How to benefit from the big US Infrastructure push

Economics / Infrastructure Jul 21, 2020 - 04:50 PM GMTBy: Richard_Mills

The US economy continues to flounder like an East Coast freighter bashed by a mid-winter Nor-easter.

Fifty million claims is the latest unemployment milestone surpassed by the American workforce during the ongoing coronavirus pandemic that has drubbed the United States worse than any other country including China, where it started.

In a stark contrast of how the two biggest economies have fared, on Wednesday China reported its gross domestic product grew by 2.5% in the second quarter, beating analysts’ expectations and rebounding from a sickly first quarter when the country was assailed by the coronavirus. (Q1 output fell by 6.5%, the first quarterly GDP decline in China since 1992 when official records started being kept)

The news came as lockdowns to contain a second wave of covid-19 eased, and Beijing rolled out stimulus measures to keep its economy growing, including fiscal spending, cutting interest rates and lowering the amount of cash that banks must hold in reserve.

In the United States, a contraction in manufacturing has held back consumption and private investment, two cornerstones of the economy. US GDP in the first quarter fell 4.8%, more than the 3.5% estimated. According to the Atlanta Federal Reserve, economic activity in the second quarter was cut by more than half, with Q2 outlook heading for a 52% drop.

Two of the scariest indicators of an economy in trouble are unemployment, and the rising number of foreclosures and evictions - especially given that federal income supports are due to run out in less than two weeks.

For the week ending on Independence Day, another 1.3 million workers field new unemployment claims, and while that was 7% less than the week before, it brings the national total to 50.2 million out of a workforce of 164.5 million. Over the past five weeks, state unemployment claims totaled 7.25 million, an average of 1.45 million per week.

According to the Mortgage Bankers Association, 8.2% of all mortgages in the US, or 4.1 million loans, are currently in forbearance. In April the share of mortgages past due soared to 3.4%, the highest since 1999. During the 2007-08 housing bust, the rate peaked at 2%.

As Wolf Richter from Wolf Street states, These delinquency rates are the first real impact seen on the housing market by the worst employment crisis in a lifetime, with over 32 million people claiming state or federal unemployment benefits. There is no way – despite rumors to the contrary – that a housing market sails unscathed through that kind of employment crisis.

Fully 30% of Americans didn’t make their housing payments for June, with one-third of the 30% making a partial payment and two-thirds unable to afford any payment at all. During, and shortly after, the 2008 financial crisis, more than 10 million mortgages were foreclosed in the US.

Millions of Americans also face evictions. According to an analysis from UrbanFootprint, a tech company that makes urban planning software, up to 6.7 million households won’t be able to make rent when the extra $600 in weekly UI benefits runs out at the end of July.

In another indication of how bad it is, US banks are bracing for a wave of losses. As Quartz reported on Wednesday, Six of the biggest lenders all expect heavy credit defaults and soured loans, as shown by their loan loss provisions, which jumped 43% from the already hair-raising totals in the first quarter to a combined $36 billion in the second quarter...

If the government doesn’t agree on ways to continue supporting the economy as the initial relief programs expire, “things could start to fall off” for the banks, says David Ellison, a portfolio manager at Hennessy Funds. “And that’s where the banks are saying, ‘If that happens I have to be prepared for it...”

Bank of America’s top executive expects the recession to extend “deep into 2022.”

These are clearly unprecedented times. And unprecedented times call for unprecedented measures. Since the coronavirus crisis hit North America in March, we at AOTH have been calling for a major infrastructure program to kickstart the sputtering US economy.

Something on par with President Roosevelt’s New Deal package of spending measures and so-called progressive legislation that, along with the ramp-up in military spending to handle World War II, helped the United States out of the Great Depression. Given the current state of the US economy, any future infrastructure program may in fact dwarf FDR’s New Deal.

Arguably, a major component should be “clean and green”, including investments in electric vehicle/ charging infrastructure, renewable energies and expansion of 5G/ broadband.

Two roads

There are two directions a national infrastructure program could take. One is spearheaded by Joe Biden, the Democrats’ presumptive nominee to take on Trump in the November presidential election. Biden has just announced a $2 trillion climate plan, seeking to boost clean energy and rebuild infrastructure.

