A Bond Market Crisis Is Coming... Here's What to Do

Interest-Rates / US Bonds Jul 24, 2015 - 06:03 PM GMTBy: DailyWealth

Dr. David Eifrig writes:

Wall Street is already sending warning signals about the next financial cataclysm. Analysts are using phrases like "liquidity crunch" and "crisis situation."

Dr. David Eifrig writes:

Wall Street is already sending warning signals about the next financial cataclysm. Analysts are using phrases like "liquidity crunch" and "crisis situation."

It could happen next week... or next month...

Predicting exactly how a crisis will happen is difficult. Predicting exactly when is impossible.

But we can prepare for it today. Below, I'll show you how.

Let's get started by taking a closer look at the developments in the bond market...

The bond market has changed over the last five years. In the past, big banks acted as "market makers." A market maker facilitates trades between buyers and sellers... maintaining both a bid price and an ask price... and it makes money on the difference between the two, called the "spread."

Sometimes, a market-maker bank would step in to buy when others wanted to sell, and sell when others wanted to buy. That helped keep markets stable.

However, big banks have reduced their bond-trading activities because of new regulations and higher capital requirements. It simply doesn't make financial sense for the big banks to be in this business anymore.

Now, liquidity in bonds has dried up. By liquidity, we mean that investors can buy and sell bonds quickly and at low transaction costs. When markets become illiquid, it can lead to wild swings and big, instantaneous jumps in prices.

A single hiccup in bond markets could lead to a "liquidity crisis."

In the U.S. Treasury securities market, financial-services giant JPMorgan Chase estimates that five years ago, you could move about $280 million worth of Treasury securities before your trades moved the market's price. Now, that's down to $80 million... a decline of more than 70%.

When a panic sets in, reduced liquidity can cause big swings in market prices. We're not the only ones concerned about this development...

• JPMorgan CEO Jamie Dimon has called recent moves in bond and currency markets "a warning shot across the bow."

• The Bank for International Settlements, an international organization of central banks, concluded in a research note that market liquidity will be fragile in the short term.

• A U.K. portfolio manager, quoted in the Financial Times, said, "If everyone wants to redeem at once, there could be a liquidity crunch because without the banks, there won't be anyone bidding for bonds."

The lack of bidding is the crux of a liquidity crisis...

In a run-of-the-mill bear market, you just have a downward trend... When enough investors are selling bonds, it drives down prices. Falling prices lead more investors to start selling. We see that all the time.

A liquidity crisis goes even further. It's like a classic run on a bank... Without sufficient liquidity, the sellers don't just see lower prices... they see no prices. Since no one wants to buy bonds at this particular time, the price for them effectively becomes zero.

This is a big problem for mutual funds and Wall Street money managers...

As a liquidity crisis begins, investors start demanding their money back. So the funds need to sell their bonds to pay the investors back. But the market isn't functioning properly. The prices of bonds drop even more.

This may sound bleak, but an astute investor sees the opportunity here...

In a liquidity crisis, bonds don't suffer any damage to their real value... It's simply the price that collapses. As long as the issuing company doesn't go bankrupt, they'll continue to pay interest payments and principal at maturity.

Here's the crazy part. Everyone knows that these assets will quickly return to their prior prices. But only individual investors like you can take advantage of situations like these.

It's the biggest advantage you have over Wall Street.

With panicked investors demanding their money back, hedge funds, mutual funds, and banks know these bonds are a steal. But they simply can't buy them. Any cash they have is needed for investor redemptions or meeting margin calls.

As an individual investor, you don't answer to anyone but yourself. You don't have to provide quarterly updates or report the daily values of your assets.

Only the U.S. Federal Reserve has the same freedom. And it made billions in profit by buying up mortgage bonds when no other investor would (or could) touch them in 2008.

In a liquidity crisis, you (and the Fed) can buy up cheap bonds... while professional investors watch with jealousy.

