The Fed at Interest Rate Crossroads Between Inflation and Economic Growth

Economics / US Economy May 18, 2008 - 03:30 PM GMTBy: John_Mauldin

Retail Sales Take a Dive

Retail Sales Take a Dive - Accounting for Inflation

- The Fed at the Crossroads

- Sell in May and Go Away

Is the economy poised for a recovery, as the stock market seems to expect? Or are we in for another few more quarters of recession and/or slow growth? In this week's letter we take a look at consumer spending, inflation, and other data to see if we can find a clue or two to give us an idea of the direction of the economy. There is a lot of data, so let's jump right in.

Retail Sales Take a Dive

Many commentators, looking for a bullish lifeline, have pointed to the fact that retail sales grew in April by 1.8% over this time last year. But that is truly grasping at straws. Just last November they were growing at 6% year over year and have been dropping relentlessly for the last six months. And as good friend and data maven Greg Weldon points out, retail sales last November were 1.3% over inflation and now are a negative 2.1% below inflation. Retail sales are clearly headed down. ( www.weldononline.com , a must-read for those who need in-depth analysis of all things and data economic)

But there was growth. Gasoline sales were up 16.3%. And food sales were up 6.1%. 77% of the increase in retail sales this year has been from increases in food and gas sales. If you take out food and gas, retail sales are down by about 2% in the last three months.

The consumer is getting squeezed. Reuters did a rather anecdotal, but revealing survey of Wal-Mart buyers at the beginning of the month. They found a significant increase in store traffic from the end of the month to the first of the month. Surveys showed that shoppers were stretched on their budgets due to rising gas and food costs and simply had to wait until their monthly checks came to go to the store for food. Many indicated they had changed their buying habits, now shopping at lower-cost stores like Wal-Mart.

At the Mauldin household I must admit to a kind of food shock upon my return. I eat a lot of smoked turkey from a local grocery deli. Arriving back from South Africa last night, I sent my oldest son to the store to put in a supply for the next few days. My "regular" turkey that was about $5.99 a pound a few months ago is now selling for $8.99. That is considerably higher than the 5.9% food-at-home inflation rate that the folks who give us the CPI tell us is the case. Next time I will find a less expensive brand, as the Reuters survey suggest shoppers all across the country are doing.

(I do recognize the inconsistency of saving a few dollars at home while I eat out at nice restaurants where the price increases are even greater. It is all about what is in your head. There are books and massive studies devoted to such behavior.)

"Leslie Dach, executive vice president of corporate affairs and government relations at Wal-Mart, said the cycle of shoppers running out of money in between paychecks and then flocking to its stores on payday is 'more pronounced, more visible.'

While many U.S. retailers are facing waning sales as shoppers cut back on purchases of clothes, jewelry or home furnishings, Wal-Mart's vast grocery business and its emphasis on low prices is spurring a resurgence at its U.S. stores and in its stock price." (Reuters)

But prices are actually up at Wal-Mart. And not just from food. Looking at the latest Commerce Department data, we find that US import prices are up 15% year over year. Even taking out gasoline, prices are up 6.2%. And it is somewhat surprising that it is only 6.2%. Why?

Because the dollar has fallen by more than 6%. The Chinese ambassador to the US, Mr. Zhou Wenzhong, recently pointed out that the Chinese renminbi has appreciated almost 19% since July of 2005. I have been writing for years that the Chinese would allow their currency to appreciate slowly and steadily for their own purposes and on their own schedule. They need to do so in order to contain their own rising inflation. Look for it to rise another 10% by the middle of next year.

Consider that because of the rise of the renminbi, the prices for oil and food imports in China have risen 20% less than for US consumers. And the prices they charge us for their goods are only about 4% higher. But that meager growth is up from only 1% last fall. Those (notably economics-challenged Senators Schumer and Graham) who have been pressing for China to allow its currency to rise are going to find that such a rise ultimately means higher prices for US consumers. Be careful what you wish for, Senators. You just might get it.

