12 Reasons Why I Started Investing in Uranium Stocks

Commodities / Uranium Sep 09, 2017 - 03:20 PM GMTBy: Michal_Matovcik

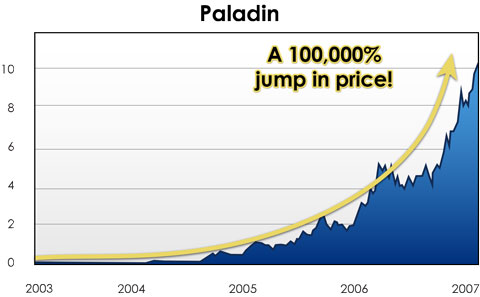

In the 2001–2006 timeframe.. that was easily — and this is a poor pun — the most explosive bull market I have ever seen in my career. I remember there were 5 uranium juniors, 5 companies worldwide where the management teams had a deep enough memory to be able to spell uranium. And over the course of that bull market, the poorest performer of those 5 juniors ran 22:1. The best performer in that market, Paladin Uranium, ran from a bottom of 1 penny to a high of $10. The single oddest experience of my financial career. Rick Rule

In the 2001–2006 timeframe.. that was easily — and this is a poor pun — the most explosive bull market I have ever seen in my career. I remember there were 5 uranium juniors, 5 companies worldwide where the management teams had a deep enough memory to be able to spell uranium. And over the course of that bull market, the poorest performer of those 5 juniors ran 22:1. The best performer in that market, Paladin Uranium, ran from a bottom of 1 penny to a high of $10. The single oddest experience of my financial career. Rick Rule

My story with uranium stocks began in November 2016 as an accidental by-product of the search for my next investment in gold and silver junior mining companies. I was in the process of finding opportunities where I can generate some meaningful wealth in the next 3–5 years period.

Price, supply, and demand are three fundamental aspects defining the immediate potentiality of every single market. In case of uranium, all of them signal major changes and suggest a better long-term outlook even compared to the situation before the beginning of the last bull market in 2001. After a deeper research, I wasn't able to find any other market with better fundamentals where the capitalization of the whole industry is merely 6 billion dollars. Let's look at them one by one.

1. Long term bear markets are the authors of bull markets

Bear markets are the authors of bull markets, just as the spectacular bull market we enjoyed last decade was the author of the bear market that we just suffered.

Rick Rule

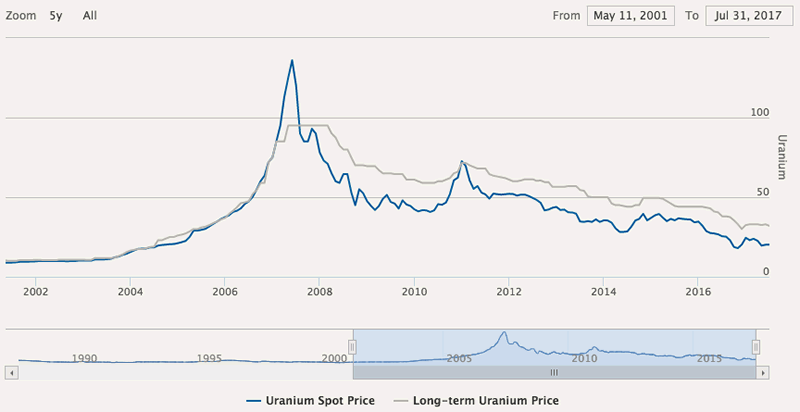

This year uranium celebrates the 10 year anniversary of the bear market where the price of uranium today is 85% below 2007 highs at 137 US$/lb. Uranium equities have suffered even more pain.

The bear market would have probably ended sooner if it had not been for the tragic events in Fukushima. Since 2011 the price fell from $85 a pound all the way down to a low of $18.

Last year the market created a price low at $18 and uranium was able to hold this level for 8 months now.

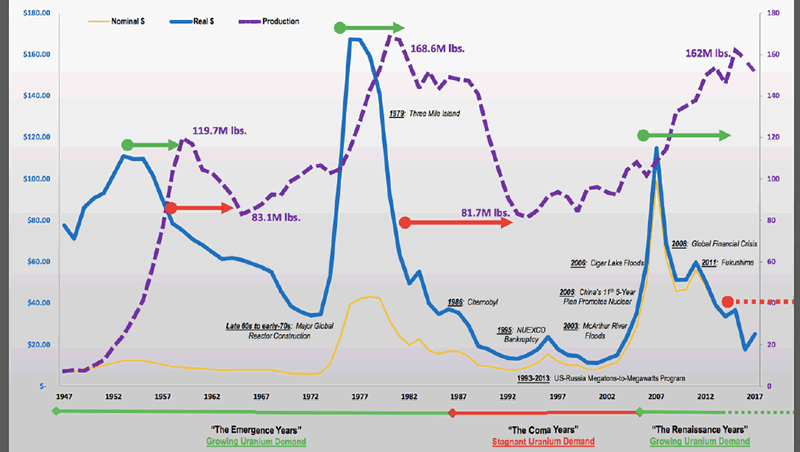

The long-term price chart of historical cycles reminds us that when the bull market in uranium begins one must be there 3 years ahead or you can be too late. Also, it is extremely difficult to jump into the rapid moves upwards. The psychology of entering the market after 100% rise in price is not easy to digest even for a seasoned investor.

