC, which has expanded responsibilities because of Dodd-Frank financial reform legislation and has to step up enforcement actions (besides Libor settlements, the agency brought civil charges against brokerage MF Global and is examining whether banks owning commodity warehouses manipulated metals prices) still has to grovel to get adequately funded to do its job.

The agency is facing a huge budget crunch this year after the Republican-dominated House of Representatives last year approved maintaining the current CFTC funding level of $195m, which is less than the Obama administration's 2014 fiscal year budget request of $315m.

But it is difficult to change the budgeting process for the CFTC, partly because lawmakers on the agriculture committees in Congress rely on their jurisdiction over the CFTC to help raise money for their political campaigns. Which is how it goes with regard to funding all the regulatory agencies.

So, where does the money we read about the banks paying actually go? Here are some examples and explanations about what's behind the curtain.

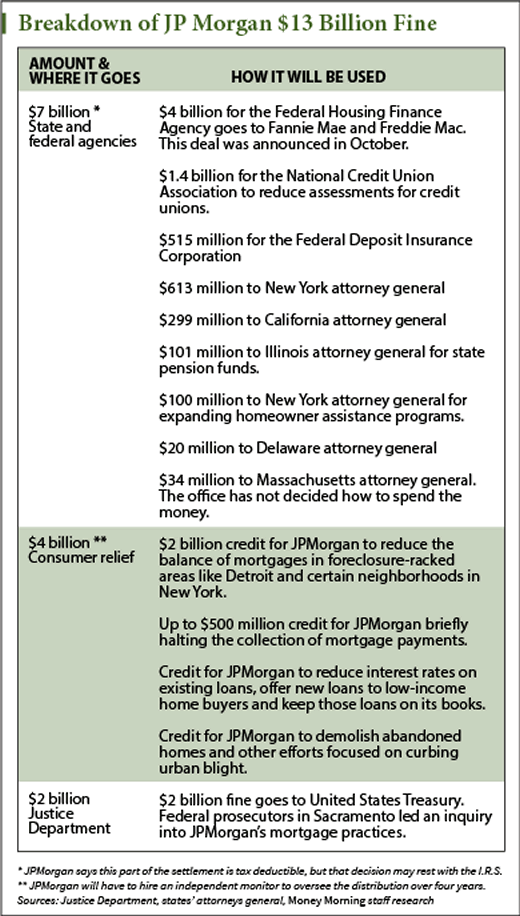

JPMorgan Chase just agreed to the largest single settlement fine ever, $13 billion for its part in causing the mortgage-related financial meltdown. Here's the breakdown of payments:

The headline number was $13 billion. But, $4 billion of that had already been paid to Fannie and Freddie, who passed that along to the Treasury in the form of dividends because the Treasury Department essentially owns Fannie and Freddie. Another $4 billion was in the form of "credits" that the bank gets for setting up facilities to aid aggrieved homeowners, credits that aren't cash outlays and that will ultimately help the bank's bottom line as they force borrowers to continue to be clients and customers of the bank to get any "restitution" or ancillary benefits.

Of the $13 billion, JPMorgan is going to take a $7 billion write-off. While the IRS has the authority to challenge that write-off, the IRS has rarely ever challenged a big bank on the write-offs they take against settlements. Maybe that has something to do with the negotiations that the public never hears about.

Prior to the JPM $13 billion settlement headline, there was the $25 billion settlement a joint state-federal group announced with the nation's five largest mortgage services: Bank of America Corporation, JPMorgan Chase & Co., Wells Fargo & Company, Citigroup, Inc., and Ally Financial, Inc. (formerly GMAC). The five banks service nearly 60% of the nation's mortgages.

"This agreement delivers real help to homeowners affected by the banks' dual tracking and other improper mortgage- and foreclosure-related processes," said Colorado Attorney General Suthers. "As a result of this settlement, the banks will end a series of problematic processes that put homeowners at a severe disadvantage during the foreclosure process. This settlement will not solve every problem with the housing market, but it goes a long way to helping homeowners in distress now and leveling the playing field for consumers."

Under the agreement, the five servicers agreed to the $25 billion penalty under a joint state-national settlement structure:

- Servicers commit a minimum of $17 billion directly to borrowers through a series of national homeowner relief effort options, including principal reduction.

- Servicers commit $3 billion to an underwater mortgage refinancing program.

- Servicers pay $5 billion to the states and federal government ($4.25 billion to the states and $750 million to the federal government).