Trump also has infrastructure on his mind, but it would likely be more black and grey than green, focusing on road & bridge replacement, new water/ sewer infrastructure, public buildings, etc., with some funds set aside for 5G wireless infrastructure and rural broadband.

Which one is better? Does Trump’s plan do enough to put America on the runway to a clean-energy, high-tech future? Is Biden’s ‘Build Back Better’ pie-in-the-sky rhetoric with no chance of passing an accounting analysis, let alone a room full of skeptical Republican lawmakers? Is the level of economic growth, and new jobs, likely to outweigh the risk of inflation, and higher debt loads incurred by a second wave of massive fiscal stimulus? How would all this new infrastructure be paid for? And of most interest to us, at AOTH, which metals should we be invested in, to prepare for the inevitable spending spree?

MMT

We are fairly confident that Biden’s plan, explained in detail below, was inspired by the likes of Stephanie Kelton, an economics professor who advised Bernie Sanders’ 2016 presidential campaign. Prof. Kelton is one of the main adherents of “Modern Monetary Theory”.

MMT is a new way of approaching the US federal budget that is unconventional, absurd and out of touch with real world reality. It posits that rather than obsessing about how large the debt has grown (over $26 trillion) and the ongoing annual deficits that fuel debt, we should focus on spending, specifically, how the government can target certain spending programs that will cause minimal inflation. Fiscal policy on steroids is, according to its proponents, to be the new engine of US growth and prosperity.

Government is therefore given a free pass on spending, because the only thing that we have to worry about with the national debt is inflation. Curb inflation and the debt can keep growing, with no consequences. This is because the US government can never run out of money. It just keeps printing money, because dollars are always in demand (with the dollar being the reserve currency, and commodities are traded in dollars).

Among the statements Kelton makes in a video explaining MMT, Kelton says “The US dollar is a simple public monopoly. In other words, the United States currency comes from the United States government.” That means the federal government doesn’t need to “come up with the money” in order to be able to spend. It just prints money and spends it.

From this follows the logical conclusion that deficits don’t really matter; the only thing that matters is inflation. According to Kelton, “The only potential risk with the national debt increasing over time is inflation. To the extent that you don’t believe the US has a long-term inflation problem, then you shouldn’t believe the US has a long-term national debt problem.”

Inflation & money-printing

Inflation really is the screw upon which MMT turns. Kelton also says, via Forbes, that running a deficit is okay as long as it results from spending on valuable items, like infrastructure, education and R&D. In contrast, deficits and debt are harmful when they accrue from unproductive spending.

The opposite argument is put forth by Paul Krugman, economist and New York Times columnist, who represents the current school of thought favored in Washington. Forbes states,

He argues that federal budget deficits always cause harm. They increase the demand for borrowing and so cause interest rates to rise, crowding out private investment in the economy and so slowing growth regardless of the sorts of policies that caused them.

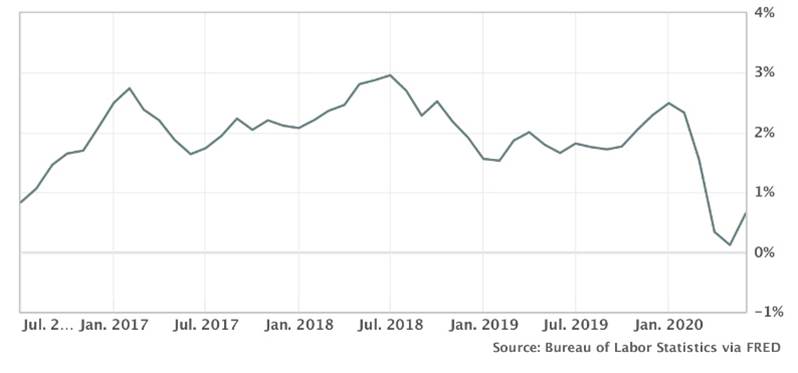

Thankfully, we don’t need to pick a side in a complex economic debate. While the current economic conditions owing to the pandemic have resulted in deflation (falling prices) due to a severe slowdown in industrial activity and consumer spending, which makes up three-quarters of the US economy, we are already seeing inflation creeping into the picture.

