Credit Crisis Losses Pass $1.6 Trillion as Credit Contraction Ensures Recession

Economics / Credit Crisis 2008 Jul 12, 2008 - 09:50 AM GMTBy: John_Mauldin

$1.6 Trillion in Losses and Counting

$1.6 Trillion in Losses and Counting - Banks Start to Reduce Their Lending

- Take Freddie Mac. Please.

- The Ugly Muddle Through

- Once Again, the BLS Numbers Paint a False Picture

It seems that with each passing month the estimates for losses in the international banking system keep rising. This time last summer the largest estimates (from credible sources), if memory serves me correct, were around $400 billion, give or take a few months. By the end of the year it was in the neighborhood of twice that. Then last quarter we saw estimates approaching $1 trillion. Last week, the number being broached was $1.6 trillion, by Bridgewater Associates, one of the top, and more credible, analytical firms in the world.

In this week's letter we look at the implications of that projection, analyze recent lending patterns by banks, briefly touch on the implications of the recent unemployment numbers, and end with a few comments on the bear market. It will make for an interesting letter. Warning: remove sharp objects from your vicinity before reading.

But first, I need your help, and in return I would like to give you a link to a recent speech I gave, where I speak about what I think is the development of an important new asset class, one which will come about precisely because of the problems I am writing abut today. I have not yet written about this topic in public, and the speech has been well-received. I think you will like it. Now, as to how you can help me ...

I get to travel a lot with my daughter and business partner Tiffani (actually she runs the business) and meet new people. Over the years, she has become as fascinated as I have with their individual stories. Everyone has a story to tell or a lesson to teach. We have decided to write a book about those stories, looking at the differences in perspective between old and young, retired and working, those who are wealthy and those who aspire to wealth. What are the differences in attitudes, in work habits, in how you manage money, in how you look at the future, and a score of other items? How do all of these things correlate?

We have created a totally anonymous online survey seeking answers to these questions and more. We hope to get at least 10,000 people to fill out the survey; and we are eager to see what we find as we pore over the resulting data and engage in a lot of in-depth analysis. Are the rich really different? Is there a difference in people from Europe, Asia, Latin America, Africa, and the US? I think we will find some very interesting information. Please note: this is not just a survey for millionaires. We want everyone, of all income levels and ages, to take the survey, so we can get a true representative sample.

You can get to the survey page by clicking here . It will take about ten minutes to complete, and I think that going through the questions will make you think about your own situation. Some have told us the survey is quite thought-provoking. If you have attempted to take the survey and had problems, we think we have worked out the bugs.

At the end of the survey, you will be sent to a page with the speech. If you cannot listen to it immediately, then simply save the page or the address. And of course, you can just take the survey to help us.

Also, Tiffani and I want to do live (mostly by phone) interviews with 200 millionaires, of all shapes and sizes and locales. We will interview you for about 30 minutes, and then you can have equal time asking me anything you want. Since I will have learned a lot about you, those questions can be as detailed or as general as you like. We want at least 20% of the interviews to come from outside the US. We will use those interviews in the book, but will attach no identifying items or real names. If we use something from your interview in the book, we will let you see it first. If you are interested in being one of the interviewees, just drop Tiffani a note at eu@2000wave.com and she will get back to you and work out the details.

I am really excited about this project and even more so about working with Tiffani. We will report back to you on what we find. Thanks for your help. And if you have any questions, please feel free to reply to this email.

$1.6 Trillion in Losses and Counting

One of the great privileges I have is getting to read a wide variety of economic research. While I get a lot of material direct from the source, I also have a wide network of people who read other sources and send me what they think is important. When Ambrose Evans-Pritchard wrote this week about a report done by Bridgewater Associates, it got my attention, and fortunately this report was sent to me by a few friends. In my book, Bridgewater is one of the top analytical groups in the world. I pay attention and give strong credence to what they write. And this report is quite sobering.

First, let's look at what Evans-Pritchard wrote in the London Telegraph:

"Bridgewater Associates has issued an apocalyptic warning to clients that bank losses from the worldwide credit crisis may reach $1,600bn [$1.6 trillion], four times official estimates and enough to pose a grave risk to the financial system.

"The giant US hedge fund said that it doubted whether lenders would be able to shoulder the full losses, disguised until now by 'mark-to-model' methods of valuing structured credit.

" 'We are facing an avalanche of bad assets. We have big doubts as to whether financial institutions will be able to obtain enough new capital to cover their losses. The credit crisis is going to get worse,' said the group in a confidential report, leaked to the Swiss newspaper Sonntags Zeitung.

