INFLATION Means the Choice Between Stagflation and Recession- Part 2

Economics / Inflation Jun 15, 2008 - 07:53 AM GMT

Click here for Part 1 - Jim Sinclair (Mineset): Bernanke has painted himself into a corner

“The euro is down hard today on the premise that this is the start of increased interest rates in the US, a statement that is totally ludicrous.

“There are two possibilities here:

1) Bernanke and Trichet are in the midst of a pissing contest with the US Fed not paying any attention to the financial hell they are about to release.

2) Saving face at the Fed is more important than the cost thereof.

“There is only one result possible: Any nitwit knows what happens if you increase the discount rate when business is accelerating its downturn.

“Now what happens if the Fed does not increase rates? Bernanke has painted himself into quite the corner.

“There is absolutely no possibility on earth that the Fed can start a series of increases as that will end the financial world, not as we know it, but totally.”

Source: Jim Sinclair, Mineset , June 10, 2008.

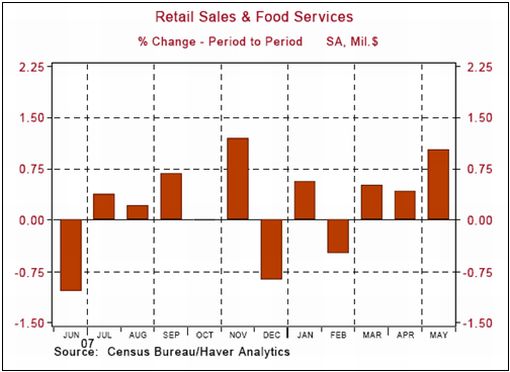

Asha Bangalore (Northern Trust): Retail sales – temporary boost from rebate checks

“Retail sales increased 1.0% in May, with a significant probability of rebate checks providing a temporary boost to the headline.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , June 12, 2008.

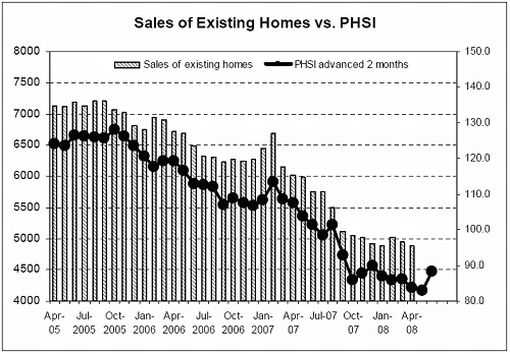

Asha Bangalore (Northern Trust): Additional evidence necessary to call bottom of housing market

“The 6.3% increase in the Pending Home Sales Index (PHSI) of the National Association of Realtors to 88.2 in April, is impressive after the downward trend that has been in place for several months. The PHSI increased in the Midwest (+13.0%), West (+8.3%) and South (+4.3%) but fell 1.9% in the Northeast. It is too early to attribute a single-month's gain to a major improvement of conditions in the housing market. The April reading of the PHSI points to sales of existing homes in the May to June period.

“… the increase in the PHSI for April is a signal of improving conditions but we need to see data for sales, prices, and inventories for a few consecutive months to call a firm bottom of the housing market.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , June 9, 2008.

Bloomberg: Mortgage bonds resume stumble, trading near lows

“Some of the US mortgage bonds at the center of the yearlong credit crisis are slipping toward new lows, as climbing gas prices, unemployment and interest rates deepen concern that homeowner defaults will increase.

“The benchmark Markit ABX index linked to the last-to-be-repaid of originally AAA rated subprime-mortgage bonds from the first half of 2007 fell today to a record low of 50.55, down about 16% from May 19, suggesting a corresponding drop on similar securities. Top-rated, bonds of ‘option' adjustable-rate mortgages are also falling, according to a report from RBS Greenwich Capital.

“‘There's a tremendous amount of extraneous events going on away from the mortgage market that are making people scared,' said David Castillo, a senior trader at Further Lane Securities. ‘Market activity over the last two weeks is down significantly over the previous four weeks.'

