LIBOR Gone Crazy as Commercial Paper Market Implodes

Interest-Rates / Credit Crisis 2008 Oct 04, 2008 - 03:08 PM GMTBy: John_Mauldin

The Curve in the Road

The Curve in the Road - Necessary but Not Sufficient

- Why the Government Had to Step In

- All the King's Horses

- How Can I Be 59?

The "Bailout Plan" was passed. Will it work? The answer depends on what your definition of "work" is. If by work you mean no more government intervention and no further costly programs and a functioning market, then the answer is no. But there are things it will do. This week I try to help you see what might lie ahead around the Curve in the Road. We look at how the rescue plan will function, see what is happening in the economy, and finally muse as to whether Muddle Through is really in our future. It will make for an interesting, if not very upbeat, letter, so strap in. I would like your promise to not shoot the messenger. I am just trying to give you some of my thoughts as to what may lie in our future. And remember, as you read this, we will get through it. There are better days "a'coming."

But first, a few housekeeping items. Let me welcome some 200,000 new readers from EQUITIES Magazine. I have recently joined EQUITIES Magazine as a regular contributing editor. My column, Back to the Frontline, is featured in both their print publication and at equitiesmagazine.com . I am excited to be associated with this esteemed magazine with a rich history covering the global markets for over 57 years.

They've once again agreed to offer any reader of mine a free subscription to EQUITIES Magazine. For those who did not take advantage of the free subscription the first time, here is your chance. You can go to http://www.equitiesmagazine. com/mwi and simply register to get the magazine sent to your home or office. There is also a link to an interview I did in April with them. They have a lot of content and free resources like "live" real-time stock quotes and "live" real-time portfolio managers. Check it out!

Second, a quick commercial. There are managers who are successfully navigating these markets. If you would like to learn more about who they are and how you can put them to work for you, my partners would be delighted to introduce them to you. If you are an accredited investor (generally, net worth of more than $1.5 million), please go to www.accreditedinvestor.ws , register there, and my partners in the US (Altegris Investments) or London (Absolute Return Partners) will show you various alternative investments like hedge funds and commodity funds which might help diversify your portfolio. You really should see what is available behind curtain #3.

And for those with not quite that amount of net worth, I work with CMG in Philadelphia. They have developed a platform of money managers who can take direct accounts, and I recommend that readers interested in outside money management take a look at them. If you would like to talk with Steve Blumenthal and his team about the managers on the platform, simply click on the following link, fill out the form, and they will call you. http://www.cmgfunds.net/ public/mauldin_questionnaire. asp .

(In this regard I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA. And please read all the risk disclosures.) And now, let's jump in to the letter.

The Curve in the Road

When you are out driving on a strange new road, you can't see around the curve ahead. But you can read the warning signs to get an idea of what might be coming. And while we can't really know how the developments in the economic world will actually unfold, there are some signs we can point to that might give us a few ideas.

First, let's look at the "rescue plan" as passed by Congress. As I pointed out last week, this is a bad bill. But it was necessary to pass something, and soon. Earlier this week I sent out a report that reviewed a study of 42 major baking crises. The conclusion: navigating them successfully depended upon quick action.

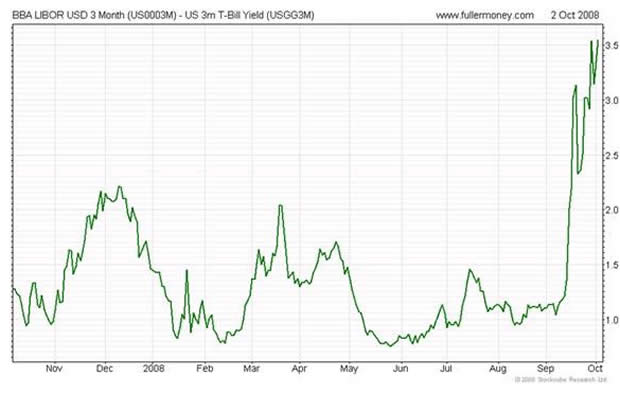

As everyone should know, the credit markets are almost completely frozen. LIBOR is bid only, no offers. Commercial paper markets are imploding. And what is trading is often at rates that are much higher than they were a few months ago. Corporations are being strangled on high rates. Corporations have little or no access to normal credit markets, and they will face massive problems when it comes time for them to roll over short-term debt.

LIBOR has gone crazy. This is not an orderly market.

Look at the following chart from friend Greg Weldon. For most readers, the commercial paper market is something you don't think about. But it is the lifeblood of business. We have seen this market drop by almost 30% in a year and by 10% in just the last three weeks! I simply cannot overstate how serious this is. Left unchecked, business activity in the US would soon slow enough to bring thoughts of the Great Depression. It will not be left unchecked.