2. Demand side is booming

One way to turn around commodities bear market is new demand creation. This is also the most important fundamental factor why I considered any investment in uranium stocks.

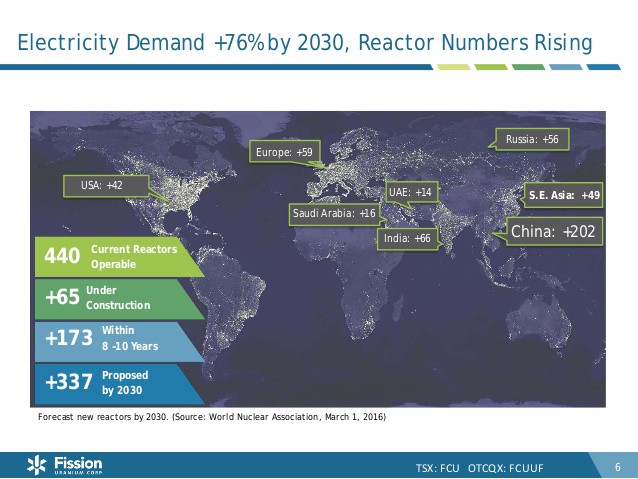

Today there are some 440 nuclear power reactors operating in 31 countries. Nuclear power capacity worldwide is increasing steadily, with over 60 reactors under construction in 15 countries. Most reactors on order or planned are in the Asian region though there are major plans for new units in Russia and significant further capacity is being created by plant upgrading.

Great news for uranium demand are the plans for building 337 new reactors by 2030. This alone should be the very powerful long-term fundament for the next exceptional uranium bull market. For sure the plans are very ambitious and we need to be cautious about the ability of China to execute this plan — White Paper: Prospects for China’s Nuclear Program.

Still, whatever the final number of new reactors will be, the trends are clear. Considering the air pollution problem in China, there will be limited alternatives in providing low-cost fuel for emission free electricity.

There’s only one technology that we know of that supplies carbon-free power at the scale of modern civilization requires, and that is nuclear power.

Ken Caldeira of Stanford University’s Department of Global Ecology

Here you can find the most up-to-date numbers of nuclear reactors worldwide World Nuclear Power Reactor table.

Delayed nuclear restarts in Japan still have crucial impact on demand side

The reality is that today the uranium market is oversupplied and many long time uranium investors admit they were too early to call the beginning of the bull market during 2015–2016. The expectation was that Japan will turn on their reactors at much faster pace.

So today there is approximately 10–12% more supply than demand and we may also not see the impact of Japanese nuclear restarts immediately as they continued to build inventories during the shutdown. Japanese utilities are now holding somewhere between 60–80 million pounds more uranium stockpiles than they need, even if they restart the reactors.

Of Japan’s 48 operable reactors, five units have resumed commercial operation after meeting revised post-Fukushima regulatory standards — Takahama 3 and 4, Ikata 3 and Sendai 1 and 2. Seven reactors have cleared safety examinations under the revised standards, and work towards their restart is progressing.

The timing of uranium price recovery will be a function of Japanese restarts as they accounted for 13% of world uranium demand before Fukushima.

3. Supply side destruction guaranteed at current uranium prices

The crucial news came out of Kazakhstan in January 2017 from the world's biggest uranium producer Kazatomprom with the announcement of 10% production cut due to market oversupply.

Chairman of the Management Board of NAC Kazatomprom JSC Askar Zhumagaliyev, announced today that due to the prolonged restoration in the uranium market, uranium production, planned in the Republic of Kazakhstan for 2017 will be reduced by approximately 10%. The reduction will be over 2,000 tons of uranium (more than 5 million pounds of U3O8) of the planned production of 2017. Overall, this equals 3% of the total world uranium production.

Chairman of the Management Board of Kazatomprom Askar Zhumagaliyev said:

“While the prospects of nuclear energy continue to grow as confidently as it has been for many years, the glut of supply will be the reality of the uranium market in the nearest future. Kazatomprom and its joint venture partners had to make responsible decisions in light of these market challenges. It will be better for our shareholders and stakeholders that these strategic Kazakhstan resources remain in the bowels of the earth for the time being, rather than adding to the current oversupply situation. Uranium will instead be realized under more favorable market conditions in the coming years.”

This was the desired development and strong signal for uranium market. It shows that it is not economically viable to expand production at current uranium prices or to further support the temporary supply glut coming primarily from Japan where the nuclear plants are coming online very slowly.

Currently, no producer on the planet is covering production costs in the low $20/lb range. The International Energy Agency estimates that the global total cost to produce a pound of uranium today is about US$60. So, worldwide, we spend $60 a pound to make uranium and we sell it for $20 a pound.

