London House Prices Are Falling – Time to Buckle Up

Housing-Market / UK Housing Oct 10, 2017 - 05:35 PM GMTBy: GoldCore

– London house prices fall in September: first time in eight years

– London house prices fall in September: first time in eight years

– High-end London property fell by 3.2% in year

– House sales down by over a very large one-third

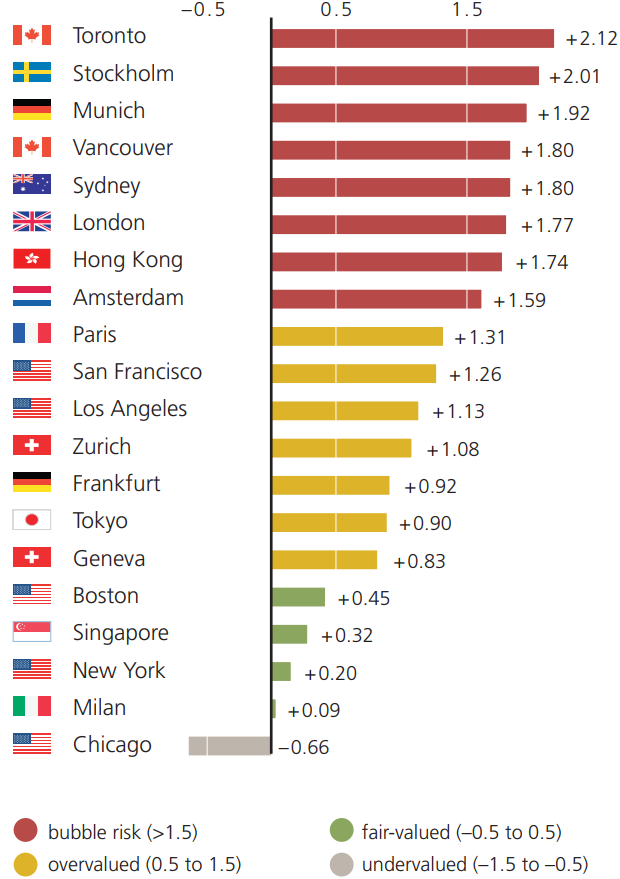

– Global Real Estate Bubble Index – see table

– Brexit, rising inflation and political uncertainty causing many buyers to back away from market

– U.K. housing stock worth record £6.8 trillion, almost 1.5 times value of LSE and more than the value of all the gold in world

– Homeowners and property investors should diversify and invest in gold

Editor Mark O’Byrne

In what might be a sign of things to come, London house prices have fallen for the first time in eight years.

London house sales have fallen by a third as years of frenzied bidding come to a shuddering halt.

The capital remains expensive. Housing still costs 10 times the average salary and only 50% of Londoners own their own homes, the EU average is 70%.

Currently the rest of the UK appears to be benefiting from the lack of affordability and stock in London. Buyers are moving further out of the capital in order to secure their footing on the housing ‘ladder’… no snakes here …

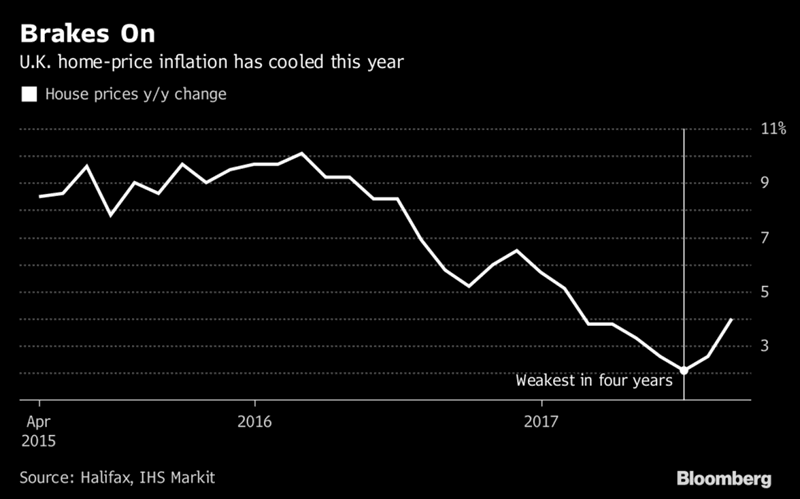

Last month U.K. house prices regained their fastest pace since February. A Halifax house price survey showed a 4% price rise in the three months to September compared with the same period last year.

Long-term, a fall in London prices may be an indicator that concerns over Brexit, inflation and political stability are beginning to affect the U.K property market.