The credit crisis is not simply a Wall Street issue. It has fast become a Main Street issue. And Main Street is where jobs are created and maintained.

As I have said repeatedly for months, the problem is that financial institutions are having to deleverage. They have massive losses and simply have to raise capital in order to survive. If you can't raise equity capital (and most can't), one of the ways you do that is to make fewer loans and to take less risk. You also charge more for the loans you do make.

Larger institutions cannot raise capital on competitive terms. GE is an AAA-rated company. Yet they had to pay Warren Buffett 10% to get $5 billion, plus in-the-money warrants worth at least another 10%. Buffett is likely to double his money on this deal over 4-5 years. A short while ago, GE could get short-term commercial paper for a few percentage points. That difference is going to significantly impact GE's bottom line. But they had no real choice. They took the money.

As did Goldman Sachs. Yet another Buffett $5 billion preferred-share purchase (with more warrants) at a rate that even Goldman will find it hard to make money on. But they had to raise capital quickly, and they had little choice.

I had lunch with Michael Lewitt and Joe Harch yesterday. They were in town to meet with a client, and we took the opportunity to get together and share notes. They run (among other things) a collateralized loan obligation fund. They buy bank and corporate debt. They now have the opportunity buy well-collateralized loans from rated companies at prices well below par. They related story after story of debt from quality, highly rated companies selling below $.90 on the dollar, and some much lower.

If GE and Goldman are paying 10%, what do you think it costs a firm with "only" a B rating? 15%? More? Junk bond yields have simply gone ballistic. Firms which used the credit market to access capital now are simply shut out. If they are a small public company, they can go to what are known as PIPE hedge funds (Private Investment in Public Equity) and sell equity at usurious rates (which is what Buffett does but on a larger scale). But a small or medium-sized private company? It is a hard time to go looking for money.

Left alone for the markets to work out, the economy of the US and the world would be in a depression within two quarters and would need years to recover. Think Japan.

Necessary but Not Sufficient

Now for the bad news. The Rescue Plan was necessary but not sufficient to fix the crisis. There is going to have to be more heavy lifting, I am afraid. Let me offer a few ideas about what possible actions might be taken in the future. I am not advocating these actions, I am simply telling you what might happen. These are possible, because authorities will do whatever they deem necessary to avoid a systemic economic meltdown and a potential depression.

If you are a large investor or sovereign wealth fund which put money into banks last year, you are down anywhere from 35-50% (unless you invested in Washington Mutual, and then you are down 100%). You are unlikely to invest more in any financial institution without some very real understanding of what is on the balance sheet of the bank that is asking for your money. What the Paulson plan potentially does do is remove the questionable debt. The bank may have to write down assets in order to sell the debt to the government, but they end up with a transparent balance sheet with hopefully known risks. Then they can go to the market and try and raise capital. Shareholders will get diluted. Such is the way of the world.

Sidebar: taxpayers really must demand that someone like Bill Gross of PIMCO and/or other savvy market specialists run this new government operation. He offered to do it, and I think we should take him up on his offer. Taxpayer losses should be kept to a minimum, and I believe someone like Gross would do his best to see that would be the case. The point of this exercise is to restart the frozen credit markets, NOT to bail out banks. Some banks may get bailed out in the process, but it should be at a cost to their shareholders and management, not to the taxpayer.

I am asked, why can't private money solve the problem? Because there is simply not enough private money. Buffett offered to take 1% of the new government pool. If that is all the largest pile of free money in the world can take, why does anyone think there is enough private capital to take the other 99%? Insuring the mortgage bonds is not sufficient, because there is not enough money to buy them in this market. When things have sorted themselves out in a few years, I think the bonds can be insured and sold, and likely at a profit if bought correctly. But we do not have the luxury of waiting a few years.

Between the relaxation of the mark-to-market rules and removing ambiguously priced loans from financial institutions at prices which allow the government pool to make a small profit, if held for five years, that part (the lack of a known price) of the problem can be solved. Banks can hopefully buy themselves time in which to work their way out of the problems they created.

It is much like 1982, when every major US bank thought it was a good idea to loan lots of money to Latin American countries. It was a most profitable business, right up until the countries decided to default. Then every US bank was more than just technically bankrupt. In a mark-to-market world, every large US bank would have collapsed. It would have been the end of the world as we knew it.

What did they do? The Fed let the banks keep the loans on their books at face value. Over time, they worked their way through the debt, making enough money to be able to write down the loans. That was done simply to give the banks the ability to buy time.

We are in a very similar situation. We have to buy some time in order for financial institutions to heal.

