Seven Key Words That Explain "Stupidly High" Bond Market Prices

Interest-Rates / International Bond Market Aug 23, 2019 - 08:26 AM GMTBy: Dan_Amerman

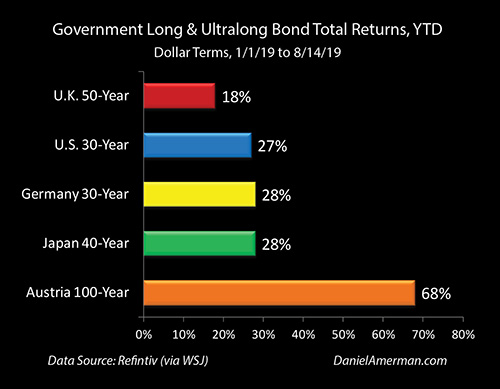

The front page of the August 16th Wall Street Journal contains the information found in the remarkable graph below.

The front page of the August 16th Wall Street Journal contains the information found in the remarkable graph below.

As can be clearly seen, year to date around the world - including in Austria, Japan, Germany, and the U.S. and the U.K. - we are in practice seeing some of the most astonishing short-term returns ever seen when it comes to long and ultralong bonds.

The title of the WSJ article is "Forget Stocks. Ultralong Bonds Are The Real Gamble", and the author refers to the current bond price levels around the world as being "stupidly high". If we look at the dominant investment theories from prior decades, which the great majority of financial planners, financial journalists and retirement investors still treat as being the gospel wisdom for today - then he makes some very strong points about just how ridiculous those prices are, and why they shouldn't exist.

But yet, in reading the article, I couldn't avoid the feeling that I was reading about an admiral planning to send a formation of sailing ships of the line against a fleet of iron-clad dreadnoughts, or a general planning a classic cavalry charge, with trumpets blaring, against trenches defended by barbed wire and machine guns. In each case, the impeccable wisdom that had worked for centuries, would have gone disastrously wrong in a new world, with new rules.

In this analysis we will explore how the world has changed, and why it is that many of the most sophisticated investors in the world have been lining up to pay the "stupidly high" prices, that have created such astonishing profits for them in the real world of 2019 - and the equal or larger profits that may yet still be on the way. There are seven key words that sophisticated investors are focusing upon - but none of them are part of the traditional financial education for individual investors.

This analysis is part of a series of related analyses, which support a book that is in the process of being written. Some key chapters from the book and an overview of the series are linked here.

Article Review

The Wall Street Journal article was by written by James Mackintosh, and is linked here for those with WSJ subscriptions.

"Superlow yields on superlong bonds are everywhere: Germany’s 30-year is at minus 0.22%, Japan’s 40-year at 0.19%, Britain’s 50-year at 0.94% and Austria’s century bond at a mere 1.1%. All yield less than inflation.

These yields can’t be justified on the basis of holding the bonds to maturity. To make sense, investors would have to think both that the world will have extremely low interest rates and no inflation for decades and that governments won’t respond by borrowing and spending. That might be true for a while, but to believe in both lasting without a political upheaval—until 2117 in the case of Austria—is to deny history."

Mr. Mackintosh is absolutely correct - very low long term rates that are either negative or below the rate of inflation make no sense whatsoever from a buy-and-hold perspective. If we assume that prices and yields are determined by knowledgeable investors rationally acting in their own self-interests, then nobody should be stupid enough to buy at those prices.

Just as nobody should be dumb enough to actually deposit money in exchange for a zero percent interest rate, particularly when even low rates of inflation are locking in annual losses in purchasing power. And for most of our lifetimes - the idea that someone could be such a complete imbecile as to actually lock in negative nominal interest rates on their investments would have been dismissed as preposterous by most professional investors, journalists, and academics.

But yet, here we are with about $15+ trillion in global debt trading at negative yields - which is stupid. And we had seven years of zero percent interest rates in the U.S., even while the Fed sought to generate an annual rate of inflation - which is moronic.

Obviously, we can dismiss pretty much the entire last 11 years as not existing, because it would be stupid for them to exist, so they didn't and they don't. With the natural corollary being that we can therefore safely invest our entire life savings on the premise that those years didn't happen because it would have been dumb for that to have happened.

