Worst of the Credit Crisis May be over as Investors Switch from Bonds to Equities on Inflation Concerns - Part 1

Stock-Markets / Financial Markets Apr 27, 2008 - 05:06 PM GMT

The last week was characterized by investors increasingly taking the view that the worst of the credit crisis was over. They seemed to be shrugging off further substantiation of the dreadful state of the US housing situation, as they digested the latest round of quarterly earnings reports. The latter ranged from plunging profits from Bank of America (ANC) to a dreadful report from Ambac (ABC) to guidance from Microsoft (MSFT) that failed to live up to investors' expectations.

The last week was characterized by investors increasingly taking the view that the worst of the credit crisis was over. They seemed to be shrugging off further substantiation of the dreadful state of the US housing situation, as they digested the latest round of quarterly earnings reports. The latter ranged from plunging profits from Bank of America (ANC) to a dreadful report from Ambac (ABC) to guidance from Microsoft (MSFT) that failed to live up to investors' expectations.

Stock markets see-sawed as investors assimilated the various economic and earnings reports, with the S&P 500 Index eventually eking out a positive return of 0.5% for the week, thereby consolidating the previous week's gains (+4.3%).

Evidence of a more relaxed undertone among equity investors was confirmed by the Volatility Index (VIX) falling to its lowest level of the year and below the psychological 20 barrier, i.e. the level that had set the ceiling for fear until the credit crunch began in July 2008.

Evidence of a more relaxed undertone among equity investors was confirmed by the Volatility Index (VIX) falling to its lowest level of the year and below the psychological 20 barrier, i.e. the level that had set the ceiling for fear until the credit crunch began in July 2008.

The real action, however, was in the government bond markets where prices plunged (i.e. yields jumped) as investors were spooked by life-time high oil prices, stoking inflation pressures (see graph alongside of the price of the 10-year US Treasury Note). Furthermore, safe-haven considerations, which were dominant for most of the duration of the credit crisis, took a back seat on the prospect of a better US economy ahead.

The real action, however, was in the government bond markets where prices plunged (i.e. yields jumped) as investors were spooked by life-time high oil prices, stoking inflation pressures (see graph alongside of the price of the 10-year US Treasury Note). Furthermore, safe-haven considerations, which were dominant for most of the duration of the credit crisis, took a back seat on the prospect of a better US economy ahead.

A word of caution, however, came from John Hussman ( Hussman Funds ) who said: “Aside from short-term speculative pressures (largely driven by relief about Bear Stearns), nothing in recent data suggests a material abatement of recession risk, mortgage risk, profit margin risk, or dollar risk.”

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

Last week saw only a handful of economic reports, showing further declines in the housing market, better-than-expected news for weekly initial jobless claims and durable orders, excluding transportation, and another depressed consumer sentiment reading coming in at a 26-year low.

Asha Bangalore ( Northern Trust ) said: “Although the National Bureau of Economic Research is yet to announce that a recession is under way, incoming data strongly suggest that the economy is in recession. The more important questions now are about the depth and duration of the recession and what the nature of the recovery process is. In terms of duration, the recession could be close to the average post-war recession of 10 months, but the severe credit crunch that is hampering the smooth functioning of financial markets supports forecasts of a prolonged and sluggish recovery.”

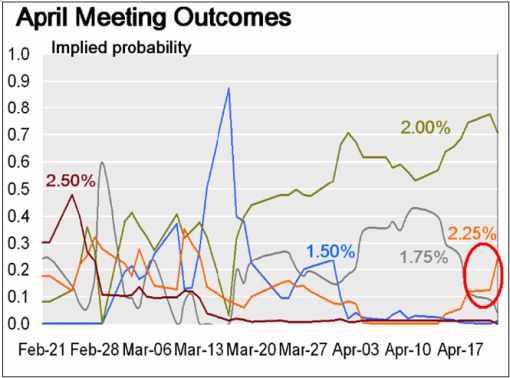

As far as Wednesday's interest rate announcement by the FOMC is concerned, the graph below indicates that the Fed fund futures see a 70% chance of a 25 basis point rate cut from 2.25% to 2.0% (green line) and a 25% chance of no rate cut (orange line). One month ago, the futures saw an 88% chance of a 50 basis point cut; one week ago it was a 46% chance. Now the futures see only a 5% chance of a 50 basis point cut. This serves as confirmation of how market participants' apprehension about the credit crisis has lessened.

Source: Paul Kedrosky, Infectious Greed , April 24, 2008.