This will be a hard landing for a country that is so convinced that putting all one’s eggs in the housing basket is the answer to securing and growing wealth.

‘Global Real Estate Bubble’

Last month, UBS Wealth Management published its Global Real Estate Bubble Index. London came sixth with a score of 1.77. The group concluded that London is still firmly in bubble-territory.

The research found that London house prices have climbed 15% in the last year and 45% since the financial crisis, when adjusted for inflation.

This suggests September’s fall in prices might be a signal that the top of the market is just behind us. This is no surprise when one considers both the known and unknown events on the horizon for the city.

Brexit is the most discussed threat. Foreign buyers are wary of what the future holds and there is anecdotal evidence that EU workers are being offered shorter contracts. Four years ago foreign buyers accounted for 82% of property purchases.

Brexit is the main stymie of political progress in the country.

Conferences, policy announcement and parliamentary discussions are dominated by how this may or may not play out. No-one knows what will happen, prompting many to feel uncomfortable with making major financial decisions.

This could go on for some time.

Meanwhile the Bank of England are tasked with sorting out the economy. They continue to encourage inflation and plan to raise interest rates. Thus devaluing the value of the pounds in our accounts and increasing the cost of borrowing.

It is not surprising, therefore, that it is not just in London that we are looking at the bursting of the property bubble.

Rest of the UK still climbing…according to some

London, often an indicator for things to come for the rest of the U.K., should be a beacon for the rest of the country’s housing market.

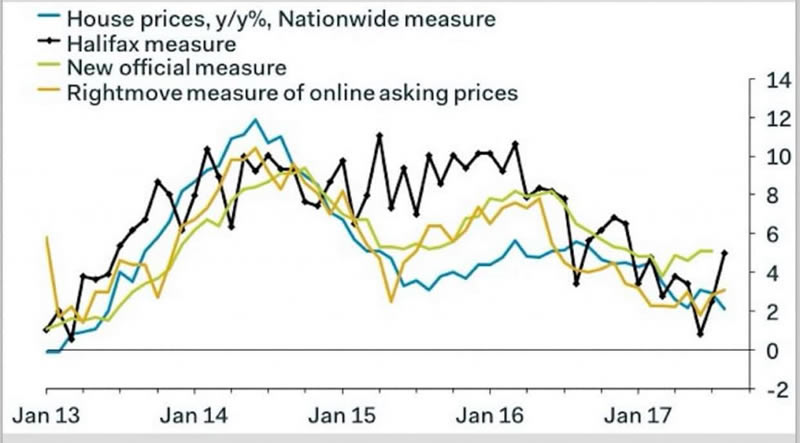

Halifax data shows in September house prices had their fastest annual rise since February. The year-on-year increase jumped a surprisingly large 4%.

Pundits believe this is an indicator that buyers are shrugging off threats of a rate hike by the Bank of England.

Others aren’t so sure. Nationwide’s own home price survey showed more subdued numbers (2%), suggesting there is a slowdown in house prices across the country, particularly in certain regions.

The pace of national price increases has slowed and is down from a peak of 10% in early 2016, to 4% today.

Halifax said future demand might be limited by ‘a squeeze on spending power from higher consumer price inflation and the high cost of property.’ However it does not think that future interest rate price rises would affect the market.

Despite concerns over inflation stretching affordability, mortgage approvals remain at an average pace of almost 67,000 a month, little changed from 2016.

The economist Samuel Tombs of Pantheon Macroeconomics told the Guardian that he thought Halifax was way off the mark.

“Other surveys show that the pipeline of demand is soft; Rics [the Royal Institution of Chartered Surveyors] has reported that new buyer inquiries have fallen in six of the last seven months. Real wages still have further to fall over the next six months and mortgage rates will rise soon in response to the increase in banks’ funding costs.”

Obsession with home ownership

Last week Prime Minister Teresa May referred to the ‘British Dream’. Judging by Twitter few understood what she meant.

If there is such a thing it has to be the desire to own the roof over your head and then sell it at a ridiculous profit.

In the UK this comes at a serious price, but one which few of us question. Often first-time buyers have to rely on family to help, then be comfortable with a 25-year mortgage and restrict their lifestyles well into middle-age.

Ten years later they have to do it all again as a baby’s on the way, house prices are climbing and they want to climb the proverbial ladder.

Failure to do this is seen as just that … a ‘failure’.

To not pursue home ownership in the UK and in Ireland is seen as pretty nuts and irresponsible.

The problem is that in the UK, renting is enough of an incentive to put yourself in such a dire financial situation. It is very different to continental Europe. In the UK and Ireland few leases are long-term and landlords hold the majority of rights. As a result you feel very insecure in your home.