Unless... there were something else moving prices and returns besides the traditional market forces. Because, if there were something else moving prices and changing investor behavior (which brings us back to the Seven Key Words below), then the rational thing to do would be to invest for what was actually changing prices and returns, rather than for a theory that has been contradicted almost continuously by the real world of the last decade and more.

Let's return to the Wall Street Journal article:

"...the scale of the recent rise in long bond prices and decline in yields also smacks of panic. Bonds are being bought because people are again worried about a weakening global economy, the worsening of the trade fight between the U.S. and China, the growing belief that a new Cold War beckons and the failure of central-bank efforts to boost inflation. Political troubles in India, Hong Kong and the U.K. encourage a search for safety, too.

Moves of this scale usually only come when the imagined outcomes are terrible: a U.S. default was in prospect in 2011 and the eurozone really did look like it would blow up its own currency, while in 2008, major banks were failing. You might lose money after inflation on bonds, but equities would fall far more.

Back then, the fears were eventually assuaged when central banks stepped in, and long bonds sold off horribly. This time, the imagined future mostly isn’t so bad—investors are bracing for a recession rather than a complete financial or currency collapse—but the ability of central banks to help appears to be impaired. Interest rates can’t be cut nearly as much as they usually are in a downturn, while global coordination seems unlikely given Donald Trump’s antipathy to China and objections to lower European interest rates."

In other words, the only way to explain what is happening is panic. Rational people wouldn't behave this way. There is no reason to panic (or at least not from the respectable heart of the mainstream). And bond prices will come back to earth as the panic recedes and we return to bond markets where rational buy-and-hold investors demand real rates of return on long-term bonds that are substantially above the rate of inflation, as they did for so many decades (the resulting explosion of the U.S. deficit with higher interest rates and the plunge in stock and real estate values that would result notwithstanding).

Based on the assumption that rational investors rule - that is a good argument.

But it still leaves us with the problem of not being able to explain the last few months or the last 11 years, other than saying "panic", or "stupid" or "irrational" (and by the way, using a decade of inexplicable irrationality to explain away why theories based on an assumption of rationality have been failing in practice... is, well... something worth thinking about).

The Seven Key Words

There are seven key words that are understood by many professional investors around the world right now - but are not at all understood by most individual investors, nor by many commentators without specialized financial backgrounds. The seven key words are "quantitative easing", "maturity extension programs" and "forward guidance".

These have been key to a book that I'm in the process of writing, and I'm only going to very quickly touch on the first five words, with references to some of the previous chapters. Then we will take a close look at the relationship between "forward guidance" and some of the eye-popping profits that have been seen in long and ultralong bonds so far in 2019.

Our starting point is something that I've been writing about for some years now, and which is referenced in the WSJ article: "Interest rates can’t be cut nearly as much as they usually are in a downturn".

Exactly. And the Federal Reserve knows that as well as anyone. The Fed also has some quite public plans (i.e. forward guidance), that could even be called instructions - for those who understand the concepts and the vocabulary - on what they plan to do instead, and where they will steer the profits if there is another round of recession.

In Chapter Thirteen, we reviewed some language from the Federal Open Market Committee minutes (FOMC) about what the Fed staff was planning in the event that another recession caught them while interest rates were too low for the usual containment measures to work.

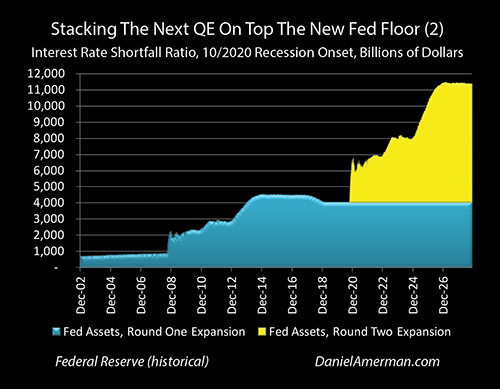

A potentially massive round of "quantitative easing" - creating new money to spend on buying bonds - is a key part of the plan, only this time they plan to do it immediately. In the process, they would stack a new round of massive monetary creation right on top of the last round (as illustrated above).