"Bank losses on this scale would have far-reaching effects. Lenders would have to curtail loans by roughly 10-to-one to preserve their capital ratios. This would imply a further contraction of credit by up to $12,000bn [$12 trillion] worldwide unless banks could raise fresh capital."

Let's look at some of the details in the report. First, these losses are not all subprime. In fact, more than half of it is from corporate liabilities, around $800 billion. About $550 billion of the corporate losses have yet to be written off. As an example, Bridgewater estimates losses on commercial loans to be as much as $149 billion, none of which has been written off.

Better than 90% of the losses from subprime assets that are on the books have already been written off. That is good. But Bridgewater estimates that there are losses lurking in the prime and Alt-A loan portfolios that could be much bigger than the subprime problems, as those loan books are more than six times the size of the subprime. Quoting:

"The US commercial banks are in a position to suffer the greatest losses, because the core of their portfolio is risky US debt assets. In order to get a sense of their expected losses we examine both their loan book and their securities portfolio and price each type of asset out based upon a reference market. If we use this current market pricing as a guide, there is a long way to go, as these institutions have only acknowledged about 1/6 of the expected losses that they will incur as a result of the credit crisis."

I could go on, but the details are not important. The bottom line is that they estimate there is at least another $1.1 trillion of losses that will have to be written off by institutions all over the developed world, including very large potential write-offs from insurance companies.

Banks and investment institutions worldwide may need another $400 billion in capital infusions. But where they are going to get it is the problem. They have burned through the usual suspects, and burned is the correct word. Any sovereign wealth fund or large investor who has put money into an investment or commercial bank has watched their investment take large losses in a very short time. How likely are they to be willing to belly back up to the bar with more money, on anything except very dilutive terms to current shareholders? The answer is obvious.

And let me be clear. There are some very large commercial and investment banks which are simply going to be absorbed, as regulators move to keep the entire system working. Bear Stearns is not a one-off deal. I think it is likely we will see at least one European bank nationalized. Losses the size that Bridgewater describes are beyond ugly. They are life-threatening for more than one major institution. More on this later.

Banks Start to Reduce Their Lending

Further, let's revisit a theme I have written about on several occasions over the past year. As banks incur losses, they either have to find new capital or reduce their lending in order to maintain their capital ratios, or some combination of both. And what we are seeing is that lending is starting to actually decrease.

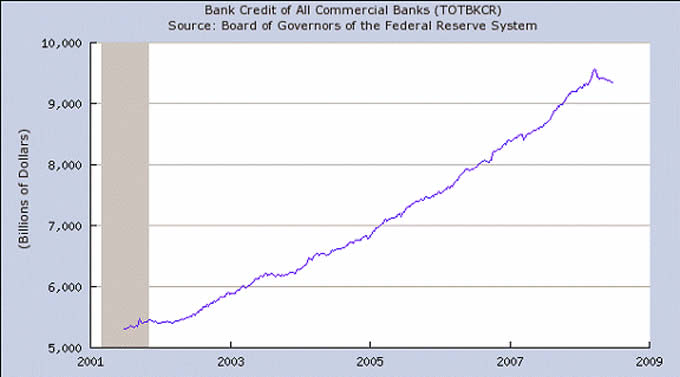

Earlier this year lending rose as normal, even though anecdotal reports told of tightening lending standards and reduced loan lines. The tightening of standards did not seem to be affecting actual loans being made, which was odd. But this was partly illusion, as banks were taking back loans they had spun off in SIVs, taking capital away from their traditional loan business. This gave the appearance of expanding loan capacity. Evidently, this bringing back of off-book loans is now being worked through, as evidenced by this analysis by good friend and analyst par excellence Greg Weldon, who slices and dices the data to give us this view ( www.weldononline.com ):

"[looking at the chart below] ... FOR SURE, the recent decline strongly suggests that the risk of a US recession has intensified CONSIDERABLY, as defined by what amounts to one of the largest nominal credit contractions in DECADES, at (-) $154.3 billion, and a clear-cut violation of the uptrend in place since at least 2001."

Greg goes on to suggest that bank credit could contract a further $6-700 billion over the next nine months, which is a contraction of about 8%. Healthy economies have a rising rate of bank credit, which is one source of expansion. When banks have to reduce their lending, it reduces the growth of the economy or can put it into outright recession.

And if the Bridgewater report is anything close to right, Greg is being an optimist, which is not his normal milieu. Now, do I think worldwide credit will shrink $12 trillion, as Evans-Pritchard suggests? (Note, that was not a suggestion or conclusion by Bridgewater.) Not in my worst nightmares. Capital will be raised, and the various central banks of the world will do what is necessary to give banks the time to work through their problems.