Lower consumer spending is not just due to gas and food. There is also a psychological component. Frederic Mishkin, one of Ben Bernanke's colleagues at the Fed, has done research that suggests the "typical American family will cut its spending by up to 7 cents for every dollar in housing wealth it loses. Given a 20% fall in prices, this adds up to a nationwide reduction in consumer spending of about $350 billion a year, or 2.5% of the U.S.'s gross domestic product. That's a big number - more than enough to tip the economy into recession." (Conde Nast)

And that's if the fall in prices is only 20%. I continue to put forth the proposition that we are going to see a slow Muddle Through Recovery, as the boost we got from Mortgage Equity Withdrawals during the last recession will not be available this time.

Accounting for Inflation

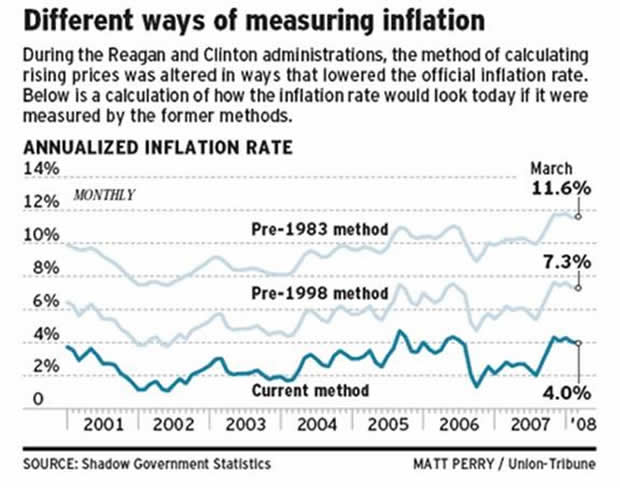

If beauty is in the eye of the beholder, inflation is in the eye of the statistician. Because the number you end up with is dependent on the models and assumptions you choose. As the chart below shows, there have been two major revisions to how inflation is figured, one in 1983 and another in 1998. (Thanks to Barry Ritholtz at The Big Picture for this source.)

Note that using the same methodology as was used in 1983, inflation would be around 11.6% today. Before 1983, the BLS used actual home prices to account for inflation. After that time, they used something called Owners Equivalent Rent or OER. This is the theoretical price a home would rent for. There are sound reasons to use OER and equally good reasons to use actual home prices (as is done in Europe). But both methods have flaws. You just have to pick a methodology and stick with it.

And there are reasons to think that OER may not rise as it would normally do in this part of the cycle, because so many homes which cannot sell are being rented out, and rent prices might not rise as much as in past cycles.

Using actual home prices is only useful in an average sense over long periods of time. If you own a home with a 30-year mortgage you bought ten years ago, then you have not experienced price inflation for ten years. You have seen the value of your home go up, but that is not (necessarily) inflation. Your mortgage is the same. And a first-time buyer today has the potential to see a 30-50% deflation in home prices from a year ago if he is in the right area, like Florida or California.

Further, the OER tries to measure what a house would rent for. If someone pays more than that rental price, then there is some other factor at work. The Bureau of Labor Statistics suggests that this other factor is investment. If someone pays more for a house than the equivalent rental price because it is perceived as a good investment, then you are measuring apples and oranges. The OER tries to take out the investment angle.

Because the government agencies use OER, inflation was understated in the recent housing bubble. As home prices drop, OER would normally overstate inflation somewhat. If we had used actual home prices then inflation would have been overstated in the last six years, and now the CPI would be turning negative, even as gas and food are rising dramatically.

As I said, neither method is perfect. Over very long periods of time, either will give you reasonably accurate data. But over a time period as short as a few years, let alone a few months, there can be considerable "noise."

Also, notice in the chart that in 1998 the Clinton administration adopted new methodologies, among them hedonic pricing. Hedonic pricing suggests that as a product or service improves, the price for the equivalent item in today's market will fall. As an example, if we buy a computer that is twice as powerful as it was a few years ago, the statisticians assume that prices have fallen even if we pay the same for the computer.

In the same way, if in one year you had to pay extra for features like power steering or power windows in a car, and a few years later they were considered standard, then once again the price would be deemed to have gone down, as you were getting more "value" for your dollar. This is considered to be the case even if in actual dollars you paid more for the car.

Again, you can make a rational and serious economic argument for hedonic pricing. And believe me, many economists do. But those changes, along with others, have lowered the official rate of inflation. And since many government benefits are also tied to the official rate of inflation, the current methodology has lowered government expenses as well, including inflation adjustments for Social Security and pensions.