What this means is that the industry is in liquidation. Why would anybody invest in an industry in liquidation? How much should one pay for the privilege of losing $36 a pound on volume? The reason is, of course, that either the uranium price goes up or the lights go out. Well, uranium is a politically unpalatable source of energy. It’s a widespread source of energy, nonetheless. Responsible at the present time for between 15% and 16% of total US base load demand after 2 decades of very strong investment in a variety of alternatives including wind, solar and natural gas.

While it’s a politically unpopular form of energy, it’s a necessary form of energy. And I would submit to you that within the intermediate term timeframe, that is, the 3- to 5-year timeframe, we have two expectations. One alternative is that the price of uranium goes up to the cost of production or the other is that the lights go out. And my suspicion is that it will be the former rather than the latter.

Source: Rick Rule — Rick Rule on Uranium: Early means wrong, unless..

Inventories

In 2016 utilities were holding globally about 770 million pounds of U3O8, compared to the current annual demand of 174 million pounds. This translates to 4.4 years of demand. However, China is estimated to hold approximately 40% of this inventory given that the country plans to grow its nuclear energy generation from the current 30 gigawatts of electric capacity to 130 GWe by 2030 (and 240 GWe by 2050), according to the World Nuclear Association (WNA).

If we exclude China with their inventory, then the utilities worldwide hold around 2.9 years of inventory what is within the historical inventory levels between 2 and 3 years.

Secondary supply

Primary mine production supplies approximately 86% of current demand. The balance of demand is supplied from secondary sources such as commercial inventories, reprocessing of spent fuel, sales by uranium enrichers and inventories held by governments, in particular, the U.S. Department of Energy. Approximately one-third of the secondary supply is now attributed to Japan shutdown.

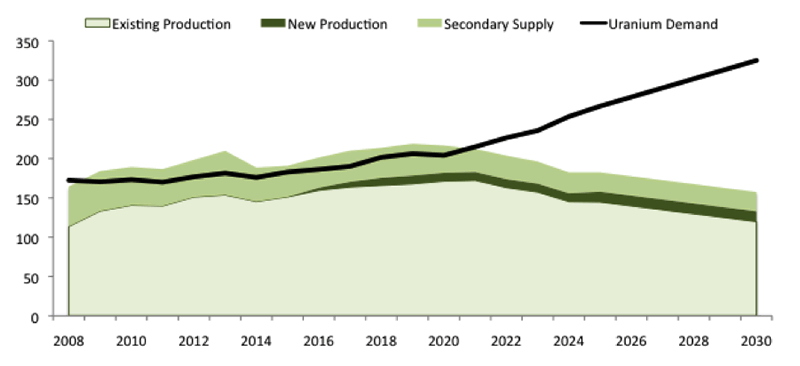

Looking ahead, UxC expects that secondary sources of supply will fall from 2016 levels of 45.9 million pounds U3O8 per year to only 30.7 million pounds U3O8 per year by 2025.

Considering the above-mentioned developments in price, supply, and demand, these are my Top 12 reasons to invest in uranium stocks:

- Uranium market is in a 10-year bear market currently at 85% decline from 2007 highs.

- During the last bull market there were 24 reactors under construction, today there are more than 60. There were also 3 major new mines coming into production, today there are none.

- I believe Japan will continue to restart their nuclear reactors and Fukushima disaster will make nuclear reactors safer going forward. There are some forecast about 18 reactors up and running at the end of 2018.

- No producer on the planet is covering production costs in the low $20/lb range and the industry average for all-in sustaining costs is around $50-$60/lb.

- The price of uranium needs to go up to the cost of production or the lights will go out as producers can't continue with $40 loss per pound of uranium and reactors can't run out of fuel.

- When the market turns, there will be no time for new production expansion as it takes 7–10 years to develop a new uranium project.

- Demand would not be constrained even if prices of uranium skyrocket as the price of producing electricity from a nuclear reactor is completely independent of the price of uranium. The uranium costs as a percentage of the cost of generated electricity in a nuclear reactor are commonly between 3% and 5% of total costs. There is very little demand elasticity even if prices of uranium go north of $100.

- World's biggest uranium producer Kazatomprom started to cut the production because of low uranium prices and oversupply.

- Secondary supply has devastated the market and is now in decline. Japan is coming back online, enrichment underfeeding on the decline, DOE sales reduced. Combined, the Kazakh and U.S. DOE cuts amount to 7.6M lbs of uranium, which is around 5% of uranium production for 2017.

- There is a scarcity of projects that are production ready due to the 6-year bear market in uranium and consequent underinvestment in new production.

- The number of uranium miners went from 500 to 40. Companies with capable management teams probably up to 10.

- Capitalization of all uranium producers combined is so small that even a small shift in money from bubbly stock and bond market can create exponential rise.

While the uranium companies are is still under huge price pressure, the future is starting to look promising, with the main negative factors dissipating in the coming 2–3 years. Coupled with strong demand and limited supply we may be now at the cusp of another rare opportunity to participate in the early stages of the new bull market. Because..

If you hit rock bottom there is only one way to go.

Michal Matovcik

I am a self-taught trader for the past 15 years with the experience of day trading, swing trading and long-term investment in stocks, commodities and currency markets.

© 2017 Michal Matovcik - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.