What the Bearish Analysts Missed About Crude Oil Prices

Commodities / Crude Oil Feb 16, 2015 - 12:49 PM GMTBy: Money_Morning

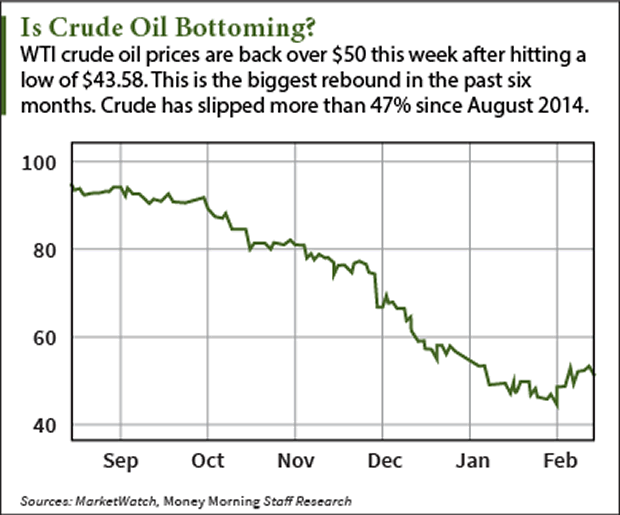

Dr. Kent Moors writes: Pundits continue to wrongly predict more pain in oil markets.

Dr. Kent Moors writes: Pundits continue to wrongly predict more pain in oil markets.

Citigroup analyst Ed Morse just came out with his most bearish forecast yet, claiming oil prices could fall to $20 a barrel. As for the recent rebound, Morse thinks it looks more like a "head-fake" than a sustainable turning point.

The market, of course, has ignored these concerns, as crude oil prices continue to climb.

But this hasn't stopped similar calls from others pushing their own doom-and-gloom forecasts.

Here's the one glaring problem with all of this bearish analysis…

Oil Prices Have Already Begun to Stabilize

As I've previously discussed, the nearly 60% plunge in the price of oil resulted in an abnormally oversold market, driven largely by the shorts. And without an actual pronounced decline on the demand side, there is very little likelihood of an oil price "Armageddon" happening anytime soon.

In fact, the oil picture has already begun to stabilize.

Now, admittedly, absent a major geopolitical crisis, we are not going back to triple-digit oil prices anytime soon.

But the trajectory now clearly indicates a new medium-term floor in the mid $50s in New York and about $60 in London. By the fourth quarter of this year, oil prices will likely trade even higher, somewhere in the $70s.

Fueled by the onslaught of huge reserves in U.S. unconventional (shale and tight) oil, the oil picture is rapidly changing. Scarcity has suddenly been replaced with abundance.

Today, we're facing a supply-side squeeze that will continue to influence crude oil prices – especially as the "shale revolution" goes global.

As for demand, it continues to climb globally – where the actual pricing dynamics take place. Just yesterday, OPEC revised its near-term demand projections higher, while cutting expected production from non-cartel nations. According to the cartel, demand for OPEC oil will average 29.21 million barrels per day (bpd) in 2015, up 430,000 bpd from its previous forecast.

OPEC determines its monthly production quota by estimating worldwide demand, then deducting non-OPEC production, resulting in what is referred to as "the call on OPEC."

But as I noted last week, this long time market barometer is undergoing a significant revision, and it's not in OPEC's favor. Now U.S. production is determining the price. Or as Morse puts it, "the call on OPEC" has been replaced by "the call on shale."

Now, the Paris-based International Energy Agency (IEA) expects global growth in oil demand to accelerate to 1.13 million bpd in 2016 from 910,000 bpd in 2015. Some of this is the simple reaction to lower crude oil prices – people use more oil when it costs less, especially in developing parts of the world where the use of diesel and other oil products is needed to generate essential electricity.

And there is another factor these "sky is falling" soothsayers fail to recognize. Despite a price decline of nearly 60% (most of that coming in the last quarter of 2014), we still ended up with the highest daily demand figure in history.

What makes this price decline different from all the others is the cause. Despite increasing global demand, the supply available to meet it has been rising even faster. That has put the brakes on the normal spikes in price that would result from any perceived interruption of the oil flow from world events or a rise in demand.

Of course, the ability to accurately estimate the available supply has become the mantra of the profession.

However, two fundamental mistakes are being made in the process…

The Rig Count Falls as the Market "Self-Corrects"

Both mistakes arise from trying to use traditional yardsticks to a measure a "non-traditional" market.

First, the talking heads have been incessantly harping on shale and tight oil reserves available for uplift. However, just because reserves are extractable does not mean they will be produced. Because this potential has recently emerged, shale reserves have created an overhang on the market, and the cost-side triggers required to cut production are still unknown.

Nonetheless, the reaction to the oil price decline in the U.S. has been pronounced. The rig count has fallen dramatically to levels not witnessed in over a decade. In addition, operating companies are mothballing more expensive projects and trimming capital expenses.

Yet the doomsayers respond that there is still considerable volume available from ongoing existing projects. That is true. But, as usual, they miss the governing factor. The continuing volume from existing projects is already factored into a market where demand is not collapsing.

As for the stockpiles at places like Cushing, OK, these surpluses have been weighing on the pricing spread between WTI oil and Brent oil for some time now. But they are hardly a major factor moving forward.

New sections of the Keystone Pipeline system (located within the U.S. and not needing approval) are already draining oil from Cushing to the Gulf Coast refineries. What's more, the decisions to reverse the flow in other pipelines – away from Cushing to the coast – are doing the same.

That makes the concern over an expanding glut at Cushing completely unwarranted, especially in an environment where domestic production is about to be reduced.

And what is underway among American producers is already taking place in Russia – the other primary non-OPEC producer. In Moscow, a central budget dependent on much higher oil prices has prompted a move to offset costs by delaying projects and reducing production.

That leaves the second overarching concern. This morning, the IEA reported that it may take some time to rebalance the oil market. Some pundits are already making bearish waves on the IEA statement, as much to offer an enticement to the next short play on oil as anything else.

Here's the problem. We don't need a perfectly balanced oil market. We never have. That's what trading arbitrage is all about, as future contracts expire and collide with the actual consignments of oil.

So long as there is a trading range, the system works quite nicely. According to just about any matrix, the market has not been balanced for much of the last decade. There are pricing changes in both directions, but the lack of a textbook balance has no appreciable impact.

It's just another red herring.

Yes, this is a "brave new world" of oil. Yes, the factors colliding are operating in new ways. But it's still the trade in oil that determines the price.

The sky is simply not falling… and we are going to continue to see fantastic profit-making opportunities in the months ahead.

The Shape of the World Today Is Dominated by Energy… On Jan. 29, two events thousands of miles apart demonstrated how central energy has become in the world of geopolitics. The map is being recast right before our very eyes. Here's why the Keystone XL will be built in the end…

Source :http://moneymorning.com/2015/02/10/how-analysts-are-wrong-about-crude-oil-prices-again/

Money Morning/The Money Map Report

©2014 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.