Elsewhere in the world, the Bank of England on Monday announced a massive operation to support liquidity in British banks. The BoE will offer to acquire asset-backed securities from banks in exchange for Treasury bills, expecting to swap £50 billion to help restore confidence to the sector.

Germany's Ifo Business Climate Index came in below expectations in April, suggesting that German industry and trade are starting to feel the pinch of the strong euro and high commodity prices.

Further to the east, Japan's headline core CPI rate, which includes fast-rising energy prices, leapt 1.2% year-on-year, the highest in 10 years. This is seen as an indication that Japan could be close to shaking off 10 years of deflation.

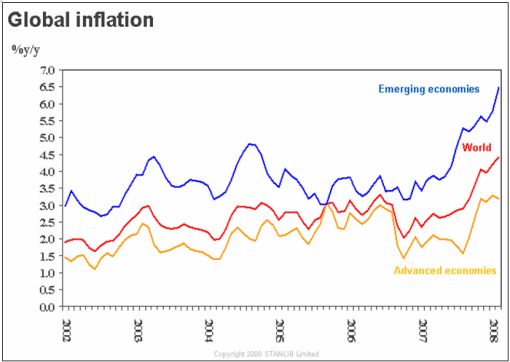

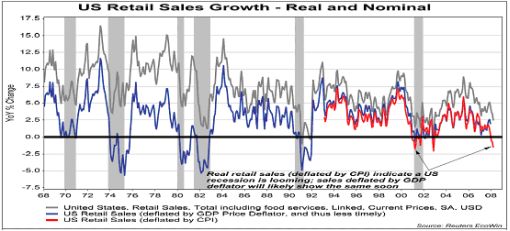

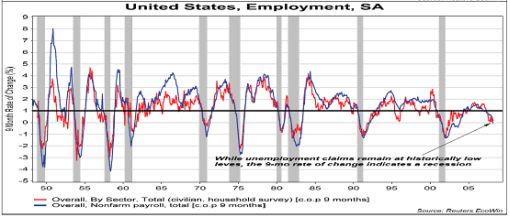

With prices rising strongly throughout the world (as shown in the graph below), investors appear to be placing more emphasis on the inflation outlook than on credit-related matters at the moment.

Source: Stanlib

WEEK'S ECONOMIC REPORTS

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Apr 22 | 10:00 AM | Existing Home Sales | Mar | 4.93M | 4.90M | 4.92M | 5.03M |

| Apr 23 | 10:00 AM | Existing Home Sales | Mar | - | 4.90M | 4.95M | 5.03M |

| Apr 23 | 10:30 AM | Crude Inventories | 04/19 | 2421K | NA | NA | -2356K |

| Apr 24 | 8:30 AM | Durable Orders | Mar | -0.3% | -0.5% | 0.0% | -0.9% |

| Apr 24 | 8:30 AM | Initial Claims | 04/19 | 342K | 375K | 375K | 375K |

| Apr 24 | 10:00 AM | New Home Sales | Mar | 526K | 585K | 580K | 575K |

| Apr 25 | 10:00 AM | Mich Sentiment-Rev. | Apr | 62.6 | 63.2 | 63.2 | 63.2 |

Source: Yahoo Finance , April 25, 2008.

In addition to the FOMC's interest rate announcement at the end of its two-day meeting on Wednesday (April 30), the next week's economic highlights, courtesy of Northern Trust , include the following:

1. Real GDP (April 30): The US economy is most likely to post the first decline in GDP (-0.1%) since the third quarter of 2001. Broad-based weakness inclusive of significant decelerations in consumer spending and business investment expenditures and a sharp decline in residential investment expenditures are predicted to have held back the growth of GDP in the first quarter. Consensus : 0.3%. The forecast range for GDP growth in the first quarter is -0.2% to +1.5%.

2. Personal Income and Spending (May 1): The earnings and payroll numbers for March indicate only a small gain in personal income (+0.1%). Auto sales fell in March (15.1 million versus 15.4 million in Feb.) and non-auto retail sales were noticeably weak, which points to likely drop in goods outlays. An offset from services should leave consumer spending nearly flat in March. Consensus : Personal income +0.3%, consumer spending 0.3%.

3. ISM Manufacturing Survey (May 1): The consensus for the manufacturing ISM Composite Index is 48.0 versus 48.6 in March. If the consensus forecast is accurate, it would be the fourth monthly reading below 50 in the last five months. Consensus : 48.0 versus 48.6 in February.