That is important, but this next part is even more important for understanding the rally that we have seen in long and ultralong bonds in the U.S. (and the related reasons for the moves in other nations). As covered in Chapter Thirteen, the Fed intends to use the money to fund a "maturity extension program". In other words, the Fed doesn't just plan on buying bonds in general, but medium and long term bonds that will extend the average maturity of their portfolio of U.S. Treasury obligations.

Now, I get it: for the average person, this may be sounding very dense and obscure, and of little practical importance for their investment decision making process. But, for someone who understands the vocabulary and concepts, this jargon translates to "money, money and more money".

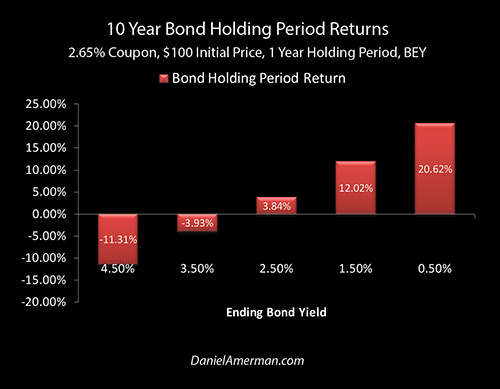

As covered in Chapter Nine and illustrated above, what the Fed would be doing is creating potentially trillions of dollars in new money, in order to buy existing bonds (from someone) at prices so high that it could create the 21% holding period return shown above, for those who owned 10 year U.S. Treasury obligations.

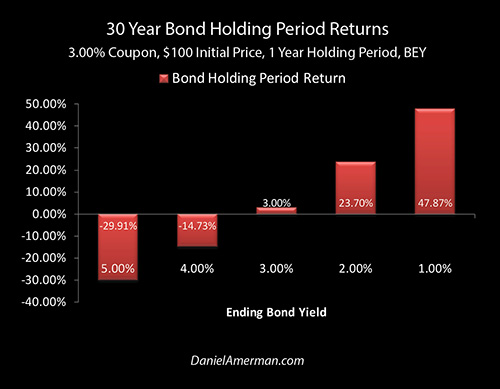

What works for 10 year securities - can work much better for 30 year bonds. With similar assumptions, the combination of quantitative easing and a maturity extension program could produce the 48% one year holding period return illustrated above for a 30 year U.S. Treasury bond owner. (I had published the graph above in an explanatory analysis in March, in advance of much of the rally (link here) - and the 27% return year to date is actually a partial fulfillment of those principles, even as it has moved the starting yield.)

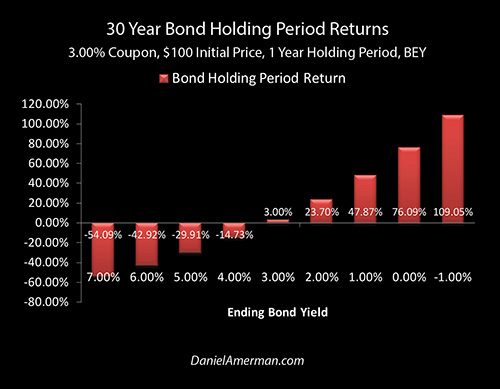

As explored in recent analyses, we also may have an increased chance of negative interest rates in the United States in the not too distant future. Now, this would clearly be a remarkably stupid thing if it were to happen, something that no rational buy-and-hold investor would ever allow to happen within a free market.

But if massive Federal Reserve interventions used trillions in created money to completely distort U.S. Treasury prices, so that our bonds joined the current $15+ trillion in negative interest rate debt in nations whose central banks have already taken the complete irrationality path - then we could see the results illustrated below.

A move to negative interest rates of 1% would more than double the holding period return of a 30 year bond owner, up to 109% in the illustration above (which is from this spring). So, at least for the example of 30 year bonds and negative rates, more than 50 cents on every new dollar created by the Fed using quantitative easing would be going directly to investors as profits on their investment - if they got in early enough. And they would, if the Fed told them far enough in advance - which is one of the most ingenious parts of the plan.