But in the meantime, the trend toward lower lending is likely to continue. And lower lending is going to be a huge headwind for an economy that is already struggling.

This week Ben Bernanke suggested that the "temporary" Term Auction Facility might be extended into 2009. Let me suggest that it will be extended into at least 2010 before it is no longer needed. Banks are going to need to be able to take their illiquid paper and convert it into liquid Treasuries against which they can make loans and continue to function.

As I have written for a long time, it is all about buying time. In 1980, every major bank in the US was technically bankrupt, as they all had large amounts of Latin American bonds in their portfolios, at a size far larger than their capitalization. When the Latin American countries started to default, if the Fed had made the banks mark their portfolios to market, it would have been a disaster of biblical proportions. There would have been no American banks left standing. The US economy would have gone into a deep depression.

Instead, with a wink and nod, they let them keep the bad bonds on their books at face value, which they all did. Then in the latter part of the decade, starting with Citibank in 1986 (cue the irony), they began one by one to write off the bad loans, but only when they had enough capital to do so. It took six years (or more) of profits and capital raising to get to where they could deal with the problems without imploding themselves and the economy of the US at the same time.

Today is only different in the details. The Fed and central banks around the world are allowing banks to buy time to work through their problems. There really is no other option. That extra $1.1 trillion that the research by Bridgewater says will have to be written off? You can take it to the bank, pardon the pun, that it will not be written off this quarter. This is going to be an ongoing process that will take several years at a minimum. Just like in 1980, the regulators are going to allow banks to write down their losses as they can, except in the most egregious of circumstances, in which case those banks will be "absorbed," a la Bear Stearns.

Treasury Secretary Paulson said Thursday that no bank is too big to fail. That is for public consumption. The fact is that there are any number of banks that are too big to fail, depending upon (and borrowing from my favorite linguist, Bill Clinton) what your definition of fail is. If by fail you mean that shareholders are wiped out, then he is correct, there is no institution too big to fail. If by fail you mean that the operations and debt obligations will be allowed to collapse, then there are institutions whose collapse would pose major systemic risk to the world markets. They cannot be allowed to collapse.

Take Freddie Mac. Please.

(Cue Henny Youngman) Take Freddie Mac. Please. Its shares are down almost 90%. "Freddie Mac owed $5.2 billion more than its assets were worth in the first quarter, making it insolvent under fair-value accounting rules. The fair value of Fannie Mae [down 78%] assets fell 66 percent to $12.2 billion, data provided by the Washington-based company show, and may be negative next quarter, former St. Louis Federal Reserve President William Poole said." (Bloomberg) Poole asserted that these institutions are essentially on a short path to insolvency.

But in the same story, Senators Schumer and McCain both said Freddie and Fannie would not be allowed to fail. Even curmudgeonly former Fed Vice-Chairman Wayne Angell (someone whom I sincerely respect), said on CNBC yesterday that the government regulator of the GSEs (Government Sponsored Enterprises) ought to get some money from Congress to buy preferred stock and then get even larger amounts from the public through an offering of preferred stock. He said that Congress ought to learn about its responsibilities with regard to a GSE; and the public ought to realize that we are in for a long, tough fight. (He also expects the second half of 2008 to be no better than the first half, and he sees 1% growth in 2009.)

I wrote the above paragraph, and a few I deleted below, on Thursday, as I am on a plane to Las Vegas and need to finish the letter in order to attend a conference. I wrote with suggestions about how a collapse of the two Government Sponsored Enterprises might be handled. Last night, the New York Times broke a story that government officials are looking at how to go about taking over operations at Freddie and Fannie, should worse come to worst. Then this morning, the Wall Street Journal in its lead story elaborated on this theme.

The basic problem is that both Fannie and Freddie need more capital, and perhaps far more than their current market capitalization. Where to find it? What investor wants to try and catch this falling safe, without government guarantees? The Journal article quotes numerous people with various ideas about what to do. Most of their ideas will potentially cost US taxpayers.

And make no mistake. The problems with Fannie and Freddie have to be solved. They are now doing 80% of the mortgages in the US. Without them the housing market would grind to a halt quickly and housing prices would drop even beyond Gary Shilling's pessimistic views.

Not to mention that the world has assumed the implicit backing of the government in buying the paper of Freddie and Fannie. How easy would it be to finance US debt if this paper was allowed to default? The implications are serious. I understand the arguments for allowing them to fail, and I think shareholders should bear the risk they take on when buying equity.

