Most Hated Stocks Bull Market!

Stock-Markets / Stock Markets 2014 Jul 11, 2014 - 11:04 AM GMTBy: Puru_Saxena

BIG PICTURE - The ongoing bull market is over 5 years old and both the Dow Jones Industrial Average and the S&P500 Index have climbed to record highs. Yet, the vast majority of retail investors are still not convinced and many are waiting for the elusive stock market crash!

BIG PICTURE - The ongoing bull market is over 5 years old and both the Dow Jones Industrial Average and the S&P500 Index have climbed to record highs. Yet, the vast majority of retail investors are still not convinced and many are waiting for the elusive stock market crash!

Despite the fact that this primary uptrend has tacked on impressive gains, it remains one of the most hated bull markets in recorded history. If you follow the mainstream financial print media, you may have seen that many prominent publications have recently called this stock market a 'bubble'! In fact, the very same magazines have doubted the durability of this bull market since its very inception.

In our view, such bearish 'bubble' sentiment is precisely the reason why we are nowhere near the end of this bull market. With all due respect, financial magazines have an awful track record of market timing and their forecasts are better served as contrary indicators. After all, such publications pronounced the 'death of equities' in 1979, the 'new era' in 2000 and "why we love housing" in 2005!

Bearish sentiment aside, the truth is that this is one of the most powerful bull markets ever and in our opinion, the party is likely to continue for at least another 2-3 years. Undoubtedly, this primary uptrend has been powered by the Federal Reserve's unprecedented monetary policy and it is conceivable that the bull run may continue until the inversion of the yield curve.

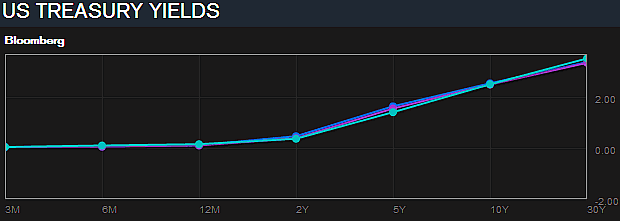

Today, central banks are accommodative throughout the developed world and as Figure 1 confirms, the US yield curve is steep (long term rates are higher than short term rates). Furthermore, it is notable that over the past several decades, prolonged bear markets in stocks have always been preceded by the inversion of the yield curve.

Figure 1: US Yield Curve is steep

Source: Bloomberg

So, unless this time is different, it is probable that the ongoing bull market in common stocks will also end after the inversion of the yield curve; which will be followed by the next economic recession.

If our assessment is correct, the yield curve will not invert for at least another 2-3 years and this implies that stocks should continue to appreciate over this time frame. Although we do not possess a crystal ball, we suspect that at the very earliest, the Federal Reserve will start raising the Fed Funds Rate by next summer. Thereafter, the Fed Funds Rate will probably be increased in baby steps (25bps) and the rate hiking cycle could continue for 2-3 years. Under this scenario, stocks may continue to rally until mid-2017, so we recommend full exposure to equities.

In addition to the monetary backdrop, the various technical indicators we follow also remain supportive of this bull market. For instance, the NYSE Advance/Decline Line has now climbed to a record high, approximately 76% of the NYSE stocks are trading above the 200-day moving average and the number of 52-week highs is significantly greater than the number of 52-week lows.

More importantly, after a brief pullback to the 200-day moving average, the (technology-heavy) NASDAQ Composite has now climbed to a multi-year high (Figure 2). Joining the bull parade is the Russell 2000 Growth Index, which has also completed its multi-week pullback and is now trending in the right direction.

Figure 2: NASDAQ Composite (daily chart)

Source: www.stockcharts.com

Bulls should take comfort from the fact that the growth stocks and technology counters are now participating in this stock market rally and over the past few weeks, they have outperformed the broad market. The favourable price action in these 'risky' stocks suggests that we are amidst a healthy stock market environment.

In terms of specific sectors, we see strength in banks, consumer staples, energy, healthcare, industrials, technology and transportation stocks. Accordingly, we have concentrated our equity and fund portfolios in these areas.

Since we are now in a mature bull market, over the following months, we suspect that energy (upstream, integrated and pipelines), industrials and transportation stocks will probably outperform the broad market. Therefore, we recommend reasonable exposure to these sectors of the economy.

Elsewhere, it is notable that the semiconductor sector has only recently broken out of a massive multi-year trading range; therefore, new buying can be done in these securities.

Last but not least, we believe that the farm equipment and heavy construction stocks are getting ready for a large advance, so some of the prominent names in this industry group may be worthy of your investment dollars.

