Bond Market Bear Creating Gold Bull Market

Commodities / Gold and Silver 2018 Jan 19, 2018 - 05:32 PM GMTBy: Richard_Mills

Gold is climbing as bond yields rise and the dollar falls, over speculation that China is pulling back on buying US Treasuries and Japan signals it is winding down its quantitative easing program. Meanwhile, US debt continues to grow after the Republicans under President Trump pushed a trillion dollars worth of tax cuts through the Senate, that the Congressional Budget Office thinks will add $1.7 trillion to the deficit over the next decade.

Gold is climbing as bond yields rise and the dollar falls, over speculation that China is pulling back on buying US Treasuries and Japan signals it is winding down its quantitative easing program. Meanwhile, US debt continues to grow after the Republicans under President Trump pushed a trillion dollars worth of tax cuts through the Senate, that the Congressional Budget Office thinks will add $1.7 trillion to the deficit over the next decade.

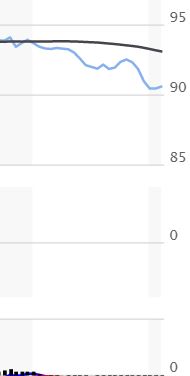

The dollar, 10 year yields and golds price

It’s all good news for gold which thrives on the spectre of high government debt leading to more money-printing (aka the Federal Reserve buying Treasuries) and inflation.

Today’s Federal Debt is $20,493,401,574,964.07.

The amount is the gross outstanding debt issued by the United States Department of the Treasury since 1790 and reported here.

But, it doesn’t include state and local debt.

And, it doesn’t include so-called “agency debt.”

And, it doesn’t include the so-called unfunded liabilities of entitlement programs like Social Security and Medicare.

Federal Debt per person is about $62,805.

usgovernmentdebt.us

Inflation, of course, diminishes the value of the currency and hikes gold prices, since the US dollar and gold normally move in opposite directions.

Gold is seen as a hedge against inflation.

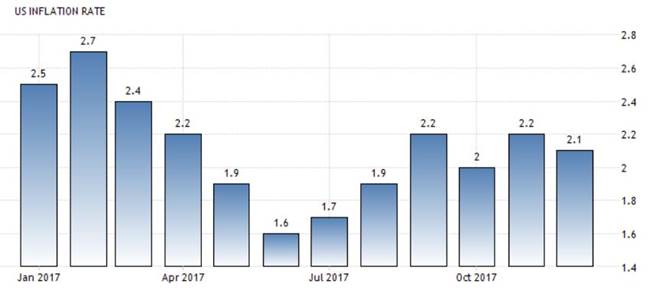

Consumer prices in the United States increased 2.1 percent year-on-year in December of 2017... Figures came below market expectations of 2.2 percent amid a slowdown in gasoline and fuel prices. Still, core inflation edged up to 1.8 percent and the monthly rate increased to 0.3 percent, the highest in eleven months. tradingeconomics.com

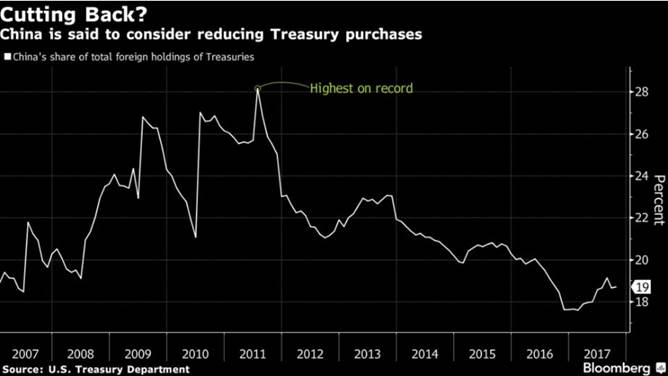

China Treasury purchases in doubt

Last week was very interesting for the bond markets which are a key determinant of the US dollar and therefore gold prices. On Friday, January 12, spot gold hit $1,337.40, having enjoyed a three-day run of $21.40 following an announcement from the Chinese that they could either slow or halt their purchase of US Treasuries. China holds $1.3 trillion worth of US debt, the most of any country.

The Chinese buy Treasuries - effectively lending money to the US government - so that the US can keep buying Chinese goods and China can keep selling their products, earning enough dollars to convert into Chinese yuan to pay workers and suppliers. The People’s Bank of China buys US dollars from exporters, accumulating large forex reserves, and sells them yuan, to keep the dollar higher against the yuan. This gives China a competitive trade advantage.

From November 2016 to November 2017 China’s trade surplus with the US was $416 billion, with the bulk of those earnings in US dollars, South China Morning Post pointed out in an editorial on Monday. Exports rose 10.9% in December.

Whether or not the Chinese follow through (officials later denied the rumour), bond investors got spooked at the prospect of the world’s largest T-bill holder losing faith in US debt, and by extension, the US economy. A large selloff ensued, with the 10-year US Treasury bill hitting its highest yield in 10 months at 2.59% (bond prices and yields are inversely related: when prices drop, yields go up).