At one time, you could make a good case that the inflation numbers overstated inflation. But I am not persuaded that is the case anymore, even though many economists still argue that point. The CPI is more or less accurate ON THE AVERAGE. But that may not be the case for you. Your actual rise (or fall) in the level of your expenses may be more or less than the average.

But we do notice the increases more. The Bank Credit Analyst has a very interesting chart in its recent May issue. It shows that the high-frequency spending items like gasoline, food, education, and medical care make up 50% of the Consumer Price Index. These are items which we buy on a regular basis. And they are going up at a weighted average rate of 6.8%, a lot higher than the 4% for the CPI as a whole.

The 20% of the CPI which are low-frequency items like furniture, appliances, vehicles, and so on are actually falling at a -0.7% rate. Since OER (equivalent rent) is roughly 30% of CPI and is rising at 2.8%, even as home prices fall the overall rate is about 4%.

Our tendency to notice the price increases in more frequently purchased items more than the drop in less frequent expenditures is known as salience. What we see every day is more visible to us and is on our minds. And because the reality is that those prices are rising much faster than headline inflation, we tend to think inflation is understated.

I can look at my credit card bills and know that my restaurant bill is rising at much more than 4% a year. I do not think I am eating all that much better, and am actually eating less food in an attempt to hold down my weight. My travel expenses are up by more than the 5-7% in the BLS numbers. Those prices, and the price of turkey, are in my face constantly.

The Fed at the Crossroads

"I went down to the crossroads, fell down on my knees.

"Asked the Lord above for mercy, 'Save me if you please.'" - Robert Johnson

Legendary blues singer Robert Johnson was said to have sold his soul to the devil at the crossroads outside Rosedale, Mississippi, to be the best blues singer ever.

The Fed is also at a crossroads. What's the price for low inflation and a booming economy? Can you have both in today's environment without a deal with the devil? And can even Old Slewfoot deliver on such a dream?

Inflation is uncomfortably high at 4%. Even core inflation is well above the 1-2% comfort zone. But the economy is soft and getting softer. Even with the stimulus package kicking in this quarter, consumer spending is likely to be weak. There are some at the Fed who would like to raise rates as soon as possible to deal with inflation, but the economy is not cooperating. The housing crisis just keeps getting worse, and the credit crisis is causing banks to tighten lending standards on every manner of credit, even with Fed fund rates low. LIBOR and other credit costs and spreads are not dropping as one might have thought they would in response to low Fed fund rates. Tax receipts are slowing well below projections, especially sales tax receipts.

Let's look at some of the pressures on the economy. According to the National Small Business Association, more than 5,000 firms filed for bankruptcy in April 2008, the most in any month since new bankruptcy laws took effect in 2005. The data also show that in the first quarter of 2008 13,155 businesses filed for bankruptcy, an increase of nearly 45% from the 9,103 business bankruptcy filings during the same period in 2007.

Economists suggest that the leap in bankruptcy filings is a result of the troubles that started with subprime mortgages and other financial instruments of Wall Street, which are now trickling down to Main Street. The ensuing credit crunch, skyrocketing commodity prices, and dormant consumer sales are likely culprits for pushing many more businesses to the brink of bankruptcy throughout 2008.

The debt of 174 large US companies is trading at distressed levels, at well over 10% above comparable treasuries. Diane Vazza, S&P's credit chief, says defaults are rising at almost twice the rate of past downturns.

"US and European banks and financial institutions have 'enormous losses' from bad loans they haven't yet recognized and may have a harder time wooing sovereign-fund rescuers, Carlyle Group Chairman David Rubenstein said.

"'Based on information I see,' it will take at least a year before all losses are realized, and some financial institutions may fail, Rubenstein said... He didn't name any companies." (Bloomberg)

JPMorgan Chase & Co.'s chief executive said Monday that while the crisis in the credit markets appears to be three-quarters over, he believes a US recession is just beginning.

"'Even if the capital markets crisis resolves, it does not mean that this country will not go into a bad recession,' said CEO James Dimon, whose bank saw its first-quarter profit fall by half due to the recent collapse of the US mortgage market. 'The recession just started."