A very reasonable idea was broached by Steve Forbes on a BizRadio program this afternoon, which Dan Frishberg graciously allowed me to co-host. He suggests breaking Fannie and Freddie into eight smaller companies, giving them whatever backing they need in the form of public financing to start business, and then cut them off to sink or swim on their own, with much tighter capitalization controls. Remember, this is one of the more free-market conservative thinkers.

The authorities are slowly losing control. All they can do is crisis manage. There are no good solutions, only expedient ones. And we must all hope they choose the best among a handful of not particularly pleasing options. Allowing the system to devolve into chaos is not an option. The Fed and whatever administration comes in will do the same as the current group, which is to buy time so that the wounds can heal, and hopefully put in place rules to prevent another such occurrence.

(Sidebar: I will go into greater detail in a later letter, but regulators need to move NOW to create a Credit Default Swaps Exchange. A problem/crisis in that unregulated market is actually a far bigger problem than the current subprime crisis. Why do you think Bear Stearns was not allowed to go into bankruptcy? There are banks that are too big to fail, despite what Paulson says for public consumption.)

There are a lot of conflicting opinions, which you can read at www.bloomberg.com if you care. Some say Fannie and Freddie will have to lose $70 billion before the regulators step in. Poole says they are insolvent now, using fair market accounting methods. I don't know, and neither do 99.9 % of the shareholders. At this point Fannie and Freddie are not an investment, they are a gamble. Sitting here at Caesar's in Vegas, and reading the opinions, makes me think I have better odds at the tables below me.

I hope that when (not if!) taxpayer money is used, it is at market rates and means that shareholders are last in line, if at all, to recoup any money. For those of us who for years have called for tighter regulation and increased capitalization of the GSEs, as well as a clear removal of any government backing, implicit or explicit, being able to say "I told you so" does not feel all that good. Freddie and Fannie cannot be allowed to go out of existence. They are too tightly wound into the core and fiber of the US economy.

What can and should happen is that shareholders bear their losses, taxpayers pick up the bill, and when they are healthy again, as they will be at some point, another public offering should be done to hopefully recoup the losses to taxpayers. Or perhaps an auction with some guarantees to a potential buyer, but a complete removal of implicit government guarantees on future loans, and higher capitalization requirements. There are any numbers of ways to lessen the ultimate cost to the taxpayer.

What I fear is that politicians will use the opportunity to prop up the mortgage markets with taxpayer guarantees and create much larger losses, which could quickly mount into the hundreds of billions if not properly dealt with. A new populist-oriented administration could find this problem on their desk as they take office.

I would not want to own any stock in the financial sector. There is going to be a continual stream of write-offs over the coming year, at a minimum. Yes, some banks are better managed and will avoid the real life-threatening problems. Some will be like JP Morgan and end up with solid assets backed by government guarantees.

But which ones? Do you want to trust the analysts that have been telling you there is value in the financials at each step, all the way down? The management who insists they are in good shape, then raises capital at dilutive prices? The very people who did not see the problems to begin with, telling you that they are now solved?

The "value" that analysts optimistically see in various financial stocks is evaporating with each quarter, as they slowly write down ever more losses. With another potential $1 trillion to be written off or absorbed through earnings from profitable parts of the business, there is more pain to come. Investing in financials today is like trying to catch a falling safe.

The Ugly Muddle Through

Goldman Sachs published a report Thursday in which they suggest the most probable scenario for the next 12 months is GDP growth between -0.25% and 0.25%, or basically zero. Wayne Angell, mentioned above, expects the second half of '08 to be no better than the first half and for GDP growth to be 1%.

In the Bridgewater report mentioned above, they estimate that the net worth of US-based assets is down about 13% since January 2007, a total loss of almost $8 trillion. This is hitting pension plans, corporations, and consumers, making them think twice about planned investments and expenditures.

Earnings estimates are being cut with each passing month. The P/E ratio for the S&P 500 is currently at a sporty 23. Historically, in times of rising inflation, the stock market goes through "multiple compression." That means P/E ratios fall more than earnings. If multiples fell just 20%, back to 18, which is still above long-term trends, the market would see another 20% drop from here. Even with earnings growth, the market is going to have a challenge rising in the current environment.

Sidebar: A number of you have written questioning my source for the P/E ratio, as you read or hear different numbers from what I write. You can indeed find estimates of forward P/E ratios as low as 12 a year from now. That is a lot different than the 23 I cited above.