The move up was also influenced by the Bank of Japan, which on Jan. 9 trimmed its purchases of Japanese bonds by about $20 billion. The Japanese cutback fueled speculation that the BOJ would end quantitative easing, just as the Federal Reserve did last September; the yen rose immediately by half a percent, as did Japanese bond yields.

Gold-bond yield correlation is weak

While rising bond yields are typically bad for gold, since they increase the opportunity cost of owning gold which pays no income for holding the metal, the present lift in gold prices, even though bond yields are rising, means the correlation is weaker than normal, according to analysts quoted by Kitco.

The head of commodity strategy at TD Securities said that gold is benefiting from uncertainty given that the US dollar is weaker as bond yields push higher.

“This tells me that markets don’t have a lot of confidence in the U.S. at the moment,” [Bart Melek] told Kitco. Vince Lanci, founder of Echobay Partners, said that the fact that gold can rally in a higher bond environment is further proof that the yellow metal has entered a new phase of its bull market. “China buying or not buying Treasuries in the short term is not the big factor… the fact that gold rallied on it means the path of lesser resistance, for now, is up,” he said.

A bear market in bonds

Still, the fact that bond yields are rising is a strong signal to gold investors that: 1/ the demand for US Treasuries is falling and 2/ that the stage is being set for a higher inflationary environment which would mean higher interest rates and increased stock market volatility.

According to a 2017 report from Bank of America Merrill Lynch, when gold prices and bond yields rise in tandem, the stock market tends to move the other way. The report notes both the stock market crashes of 1973 and Black Monday in 1987 were preceded by three quarters of rising bond yields and rising gold. That’s because when both investment vehicles rise, it signals higher inflation, and that leads to rises in interest rates, which are generally bad for stock markets. When stock markets fail, investors turn to more concrete safe havens Ie. gold.

Coupling the current 10-year benchmark Treasury rise, with the fact that a slew of maturing government debt hit the market last week - $32 billion of 10- and 30-year US bonds were sold, along with 4 billion euros of German bonds - “bond King” Bill Gross declared a bear market for bonds. Quotes Bloomberg:

“Bond bear market confirmed,” Gross said in a Twitter posting [last] Tuesday, noting that 25-year trend lines had been broken in five- and 10-year Treasury maturities. The billionaire fund manager at Janus said last year that 10-year yields persistently above 2.4 percent would signal a bear market...

What about inflation?

Bonds tend to sell off when investors believe that more inflation is coming. That’s because the yield gets eaten away by inflation (Eg. you own a 10-year Treasury bill that pays 3%. If inflation is 2%, your real return is only 1%.)

Data last Friday showed that US inflation is now above 2%, with most analysts believing that more rate hikes (an anticipated three more interest rate rises by the Fed this year) have been priced into the inflation rate. Rates could even go higher. In a Wall Street Journal article, Boston Fed President Eric Rosengren said he expected “more than three” rate hikes in 2018 because it wants to get ahead of inflation and not tighten too quickly.

The rise in the two-year Treasury bill - the benchmark Treasury most sensitive to Federal Reserve rate hikes - pushed above 2% last week for the first time since the collapse of Lehman Brothers in 2008, the start of the financial crisis.

The two-year note now provides more income than dividends on the S&P 500 Index. Could this be the harbinger of the next stock market crash?

More debt will hike interest rates, sink the dollar

Meanwhile the elephant in the room is the ballooning US debt. In under a decade, mostly under the Obama Administration, the amount of debt doubled from US$10 trillion to $20 trillion. The chief economist at Goldman Sachs recently revised his deficit projections from below $500 billion in 2018 to over $1 trillion in 2019 due mainly to the Trump tax cuts which will require an additional $200 billion in each of the next four years. How will Congress get the funds? By issuing more Treasuries. Goldman expects net borrowing to go from $488 billion in 2017 to $1.03 trillion this year, and the same amount in 2019. Importantly, under this forecast the debt to GDP ratio rises from 3.7% in 2018 to 5% in 2019, which increases borrower risk. To compensate, and attract T-bill buyers, the Fed is likely to offer higher interest rates. ZeroHedge quotes future Fed chair Jay Powell predicting that is exactly what is going to happen, in a 2012 Fed meeting:

“I think we are actually at a point of encouraging risk-taking, and that should give us pause. Investors really do understand now that we will be there to prevent serious losses. It is not that it is easy for them to make money but that they have every incentive to take more risk, and they are doing so. Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that is our strategy.”

The “big losses” Powell refers to “down the road”, which is actually now, is the extra interest the US government will be forced to pay on its Treasury bills, as the yield curve continues to climb. This will start a vicious cycle that goes something like this: Higher interest rates boost the cost of borrowing for businesses and individuals, thereby slowing the economy. This necessitates more government borrowing, thus pushing up the debt to GDP ratio which makes US T-bills more risky and less attractive to investors. If demand for Treasuries drops, so will the dollar, meaning foreign bond holders get paid in US dollars that are worth less, further slowing demand for them. Finally, as the dollar continues to fall, the US government will have to pay exorbitant amounts of interest on the Treasuries upon maturity, increasing its risk of defaulting on the loans once they become due.