“Non-agency mortgage bonds, the type that have experienced unprecedented downgrades and price declines since mid-2007, lack guarantees from government-chartered Fannie Mae and Freddie Mac, or federal agency Ginnie Mae. The market totaled $2.1 trillion on March 31, excluding derivative exposures, according to Fed data.”

Source: Jody Shenn, Bloomberg , June 11, 2008.

Eoin Treacy (Fullermoney): US government bonds in long-term bear market

“The US 10-yr yield bottomed in 2003 and bonds are now in a secular bear market. The recent fall in yields found support above the lows near 3% and would need to sustain a move below that level to offset scope for a rally towards the upper side of the base over the coming years. Yields took 22-years to fall from their accelerated peak and may yet take as long again before they reach the highs of this secular move.

“This is a long-term cycle, and it will not be the same as the last bond bear market, but it will give context to almost every other asset class over the coming decades.”

Source: Eoin Treacy, Fullermoney , June 10, 2008.

John Hussman (Hussman Funds): Return on Treasuries not compelling

“… my inclination is to expect some downward pressure on yields as economic signals deteriorate. There is a good deal of ‘headline pressure' from the spike in unemployment, rising oil prices, and weak housing. All of these are likely to reinforce some retrenchment among consumers, which could help to tip the US economy more definitively into recession.

“Still, the prospect of 10-year total returns of just 4% in Treasury bonds is not particularly compelling on an investment basis, so the primary driver of bond returns will be speculation about economic weakness and a ‘flight to safety' from credit concerns.”

Source: John Hussman, Hussman Funds , June 9, 2008.

David Fuller (Fullermoney): Stock markets – give upside benefit out the doubt

“The Fullermoney view has been that important lows were reached following a selling climax in January. A rebound occurred but those lows were tested a couple of months later, and mostly held during further climactic selling in mid-March. Sentiment indicators, which we prefer in attempting to identify important lows, reached their most extreme levels since at least October 2002 as this year's January and March troughs were established.

“Following the mid-March lows, most stock market indices experienced orderly rallies which carried into mid-May. A few indices remained generally weaker, even extending their overall declines, but many more were stronger and pushed to new all-time highs. The weaker markets usually had a heavy weighting of banks, whilst the new highs were mostly achieved by what we think of as primarily resources indices.

“In late May I said that a stock market reaction had commenced. Subsequently and gradually, technical action for most indices continued to deteriorate, and not without reason.

“Bank indices, which we generally regard as lead indicators, deteriorated in the west, breaking their January and March lows, and experiencing significant additional declines in some instances. Petroleum contracts spiked higher, as have corn prices in a move that has firmed most agricultural commodities. Central bankers have become noticeably more hawkish in commenting on rising inflation. Long-dated government bond futures have weakened. Most forecasts for GDP growth and corporate profits have been lowered.

“‘Stuff happens' as some analytical genius once said, and investors now have more to worry about than the credit / derivatives crisis and its knock-on effects, which were bad enough. The Wall Street leash-effect has been negative with the Dow and S&P 500 indices approaching their January and March lows. The Nasdaq and Transports had been much stronger, but they too have suffered technical deterioration recently.

“In other words, the news probably could not get much worse, although perhaps this statement shows a lack of imagination on my part. Is there any good news out there and perhaps more importantly, scope for it to improve?

“Valuations have improved as a consequence of the earlier sell-off, although they are not timing indicators. Moreover, valuations are neither sufficiently attractive nor the economic environment encouraging enough to persuade conservative bears to buy aggressively, and we can be reasonably certain that hedge funds which can short stock markets have been doing so.

“Short covering could provide the fuel for a technical bounce, now that stock markets are technically oversold on a short-term basis. Also, many investors hold reasonably high levels of cash, but what would persuade them to buy?

“I do not know, although I suspect many would want a catalyst; not least evidence that the January and March lows were holding. Also, I suspect that central banks will remain an influence. From China recently to the USA previously, we have seen evidence that monetary officials would like to check the stock market slide. Psychologically, the Fed and US Treasury's actions are probably more important, due to the leash-effect and also because the US is still perceived as the epicentre of global economic problems.