Now, not all of the quantitative easing would go to what is currently the long end for U.S. bonds, and the percentage of QE that would be profits would be less for shorter maturities (shorter durations). However, interestingly enough, according to Bloomberg the U.S. Treasury is currently considering the possibility of issuing ultralong Treasury bonds, perhaps with 50 year and/or 100 year maturities. Such ultralong bonds at current very low interest rates would make even less sense for rational buy-and-hold investors - but they could produce much higher returns than those shown above, for investors who are playing a quite different game.

The Efficiency & Profitability Of Forward Guidance In Practice

The basic idea behind "forward guidance" is that the cheapest and most efficient way for the Federal Reserve to move the markets may not be with actual quantitative easing or actual FOMC interest rate changes, but by just providing guidance, i.e. talking about what they have in mind for the future, with a close eye on what the markets will do today with that information.

That may not sound too impressive - but "forward guidance" can be one of the most powerful tools that the Fed has, and it can be highly effective (particularly when the Fed chairperson stays "on message").

The idea is that for the institutional investors who have extraordinary sums of money under management, they have no desire to "fight" the unleashed Fed of recent years, with its new powers of unlimited monetary creation and recent history of major direct market interventions. Instead, they want to align their interests, so that the large investors make their money by following along with what the Fed has in mind.

In the process of following the guidance of the Fed as a group - these investors change market prices and market yields, sometimes by very large amounts. So, this creates a form of insider loop that can be beneficial for both sides. The Fed gets the ability to use the money of profit seeking institutional investors to move markets - without going to the expense and risk of direct intervention. And if things go as planned, the institutional investors in exchange gain an edge in terms of higher profits at lower risks, than what would exist in a truly free and random market.

(As an aside, there is still risk - there is always still risk of substantial losses, particularly with economic improvements in this particular case - but the outside central banking interventions deliberately driving major price changes produce a non-random skew that creates a non-normal distribution, with a "fat tail" on the profit side that would otherwise not exist, while "thinning" the other tail and reducing the chances of truly major losses. That said, the more irrational the prices, then the greater the size of the second level of "fat tail" - this time with greater losses than should exist with free markets - if the Fed ultimately loses control, and we do return to more rational long term bond yields and valuations. However, that is based on a change in the outside interventions that could trigger catastrophic losses in the stock and real estate markets as well, and not just internal market-driven changes in the bond market.)

For a case study example of how "forward guidance" can work for both sides - just look at what has happened with long and ultralong bond yields in 2019 to date. Let's consider 1) profits; 2) interest rates, 3) the interests of the Fed, 4) the interests of the sophisticated investors; and 5) the seven key words.

Starting with profits - the profits earned by primarily institutional investors have been exceptional and even record setting.

The profits were earned by understanding and following the seven key words, which were the forward guidance given by the Fed that it intends for the first time to initially respond to a recession by engaging in a potentially massive quantitative easing program that would be used to fund a maturity extension program. Piercing through the jargon, the Fed was effectively telling (primarily) institutional investors that if there was a recession, it would create massive sums of money for the express purpose of buying long bonds at the highest prices in history. The longer the maturity (actually the duration), then the bigger the portion of the new money that would go to profits.

That is good to know, and therefore as the chances of recession were seen to be rising fast, that meant that the chances of the record payouts were rising, and hordes of major investors were piling into long bonds.

Indeed, according to the Merrill Lynch survey of fund managers, buying long bonds was the single most crowded trade among fund managers in both June and July of 2019 - much of the market was trying to get a piece of that action. This is what created the yield curve inversion, for the reasons I explained in multiple analyses in 2018. (It is also worth keeping in mind as covered in the previous yield curve inversion analyses, that the professional investors of the bond markets arguably have a far better record of accurately predicting recessions than stock investors.)

So what happened? The markets - following the forward guidance - dropped the rate on 10 year bonds from over 3.20% to under 1.60%, cutting rates in half, but without the Federal Reserve itself spending a dime to buy an additional long bond (other than replacing maturing bonds). The corresponding dramatic reduction in rates for borrowers - and new mortgages - was intended to reduce the chances that the economy went into recession. The forward guidance was remarkably effective at serving the interests of the Fed, and it was the cheapest possible way of doing so.

