The Looming Uranium Crisis: Strategic Implications for the Colder War

Commodities / Uranium Nov 14, 2014 - 08:59 PM GMTBy: Marin_Katusa

In the wake of one singular event—the disaster at Fukushima in March 2011, the effects of which are still being felt today across the planet—nuclear power has seemingly fallen into utter disrepute, at least in the popular mind. But this is largely an illusion.

In the wake of one singular event—the disaster at Fukushima in March 2011, the effects of which are still being felt today across the planet—nuclear power has seemingly fallen into utter disrepute, at least in the popular mind. But this is largely an illusion.

It’s true that Japan took all 52 of its nuclear plants offline after Fukushima and sold much of its uranium inventory. South Korea followed with shutdowns of its own. Germany permanently mothballed eight of its 17 reactors and pledged to close the rest by the end of 2022. Austria and Spain have enacted laws to cease construction on new nuclear power stations. Switzerland is phasing them out. A majority of the other European nations is also opposed.

All of this has resulted in a large decrease in demand for uranium, a glut of the fuel on the market, and a per-pound price that fell as low as $28.50 in mid-2014, down nearly 80% from its peak of $135 in 2007. Currently, it’s languishing around $39 per pound, still below the cost of production for many miners—about 80% need prices above $40 to make any return on investment, and even at that level, no new mines will be built. It’s easy to hear a death knell for nuclear energy on the breeze. And that may well be the case for Europe (except for France). But Europe is hardly the world.

South Korean plants are back online. Japan is planning to restart its reactor fleet (despite a great deal of citizen protest) beginning in 2015. Russia is heavily invested, with nine plants under construction and 14 others planned. China, faced with unhealthy levels of air pollution in many of its cities due to coal power generation, is going all in on nuclear. 26 reactors are under construction, and the government has declared a goal of quadrupling present capacity—either in operation or being built—by 2020. India has 20 plants and is adding seven more. And in the rest of the developing nations, nuclear power is exploding.

Worldwide, no fewer than 71 new plants are under construction in more than a dozen countries, with another 163 planned and 329 proposed. Many countries without nuclear power soon will build their first reactors, including Turkey, Kazakhstan, Indonesia, Vietnam, Egypt, Saudi Arabia, and several of the Gulf emirates.

For years, China, with its stunning GDP growth rate, has been seen as the leading destination for natural resources. “Produce what China needs” has been every supplier’s ongoing mantra. Yet, as many Americans fail to realize, it’s their own home that is the biggest uranium consumer. Despite having not opened a new plant since 1977 (though six additional units are scheduled to open by 2020), the US is the world’s #1 producer of nuclear energy, accounting for more than 30% of the global total. France is a distant second at 12%; China, playing catchup, sits at only 6% right now. The 65 American nuclear plants, housing just over 100 reactors, generate 20% of total US electricity.

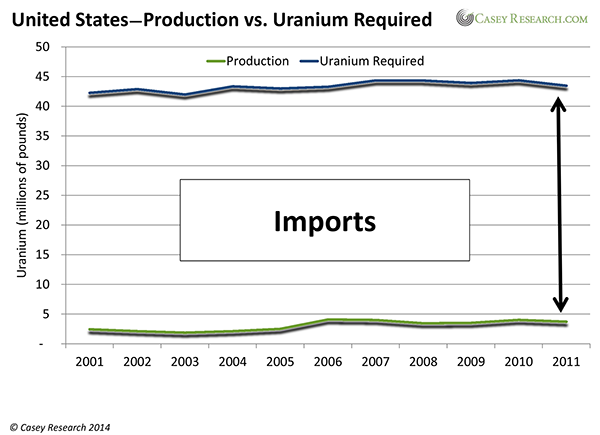

Yet uranium is the one fuel for which there is very little domestic supply.

As you can see, the US has to import over 90% of what it uses. That’s a huge shortfall—and it’s persisted for many years. How has the country made it up?

In a word: Russia.

America’s former Cold War archenemy—and antagonist in the unfolding sequel, the Colder War—has in fact been keeping the US nuclear fires burning, through conduits like the Megatons to Megawatts Program.

When the USSR collapsed, Russia inherited over two million pounds of HEU—highly enriched uranium (the 90% U-235 needed to fashion a bomb)—and vast, underused facilities for handling and fabricating the material. Starting in 1993, it cut a deal with the US dubbed the Megatons to Megawatts Program. Over the 20 years that followed, 1.1 million pounds of Russian weapon-grade uranium, equivalent to about 20,000 nuclear warheads, was downblended to U3O8 and sold to the United States as fuel.

That source was very important in helping to fill the US supply gap for those two decades. It represented, on average, over 20 million pounds of annual uranium supply, or half of what the country consumed. I’m sure it would have come as a shock to most Americans if they’d realized that one in ten of their homes was being powered by former Soviet missiles.

Megatons to Megawatts expired in November 2013, but US dependence on Russia did not. Russia is easily able to maintain its sizeable export presence, due largely to present economics.