“Meanwhile Wall Street and other leading stock markets are approaching their moment of truth in terms of the year's earlier lows. Once again, the recovery hypothesis is for the bulls to prove. Financials need to improve their relative performance.

“Anything less would be inconsistent with the support building hypothesis that I have been advocating. I have previously said on many occasions that I would give the upside the benefit of the doubt, provided the January and March lows for most indices held. I am concerned by the recent deterioration but will not change my medium-term view against the background of today's somewhat overstretched declines and while most of the year's earlier lows continue to hold.”

Source: David Fuller, Fullermoney , June 12, 2008.

Eoin Treacy (Fullermoney): Philadelphia Bank Index becoming overextended

“The Philadelphia Bank Index is leading other banking sectors on the downside, but is becoming overextened as it approaches a potential area of support near 60. An upward dynamic is needed to check momentum while a sustained break of the lower highs with a move above 90 would be needed to question downside scope.

“The fact that the Fed has been supplying cash to the banking sector for the last number of months is well known. This is not something we would expect to continue in perpetuity and is more of a stop-gap measure to get the economy through the credit crisis.”

Source: Eoin Treacy, Fullermoney , June 10, 2008.

CNBC: Meredith Whitney – Investment banks' recovery not imminent

Source: CNBC , June 11, 2008.

Financial Times: Banks face $10 billion monoline charges

“Citigroup, Merrill Lynch and UBS, the banks most exposed to Ambac and MBIA, could face further writedowns of up to $10 billion after the bond insurers last week lost their fight to retain their triple A credit ratings.

“Wall Street executives said they had been wrong-footed by the timing of the downgrades by Moody's and Standard & Poor's, saying they had not expected the rating agencies to take action for several months after affirming the triple A ratings of Ambac and MBIA in February and March.

“‘I think Moody's jumped the gun,' a Wall Street executive said. “They and other credit rating agencies have been under pressure to anticipate developments, rather than lag behind the curve, and this looks like an attempt to do just that.'

“The banks have used the bond insurers to hedge holdings of complex bonds such as collateralised debt obligations and other mortgage-backed securities.

“The prospects of further writedowns related to bond insurers, also known as monolines, could deepen concerns over the financial health of US and European banks.

“Meredith Whitney, analyst at Oppenheimer, said in a report this week that UBS had the largest exposure to monolines of $6.3 billion, Citigroup came second with $4.8 billion and Merrill Lynch followed with $3 billion.”

Source: Aline van Duyn and Francesco Guerrera, Financial Times , June 10, 2008.

Richard Russell (Dow Theory Letters): Lowry's Buying Power Index making new lows

“‘On June 3, June 4 and again today, Lowry's Buying Power Index dropped to new lows, showing that the strong, persistent demand needed to push the broad list of stocks substantially higher was simply not in evidence. Nor is it likely to emerge in the near future. There is not a single case within our 75 year history in which the Buying Power Index was still making new lows eight or ten weeks after an important market bottom.'

“The implications of the Lowry's statement is clear enough. If there is no case of Lowry's Buying Power making new lows many weeks after an important market bottom – then the fact that Lowry's Buying Power is now making new lows indicates that the stock market has NOT yet put in an important bottom. In other words, we have not yet seen a bottom so far in 2008. If this is true, then the major averages and many, if not most, stocks are fated to break to new lows.

“Whew! That's a critically important observation. Let's suppose the Lowry's stance is correct, suppose the January-March lows were only temporary stops in a bear market that is fated to head lower. I've stated that this is a critically important question – are we in a bull or bear market? If Lowry's is correct, if the bear market lives, then in due time the market will smash below its January-March lows, and in doing so we will have a forecast of worse times ahead. To put it another way, new lows will mean that the market has not yet discounted the worst that lies ahead.”

Source: Richard Russell, Dow Theory Letters , June 9, 2008.

Coloradoan: Litman-Gregory study – focus on longer term

“Litman-Gregory … with the help of Ned Davis Research … studied periods of S&P 500 market declines of 15% or more since 1950.