4. Employment Situation (May 2): Payroll employment in April is predicted to show the fourth monthly decline (-75,000) following a loss of 80,000 jobs in March. The jobless rate is predicted to have risen to 5.2% from 5.1% in March. Consensus : Payrolls – -75,000 versus -80,000 in March, unemployment rate – 5.2% versus 5.1% in March.

5. Other reports : Consumer Confidence (April 29), Employment Cost Index (April 30), and factory orders (May 2).

Markets

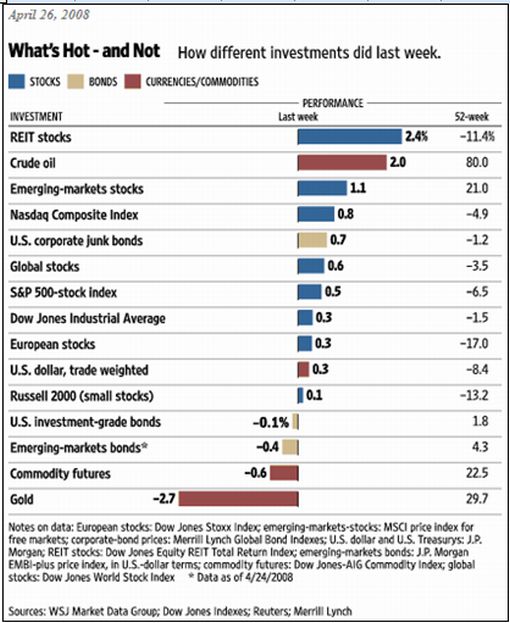

The performance chart obtained from the Wall Street Journal Online shows how different global markets fared during the past week.

Source: Wall Street Journal Online , April 26, 2008.

Equities

Global stock markets added to the previous week's gains but in more modest fashion, with the MSCI World Index closing 0.6% higher on Friday. Japan's Nikkei 225 Average (+2.9%) fared the best among the mature markets, whereas emerging markets (+1.1%) also put in a good performance.

The Chinese market was a highlight as the Shanghai Stock Exchange Composite Index jumped by 15.0% after news of a cut in the share-trading tax. That helped the Hong Kong Hang Seng Index surge by 5.5%, while the South Korea Seoul Composite rose by 3.0%.

As the first-quarter earnings season in the US got into full swing, the strongest stock market index was again the Nasdaq Composite Index with a gain of 0.8%, followed by the S&P 500 Index (+0.5%), the Dow Jones Industrial Index (+0.3%) and the Russell 2000 Index (+0.1%). The Dow Jones Transportation Average is now up 10.6% for the year, which is particularly interesting as the “trannies” are often viewed as a leading indicator of economic activity.

All eyes will be on the S&P 500 Index during the coming week as the Index is just a whisker away from the key 1,400 resistance level. Please let me know how you see this panning out by clicking here to participate in a quick poll on the direction of the stock market.

Fixed-interest instruments

Fading concerns about an economic Armageddon and commensurate less safe-haven buying, together with mounting inflation worries, resulted in investors switching from government bonds to equities, pushing government bond yields sharply higher in most parts of the world.

The yield on the two-year US Treasury Note jumped by 19 basis points to 2.37%, thereby exceeding the Fed funds rate of 2.25% for the first time since June 2006. The 10-year US Treasury Note yield rose by 10 basis points to 3.85% and the 30-year Bond yield to by 5 basis points to 4.57%, resulting in a flattening of the yield curve.

Government bonds elsewhere in the world followed a similar pattern, with Japanese bonds in particular taking a beating as a result of inflation reaching its highest level for a decade.

Bond prices are facing their first monthly decline since June 2007.

US mortgage rates also increased, with the 15-year fixed rate rising by 3 basis points to 5.57% and the 5-year ARM rate increasing by 8 basis points to 5.81%.

Currencies

The past week again saw quite a bit of volatility in the currency markets. On Tuesday the US dollar hit an all-time low against the euro of $1.6018, but then reversed course to close at $1.5618 – its strongest level in a month.

The past week again saw quite a bit of volatility in the currency markets. On Tuesday the US dollar hit an all-time low against the euro of $1.6018, but then reversed course to close at $1.5618 – its strongest level in a month.

The turnaround in the US dollar's fortunes came on the back of a perception that the Fed may be close to halting its recent slew of interest rate cuts, whereas the economic outlook in the Eurozone has deteriorated.

The US dollar strengthened by 1.2% against the euro during the week, 0.7% against the Japanese yen, 1.5% against the Swiss franc and 0.7% against the British pound.