In June, the cost of consumer goods and services rose for the first time in four months, led by increases in food and gas prices.

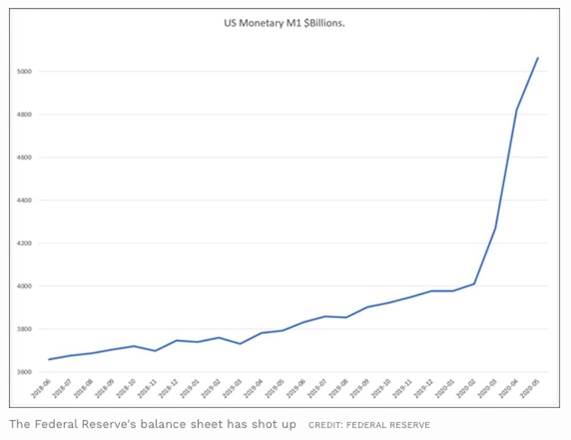

There has also been a huge increase in the money supply - a significant factor in moving the inflation rate. At the end of June, Forbes reported a 33% increase in M1, the most liquid portions of the money supply, in the previous 12 months, or a 105% increase in the last three months to May.

According to Bank of America, via Zero Hedge, the amount of global fiscal and monetary stimulus has already reached an astronomical US$18.4 trillion in 2020, consisting of $10.4 trillion in government spending and $7.9 trillion in central bank asset purchases, “for a grand total of 20.8% of global GDP, injected mostly in just the past 3 months [prior to June]!”

As an example of explosive monetary stimulus via money printing, consider: at the end of 2019, the Fed’s balance sheet as a percentage of GDP was 19%; six months into 2020, it has already doubled, to 39%.

So, the central bank and the US Treasury have already put the economy on a path to further inflation. The way we see it, the government is in a conundrum - it needs to do a major infrastructure program to get people back to work but, paying for it is inflationary. Normally the Treasury could just auction Treasuries (ie. get other countries to take on US debt), but at such low yields, who would buy them? Plus the dollar is falling and will continue to lose value, as long as the country is in the pandemic's grip. Why would trade war opponent, and increasingly military antagonist China, want to increase its $1.3 trillion in US Treasuries when they’ll only be worth $800,000 in a year? The federal government has no choice but to print the money it plans to spend. And it will have trouble stopping the printing presses, as the economy inflates. As Forbes argues in a separate article,

If the Fed thinks it will be allowed to chop the semi-crippled U.S. economy off at the ankles with quantitative easing as inflation strikes, it is going to have a nasty political tussle on its hands. With either side of the aisle in the White House, trying to slam money supply in reverse to stave off a burst of inflation is not going to be politically deliverable with government budgets torn to pieces and with the Federal Reserve likely to be furiously printing to monetize government debt or shove it into proxies.

Summing up, with the US economy’s fortunes tied to exiting the pandemic, which do not look good, given all the false starts and second waves in states that reopened too soon, the only way to get things moving again is to do a major infrastructure program. Paying for it, however, is bound to be inflationary, whether or the economic model followed is MMT, or the dovish monetary policy (printing money, monetizing debt, keeping interest rates low) preferred by the US Federal Reserve, and the Trump White House.

Now the question is, which metals will thrive in the event of a Biden infrastructure push? How about a Trump program to fix American’s crumbling cities? No need to ponder. The answer is gold, silver and copper. Ironically, President Trump is helping Biden to pursue his objectives, should the former Vice President succeed in November.

Trump’s plan

Personally I don’t believe Trump will get re-elected to a second term, but you never know. At least 30 million Americans will vote for “The Donald” no matter what. I just think he’s done such a poor job of managing the pandemic, racial tensions, and the economy - the only thing he had going for him pre-coronavirus - that voters have had enough. I may be wrong.

In any case, Trump has come out with an infrastructure plan that is heavy on reducing bureaucracy, and light on federal spending; in a nutshell, he’d rather have the states and cities pay.