“It found that the average length of the 12 declines was 28.5% and that the median loss was 24.6%. The average gain in the intermittent periods was 112%. The gains' periods lasted on average about 3½ years.

“There were numerous market declines of 10% to 15% but they quickly reversed. However, there were few periods where the decline reached 15% and did not go to 20% or more, which is the official designation of a bear market.

“Over the period since 1950, bear markets have generally not lasted as long as bull markets have. During the 58-year period, the market has risen in 46 years and declined in only 12 years.

“In the 12 loss periods, a 15% or more loss in the S&P 500 occurred over six months.

“Seven of the nine recessions occurring since 1950 overlapped market declines. In six recessions, stock prices began recovering before the recession ended. In seven of the 12 declines of 15% or more, there was no recession.

“Of the 12 bear markets since 1950, investors recovered their losses in about 14 months. The median recovery period was eight months. Dividends played an important role in investor returns. On average, dividends allowed investors to recoup their losses in about seven months.

“The Litman-Gregory's study looked at the S&P 500 total return performance in years immediately following market declines of at least 15%. In 11 of the 12 periods following declining stock prices, the market produced a positive total three-year return. However, in the five years following a 15% loss, positive returns were in single digits half the time. On average, the market return was 9.8% annually in the five years following the point at which a 15% loss was reached.

“According to Bob Brinker's Marketimer newsletter, corrections in the 15% to 19% range are extremely rare in a presidential election year. In the past 60 years, there have been only two brief and mild recessions during presidential election years. There has never been a bear market, a decline of 20% or more, in a presidential election year.”

Source: James Watt, Coloradoan , April 27, 2008.

Bloomberg: China's benchmark stock index tumbles

“China's stocks plunged 8.1%, the most since February 2007, after the central bank ordered lenders to set aside record reserves to curb credit growth and inflation.

“More than half of the benchmark stock measure's 300 members slumped by the 10% daily limit, dragging the CSI 300 Index 45% below its October 16 record.

“Industrial & Commercial Bank of China led banks lower after the central bank said June 7 it will raise the reserve ratio for the fifth time this year by a full percentage point, withdrawing about $61 billion from the financial system.

“‘Panic is arising from a jolt of bad news,' said Peter Chiang, Singapore-based chief equity strategist at DBS Asset Management Ltd., which oversees the equivalent of $18 billion. ‘There are problems with inflation, China is slowing down and corporate earnings could be vulnerable.'

“The CSI 300 has fallen 40% this year, the steepest decline among the world's 20 biggest equity markets, on concern that measures to keep price increases in check will erode earnings. The rout has wiped at least $1.31 trillion from China's stock market and helped the CSI 300 close a price-earnings gap with the Standard & Poor's 500 Index to 3.1% from 127% at the start of 2008, data compiled by Bloomberg show.”

Source: Zhang Shidong and Chua Kong Ho, Bloomberg , June 10, 2008.

Eoin Treacy (Fullermoney): African stocks outperforming rest of world

“Africa remains an interesting, if high risk, investment destination. It may also be benefitting, at this time, because it is non-correlated with the rest of the financial world and is currently outperforming. However, investors should also be aware that markets with such small capitalisations are easily manipulated and often rise extraordinarily because of the weight of money. When investors eventually decide to take their money out, apparently strong markets can turn into laggards overnight. I have every belief that Africa will eventually emerge as a safer place to invest but it will take decades and the path will be far from linear.”

S&P Africa Frontier Price Index

Source: Eoin Treacy, Fullermoney , June 9, 2008.

Bloomberg: Analysts lose 17% for investors in brokerage picks

“Investors who followed the advice of analysts who say when to buy and sell shares of brokerage firms and banks lost 17% in the past year, twice the decline of the Standard & Poor's 500 Index.

“Buying shares on the advice of Merrill Lynch's Guy Moszkowski, the top-ranked brokerage analyst in Institutional Investor's annual survey, cost investors 17%, according to data compiled by Bloomberg. Deutsche Bank analyst Michael Mayo's counsel to purchase New York-based Lehman Brothers lost 59%. Citigroup's Prashant Bhatia still rates Merrill ‘buy' after its 56% retreat from a January 2007 record.