Elsewhere, the Australian dollar rallied to a 24-year high against its US namesake on the back of stronger inflation data.

Commodities

The Dow Jones-AIG Commodity Index (-0.6%) took a breather as the stronger US dollar impacted negatively on some agricultural commodities, industrial metals and precious metals.

The West Texas Intermediate oil price (+2.1%) came to within touching distance of $120 a barrel on news of strikes in Scotland and Nigeria, another pipeline attack in Nigeria, and a report on Friday that there had been a skirmish in the Persian Gulf between a US cargo ship and Iranian fast boats.

The rebound in the US dollar caused further profit-taking in the precious metals complex, with gold losing 2.8%, platinum 5.0% and silver 4.8%.

Rice again traded at record levels, reaching prices in excess of $1,000 a ton.

Now for a few news items and some words and graphs from the investment wise that will hopefully assist in making sense of a week that is filled to the brim with important happenings that include earnings reports from over 100 S&P 500 members, an FOMC meeting and a batch of influential economic data.

Source: Slate , April 2008.

Moody's Economy.com: Global business confidence at record low

“Global business confidence fell to a record low in mid-April. Businesses' assessments of current business conditions are bleak as are their views on the strength of sales. Equipment investment is holding up much better, but it too has weakened notably in recent weeks. Hiring intentions in April are consistent with another month of job losses. Financial services firms are glum. The only good news in the report is tentative indications that the inventory drawdown is abating. Asian confidence is also holding in better.”

Source: Moody's Economy.com , April 21, 2008.

CNBC: Wilbur Ross's world tour

Fresh from his around-the-world tour, Wilbur Ross grants CNBC's Maria Bartiromo an exclusive interview.

Source: CNBC , April 25, 2008.

CNBC: Where's the economy going? Nobel winners weigh in

“CNBC's ‘Squawk Box' hosted a meeting of the minds this morning: Past Nobel Prize winners shared their insight on the future of the markets.”

Nobel thoughts

“‘The real important point from an economic perspective is the gap between the economy's potential growth and its actual growth. And without a doubt, there's a big gap. I think we're probably in a recession. The real concern is how long, how deep. This is one of the worst – clearly going to be the worst … downturns since the Great Depression.'

Joseph Stiglitz, 2001 Nobel Prize winner and Columbia University professor

Nobel optimism

“‘I think that we've got a lot of strength that's going to come out of the export sector, the technology sector. We've seen good earnings reports from some of them. They're thriving on this weak dollar. It's giving them a chance to sell goods all over the world. And I think that's going to probably pull us out.'

Robert Engle, Nobel Laureate Economist winner 2003 and New York University professor

“‘The rise of the unemployment rate has been mild, and it started from a very, very low level of 4.3 just ten or twelve months ago. By that metric, this is a mild downturn.'

Edmund Phelps, Nobel Prize winner in economics 2006

Nobel innovation

“‘I think that we should be thinking forward to creating new mortgage institutions that are relatively immune from this moral hazard and that shelter people from it – what I'm talking about is what I'm now calling a continuous workout mortgage. These would be mortgages privately issued so that the cost would be priced into the rate. And they would be mortgages that are flexible in the sense that the payout scheme responds to changing economic conditions and changing ability to pay.'

Robert Shiller, Yale University professor of economics

Source: CNBC , April 25, 2008.

CNBC: Nobel prize-winning e-mails

Answering viewer e-mails with Robert Hormats, Goldman Sachs International, Joseph Stiglitz, Nobel Prize Winner 2001 and Columbia University professor, and Edmund Phelps, 2006 Nobel Prize winner in economics.

Source: CNBC , April 25, 2008.

GaveKal: Statistics show US economy is in recession

Source: GaveKal – Checking the Boxes , April 21, 2008.

Steven Keen (Oz Debtwatch): Debt levels could jeopardize demand constraint

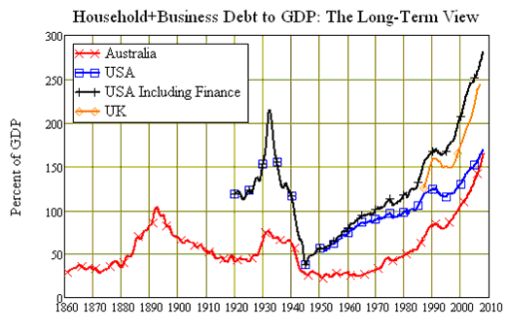

“Fragility is indicated by the proportion of GDP needed to service debt; the higher this proportion is, the less there is available to both consume and invest. Economists habitually excuse any private borrowing on the assumption that it will lead to increased output, and thus finance itself. But 90% of the debt incurred in the past three decades has financed speculation rather than investment. Productive capacity has risen far less than debt, so that the debt ratio has grown exponentially.