- Homeowners receive comprehensive new protections from new mortgage loan servicing and foreclosure standards.

- An independent monitor will ensure mortgage servicer compliance.

- States can pursue civil claims outside of the agreement including securitization claims as well as criminal cases.

- Borrowers and investors can pursue individual, institutional, or class action cases regardless of agreement.

Sounds like a good deal for the poor folks who were illegally foreclosed and thrown out of their homes, for the folks who lost everything and had their credit destroyed by manipulating banks, right?

No really. It's a good deal for the banks because they get to write off all the "credits" they get for setting up these homeowner relief facilities. And they get to write off all the principal amounts they "forgive."

For homeowners who get relief starting in 2014, it's not such a good deal.

Why? Because the Mortgage Forgiveness Debt Relief Act expired Dec. 31, 2013.

The Act prevented homeowners who go through a short sale or foreclosure from being taxed on the amount of their mortgage debt that had been forgiven. (Normally, debt that has been forgiven by a lender counts as taxable income.) A short sale transaction would have had to close before Dec. 31, 2013 in order to take advantage of the Act's tax exemption.

By way of example, if a homeowner makes $40,000 in 2014 and by the grace of one of the big banks gets their mortgage principal reduced by $100,000 in the same year, their taxable income for 2014 would be on $140,000. That's some deal the government cut to teach the banks a lesson (who write off the $100,000) and the homeowners who suffered at their greedy hands.

Of course, the always-considerate IRS offers a tax-saving alternative with their "Insolvency Clause," which is a way to avoid paying income tax on forgiven debt.

The clause states that a seller is exempt from paying tax on any forgiven debt to the extent that they are insolvent. In other words, if the seller's debts and liabilities exceed their assets by more than the amount of debt forgiven, they do not have to pay taxes on the forgiven debt.

Even when the big banks have to pay, they often don't have to pay. That's because they have insurance.

Traditional D&O (directors and officers) insurance policies typically cover losses based on damages, judgments, settlements, and cover defense costs. In the past, D&O policies expressly excluded from "covered loss" things like punitive damages, exemplary and multiplied damages.

But that's changed. Many insurance policies now allow coverage for such damages, while some allow coverage only for vicarious liability for such damages, and still others preclude coverage entirely.

Recently however, the FDIC announced that it will impose a fine on any financial institution that has purchased D&O or other insurance to cover civil money penalties. And as far as state governments and the question of insurability in regard to coverage for punitive, exemplary, and multiplied damages, responses have been anything but uniform.

Besides the question of legal insurability, there's the question of market willingness to insure.

Which apparently isn't much of a question after all. From a covered loss perspective, D&O insurance has continued to expand, even in the face of mounting financial exposures.

A recent report on D&O insurance I came across states, "This split among the states on insurability has resulted in the inclusion of 'most favorable jurisdiction' language on this issue in most D&O policies, providing that the policy's coverage will be interpreted by that state's law that most favors the insurability of such damages and that has some connection to the claim. For many insureds, this uncertainty over coverage for punitive, exemplary and multiplied damages, particularly when domiciled or operating in a state that prohibits insurance for such damages, has made the purchase of insurance 'off shore' - and therefore potentially outside the reach or jurisdiction of the U.S. court system - more attractive."

It doesn't seem to matter: Whether settlements are confidential or seemingly public, however settlements are structured, or whomever pays, the banks have been getting away with murder - well, almost.

There are a few voices in Congress trying to be heard above the banks' never-ending ringing cash registers. Three bills have been floated to make settlements fairer and more transparent. None have gone anywhere.

In the first week of January 2014, Senators Elizabeth Warren (D-MA) and Tom Coburn (R-OK) introduced the Truth In Settlements Act. Before that in November 2013 Senator Jack Reed (D-RI) and Senator Charles Grassley (R-IA) introduced the Government Settlement Transparency and Reform Act. And a few weeks before that bill was introduced, over at the House of Representatives, Rep. Peter Welch of Vermont and Luis Gutierrez of Illinois introduced the Stop Deducting Damages Act. None of the bills have gone anywhere.

That's how the settlements games are played.

Next week I'm going to have some heavy-hitters weigh in on what should be done about this, why things aren't being done, and whether anything should be done, or are the banks just getting a bad rap. That conversation will be interesting, I can guarantee you that.

Source : http://moneymorning.com/2014/02/20/shocking-deals-behind-banksters-fines/

Money Morning/The Money Map Report

©2014 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.