“Of the 39 analysts tracked by Bloomberg who follow stocks in the Amex Securities Broker/Dealer Index, 32 produced losses for investors. Investors who bought brokerages on ‘buy' recommendations, sold when they switched to ‘hold' and speculated prices would decline when analysts said ‘sell', lost 17% in the last year through June 3, compared with the S&P 500's 8.5% drop.

“‘One would expect that if there was any industry Wall Street estimates would be more precise on, it would be their own,' said Richard Weiss, who oversees $60 billion as chief investment officer at City National Bank. ‘But this particular debacle was so global in nature and pervasive, you can't blame them for missing this one.'”

Source: Eric Martin and Josh Fineman, Bloomberg , June 6, 2008.

Fortune Magazine (via CNN Money): Buffett's big bet

“Will a collection of hedge funds, carefully selected by experts, return more to investors over the next 10 years than the S&P 500?

“That question is now the subject of a bet between Warren Buffett and Protégé Partners, a New York City money management firm that runs funds of hedge funds – in other words, a firm whose existence rests on its ability to put its clients' money into the best hedge funds and keep it out of the underperformers.

“Protégé has placed its bet on five funds of hedge funds – specifically, the averaged returns that those vehicles deliver net of all fees, costs, and expenses.

“On the other side, Buffett, who has long argued that the fees that such ‘helpers' as hedge funds and funds of funds command are onerous and to be avoided has bet that the returns from a low-cost S&P 500 index fund sold by Vanguard will beat the results delivered by the five funds that Protégé has selected.

“We're way past theory here. This bet, being reported for the first time in this article (whose author is both a longtime friend of Buffett's and editor of his chairman's letter in the Berkshire annual report), has been in existence since January 1 of this year.

“It's between Buffett (not Berkshire) and Protégé (the firm, not its funds). And there's serious money at stake. Each side put up roughly $320,000. The total funds of about $640,000 were used to buy a zero-coupon Treasury bond that will be worth $1 million at the bet's conclusion. That $1 million will then go to charity.”

Source: Carol J Loomis, Fortune (via CNN Money ), June 9, 2008.

Richard Russell (Dow Theory Letters): “Happy time” for the US dollar

“If you're a fan of the US dollar, maybe this is ‘happy time'. Below we see one year of Dollar Index action. The low was recorded on March 17. From there the Dollar headed higher. During May-June the Dollar Index formed what appears to be a head-and-shoulders bottom. This week the Dollar broke out above its bottoming formation and also above its long declining trendline. Larry Kudlow on CNBC keeps shouting that we need a ‘strong dollar' and that ‘a strong dollar will set stocks heading higher'. Kudlow may finally be getting his long-awaited strong dollar, but we'll just have to wait to see whether he gets his rising stocks as well.

“A strong dollar should also be good for bonds, but bonds have more to worry about than just the dollar. They have inflation to worry about plus the possibility that the economy may be turning up.

“Of course a strong dollar would be a negative for gold. There should be strong support at the 850 level, even in the face of a strong dollar. I think gold is simply biding its time as it builds a base for its next advance. By the end of this year, gold should be considerably higher.”

Source: Richard Russell, Dow Theory Letters , June 13, 2008.

Ambrose Evans-Pritchard (Telegraph): Iran's switch good news for gold bulls?

“Good news for long-suffering gold bugs. Iran is switching a chunk of its $80 billion reserves into bullion.

“When I asked Barrick Gold's Peter Munk in Davos whether it was significant that Vladimir Putin had ordered his central bank to switch 10% of Russia's reserves into gold, he just laughed. “That must mean Putin wants to sell gold,” he said.

“Nothing is ever what it seems.”

Source: Ambrose Evans-Pritchard, Telegraph , June 10, 2008.

