Stock Markets Heading for Price Earnings Reversion Below the Mean

Stock-Markets / Stock Market Valuations Aug 09, 2008 - 06:18 AM GMTBy: John_Mauldin

The Rise of A New Asset Class, Part 2

The Rise of A New Asset Class, Part 2 - Unrealistic Expectations

- The Boomers Break the Deal

- A Nation of Wal-Mart Greeters

Last week's letter was the first part of a speech I have been giving on what I think will be the rise of a new asset class. This week will be the second and final part. Let me set up this section with a few paragraphs from last week's letter and then a quick summary. If you want to read the entire letter from last week, you can go to the website archives .

But first, a quick note. George Friedman from Stratfor was at my daughter's wedding rehearsal dinner last night. He had just found out about the invasion of South Ossetia by Georgia and was keeping track of the events over his Blackberry from his correspondents on the ground in Georgia.

The media is not particularly excited over the events in Ossetia and Georgia, and the markets seem indifferent. It's much more important than it looks. This the first time since the fall of Communism that the Russians have directly and openly intervened in the former Soviet Union under the claim, made by Dmitri Medvedev, that Russia is the guarantor of security in the Caucasus. That's what the Russian Prime Minister Putin also said. Russia has claimed a sphere of influence in the Caucasus. And that is of historical importance. (Think Monroe Doctrine.)

This is payback for Kosovo. Putin didn't want an independent Kosovo and was ignored with contempt. Payback is an independent Ossetia, with Russian military intervention guaranteeing it. If it's good enough for the Americans and Europeans, it's good for the Russians too. Why the Georgians invaded Ossettia is opaque. For some reason they felt they had to move. The Russians were clearly ready and by dawn had armored formations in South Ossettia and air strikes in Georgia. (The Russian army is about 40 times the size of Georgia, and far better equipped.)

The question on the table now is whether the Russians will stop there or are going into Georgia proper. US embassy personnel are being evacuated - at least some of them - so the US takes this seriously. The US has no military options at this point. We've been talking about the window of opportunity Iraq has created by diverting US forces. Well, the Russians just climbed through the window.

The important thing to watch isn't the US or Europe. It is what the states of the former Soviet Union do, from the Baltics to Ukraine to Kazakhstan. The Russians have announced that there is a new sheriff in town, and this does not apply only to Georgia. These countries hear the message - the foreign minister of Lithuania went to Georgia this morning. All of them are calculating what this means for them in the future. And you need to be thinking about world energy, grain, and other primary commodity markets if Russia dominates the FSU and starts to manage everyone's commodity production and sales. While Georgia has little oil or gas, the pipelines from Russia go through there.

Ossetia is a province (country?) of 70,000. Normally, one would think these events were of little importance. But if Russia is making a statement of a new policy and intends to rebuild the former empire in at least a de facto manner? The US has training troops and personnel in Georgia. They are quite pro-American. While the world focuses on the Olympics, the real show may be in the Caucasus. Let's hope cool heads prevail. It is interesting to note that Bush and Putin were meeting in Beijing over this topic. I wonder what Bush will see when he stares into Putin's soul this time.

I asked and George agreed to establish a free page on his web site for the next few weeks, which they will update periodically on the situation there. This is something we should monitor. The link is http://www.stratfor.com/ analysis/intelligence_ guidance_conflict_south_ ossetia This is one of the reasons why I read Friedman and Stratfor. No major news media had eyes on the ground when the trouble broke out. George did. In an interesting twist, the Russian news media is quoting Stratfor as a source. The world is truly strange. And now on to my speech.

The Rise of A New Asset Class

I think we're at a watershed moment, what Peter Bernstein defines as an "epochal event," with the very order of the investment world changing as it did in 1929, in 1950, in 1981, where a number of things came together - it wasn't just one thing but a number of events happening that conspired to change the nature of what worked in the investment world for the next period of time. It took most people a decade after 1981-2 to recognize that we were in a different period, because we make our future expectations out of past experience. It's very hard for us to recognize a watershed moment in the process. We're going to look back in five or ten years and go, "Wow, things changed." As we will see, it's going to be a change that's going to cost people in their portfolios and in their retirement habits.

We're going to look at a number of different concepts and separate ideas that in and of themselves don't make that much difference. But I think their confluence in the present moment is going to change things.

Last week I pointed out that we are in:

- A Muddle Through Economy for at least another 18 months, caused by

- the bursting of the housing bubble

- and the concurrent onset of the credit crisis, neither of which will really respond to a lower Fed funds rate, but simply have to be worked through.