There are two basic types of earnings that are reported. One is "operating earnings," or what I call EBBS, or Earnings Before Bad Stuff. Then there is "reported earnings," which is what the corporations report on their tax forms. Not all that long ago, in the mid-'90s, operating earnings and reported earnings were generally in line with each other. Companies would deduct genuine one-time, unusual losses from their reported earnings to give us operating earnings. And such a system has a valid basis for existence. If something is truly one-time, maybe an investor should overlook it when evaluating the company's potential.

But then the media and analysts started using the operating earnings as the primary number, and companies began to game the system. More and more items were considered one-time. One of the more egregious examples was when Waste Management Systems declared that painting the garbage trucks was a one-time extraordinary expenditure and should be accounted as such. Today the difference between as-reported and operating earnings can be 20-40% or more! It seems there are many losses that management assures us are just one-time items.

Standard and Poor's has a web page where you can see a spreadsheet of historical data and projections for both types of earnings. That is the source of my data. It is at http://www2.standardandpoors. com.

Analysts' estimates do tend to get brighter the further out one looks on the table. But if the growth scenarios mentioned above come about, and banks have to curtail all sorts of lending, the earnings projections are going to be way too high, as they have been for the last 12 months. That is going to mean more pain for the stock market.

I think it is quite likely we see the Dow slip below 11,000. (Ok, I wrote that Thursday!) As I said on Kudlow the other night, another 10% drop in the market would take us only to the average bear market. A "9 handle" on the Dow seems quite possible, if not likely. (Note: when someone says "a 9 handle," they mean that the first number in the index or stock price is a 9. The first number is the handle.) The risk is to the downside, given the tepid potential growth of the economy.

Once Again, the BLS Numbers Paint a False Picture

I almost get tired of writing this each month, but it is important, and I will do it quickly. The unemployment number from the BLS last week showed a loss of 62,000 jobs. Private sector jobs were off by 91,000, with the government showing growth of 29,000.

But once again, the birth/death ratio of estimated new jobs was 177,000. As The Liscio Report noted: "... without the b/d's contribution, private employment would have been down by something like 268,000. It added 29,000 [new jobs] to construction, 22,000 to professional and business services, and 86,000 to leisure and hospitality. Given the weakness of the economy and the crunchiness of credit, we doubt that there are enough startups around to match these imputations."

Revisions to the prior two months were a negative 52,000. When they do the final numbers a few years from now, we will find that the revisions will be in the hundreds of thousands for the first half of the year. We have now had five consecutive months of downward revisions, which is typical of recessions.

Unemployment held steady at 5.5%, but that masks an underlying and growing problem. There has been a huge increase in the number of people working "part-time for economic reasons" and a large number of people who are discouraged and not looking for a job but would like one. These two categories are not counted as unemployed. If you add them into the equation, the unemployment or underemployment number goes to 10.3%! (per Greg Weldon)

As I warned above, this has not made for pleasant reading. But it is reality, and we need to deal with it.

And let me say that even given the above, I am a long-term (and even mid-term) optimist. We have to work through some serious problems, but we will. Valuations are going to be low once again, and it will be time to become bullish. And researching and writing my book on how the world will change in 20 years makes me very optimistic. No one in 20 years will think of today as the "good old days." The changes that are in front of us will be amazing. So, simply take a deep breath, be conservative today, and get ready for a really wild and fun ride.

And speaking of investment banks, I need an introduction to someone who is deeply involved in the creation of Exchange-Traded Notes. Drop me a line.

Las Vegas, Maine, and a Wedding

I am at Freedom Fest in Las Vegas, and want to hit the send button so I can attend the sessions and see a lot of old friends. I really think it will be good fun. I have dinner with Frank Holmes of US Global tonight, and look forward to it. Frank is the consummate gentleman and always very interesting.

And speaking of dinner, I was with Barry Ritholtz (of Big Picture fame) last week, and we agreed we are psyched about going to Maine at the end of the month for David Kotok's annual fishing extravaganza. Lots of good friends, wine, and conversation - and I will get to collect on at least one of the group bets we made last year predicting markets, etc. And I was way wrong, but everyone else was even more wrong. Go figure. I will tell you all the details after the trip.

Daughter Tiffani's wedding is getting closer. 08-08-08. Less than a month, and a lot of coordination to be done. It is at the point where I am sitting in on meetings. Flowers cost what? Fireworks? Credit lines are being squeezed. But it is going to be so much fun!

Remember, the markets are not where you live. If your investments keep you up at night, sell until you can sleep. Life is to be enjoyed, and I am doing my part. So have fun this week! And call some friends and share a few laughs.

Your wishing he could be a bull analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.