David Fuller (Fullermoney): Commodity supercycle is alive and well

“Since resources have been an early and crucial investment theme at Fullermoney over the last seven years, during which we have repeatedly expressed our view that this is a commodity supercycle, I have plenty of sympathy for the pension funds and other long-term investors who wish to buy and hold essential resources, from crude oil to agricultural commodities. After all, there is supply inelasticity, rising demand and we live in a fiat currency world which all but guarantees that the environment is inflationary more often than not.

“However these commodities were never meant to be asset classes. Does anyone seriously believe that many billions of dollars invested in futures contracts, on a long only basis and rolled forward for the indefinite future, does not cushion downside risk for prices and often propel them higher?

“The good news is that this will make many farmers richer, particularly where they can sell their produce on the open markets. This will reduce the need for expensive government subsidies to the agricultural sector. The bad news is that it will also increase the cost of food for many people around the world who are least able to afford the higher, inflated prices. To the extent that it is a boon to commodity exporting countries, including oil producers, for importing countries it has the financial impact of a tax, albeit with the revenue flowing to another country.

“Obviously the Commodities Futures Trading Commission (CFTC) faces a dilemma, probably too visibly tempting for politicians not to become involved. Should the CFTC, to the extent that it has a free hand, declassify long-only investors in trackers as ‘commercials' and risk driving them to other exchanges? Or should they accept the political flack, take a long-term view and embrace the investors as new stakeholders who will help the supply of commodities to increase, where possible, over the longer term? This should be feasible for foods and if not for oil, then for other forms of energy, including renewables.

“What are the other investment implications?

“To the extent that pension funds and other long-term investors have been buying commodity trackers as a hedge against inflation and / or because of rising demand from increasingly prosperous developing countries, these arguments apply equally to precious metals. For anyone deterred from holding agricultural commodity or crude oil trackers, at least until current uncertainty regarding the CFTC's policies is resolved, a switch to gold and other monetary metals would seem obvious.

“I maintain that the long-term investment outlook for this sector remains compelling. Gold remains real money, for anyone with a sense of monetary history, and unlike agricultural commodities, supply is limited.”

Source: David Fuller, Fullermoney , June 11, 2008.

Bloomberg: OPEC's El-Badri says worldwide oil market well supplied

“OPEC Secretary-General Abdalla El-Badri talks about the impact of speculators' moves on oil prices, global demand and the OPEC's spare production capacity. OPEC, the supplier of more than 40% of the world's crude, will meet oil-consuming nations on June 22 in Jeddah, Saudi Arabia, to discuss the effect of rising oil prices on their economies.”

Source: Bloomberg , June 11, 2008.

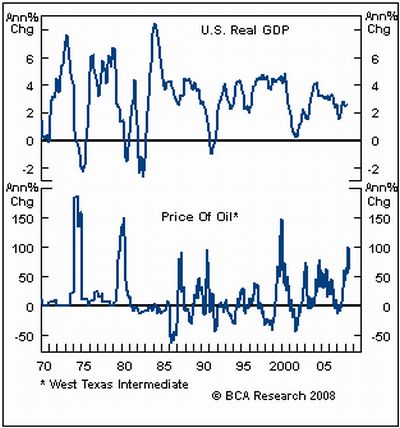

BCA Research: Oil continues to threaten growth

“Crude oil prices surged by over $10/bbl on Friday, hitting a new record high and presenting a significant headwind for the growth/earnings outlook.

“Oil prices appear to be undergoing a blow-off phase. While longer-term fundamentals remain bullish, our Commodity & Energy Strategy service expects crude prices to undergo a setback in the coming weeks, followed by a consolidation phase at historically elevated levels. Almost all momentum measures are stretched and bullish consensus is at a cyclical extreme. At the same time, the US has stopped filling its Strategic Petroleum Reserve and many emerging Asian countries are reducing or removing energy subsidies, which should help curb demand. Still, it will be critical for risky assets that the blow-off phase does not persist much longer. Energy costs are rapidly siphoning off US consumer incomes which are already under strain from declining real estate prices and a softening job market. Moreover, past spikes in oil have historically coincided with significant economic slowdowns.