Among a $1.5 trillion investment, the so-called Legislative Outline for Rebuilding Infrastructure in America, the federal government would contribute just $200 billion over 10 years. Accounting firm KPMG encapsulates the plan:

To achieve the goal of US$1.5 trillion in infrastructure investments over the next decade, the bulk of funding to rebuild roads, bridges, waterways, energy projects, rural infrastructure, public lands and other projects would need to come from state and local governments or the private sector.

The new game-plan would significantly alter if not reverse the long-standing Federal public policy of Washington contributing most of the funding needed for national infrastructure priorities, instead requiring states, municipalities and private investment to ante up as never before.

Highlights include $50 billion for rural infrastructure; $20 billion for transportation, drinking water, energy, commercial space and broadband; expanding existing financing programs; putting $10 billion aside for a revolving fund to finance purchases, construction or renovation of federally owned property; and expediting federal permitting by creating a ‘One Agency, One Decision’ approval process.

Environmental reviews and assessments would also be hurried up. Under the National Environmental Policy Act, an environmental impact statement would have to be completed within two years, and one year for an environmental assessment.

The regulation-cutting is interesting, only in the sense that if Biden is elected, for him to successfully implement his $2 trillion clean energy agenda, will require him to also cut red tape and speed environmental permitting which in the US is notoriously slow. Environmental impact statements average over 650 pages, and it takes federal agencies on average four and a half years to conduct required reviews. Environmental impact statements for highway projects take more than seven years, and sometimes up to a decade.

Of course, the Trump administration has already done much to gut the Environmental Protection Agency (EPA), which under Obama was given extended powers to regulate coal-fired power plants. One of Trump’s first acts was to do away with Obama’s Clean Power Plan.

This week Trump officials canceled an Obama-era rule compelling the country’s coal plants to reduce emissions of mercury and other human health hazards. Environmental and health groups, along with Democratic lawmakers, have faulted the administration for rolling back pollution rules for industry in the final months of Trump’s term, as the nation remains fixated on the coronavirus.

Biden’s plan

On Tuesday Biden laid out his plan for jump-starting the stalled-out US economy, through what he called “historic investments” in clean energy.

If elected President, Biden would end power plant carbon emissions by 2035, and spend $2 trillion over four years on clean energy projects. The former Vice President would also hand out cash vouchers allowing citizens to trade in their gas-powered cars for electric vehicles, and steer tens of billions of dollars toward building charging infrastructure in rural communities.

According to Green Tech Media, the ‘Build Back Better’ plan, which includes the power, building and auto sectors, would significantly expand the less than $100 billion that currently goes into clean energy technologies.

Unsurprisingly, the initiatives would be paid for by reversing Trump’s tax cuts - including raising the corporate tax rate from 21 to 28%, and upping taxes on rich Americans. Biden proposes extending clean energy tax credits and installing millions of solar panels, and wind turbines both onshore and offshore, in an attempt to chip away at the nearly two-thirds of US electricity generation that still comes from fossil fuels.

Reaching 100% renewables, a more ambitious target than Biden’s, would require adding about 200,000 miles of high-voltage transmission lines, according to an analysis by Wood Mackenzie. Grid-scale energy storage, shifting major cities towards public transportation, and upgrading 4 million buildings and weatherizing 2 million homes over four years to increase energy efficiency, are also called for under the Biden plan.

Gold & silver

In the current deflationary environment, gold is doing well because of all the other drivers that make it such an attractive investment - a high global debt to GDP ratio from the combination of falling economic growth and rising national debts, owing to massive virus-related stimulus; growth of the M2 money supply lighting a fire under gold prices; continued low interest rates until at least 2022; a steady flow of safe-haven demand, due to numerous global hot spots particularly with regard to a more belligerent China; and social/ economic chaos gripping the United States as it enters a presidential election.

Gold is also poised to gain in the likely event that all of this fiscal and monetary stimulus - at last count totaling $5.2 trillion - leads to inflation (and that is before the infrastructure spending, $1.5 trillion for Trump, $2 trillion for Biden, is unleashed)

If inflation goes, say, above 3%, yet interest rates remain near zero, that would create another bullish condition for gold - negative real rates (interest rates minus inflation). When US Treasury bond yields turn negative, investors typically rotate their funds out of bonds, into gold.