Why the Government Had to Step In

I had a lot of readers write me very nice letters this week, starting out with how much they like my letter, my insights, etc. Then they (mostly - but not all - and politely) launched on me for backing the rescue plan. Many of you had much better ideas than what was passed by Congress, which is not surprising.

I really do hate the idea of having to support a rescue plan. It goes against my every instinct. But I also know that doing nothing would result in an economy which would blow right through 10% unemployment within a few quarters, and take years to recover. The stock markets and the savings of millions of retirees would be wiped out. Home values would really go into a tailspin. Being right in theory is not worth seeing that kind of devastation.

Herbert Hoover sat by and decided to let the market solve the problems of 1929. He decided to run budget surpluses and ignore collapsing institutions. Combined with disastrous Federal Reserve policy (raising rates in a recession) and Smoot Hawley (which caused major trade wars and a slowdown in global trade), what should have been a serious recession turned into the Great Depression and resulted in the conditions for World War II.

The rescue plan does not address the need for the increased levels of capital needed by banks. As noted above, it simply creates the conditions under which capital might be raised. Banks have already raised $440 billion. They have written down $590 billion. Losses are estimated from a mere $1 trillion to as much as $2 trillion. About half of those losses would be in banking institutions worldwide. That means anywhere from $200 to $400 billion more must be raised in order for banks to get back to capital adequacy. It is probably closer to the latter number.

Until banks are adequately capitalized, they are not going to be able to do normal business lending. Further, large deposits are fleeing banks. Even with the new level of $250,000 of FDIC insurance, there is $1.9 trillion in uninsured deposits. These are mostly deposits of small to large businesses and financial institutions, which can leave a bank at the push of a button.

Nouriel Roubini tells us that there are 800 billion dollars deposited in US banks by foreign counterparties. Up until this week, if you were a foreign operation, would you rather be in large money-center US banks or European banks? Tough choice, but on balance you would pick the US. Then this week Ireland decided to simply insure every deposit in Irish banks, no matter the size. Predictably, money started flowing from all over Europe into Ireland. National banks and finance ministers are furious with Ireland.

However, Ireland may have no choice but to backstop its own depository institutions to keep them from losing deposits and becoming insolvent from a bank run by corporations acting in their own best interests. Belgium, The Netherlands, and Luxembourg each took 49% of their respective parts of Fortis Bank in return for a massive injection of capital, declaring the bank too big to fail - also wiping out a lot of already diminished shareholder equity. Europe has its own quite serious problems.

But what if the various countries, one by one, decide to guarantee deposits in order to protect their own banks? If you are an international corporation, especially if you are outside the US, do you want your $10 million in Europe or the US if Europe guarantees your deposits with no limit? Could we see silent runs on US banks?

I think it is about an even chance that the government will have to guarantee for a period of time (say 6 months to a year) every bank deposit, regardless of size, in the US.

That is a staggering thought. The potential will be large for almost-insolvent banks to pursue risky behavior to try and work their way through problems. If such a policy is pursued, tight controls must be administered so risky banks do not offer high CD rates in order to garner assets. The FDIC must closely monitor such activity. Perhaps such guarantees should be for existing depositors and not new customers. Insolvent banks and those on the edge must be shut down quickly in such an event, to prevent risky behavior.

Unthinkable? I bet you there is a working committee of government and Fed officials thinking about just that very thing and how to do it. It would be even more scary if there is not one. We are in completely uncharted waters, and every contingency needs to be thought through well in advance. We simply don't need more last-minute Paulson plans.

In the next few weeks and months, I think you can count on more extraordinary actions by the Fed and Treasury to try and jump-start the credit markets. Actions which were highly improbable a few months ago will be on the table. Will the Fed open its balance sheet to non-banks? Possibly. If they can guarantee money markets, will there be a scheme to insure commercial paper at some price? Not out of the question. Will European governments take more equity in large European banks? Very likely. Will the Fed and/or the Treasury invest even more capital in larger financial institutions? Given that We the People now own 80% of AIG and 100% of Fannie and Freddie, it is certainly within the realm of possibility that we will be the proud owners of even more private institutions.

Again, this is not just a US issue. We will likely see similar actions in Europe and some of the developing world. This is a worldwide crisis, and the response will be from central banks all over the world.

Understand, I am not advocating these actions. I am simply trying to help you understand what actions might be put into place by the various government of the world in an effort to avoid systemic economic collapse.