Raising interest rates in this type of environment would be very difficult. Seemingly everyone now reveres Paul Volker. But many forget, as Charles Gave points out, that he put the country through two severe recessions, bankrupting many Latin

American countries because of the high interest rates on the loans they had made in US dollars at much lower initial rates (shades of 'teaser rates'), which resulted in the technical bankruptcy of every major US bank. Those were not pleasant times, especially in Latin America. Be careful what you wish for.

If Ben Bernanke and the Fed governors decided to pull a Volker and raise rates in order to combat 4% inflation, there would be lynch mobs forming.

And it is not clear that inflation would respond to rising rates without a severe slowdown and an even worse recession. Oil prices would not respond to interest rates. Inflation, as Friedman tells us, is always and everywhere a function of money supply, and the money supply is not growing at anywhere near the rates of the 1970s. Oil is a function of supply and demand, spurred on by speculation. You can deliberately slow demand by tanking the economy, but are lower gas prices worth an 8% unemployment rate?

Likewise with food. Food price increases are due more to government policy (as in ethanol and subsidies) and increased demand for higher-quality foods, especially protein, from developing nations. I have yet to see a persuasive argument that food prices would respond to higher interest rates by courteously going lower. Unless, of course, you put the world economy into a severe recession. That would reduce demand for higher-quality foods. Again, not a wise policy.

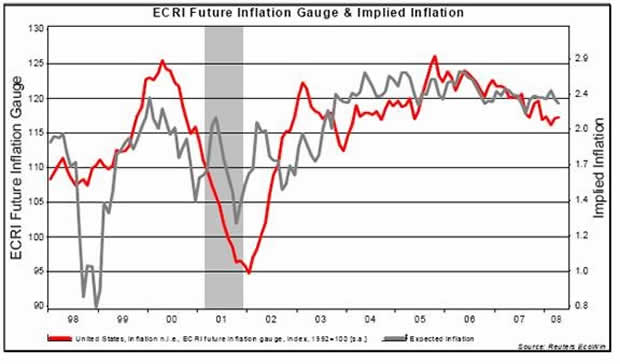

Given that, the markets seem to be telling us that inflation in the future will not be the problem that the headlines suggest it is today. Let's look at this note and chart from Charles Gave of GaveKal ( www.gavekal.com ):

"The next question is the behavior of prices in the future. And to gage this, I will review two tools: one is the ECRI future inflation gauge of the University of Columbia,

and the other is the expected inflation for the next ten years as derived from the differences between a classical bond and an inflation indexed bond.

[Note: the red line is the ECRI gauge (left scale) and the grey is the expected inflation measure (right scale).]

"The least that can be said is that neither the forecasting tool of the Columbia University (which peaked at the beginning of 2006), nor the expected inflation are showing any signs of panic. We certainly do not see any significant rise in any of these two tools similar to the ones we saw from 1998 to 2000 or from 2002 to 2006. So maybe, just maybe, what we are seeing today is a change in relative prices (food and energy higher, housing lower) and not a general rise in the inflation rate."

I would not be surprised at all to find that inflation is not the problem it is today, by this time next year. In fact, given that we are seeing two bubbles burst and a recession and slow recovery, all of which are by definition deflationary, it would be odd if inflation got worse from here. Stranger things have happened, but the odds favor a view that inflation pressures will ease.

Bottom line? I think the Fed will be on hold for a rather long time. We are in a Muddle Through Economy. Even if the economy gets worse, as Jamie Dimon predicts, the problems in the economy would not be helped by lower rates. And until the economy starts growing at a rate above 2%, it will be difficult to justify raising rates in the face of such slow growth. And given the pressure on consumer spending and housing prices, I think the recovery that should begin later this year is going to be a rather tepid one.

Sell In May and Go Away

Numerous studies show that since World War II, as much as 99% of stock market returns have been generated between November 1 and May 1. Good friend and fishing buddy David Kotok of Cumberland Advisors sums it up nicely:

"According to the Ned Davis (NDR) database, starting in 1950, $10,000 invested in the S&P 500 Index every May 1st and then liquidated every October 31st would only be worth $10,026 today. That's right: had you stayed out of the stock market from November through April and only been in the market from May through October, you would have had no change during the last 57 years. 21 of those years would have been negative; 36 were positive. This happened during the same period that stock prices were rising about 75% of the time and markets made extended upward moves.