We have the same bullish indicators for silver as for gold, in terms of safe-haven demand inciting investors to park their money in silver bullion, silver ETFs or silver mining stocks, and the fact that silver, like gold, is not subject to inflation like paper currencies.

Silver is interesting in that it has two drivers pushing it higher - investment demand and industrial demand.

Around 60% of silver is directed towards industrial uses like solar panels, electronics, and the automotive industry. 5G is set to become another major silver demand driver.

The white metal therefore stands to benefit from an infrastructure program - either Trump’s or Biden’s - both due to its inflationary impacts, which are bullish for precious metals, and because it is an important metal in building solar power and 5G.

According to the Silver Institute, The electronic components that enable 5G technology will rely strongly on silver to make the global 5G platform perform seamlessly. In a future 5G connected world, silver will be a necessary component in almost all aspects of this technology, resulting in yet another end-use for silver in an already vast and versatile demand portfolio.

The group expects silver demanded by 5G to more than double, from its current ~7.5 million ounces, to around 16Moz by 2025 and as much as 23Moz by 2030, which would represent a 206% increase from current levels.

The solar power industry currently accounts for 13% of silver’s industrial demand. According to a recent report by CRU Consulting, the amount of electricity generated by solar power is expected to increase by 1,053 terawatt hours (TWh) by 2025, which is nearly double what was produced in 2019.

All of that solar will be a major boon for silver.

CRU expects PV manufacturers to consume 888 million ounces of silver between now and 2030. That’s 51.5 million oz more than the combined output from all the world’s silver mines in 2019.

Copper

Copper’s widespread use in construction wiring & piping, and electrical transmission lines, make it a key metal for civil infrastructure renewal.

A report by Roskill forecasts total copper consumption will exceed 43 million tonnes by 2035, driven by population and GDP growth, urbanization and electricity demand.

The global 5G buildout and the continued movement towards electric vehicles - including cars, trucks, vans, construction equipment and trains - are two big copper demand drivers.

Even though 5G is wireless, its deployment involves a lot more fiber and copper cable to connect equipment.

Electric vehicles and associated charging infrastructure may contribute between 3.1 and 4 million tonnes of net growth by 2035, according to Roskill. EVs contain about four times as much copper as regular vehicles. With each charging station using about 2 kg of copper, that’s 42 million tonnes, or double the current amount of copper mined in one year.

Conclusion

As smart resource investors, we want to be invested in metals, and companies, that are at the leading edge of a trend. At AOTH we see gold, silver and copper as THE best metals to own right now, considering the multi-trillion-dollar infrastructure programs being promised by the two presidential candidates.

We agree with them, massive infrastructure spending is necessary to lift the US economy out of recession and back onto a path to growth.

It doesn’t matter whether it’s Trump’s plan or Biden’s plan, both will be hugely inflationary. The rise in food prices and gas prices are just the precursor of what’s to come, when the printing presses start churning out dollars like never before - far surpassing the quantitative easing programs that followed the financial crisis.

Inflation is good for gold and silver. Ditto for debt. The debt to GDP ratio is a reliable indicator of gold prices. The ratio is certain to go higher, as more money is printed, expanding the Fed’s balance sheet, while economic growth continues to be pinned down by the pandemic.

Fiscal and monetary stimulus will have to rise, just to keep people fed, housed and from taking to the streets; to pay the big infrastructure spend planned after the election; and regular spending priorities. It will all be inflationary - great for silver and gold.

Meanwhile, silver and copper are on an upward trajectory and will continue to do well under a Biden or Trump infrastructure push. Clearly, copper with all its green energy applications will be more in demand under Biden’s plan. Same with silver due to its application in solar panels (millions of them under Biden).

It is remarkable to see a bullish case for all three metals, no matter who clinches the presidency in November. Owning gold, silver and copper, or better yet, the companies that are exploring for them and offer the best leverage against rising prices, seems to me a very prudent investing strategy going forward.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector. His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2020 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.