At the same time, the professional investors who used their money under management to make this happen - don't have to wait on their rewards for a recession. They have already been paid and paid handsomely. Investors who bought 30 year bonds at the beginning of January, had already earned a 27% return by mid-August, just for understanding the guidance and being part of the large group going along for the ride.

Communication is achieved in the open using a specialized vocabulary which only a very small percentage of population fully understands, one hand washes the other, both of the highly sophisticated sides get what they want - and the overwhelming majority of individual investors are left out and on the sidelines, perhaps puzzling over why rational buy-and-hold investors would be panicking and paying such stupidly high prices to lock in such low yields for such a long time?

Closing this knowledge gap is of critical importance, in my opinion. As those of you who have been following my analyses over the last year know (and particularly since I started writing the book), I've been explaining what the vocabulary means, how this trade works, why yield curves invert and where the most of the money is made. I believe individual investors need to understand how the world is actually working when they make important financial decisions, instead of following popular but older theories that can have little relevance with current markets.

Cycles Of Crisis & The Containment Of Crisis

Why are we seeing these extraordinary price movements, and why are they so different from what we have seen in the past?

As developed in my current book in progress, the reason is that we are not in normal times, but are still trapped inside cycles of crisis and the containment of crisis.

1) The Federal Reserve slammed rates down to zero percent for seven years to try to contain and escape the last recession and round of crisis.

2) It was unable to get rates back up to historical levels, without the likely side effect of triggering asset meltdowns in stock and real estate (and bond) markets where prices had become dependent on ultra low interest rates. In other words, it is still stuck inside the cycle of the containment of the last recession, with unnaturally low interest rates.

3) This created a major dilemma for the Fed if there is another recession, since the traditional tools that investors (usually unknowingly) rely upon for economies emerging from recession are unlikely to be adequate, there simply isn't enough room to move short term interest rates downwards. (The situation is much worse for the Bank of Japan and European Central Bank.)

4) For those who understand the vocabulary and the concepts, the Fed is communicating that it intends a grand experiment in the event of another recession, using a combination of what is described in this analysis as being the "seven key words": forward guidance, quantitative easing and maturity extension programs.

5) Nobody knows if this grand experiment will actually work, it has never been tried before. (The WSJ article blithely presumes an ordinary recession, but the reality is much more complicated, there are no prior comparables in the United States.)

6) Whether it ultimately works or not, if the grand experiment is launched by a Fed that is caught in an interest rate trap of its own making, then we will see potentially massive monetary creation being used to fund the purchase of long bonds at historically unprecedented prices - and at levels that will (again) just not make the slightest bit of sense when viewed through the lens of rational buy-and-hold investors determining market prices.

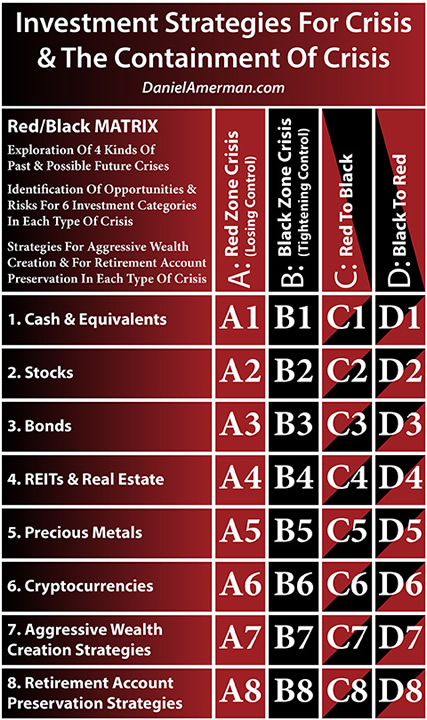

As regular readers know, I use the organizational framework below for exploring how cycles of crisis and the containment of crisis impact all of the major investment categories at the different stages. The Red in the columns is the cycles of crisis, the Black in the columns is the cycles of the containment of crisis. What we have covered in this analysis is how in the event of another Red cycle of crisis, the Fed's plan for a new Black cycle of the containment of crisis could create new and potentially record-setting profits in the #3 row of Bonds.

Information on using the Red/Black matrix framework for better understanding the cycles, the risks, and the profit opportunities, is linked here.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2019 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.