- This situation will lead to reduced growth (or even contraction) in consumer spending, which we are seeing now, from lower mortgage equity withdrawals, higher energy costs, rising unemployment, inflation in an environment of lower real income growth, and less availability of cheap and easy credit.

- I went into a detailed analysis of earnings, showing that corporate earnings are likely to continue to drop precipitously, which will eventually weigh upon the stock market. Price to earnings ratios are mean reverting over long cycles, and there is no reason to expect that not to be the case in the future. This will be a drag on long-term growth in US stock portfolios.

Let me offer one chart (courtesy of Vitaliy Katsenelson) from last week on this last topic, which illustrates the problem, and then we will jump into the final part of the speech. The current situation is worse than the chart depicts, because on Wednesday of this week the as-reported 12-month P/E ratio for the S&P 500 was 22.87 through the end of the second quarter. We have a LONG ways to go to revert to the mean. The only way for that to happen is for earnings to rise or for stock prices to fall, or some combination of both. Otherwise, you have to suggest we are in an era of permanently and significantly higher stock valuations. (Remember, these cycles last an average of 17 years. We are only 8 years into this one.)

Unrealistic Expectations

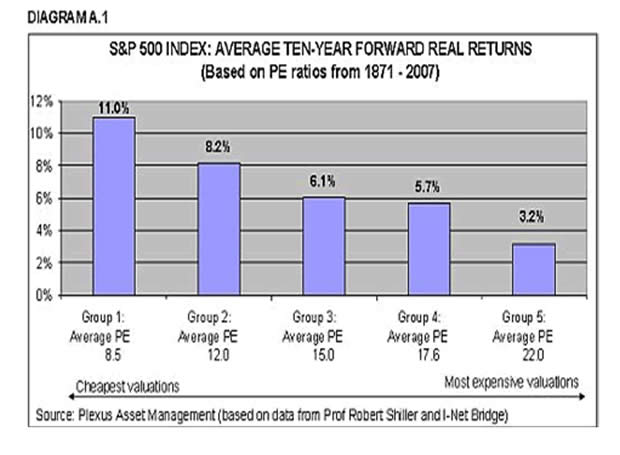

Valuations are important. They are the key to long-term returns. Your expected returns in any one 10-year period highly correlate with where you start investing. If you start when stocks are cheapest, you're going to compound at about 11 percent. But if you start when they're the most expensive, at an average PE of 22, you're going to compound at about 3.2 percent over the next 10 years. For the people and the pension funds that are expecting to get the 8 or 9 percent that they've got written into their returns in their equity portfolios, that's not good news. The following chart from my friends at Plexus illustrates the point. I should note that this calculation works not just on US stocks but in every market that I have seen studied. This is a fundamental principle of investing.

So, what we have is a situation where many aging Baby Boomers and the pension funds and insurance companies which are investing on their behalf are not likely to be able to get the returns they need in order to meet their obligations from traditional US equity holdings.

The Boomers Break the Deal

Now, let's jump to another subject. Boomers (and that would be me and most of the people in this room) are going to break the deal our fathers and grandfathers made with our kids: that we would die in an actuarially and statistically definable timeframe. Without being able to know how large populations will "shuffle off this mortal coil," things like planning for Social Security and Medicare, insurance, and pension plans become a very dicey business.

And the news we Boomers have for our kids and the actuaries who actually care about these things? We're not going to die on time. We're going to live longer, and this is going to have consequences for everyone's investment portfolios. We're not going to get into why we're going to live longer; the simple answer is that medicine is advancing. The boomers are going to live, on average, about 10 years longer than they statistically should; my kids and those under 40 are going to live, on average, a lot longer. But that is a topic for another speech.

Simple fact: the majority of Boomers don't have enough savings. Numerous studies show they haven't saved enough to be able to retire. They certainly haven't saved enough if they're going to want to live longer and take advantage of medicine to do that.

If we start living longer, there are going to be massive problems with pensions and annuities, because there are actuarial tables that say people are going to die along this timeline. If all of a sudden - and over a ten- or fifteen-year period would be all of a sudden from an actuarial or pension fund point of view-people start living longer, it's going to mean that those who pay will run out of money sooner rather than later. Since they will notice the problem long before they get to the end of the money, they will have to make adjustments. That means they are either going to have to lower pension payments, or they're going to have to get more money from somewhere (either increased contributions or increased returns).