“All major OECD nations (except France) have experienced rising private debt to GDP ratios over the past three decades. Australia's debt ratio rose 4.2% faster than GDP for the past 44 years – taking the country's ratio from 24% in 1964 (and 43% in 1977) to 165% now. The UK's private non-financial debt ratio was 96% in 1977, versus 243% now; the USA's was 93% excluding finance, and 108% including, in 1977; today it is 170% excluding finance, and 282% including.

“These levels are unprecedented. The US private non-financial debt to GDP ratio was 150% in 1929 – 20% below today's level (it peaked at 215% in 1932, due to Great Depression deflation of 10% p.a., and falling output of 13% p.a.

“Recoveries from other financial crises in the post-WWII period have worked because they have reignited the growth in private borrowing. I doubt that there is any further capacity to do this: there are no sub-subprime borrowers to whom to lend. The growth in debt levels and asset prices will reverse, and the change in private debt will therefore subtract from demand rather than augmenting it.”

Source: Steven Keen's Oz Debtwatch , April 15, 2008.

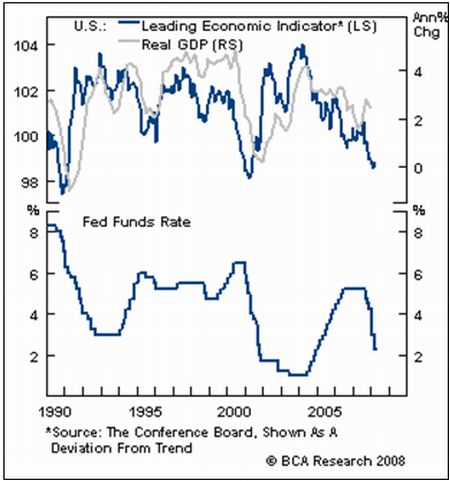

BCA Research: US Leading Economic Indicator – economic mush, at best

“The Conference Board's Leading Economic Indicator (LEI) showed a small uptick in March.

“It was slightly positive news that the LEI did not continue to erode, but the index is still well below its boom/bust line (based on a deviation from trend), which implies a weak economy for another six months. Further interest rate cuts, and possibly more non-conventional tactics, are probable, especially because credit sector problems have not been resolved. Interbank spreads have failed to narrow and mortgage rates remain stubbornly high.

“Bottom line: A sustained breakout in risk assets (i.e. a rising stock/government bond ratio and decisive narrowing in corporate bond spreads) awaits a solid rebound in the LEI.”

Source: BCA Research , April 21, 2008.

James Quinn (Telegraph): Citigroup's CFO says consumer credit now biggest risk

“Banking giant Citigroup has warned that defaults on credit cards and other consumer products could drag on the economy for the next two years.

“Gary Crittenden, chief financial officer of the financial conglomerate, believes that it is consumer credit – rather than institutional credit – which now poses the greatest risk to the banking sector, and therefore the economy at large.

“To date, the bulk of the losses besieging the banking sector have stemmed from corporate and leveraged loans and complex credit products between banks and other institutions.

“However, in the last few months, there has been growing evidence that serious problems now exist in the consumer credit market with defaults on personal loans, credit cards and car loans on the rise.”

Source: James Quinn, Telegraph , April 21, 2008.

John Authers (Financial Times): Why do so many believe that US economy will make a swift recovery?

“In the US, no indicators are yet flashing anything more than a light recession. If employment keeps falling, that could change. But the bulls' argument is that the US is getting such a jolt of stimulus – from tax rebates, base rate cuts and the weak dollar – that it can scarcely help recovering.

“The arguments against are clear: the credit squeeze has yet to hit Main Street, while the ‘wealth effects' from lower house prices and higher food and fuel prices will kill off the consumer.

“Traders hope the economy can make a ‘V-shaped' recovery. If it does, shares will go far higher. If it is only a ‘U', or even the dreaded ‘L' shape, then watch out.”

Source: John Authers, Financial Times , April 18, 2008.

Greg Ip (Wall Street Journal): Fed rate cuts expected to continue

Source: Greg Ip, Wall Street Journal , April, 2008.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.