Brits and Irish want to feel financially secure. Ironically they get this security by getting themselves into hundreds of thousands of pounds worth of debt. But the ‘wealth effect’ is so desired and so encouraged by economists, that this level of debt is both expected and accepted.

The British government has encouraged this. For them this is what capitalism is all about. Home ownership and buy-to-let mortgages. But it may run people and perhaps the economy into the ground.

Consider the number of people who subsidise their lives, savings and retirement with the ‘wealth’ they have locked up in their homes. In 2015 older homeowners borrowed £4.2m a day using equity release loans as pensions are no longer covering retirement costs.

We can only expect this to get worse given the looming pension crisis.

Pensioners will be royally scuppered if they find themselves in negative equity, with no pension to support them. Especially so given a considerable number of pension funds and investment bonds rely on UK property to generate income.

Government has a lot to answer for

The country is consistently coming under fire for a lack of housing supply and lack of affordability.

Earlier this week the government announced plans to extend its “Help to Buy” program to 135,000 buyers. The program offers interest-free loans to homebuyers. This will see an extra £6.7 billion pounds ($8.7 billion) of “stimulus” into the market.

Yet another example of leaders trying to unnecessarily stoke a market which results in increased inflation and higher debt levels for a country which is already one of the most indebted.

Currently the UK housing stock is worth nearly £7 trillion, more than the companies listed on the London Stock Exchange and more than the value of all the gold in the world.

The World Gold Council estimates that all the gold ever mined totaled 187,200 tonnes in 2017. At a price of US$1,250 per troy ounce, one tonne of gold has a value of approximately US$40.2 million.

Thus today, all the gold in the world is worth some $7.5 trillion dollars or £5.7 trillion pounds and less than the value of the UK housing stock.

The ridiculous valuation of the London property in particular is thanks to the government, banks and real estate businesses peddling the Greater Fool Theory.

The theory applies here as buyers bought property they thought was expensive but believed they would be able to sell it at a higher price, for significant profit to an ‘even greater fool’.

Falling house prices will make a fool out of everyone, whilst (no doubt) the government continue to make housing ‘affordable’.

Time to Buckle Up With Physical Gold

Housing in the UK is a single asset class but it accounts for two-thirds of the country’s wealth.

There is not a level in society whether government, businesses, banks or individuals that does not have skin in this game.

The figures and economic outlook suggest we need to start diversifying.

The government needs to stop being so irresponsible and no longer constantly peddle arguments for home ownership. However it is difficult politically to sell that story. Especially when all parties have realised the youth vote has major housing concerns and believes they have the right to own property.

Brexit is the main area of concern and no-one wishes to rock the property market any further. Instead homeowners need to consider how they can both protect themselves from falling prices and diversify their investments and wealth.

It is not prudent to have so much wealth caught up in one falling asset. Especially given that it is inevitable that London property will be affected by a number of issues on the horizon including rising interest rates, inflation and Brexit.

Gold is another real asset that millions of investors have placed their faith in over hundreds of years. Like housing, it is tangible. Unlike housing, it does not come with a massive debt burden and it benefits from rising inflation and uncertainties in both political and economic spheres.

Gold Prices (LBMA AM)

10 Oct: USD 1,289.60, GBP 977.77 & EUR 1,094.61 per ounce

09 Oct: USD 1,282.15, GBP 976.23 & EUR 1,092.01 per ounce

06 Oct: USD 1,268.20, GBP 970.43 & EUR 1,083.93 per ounce

05 Oct: USD 1,278.40, GBP 969.28 & EUR 1,086.51 per ounce

04 Oct: USD 1,275.55, GBP 960.87 & EUR 1,085.11 per ounce

03 Oct: USD 1,270.70, GBP 959.00 & EUR 1,081.87 per ounce

02 Oct: USD 1,273.10, GBP 956.48 & EUR 1,084.55 per ounce

Silver Prices (LBMA)

10 Oct: USD 17.12, GBP 12.98 & EUR 14.53 per ounce

09 Oct: USD 16.92, GBP 12.86 & EUR 14.41 per ounce

06 Oct: USD 16.63, GBP 12.73 & EUR 14.20 per ounce

05 Oct: USD 16.66, GBP 12.64 & EUR 14.19 per ounce

04 Oct: USD 16.83, GBP 12.67 & EUR 14.29 per ounce

03 Oct: USD 16.61, GBP 12.53 & EUR 14.13 per ounce

02 Oct: USD 16.58, GBP 12.46 & EUR 14.12 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information containd in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.