Now, if they're in a period where they're projecting 8-percent returns from their equity funds, and they're not getting 8 percent - if they're only getting a long-term 4 to 6 percent from here over the next ten or fifteen years - that's a big problem in funding. Public pension funds have the same problem, but it is much worse. They're a couple of trillion dollars underfunded. This is why you're seeing California cities beginning to declare bankruptcy, because they're having to tell their firemen and policemen, "We can't pay you what we agreed to pay you; let's renegotiate something." It's going to get ugly in a lot of cities. For those of you who live here in San Diego, it's a huge problem. Politicians promised the police and fire and the city people all sorts of wonderful things, they got their votes, and they are not going to have to be there to deal with the problem when it becomes a crisis in a few years. Isn't politics wonderful? Promise anything for votes today and let our kids pay for it tomorrow.

The problems that we're projecting for Social Security and the underfunding today are massively understated. We're going to have to pay a lot more for Social Security than we expected, because we're going to live longer. And the younger generation isn't going to be real happy about having to pay a lot more money to older people who are living longer and don't want to (or can't) go back to work. When they started Social Security, retirement was at 65 and the average person died at 66. There wasn't a lot of expected payout. Now people who make it to 65 will on average live well into their 80s and are soon going to live well into their 90s. This is going to create generational issues.

It will also demand an increase in taxes. It's coming guys, and you are the target. You've got a big target right on your wallet. Like in California: "If you're making over a million, we want to take an extra one percent" - that's going to happen in so many states.

A Nation of Wal-Mart Greeters

Now, let's look at it from another angle. Let's say you're getting ready to retire, you're 65, and you put your money into the most aggressive portfolio you can that historically has given the best returns - that's the stock market - and you're going to take 5 percent out a year. That seems a reasonable number. A lot of people say, "We can take 5 percent of our money out every year." What would happen? Well, remember that graph I just showed you? Depending on the P/E ratio when you retired, if you started out when stocks were the 25 percent most expensive, over 50 percent of the time you'd run out of money in an average of about 21 years. Look at the table below from my good friend Ed Easterling of Crestmont Research.

Even if you started when stocks were the 25 percent least expensive, you would run out of money before the end of your remaining 30 years about 1 out of 20 times. If I came to you and said, "You know, you got a medical problem and we're going to have to have an operation tomorrow. And oh, by the way, you've got a 5 percent chance of dying," you would probably be quite nervous. What I'm telling you now is, if you get too aggressive with your retirement and investment assumptions in a Muddle Through World, especially at the beginning, you're going to end up with problems. We could end up with a nation of Wal-Mart greeters. (Not that there is anything wrong with those happy people who greet me! It is just not the retirement many people plan for.)

But many in the Boomer generation that is getting ready to retire have not made adequate plans and are assuming very optimistic future returns. So are their pension plans. You're going to be living with neighbors and friends who have this problem. And not just neighbors and friends but voters looking for someone to solve their financial problems with your tax dollars.

The Wealth of Nations

Now, let's look at the next topic: the wealth of nations. From 1981 to 2006, our national wealth in terms of the houses we own, stocks we own, real estate, bonds, businesses - everything - our national wealth (or maybe it's better to say, the prices we put on our assets) grew from $10 trillion to $57 trillion. Over very long periods of time national wealth is by definition a mean-reversion machine. Over 40 or 50 years national wealth has to revert to the growth in nominal GDP. That's just the way the economics and the math work out.

Basically, the principle is that trees cannot grow to the sky. Just as total corporate profits cannot grow faster than the overall economy over long periods of time, neither can national wealth. Think of Japan. At one point in 1989, relatively small areas of Tokyo were worth more than the total real estate of California. And then the bubble burst and Japanese national wealth decreased and grew much less than GDP and is now in line with the long-term nominal growth of GDP.

In the US, long-term growth of nominal GDP is about 5.5 percent. We've actually grown by 7.2 percent for the last 25 years. To revert to the mean means that over the next 15 years, maybe more if we're lucky, we're going to see nominal wealth grow between 2.5 and 3 percent. That's a major headwind and a major dislocation from the experience that we've had. Investors have been expecting to get the past 25 years to repeat themselves. The laws of economics suggest that cannot be the case.

We have seen a monster growth in equities in terms of total market cap, even given the flat growth of the last ten years. We all know about the housing market.

Remember the part above where we talked about stock market valuations being mean reverting? We are watching housing values come down. What we are going to see is a very difficult period for asset growth in precisely the two areas where investors tend to concentrate their portfolios: US stocks and housing. Using history as our guide, that period could last for another 5-7 years.