Because of all the uranium swamping the market since Fukushima, separative work units (SWUs) are trading at very low prices. SWUs measure the amount of separation work necessary to enrich uranium—in other words, how much work must be done to raise the product’s concentration of U-235 to the 3-5% that most reactors require for fission?

The tails that are left behind when U-235 is separated out to make warheads still contain some amount of the isotope, usually around 0.2% to 0.3%. When the price of SWUs gets low enough, it’s a condition known as “underfeeding,” meaning it’s worth the effort to go back and extract leftover U-235 from the tails. That’s done through the process of re-enrichment, the reverse of the procedure that creates HEU. It’s kind of like getting fresh gold from old ore that had already yielded the easy stuff.

After the Soviet Union broke up, Russia had a lot of enrichment capacity it no longer needed for its military program. And major uranium companies like Areva and Urenco had sent trainloads of enrichment tails to Russia in the 1990s and early 2000s.

Great stockpiles were built up, and they’ll be put to use until the pendulum swings the other way and we get “overfeeding,” where the price of SWUs makes re-enrichment too costly to continue. We will go from under- to overfeeding in the near future. Rising demand from the Japanese restart and new plants coming online ensures that it will happen, and probably within the next 24 months. The market is already anticipating it, with the per-pound price of uranium up more than 35% in the past few months. It’s going to double to $75… at the least.

Meanwhile, though, the ability to profitably produce fuel-grade uranium from tails confers on Russia a number of significant advantages. Among them:

- It permits the country to exploit a previously worthless resource.

- The more tails it can use as feedstock, the fewer it has to dispose of.

- Most important, it means Russia can conserve much of its mineral supply for a future when higher prices will dramatically increase its leverage. That includes in-ground ore, of which it has a lot, and probably uranium picked up on the cheap when Japan did its massive post-Fukushima fuel dump (though it has never been officially confirmed who the buyers of Japan’s uranium supply were, I have some very connected sources who tell me it was the Russians who snapped most of it up).

This is one part of Vladimir Putin’s plan to dominate the world energy markets. In my book, The Colder War, I call it the “Putinization” of uranium. And he has nicely positioned his country to pull it off.

In January 2014, Sergei Kiriyenko, head of Russian energy giant Rosatom, was bursting with enthusiasm when he predicted that Russia’s recent annual production rate of 6.5 million pounds of uranium would triple in 2015.

Rosatom puts Russia’s uranium reserves in the ground at 1.2 billion pounds of yellowcake, which would be the second largest in the world; the company is quite capable of mining 40 million pounds per year by 2020. Add in Russia’s foreign projects in Kazakhstan, Ukraine, Uzbekistan, and Mongolia, and annual production in 2020 jumps to more than 63 million pounds. Include all of Russia’s sphere of influence, and annual production easily could amount to more than 140 million pounds six years from now.

No other country has a uranium mining plan nearly this ambitious. By 2020, Russia itself could be producing a third of all yellowcake. With just its close ally Kazakhstan chipping in another 25%, Russia would have effective control of more than half of world supply.

That’s clout. But it doesn’t end there.

Globally, there are a fair number of facilities for fabricating fuel rods. Not so with conversion plants (uranium oxide to uranium hexafluoride) or enrichment plants (isolating the U-235). And the world leader in conversion and enrichment is… yes, Russia.

All told, Russia has one-third of all uranium conversion capacity. The United States is in second place with 18%. And Russia’s share is projected to rise, assuming Rosatom proceeds with a new conversion plant planned for 2015. Similarly, Russia owns 40% of the world’s enrichment capacity. Planned expansion of the existing facilities will push that share close to 50%.

That’s Putin’s goal—to corner the conversion and enrichment markets—because it wraps Russian hands around the chokepoints in the whole yellowcake-to-electricity progression. It’s a smart strategy, too—control those, and you control the availability and pricing of a product for which demand will be rising for decades.

And that control will tighten, because the barrier to entry for either function is very high. Building new conversion or enrichment facilities is too costly for most countries, and it is especially difficult in the West due to the influence of environmentalists.

It’s worth reiterating. Russia is on track to control 58% of global yellowcake production; currently responsible for a third of yellowcake-to-uranium-hexafluoride conversion; and soon to hold half of all global enrichment capacity.

There’s a word for this: stranglehold.

That is what Putin and Russia will have on the supply chain for nuclear fuel in a world where new atomic power plants are being constructed at warp speed, which will force the price of uranium ever higher. It will give Russia enormous global influence and great leverage in all future dealings with the US

America can mine some uranium domestically and buy some more from its Canadian ally. But even taken together, those sources put only a small patch on the supply gap.

The US government would do well to make peace with Putin, if it can, because the domestic nuclear power industry—and by extension the economic health of the country—is at the mercy of Russia, indefinitely.

To get the full story, click here to order your copy of my new book, The Colder War.

Inside, you’ll discover more on how Putin has cornered the market on Uranium, and how he’s making a big play to control the world's oil and natural gas markets. You’ll also glimpse his endgame and how it will personally affect millions of investors and the lives of nearly every American.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.