All The King's Horses

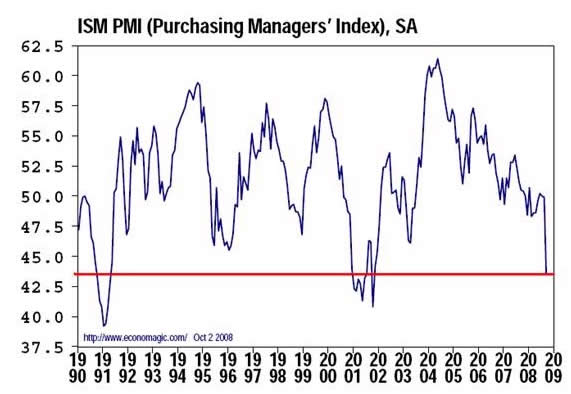

The reality is that the rescue plan does not fundamentally alter the US economic landscape. There can be no doubt we are in a recession. I think it will be dated from the beginning of the year, notwithstanding the odd 2 nd quarter growth. The manufacturing ISM was a dismal 43.5 (under 50 means a contracting US manufacturing industry). Such a level is typically associated with recessions, as the chart below shows. Given the financial crisis and the freefall in auto sales, this index is likely to fall further.

The "good news" is that the service portion of the economy is right at 50, which means that at least that important area is not contracting.

Unemployment rose by 159,000, with nearly every sector affected. Almost 1,000,000 jobs have disappeared over the last 12 months, and it is likely that we will lose another 1,000,000 jobs in the coming year. Since December, the ranks of the unemployed have grown by 1.8 million, and those not in the labor force but wanting a job by 370,000. Almost 3/4 of the increase in the unemployed have been job losers, with half the increase from permanent job losers (not temporary layoffs). (The Liscio Report)

Next week we will explore the economic landscape in detail, but let me provide a few thoughts. As I have said for a long time, we will be talking about deflation this time next year. Recessions are by definition deflationary events. Given that we have had two bubbles burst (housing and credit), there is even more potential for deflationary pressures. Add into the mix the deleveraging process, which will take years to finally abate, and the recent bout of price inflation caused by energy and food will pass, as demand destruction for oil will hold oil prices in check.

As I have said for a long time, the next move of the Fed is likely to be a cut. We are now close to such an action. A 1% Fed funds rate is again a real possibility. I am not sure it will help as much as some market participants think, but I think it likely the Fed will move before the end of the year, if not much sooner.

Europe and Japan are also probably in recession, and it is likely we are going to see a worldwide global slowdown. It would be nice if the European Central Bank, the Bank of England, and the Fed could coordinate a joint rate cut to signal that they are working together on the problems. I would not want to be short the markets that day.

At the beginning of the year, I was predicting a small recession with a lengthy and slow recovery period. I now think that the recession could be deeper than a 1% contraction. I think we could see a rather lengthy recession. Quite simply, the credit crisis has been allowed to spin out of control. That Congress almost failed to act is beyond belief. Given the above circumstances, it is not out of the realm of possibility that a recession lasts through the middle of 2009. As recessions go, that is a long time. But trust me on this, it will pass. The recovery will be a slow Muddle Through affair, though. It will be a few years before we are growing at a sustained 3%. Over the next few weeks, we will look at what that means for earnings and the stock markets. Investors who utilize a traditional 60% stocks, 40% bonds portfolio are not going to be pleased. We will look at alternatives.

Stay tuned.

How Can I Be 59?

This has been a particularly hard letter to write, as I know it is rather gloomy, and I wish had more encouraging news. I have been writing this letter for over eight years. Every letter since the beginning of 2001 is in the archives, so my record is open for inspection. I have no particular axe to grind. Since I basically help investors (in conjunction with my partners) find investment managers and funds, we can adjust the choice of funds and management ideas to suit the times, and frequently do make changes in the mix. My goal in this letter is to help us all think about the economy and our investments and to be as "right" as I possibly can. Sometimes, like today, that means not being very upbeat. But it also means looking for ways to go with the tide rather than against it. I actually hope I am wrong and the bulls are right. But that is not the way I see it tonight.

Tomorrow is my birthday. The years seem to roll by at an ever accelerating pace. (I had the reason this happens explained to me once. When you are 10, a year is 10% of your life. When you are (sigh) 59, it is 1.6% of your life. It makes some sense.) It is hard to believe I am 59. Maybe it is because I am around my kids so much, but I don't feel that old. Seven kids from 31 to 14 (plus assorted spouses and their friends) can do that. And they are all coming to town to celebrate next weekend, so tomorrow will be a quiet day. And Tiffani is already planning for a serious 60 th birthday weekend next year.

Life has been good to me, for all its ups and downs. And I firmly believe that my best years are ahead of me. I am simply having more fun than at any time in my life, with more opportunities than I know what to do with. I am blessed with great business partners. I have the best readers of any analyst anywhere. One million closest friends. I am truly one of the world's wealthiest men when it comes to friends and family, and at the end of the day that is what counts.

Thanks for being part of my life. I plan on writing for a long time, so take care of yourself so you can keep reading. And have a great week!

Your actually optimistic analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.