Let me hasten to add that I am not suggesting that the stock market will not go up over the next seven years. What I am suggesting is that we could be in a period like 1974 through 1982 where the stock market did indeed go up over those eight years (in fits and starts), but profits went up even faster. Thus, P/E ratios were in single digits by 1982.

Let's begin to put all this together. What are the requirements of retirement, whether for individuals or pension funds? I think I made the case that traditional investments are going to underperform - that's the stock markets of all the developed countries and to some degree the emerging markets.

But, you've got to have income and savings if you want to retire. You can't throw caution to the winds and invest in the most risky and volatile assets in hopes of getting the returns you need. Hope is not a strategy. You do not want to take much risk with retirement assets, which will be hard to replace.

You've got to figure out, "How do I get income in an era of low interest and low CD rates?" And, "How do I convert my savings, and what do I put them in that will give me that income?" If you're a pension fund, if you're expecting 8 percent from your equity portfolios and you're only getting 2 to 3, at some point you're going to get nervous. You're going to realize you've got to do something else. Same thing with insurance companies and annuities. That means there's going to be a drive for more absolute-return-type funds. The problem is, the place to go for reliable absolute returns is smaller funds. But most large pension funds are trying to put one or five or ten billion to work, not a few million. And if everybody tries to get in the water at the same time, the pond could get very crowded.

Now, full circle. This is where I think the credit crisis is going to come to the rescue. I think we're having a reverse-Minsky moment. Hyman Minksy said that stability breeds instability. The longer something is stable, the more instability there is when that moment of instability happens. The crisis period of instability is called a Minsky moment. So we had a long period of time of remarkable stability in the credit markets, then there were a few cracks here and there, and now we're having the crisis which started in July of 2007. The losses in both housing values and bonds will be in the trillions of dollars. Why? Because stability creates an environment for people to feel safer taking on more risk and leverage. It's just part of human nature. Note: This is not just an American disease. It has happened since the Medes were trading with the Persians and in every corner of the earth.

But now I think we will get kind of a reverse of this pattern, a reverse-Minsky moment, where instability will breed stability, because we as investors, we as human beings, don't like instability; and we'll do whatever it takes and whatever we need to do to demand a return to a stable investment environment.

So, two forces that I have touched on in this speech are going to come together. First, we have destroyed - we've vaporized - 60 percent of the buyers for the structured credit market and badly wounded the survivors. We've got to create something to substitute for that, as we need a smoothly functioning debt market to allow for growth and a healthy business environment. It is absolutely necessary for individuals to have access to credit for purchases. If we all had to go to cash, it would be a disaster of biblical proportions.

Second, there is a need for equity-like returns on the part of investors of all sizes, from the smallest to the largest pension funds. If you can't get 8-10% from equities over the next ten years, where do you turn?

I think what we're going to end up creating, and what we're already beginning to see happen, is going to grow into a huge wave: we're going to see the creation of a series of absolute-return funds that I think of as private credit funds. I don't really want to call them hedge funds, because they're not really hedging anything.

For all intents and purposes they're going to look like banks. They're going to put their green eyeshades on, and when they loan you money, they're actually going to expect it to come back. And they're going to expect it to come back with a level of risk return commensurate with the level of risk they're taking. Instead of going through the messy business of getting depositors to put money into accounts, depositors who can come in and out, and having to service them and let them write checks and all of that stuff, they're going to go to investors and say, "Give me $100 million or $200 million or $500 million, and I can attack this market and give out loans in this manner, and I can generate these returns - 8 percent, 9 percent, 12 percent."

Maybe some of these markets we can lever up two or three times. Two or three times leverage sometimes sounds like a lot. But our average commercial bank is leveraged 10 times. Our investment banks are leveraged 25 times or more. Two to three times in a properly structured debt portfolio isn't a lot of leverage, but it can give you high single-digit or low double-digit, relatively stable returns.

These private credit funds will look like private equity, in that they will have long lock-up periods, so that the duration of the investment somewhat matches the duration of the loans made. It is the mismatch of duration that has created much of the problem in the current market. All sorts of investment vehicles like SIVs, CDOs, etc. borrowed short-term money and made long-term investments.

So, we've got demand from two sources. We've got a demand from a retiring generation, from a pension generation, demanding equity-like return, when they can't get equity-like returns from the equity market. We've got a demand for credit funds - we've got to replace the people we've vaporized.