“Bottom line: We maintain our modest long/overweight allocation in global equities but acknowledge that rising oil prices is the primary threat to this call (via the drag on earnings). In contrast, we are less concerned about the inflationary implications of rising energy costs.”

Source: BCA Research , June 10, 2008.

Herald Tribune: ECB chief warns against oil shock

“The president of the European Central Bank, Jean-Claude Trichet, on Monday called on oil producers and consumers to learn from past mistakes if Western economies were to avoid a repeat of the high inflation and unemployment that followed the first global oil shock in 1973.

“That year is widely acknowledged as an economic watershed, a time when an OPEC oil embargo led to a spiral of higher prices, recession in Western economies and a wrenching contraction in the early 1980s that finally put an end to a decade of sharp inflation.

“No one, whether Western consumers or oil suppliers, should want to repeat that history, Trichet said. ‘There is a joint interest in behaving as properly as possible,' he said.”

Source: Carter Dougherty, Herald Tribune , June 9, 2008.

Financial Times: ECB damps speculation on rate rise series

“The European Central Bank moved to damp down market expectations of a flurry of interest rate rises in the coming months by signalling on Wednesday that a planned rise in eurozone rates next month was likely to be a one-off.

“Comments by ECB governing council members sought to correct financial markets' impression that July's expected hike would mark the resumption of a monetary policy tightening cycle – an expectation that has depressed bonds and the dollar while possibly helping to inflate oil prices.

“They suggested the ECB was nervous that its hardline anti-inflationary stance – which has raised concerns in Washington – had been overstated.

“Jean-Claude Trichet, ECB president, last week described a quarter percentage point rise in the bank's main interest rate to 4.25% as ‘possible' although not a certainty.

“But on Wednesday Christian Noyer, the governor of the Bank of France, said he did ‘not see a clear link' between Mr Trichet's comments and financial markets' expectations of further rises later in the year. Earlier, Jürgen Stark, an ECB executive board member, was even blunter, telling Bloomberg agency that while markets had understood last week's message, ‘we are not talking about a series of rate increases'.

“The ECB's move last week followed its mounting concerns about the surge in eurozone inflation, which has been driven higher by soaring oil prices. The ECB expected the rise to be temporary but feared that without pre-emptive action, expectations about future inflation rates in coming years would also rise – and become self-fulfilling.”

Source: Ralph Atkins, Financial Times , June 11, 2008.

Financial Times: Irish voters reject EU treaty

“José Manuel Barosso, European Commission president, called on EU member states to continue ratifying the Lisbon treaty after more than half of Ireland's 43 constituencies rejected the European Union's new reform treaty.

“The European Union was braced on Friday night for one of the most critical weeks in its 50-year history after Irish voters delivered a decisive rejection of the bloc's Lisbon treaty – a document designed to make the EU a stronger global force.

“Although the result plunged the EU into turmoil, its leaders insisted that other states continue to ratify the bloc's Lisbon treaty and said they would try to address the crisis at a summit in Brussels next Thursday and ¬Friday.

“The treaty's provisions, which cannot now come into force as planned at the beginning of next year, include the appointment of the EU's first full-time president, a strengthened role for the EU's foreign policy chief and increased powers for the European parliament and national parliaments.

“Brian Cowen, the Irish premier, said he saw ‘no quick fix', adding: ‘In a democracy, the will of the people as expressed at the ballot box is sovereign. The government accepts and respects the verdict of the Irish people.'

“Thursday's vote against Lisbon – officially put at 53.4% to 47.6% – plunged EU leaders into a crisis almost identical to that generated by Dutch and French voters when they threw out a proposed EU constitutional treaty in 2005.

“The result was a kick in teeth for the Irish political and business establishment. All the main parties were united in support of a Yes vote and had the backing of big companies and small business associations alike.

“Government ministers blamed the outcome on ‘scare-mongering' by No campaigners who raised fears the treaty threatened Irish sovereignty and the Irish way of life on issues such as taxation, neutrality and abortion.”

Source: Financial Times , June 13, 2008.

