How to Find the Best Offshore Banks

Personal_Finance / Current Accounts Jan 28, 2015 - 10:54 AM GMTBy: Casey_Research

By Nick Giambruno

By Nick Giambruno

It’s hard to think of a topic where following the conventional wisdom can be more dangerous.

And that topic is banking.

It’s generally accepted as an absolute truth by the public and most financial experts that putting your money in a domestic bank is a safe and responsible thing to do. After all, if anything were to go wrong, your deposits are insured by the government.

As a result, most people put more thought into which shoes they should purchase than which bank should be entrusted with their life savings.

It’s a classic moral hazard—a situation in which a person is more likely to take risks because the costs won’t be borne by that person. In the case of banking, that’s how a lot of people think, but it isn’t necessarily true that individuals bear no costs of their banking decisions.

The prudent thing to do is ignore the conventional wisdom and look at the facts to form your opinions. Choosing the right custodian for your life savings makes a difference—and it deserves some serious thought.

A False Sense of Security

In the US, the Federal Deposit Insurance Corporation (FDIC) insures bank deposits. In the case of a bank failure, the FDIC pays depositors up to $250,000. The FDIC has a reserve of around $30 billion for this purpose.

Now, $30 billion might sound like a lot of money. But considering that the FDIC insures around $9 trillion in deposits, the $30 billion in reserve amounts to just a drop in the bucket. It’s actually less than half a penny for every dollar it supposedly insures.

In fact, there are over 36 banks in the US that have deposits larger than the FDIC’s reserve. It wouldn’t take much for the FDIC itself to go bust. One large bank failure is all it would take. And with many of the big banks leveraged to the hilt, that isn’t as remote a possibility as many would believe.

Oddly, this doesn’t shake the confidence the public and most financial experts place in the US banking system.

Also, it’s already an established precedent that whenever a government deems it necessary, deposit guarantees can be disregarded on whim. We saw this in the early days of the financial crisis in Cyprus. The Cypriot government initially sought (but was ultimately rebuffed) to dip its hands into bank accounts under the guaranteed amount. Similarly, Spain has imposed a blanket taxation on all bank deposits. I’d bet this is only the beginning. We haven’t even made it through the coming attractions.

Taken together, this shows that the confidence in the banking system—merely because of the existence of a bankrupt government promise—is dangerously misplaced.

Follow conventional wisdom at your own peril.

Fortunately, in this day and age the decision on where to bank doesn’t have to be constrained by geography. Banking outside of your home country—where much sounder governments, banking systems, and banks can be found—is in most ways just as easy as banking with Bank of America.

The Solution

Obtaining a bank account outside of your home country is a key component of any international diversification strategy.

It protects you from capital controls, lightning government seizures, bail-ins, other forms of confiscation, and any number of other dirty tricks a bankrupt government might try.

Offshore banks offer another benefit: they are usually much safer and more conservatively run than banks in your home country… at least if you live in the US and many parts of Europe.

It’s hard to see how you’d be worse off for placing some of your cash where it’s treated best. In the event that your home government does something desperate or your domestic bank makes a losing bet, it could turn out to be a very prudent move.

When Doug Casey and I were in Cyprus, we met with a number of astute Cypriots who saw the writing on the wall. They got their money outside of the country before the bail-in and capital controls, and they were spared. It would be wise to learn from their example.

But you shouldn’t just blindly move your savings to any foreign bank. You want to consider only the best.

For me, being able to find the safest and best offshore banks comes naturally. In the past, I worked as a banking analyst for an investment bank in Beirut, Lebanon. While there, I rigorously assessed countless banks around the world. This experience and the analytical tools I developed have been very helpful in evaluating the best offshore banks worthy of holding deposits.

A basic rundown (but not inclusive) of factors I look for when analyzing an offshore bank include:

- The economic fundamentals and political risk of the jurisdictions the bank operates in.

- The quality of the bank’s assets—namely its loan book and investments. This helps you determine what the bank is doing with your money. I look for banks that are conservatively run and don’t gamble with your deposits. Banks that make leveraged bets with things like mortgage-backed securities or Greek government bonds are obviously to be avoided. Having a sound loan book with a low nonperforming ratio is crucial.

- Liquidity—a relatively safer bank will keep more cash on hand rather than invest it in risky assets or loan it out, all else equal. That way it can meet customer withdrawals without having to potentially sell off assets for a loss—which could affect its ability to give you back your deposits.

- Capitalization—this is a measure of its financial strength of the bank. It also shows you if the bank is using excessive leverage, which can increase the risk of insolvency. A bank’s capitalization is like its margin of error: the higher the better.

Another important factor is whether an offshore bank has a presence in your home jurisdiction. To obtain more political diversification benefits, it’s better that it does not.

For example, assume you are a Chinese citizen and want to diversify. It wouldn’t make much sense to open an account with the New York City branch of the Bank of China. It would be much better from a diversification standpoint for the Chinese citizen to open an account with a sound regional or local bank that doesn’t have a presence or connection to mainland China—and thus cannot have its arm easily twisted by the Chinese government.

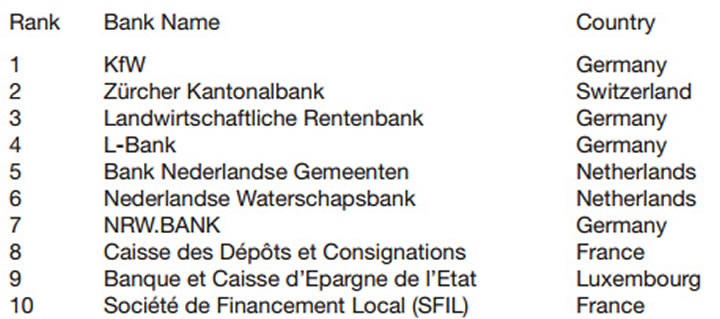

The Best Offshore Banks

Each year, a prominent financial magazine publishes a study on the world’s safest banks. Below are its top 10 safest banks in the world (notice that none of them is in the US).

Naturally, things can change quickly though. New options emerge, while others disappear. This is why it’s so important to have the most up-to-date and accurate information possible. That’s where International Man comes in. Be sure to get the free IM Communiqué to keep up with the latest on the best offshore banking options.

Now, as an American citizen, it’s very unlikely that you could just show up to one of these banks and open an account as a nonresident of that country. That is, unless you plan on making a seven-figure or high six-figure deposit. Then you might have a chance, but even then it’s not guaranteed.

This dynamic is thanks to FATCA and all the red tape that the US government imposes on foreign banks who have US clients. For foreign banks, the logical business decision is to show Americans the unwelcome mat. The costs simply do not justify the benefits.

This is unfortunately true for many banks the world over. The net effect is to drastically reduce the number of choices that Americans have when banking offshore. It’s a sort of de facto capital control.

There are of course exceptions. Some solid offshore banks still accept Americans, and some even open accounts remotely. This means you could obtain huge diversification benefits without having to leave your living room.

In our comprehensive Going Global publication, we discuss our favorite banks and jurisdictions for offshore banking, crucially including those that still accept Americans as clients. It’s a list that is constantly dwindling, which highlights the need to act sooner rather than later.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.