"Consider the results of the reverse strategy. Buy the S&P 500 Index on November 1st and sell all your stocks on May 1st. The outcome is dramatically different. Your original $10,000 would now be worth $372,890 as of April 30th closing prices in 2008. Out of the 58 periods you would have had positive results in 45 of them and negative results in only 13 years."

David goes on to show research at www.cumber.com as to why he thinks you should hold off on selling. I disagree, but then the stock market has been confirming David's position. My thought is that the Continuing Crisis will put pressure on corporate earnings throughout the summer, with more earnings disappointments at the end of this quarter.

Earnings disappointments are the stuff of bear markets. Richard Russell, one of the more astute market observers and in the past a serious bear, thinks we are now in a bull market. Dennis Gartman is now a bull. How do you argue with such astute traders?

I am sure Larry Kudlow will argue that the markets are telling us a recovery is imminent because the markets are rising. Nevertheless, I think this could be a very rocky summer for the markets in general. I look back to 2001-02 and find three bear market rallies of 20%. The market evidently did not know as much as it thought. But then, what do I know? If you have specific stocks you like, or are a trader, then that is fine. But for those whose only real equity choice in the retirement plan of investment in a long-only index, I would find one of the other options in bonds

South Africa, Flowers, and On the Road

South Africa was wonderful. I so enjoy the country and the people. The game runs were excellent at Sun City, as was the resort. I highly recommend it. And thanks to Prieur du Plessis and Paul Stewart at Plexus for being such great hosts.

And now I must tell a story about assumptions, and how they can rise up and bite you. It seems I left a bag on the American Airlines flight which I took to connect with South African Airways at Dulles in Washington, DC. It had my shoes, belt, and ties in it. So, I got to Johannesburg without the basics. On Monday morning I rushed to the local mall, walked into a well-known men's clothing store, and bought a belt and ties, paying for them with my personal Citibank credit card. I did not like the shoes in that store and went to another one and chose a nice Italian pair, as there were no other options and time was running short. I tried to use the same credit card, but it was turned down this time. I then used my Citibank business card, and promptly forgot to call Citibank to see what the problem was.

The next Sunday, at a gift shop at the Cape of Good Hope, my business credit card was turned down. I pulled out my emergency-use-only, don't-leave-home-without-it American Express card (I don't get miles from them I can use). I then called Citibank, and they said they just wanted to make sure I had the card in my possession and was using it. They then reactivated it. I asked them to do the same for my personal card.

They looked up the number and then said I needed to talk to the fraud department. I was then asked if I had charged a rather large sum of money for flowers. I informed Citibank that I had not. They said the store was trying to run the charge every day. We both assumed that someone at the first men's store had stolen my number and was using the card to run a scam, buying flowers that they could sell on the local street for cash. I was glad that Citibank was on top of things. When I got back in the office today, my new personal card was waiting.

As I was activating it, I told Tiffani to come in and began to tell her the story, with embellishments, of how I was almost the victim of fraud. Why would anyone think I would spend such a preposterous amount of money on flowers? And I am afraid I used that story in the last of my presentations in South Africa, talking about the need for credit research and liquidity (you would have needed to be there to see the real relevance).

Assumptions.

"Dad," said Tiffani with a Dad-has-done-it-again smile and a don't-tell-me shake of her head, "that was the florist for my wedding, and we have to make a deposit. We couldn't figure out why the card was not going through." I just dropped my head and gave the Dad sigh. I guess I do in fact spend mad sums of money on flowers. And I will enjoy every minute of them. August 8 is just around the corner.

I am off to La Jolla for a quick trip Monday and then back the next day, hoping to get some writing done next week. Look for a very interesting Outside the Box on Monday evening from my friends at Casey Research. They provide some very sobering data on the energy market.

We have not yet found the lost bag at Dulles. While the shoes and books can be replaced, the bag is actually a delegate bag from the 1996 Republican National Convention and has some personal sentimental value. I hope it can be found.

Have a great week. And avoid assumptions.

Your wiping the egg off his face analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.