From this brief analysis, it’s easy to see that debt is good for gold. Bullion investors don’t have to worry about the government defaulting on the piece of government debt they own, nor should they be concerned about the value of the currency falling when the T-bill plus interest matures. As long as the gold is in the form of physical metal bullion it’s a safer bet than a T-bill.

Dollar is withering

In a recent post I wrote about how China is hoping to reduce the hegemony of the US dollar, which most commodities are priced in, through the launch of a new oil futures contract. The yuan-denominated oil futures will allow exporters like Russia and Iran to buy and sell their oil through China, thus avoiding US economic sanctions and circumventing the US dollar. Moreover, the yuan will be fully convertible into gold on exchanges in Shanghai and Hong Kong.

This is just the latest move on behalf of China to usurp the economic might of the United States. Between them, Russia and China are moving to kill the dollar. If that ever happens, it will make US-Chinese military conflicts in the South China Sea look like petty squabbles.

At the end of 2015 the Russian Central Bank made the yuan an official reserve currency, and in 2017, the RCB opened its first office in Beijing. The closer cooperation was a result of US sanctions on Russia after the crisis in the Ukraine, and the oil price slump that hit the Russian economy. The two countries have also issued government bonds denominated in each other’s currencies, which are designed to compete with US Treasuries.

Since then trade between Russia and China has been increasing, following in the footsteps of landmark energy deals that have taken place over the last decade. These include the $456 billion gas deal that Russian state-owned Gazprom signed with China in 2014, a $25-billion oil swap agreement Russian oil giant Rosneft signed with Beijing in 2009, and a doubling of oil supplies from Rosneft to China in 2013, valued at $270 billion.

Russia and China are also increasingly sharing technology with possible military applications. The US Congress’ US-China Economic Security and Review Commission reported the export of Russian aerospace technology to China was “challenging US air superiority and posing problems for US, allied, and partner assets in the region.”

Another interesting development is the joint trade in gold between China and Russia. The idea is to create a link between the two gold-trading hubs, Shanghai and Moscow, in order to facilitate more gold transactions.

Quotes ZeroHedge:

“In other words, China and Russia are shifting away from dollar-based trade, to commerce which will eventually be backstopped by gold, or what is gradually emerging as an Eastern gold standard, one shared between Russia and China, and which may one day backstop their respective currencies.”

Sound familiar? What they’re talking about is the kind of monetary system that existed before the 20th century - when banks were constrained in their loans by how much gold was in their vaults. The US went off the gold standard in 1971, thereby severing the linkage between the world’s major currencies and gold. Soon afterward, the US dollar became the leading reserve currency.

Trade conflicts: throwing fuel on the fire

While President Trump under his “Make America Great Again” banner has pressured key trading partners including China, Canada and Mexico, the reality is that passing protectionist measures and ripping up existing trade agreements like NAFTA is likely to depress the dollar - further alienating foreign investors who would otherwise flock to the greenback, and hurting the US economy to boot.

For example during NAFTA negotiations last fall, currency strategist Jens Norvig was asked what would happen should NAFTA fall apart. The result he said would not only be dramatic declines in the values of the Mexican peso and the Canadian dollar, but also appreciation of the yuan and the euro versus the dollar.

“In fact, I think over the medium-term, [euro] and [Chinese yuan] would benefit from the U.S. “America First” policy, as it has to make the [dollar] a less attractive reserve currency,” CNBC quoted Nordvig saying. The benefactor, again, will be gold.

Conclusion

Gold rose 12.5% in value last year, shaking off US rate hikes, the frenzied introduction of bitcoin, and record-setting highs on the Dow and S&P 500 exchanges. While some investors have exited the precious metals space to chase alternative realities, aka the crypto world, gold has been, and will continue to be, a solid investment especially during times of economic and political upheaval when the metal functions as a safe haven.

Are there other basic, more fundamental reasons to buy gold? Well, read this excellent articlefrom Bloomberg, ‘Disastrous' deals sideline gold-mining M&A as metal rises’ posted on Mining.com.

For those who follow economic trends, the latest turbulence in the bond markets is a pretty bullish signal for gold. While there will be daily fluctuations, the short term trend seems to be one of a sustained rally, especially if bond yields continue to rise and the dollar keeps slumping.

The correlation between the bond markets, the dollar and gold is an important determinant of future gold prices. These relationships are something every gold investor should track, to determine ideal entry and extra points for both bullion and gold stocks.

I have bond market trends on my radar screen, and due diligence, which I freely share, on exceptional quality gold exploration juniors on my to do list. Do you?

If not, maybe it should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2018 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.