We're going to see the creation, I think, of a multi-trillion-dollar marketplace of people, pensions, and investors looking to be able to attack those credit markets. Initially it will be for large funds and investors, but it will eventually filter down to structures that the average person can get into.

For a lot of us, we're going to see the ability to find stable returns, equity-like returns, show up at our door. And one way to attack this initially may be funds-of-funds, where you can spread your risk over a number of these types of funds and managers. It's going to require somebody to go in and actually analyze the banker who's making the loans to see if he's, you know, a real banker. Because we know we don't want the guys from Wall Street who made the last set of loans running our funds, at least not until they've gone back to school to learn what a loan is.

I know I am leaving a lot to be said, but my time is coming to an end. Let me say in closing that while a broad asset class that I call private credit funds will share some characteristics, the individual funds themselves will be quite different as to what type of credit they provide (housing, commercial real estate, auto, corporate, credit card, student, and a score of other areas), what types of returns they target, who their customers are, and who their investors are.

Further, while private credit will initially compete with banks, I think that at some point banks will see this as an opportunity to return to their recent and very profitable model, which is to originate loans and then sell them off. Properly run, private credit will be good for the managers as well as the investors. And there is no reason that the management cannot be the banks. In some ways, they have an obvious advantage in this market, as it will be easier for them to attract large investors like pension funds and sovereign wealth funds.

This is a new era. We're going to have to shift from thinking that broad-based stock funds are for the long run. Over the last ten years, if you invested in the S&P 500, your net asset value is flat and dividends have badly underperformed inflation. With today's high inflation and lower earnings, that underperformance could last another lengthy period. If your time horizon is 30 years, then maybe you can talk about the long run. But if your time horizon is 5-10 years before retirement, you need to think about your definition of long run.

Now, you can buy individual stocks if you're a great stock picker or find a manager who is rather good at picking stocks. Donald Coxe was talking to us about agriculture, which I agree is in a bull market. There are other types of technologies - I think the biotech world is going to be huge, starting in the next decade. There are going to be places where we can go into specific target areas and make equity-like returns from equities. But I don't think we are going to be able to do it in a cavalier, "I'm going to put my 401(k) into the Vanguard 500" manner and walk away. It's going to be a challenge for your retirement portfolio if you do.

Retirement in today's world is going to take considerably more thought (and funds!) than was traditionally believed. I encourage you to look at your own situation and carefully analyze the assumptions you have made.

Weddings and 08-08-08

The wedding in a few hours has been the occasion for friends from far and near to gather. Most you will not know, but as noted above George and Meredith Friedman and Paul McCulley got to town in time to have a long leisurely lunch with us. Dr. Mike Roizen just called to say he's off the plane. My friend from first grade, Randy Scroggins, and my first business partner, Don Moore, have come in. It now seems there will be 150 people at the wedding. We first thought 75. Oh well, so much for my forecasting ability. It is great to have so many friends from both sides of the aisle here.

It is not just the Olympics that begin on 08-08-08. In about two hours, Tiffani will be saying her wedding vows to Ryan. They picked a most auspicious date, and I trust it will bode well for them.

It is an interesting set of emotions I am dealing with. I am happy for her and Ryan. It is a start of a new chapter in their lives, and in mine. They are talking about kids, and are committed to making me a grandfather, if Henry and Angel don't beat them to it. (With seven kids, I will ultimately have more than my share.) They all grow up so fast. Where did the time go?

My 91-year-old mother is in the hospital and can't come to the wedding. We almost lost her last week, from an infection she apparently caught in the hospital while there for minor surgery. She is fine now, but can't make the wedding. The contrast of old and new, looking back and looking forward, is food for some serious meditation.

The wedding is going to be something special. As anyone who knows Tiffani will attest, she cannot do anything without a serious dash of her own unique flair. Several national TV series have asked about getting options on the video.

I think I mentioned a few weeks ago that there are going to be some serious fireworks at the wedding when we do the formal toasts. Tiffani was most insistent about having fireworks, and they will be choreographed to music. And while we were going over the plans, I met with the man who is directing the fireworks. For a little extra on the side, he threw in some special effects. What Tiffani and Ryan do not know is that when the minister says, "I now pronounce you man and wife," there will be a round of fireworks going off, and when they kiss an even larger display will erupt over their heads. Every woman says they want to see fireworks when they kiss their new husband. Tiffani will. And Dad's eyes may just get a little moist.

It is time to hit the send button and put on my tux. I am not supposed to be late for this one. All the best, and have a great week.

Your getting a tad sentimental analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.