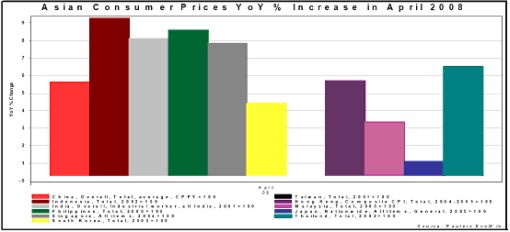

GaveKal: Asian consumer prices strongly higher

Source: GaveKal – Checking the Boxes , June 12, 2008.

Bloomberg: India raises interest rate to rein in inflation

“India's central bank unexpectedly raised interest rates for the first time in 15 months, joining a global wave of monetary tightening to combat a surge in inflation sparked by food and energy costs.

“The Reserve Bank of India increased the repurchase rate to 8% from 7.75% from today, according to a statement in Mumbai. The move came seven weeks before the bank's scheduled monetary policy meeting on July 29.

“Governor Yaga Venugopal Reddy joins central bankers in Brazil, China and Russia, the so-called BRIC nations, in raising borrowing costs. The urgency signals Reddy's concerns after India raised fuel prices at the sharpest pace in at least six years.

“‘It would have been impossible for the central bank to ignore that,' said Robert Prior-Wandesforde, senior economist at HSBC. ‘Particularly with inflation being so sensitive a subject politically in India.'

“Rising prices have eroded the popularity of Prime Minister Manmohan Singh's Congress party, which has lost ground in nine of 11 state elections since January 2007. Singh's main ally, the communist parties, and the opposition Bharatiya Janata Party have staged nationwide protests in the past week, blocking trains and roads …”

Source: Cherian Thomas, Bloomberg , June 11, 2008.

Jim Sinclair (Mineset): Total notional value of derivatives surpasses one quadrillion

“The notional value of all outstanding derivatives now totals approximately $1.144 QUADRILLION.

“This appears to be Bank of International Settlement spin to announce the largest gain in derivatives outstanding since they started to report. As of the last report it appeared that both listed and OTC derivatives was under $600 trillion. Now listed credit derivatives alone stood at $548 Trillion. The OTC derivatives are shown as $596 trillion notional value, as of December 2007. One can only imagine what number they are at now.

“Well we hit a QUADRILLION. We have more than $1,000 trillion dollars in all derivatives outstanding. That is simply NUTS because notional value becomes real value when either counterparty to the OTC derivative goes bankrupt. $548 trillion plus $596 trillion means $1.144 quadrillion.

“This means that no OTC derivative house can be allowed to go broke. This means that whatever funds are required to rescue failing international investment banks, banks and financial entities will be provided.

“Keep this economic law in mind. Monetary inflation proceeds price inflation and is its primary cause in economic history from Rome to present.

“Nothing can stop the juggernaut of price inflation heading towards every nation like a runaway freight train down a mountain.”

Source: Jim Sinclair, Mineset , June 9, 2008.

CNBC: Sex and the stimulus package – “More bang for the buck'?!

“It seems the down economy is hurting every business, even the oldest profession. The Moonlight BunnyRanch in Carson City, a legal brothel featured on HBO's ‘Cathouse', is offering the first 100 customers who show up with their stimulus rebate checks twice the ‘services' for the same price.

“It seems the down economy is hurting every business, even the oldest profession. The Moonlight BunnyRanch in Carson City, a legal brothel featured on HBO's ‘Cathouse', is offering the first 100 customers who show up with their stimulus rebate checks twice the ‘services' for the same price.

“They're calling it, (this is where I clear my throat uncomfortably), ‘more bang for your buck'. The BunnyRanch is a place Larry Flynt calls ‘America's Hottest Cat House', and he oughtta know.

“As for the stimulus offer, a guy who brings in an entire $1,200 check gets a special deal: three women and a bottle of bubbly. Anyone notice that a guy with a $1,200 check is married to qualify for that amount?

“But wait, there's more! The legal bordello plans to have all 100 customers, plus some of the Bunnies, sign a thank you card and send it to President Bush. Oy.”

Source: Jane Wells, CNBC , June 12, 2008.

Did you enjoy this posting? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.