As far as geographical exposure is concerned, we like the developed world (Europe, Japan and the US) and believe that it will continue to fare better than the emerging nations. In fact, you will recall that we first turned bullish on the developed nations almost 2½ years ago and since then, the 'old world' has done very well.

Going forward, we suspect that some of the beaten-down European nations will provide outsized returns and even Japan may surprise to the upside.

If you review Figure 3, you will note that during this lengthy consolidation phase, the Tokyo Nikkei Average has climbed back above the key moving averages and the stage may now be set for a tradable advance. Remember, Japan's policymakers are doing everything to revive the economy and if they succeed in devaluing the Yen further, the stock market will probably embark on an explosive rally.

Figure 3: Tokyo Nikkei Average (daily chart)

Source: www.stockcharts.com

Over in Asia, although the vast majority of the stock markets are caught in a trading range, there are a couple of interesting opportunities.

First and foremost, after a 6-year trading range, India's stock market has only recently broken out of its consolidation pattern and it is probable that this uptrend will now continue for several months. Accordingly, we have allocated some capital to this area.

Secondly, Taiwan's stock market is showing signs of strength and a close above the 2007-high will be extremely bullish. For now, we are watching the developments from the sidelines but if the old highs are taken out, we may allocate some capital.

In summary, despite what you may hear on the mainstream financial media, the bull market is alive and healthy. Furthermore, bearing in mind the monetary backdrop, common stocks in our preferred areas should continue to do well for another 2-3 years.

Accordingly, our equity and fund portfolios are currently fully invested in our preferred investment themes and as long as the primary uptrend is intact, we will stay the course. However, when the monetary backdrop changes and the primary trend reverses, we will try to liquidate our holdings and defend capital.

COMMODITIES - There can be no doubt that the commodities boom ended in April 2011 and we are now in a secular downtrend (bear market).

You will recall that the commodities boom during the last decade was primarily due to two factors - US Dollar depreciation and China's insatiable demand.

Between 2001 and 2008, the US Dollar declined relentlessly and since commodities are priced in greenbacks, their values automatically appreciated. Furthermore, between 2003 and 2008, the world experienced its first truly global boom which caused the demand for commodities to surge; at a time when supply was relatively tight! Thereafter, during the global financial crisis, the demand for commodities temporarily plunged; thereby triggering a panic sell-off in the sector.

In response to the global financial crisis, the Chinese authorities unleashed a massive stimulus program and this debt-fueled infrastructure boom caused the prices of commodities to soar for another 2 years. Eventually, the Reuters-CRB (CCI) Index topped out in April 2011 and since then, it has been drifting lower.

If you review Figure 4, you will observe that ever since topping out in 2011, the CCI has been in a downtrend and each subsequent rally attempt has failed beneath the previous high (blue arrows). Such price action is typical of a primary downtrend; whereby the path of least resistance is down.

Figure 4: Reuters-CRB Index (weekly chart)

Source: www.stockcharts.com

Currently, the CCI is trading just above the 40-week moving average and it will be interesting to see whether it will hold above this key level. If the CCI can stay above this moving average and then take out its recent high, it will open up the possibility of additional gains.

Until then, the path of least resistance is down and traders should either be short or out of this sector.

Looking at specific items, it is noteworthy that the price of copper has firmed over the past 3 months and it is currently trading above the key moving averages. Unquestionably, copper has been buoyed by China's better than expected manufacturing data and a favourable survey of Japan's business sentiment. In any event, as long as copper continues to trade above the 200-day moving average, one can consider participating in the festivities.

Over in the energy patch, it is worth noting that the price of crude has rallied since the beginning of this year and the next target is last year's high. Remember, the energy sector tends to do well in a late stage recovery, so it is likely that the price of oil will appreciate further.

In any event, the energy stocks are performing well and we continue to recommend exposure to the upstream firms, integrated companies and pipeline stocks. If our analysis is even vaguely correct, these securities should do well over the following months.

Puru Saxena publishes Money Matters, a monthly economic report, which highlights extraordinary investment opportunities in all major markets. In addition to the monthly report, subscribers also receive “Weekly Updates” covering the recent market action. Money Matters is available by subscription from www.purusaxena.com.

Puru Saxena

Website – www.purusaxena.com

Puru Saxena is the founder of Puru Saxena Wealth Management, his Hong Kong based firm which manages investment portfolios for individuals and corporate clients. He is a highly showcased investment manager and a regular guest on CNN, BBC World, CNBC, Bloomberg, NDTV and various radio programs.

Copyright © 2005-2014 Puru Saxena Limited. All rights reserved.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.