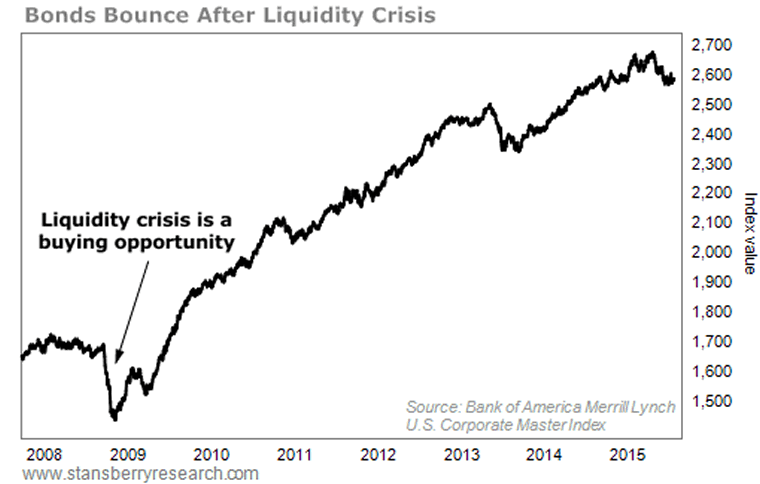

This buying opportunity occurs in even the safest assets. The Bank of America Merrill Lynch U.S. Corporate Master Index tracks corporate bonds that are rated as investment-grade. You can see that the liquidity crisis of 2008 caused them to fall... That made for a great buying opportunity:

Here's what you should do today...

When you start seeing headlines about a bond liquidity crisis, get ready to act.

The real crisis could happen in U.S. Treasury securities, foreign government bonds, or corporate bonds. We just don't know yet.

And don't be dissuaded if you haven't purchased bonds before. You don't need to be an expert.

Instead, you can look to an investment called a closed-end fund. Closed-end funds trade on an exchange just like a stock and they invest in all sorts of asset classes. (You can read our educational interview on the subject here.)

These funds have a big advantage over open-ended mutual funds and exchange-traded funds (ETFs) when a liquidity crisis hits.

Open-ended mutual funds and ETFs have to redeem customers' money each and every day. When investors hear about a big bond crash, they want to sell. This means the funds have to sell bonds into a terrible market to pay back these investors... driving down returns for everybody. After all, if the open-ended funds could just hold on until the market got back to normal, those bonds would bounce right back.

Closed-end funds DO NOT have to redeem investors' money. A closed-end fund raises capital and then its shares trade freely in the market. This means they can hold on to their bonds through a liquidity crisis and not have to sell them at depressed prices.

That's not the only advantage to closed-end funds...

The price of a closed-end fund trades independently from the assets it actually holds, called its net asset value, or "NAV." Those two prices, over time, tend to move in the same direction. But the difference can get quite large. Occasionally, you'll see discounts of 20% in certain assets. Discounts of 10% are quite common.

Panicked investors sell out of their bond funds at any price and with no regard for the underlying value.

This means that not only will the funds' bonds sell for fire-sale prices, but you can buy into the fund for even less than that.

It's not time to panic... My research team and I remain confident in the markets. We're still bullish on the stock market and content with the economy.

But at some point, we'll face another financial crisis. It's inevitable. By owning bond funds, you will have a huge advantage when it arrives...

If you're not already holding any bond funds, I urge you to be ready to act if the bond market gets the liquidity crisis that I've described.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Editor's note: Another problem many Americans face today is not knowing enough about one of the most complicated programs in the U.S.... Social Security. Fortunately, there's a solution. Right now, you can take advantage of little-known "loopholes" to start earning more money immediately...

That's why we are excited about our newest offer... where you can learn how to collect up to $200,000 from Social Security over the course of retirement. To get more details, click here.

The DailyWealth Investment Philosophy: In a nutshell, my investment philosophy is this: Buy things of extraordinary value at a time when nobody else wants them. Then sell when people are willing to pay any price. You see, at DailyWealth, we believe most investors take way too much risk. Our mission is to show you how to avoid risky investments, and how to avoid what the average investor is doing. I believe that you can make a lot of money – and do it safely – by simply doing the opposite of what is most popular.

Customer Service: 1-888-261-2693 – Copyright 2013 Stansberry & Associates Investment Research. All Rights Reserved. Protected by copyright laws of the United States and international treaties. This e-letter may only be used pursuant to the subscription agreement and any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of Stansberry & Associates Investment Research, LLC. 1217 Saint Paul Street, Baltimore MD 21202

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Daily Wealth Archive

|

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.