Commodities Comeback

Commodities / Commodities Trading Mar 24, 2021 - 05:32 PM GMTBy: The_Gold_Report

Peter Krauth, editor of Gold Resource Investor, examines the commodity supercycle and the role recency bias plays in investment decisions. Recency bias is a funny thing. It's human nature to expect the near future to look like the recent past.

But we all know that's not how things always play out.

And that can be costly, even dangerous, for investors.

Take long term bonds, for example. Ten-year Treasury yields have more than tripled, from 0.54% to 1.66% since last July. Does that mean the 40-year bond bull market is dead?

Tough to say, or course. We'll only know that for sure with hindsight. You know… recency bias.

If nothing else, the bond market is telling us price inflation is becoming a thing again, notwithstanding what the Fed might be telegraphing.

According to the Consumer Price Index (CPI), the 12-month change in February was 1.7%. And yet, if you use electricity, gasoline, pay rent or even eat, chances are your experience has been quite different.

Energy, real estate, lumber, agriculturals, metals and beyond are all on fire since last March.

Is this the start of a new commodities supercyle? It's certainly looking that way.

Signals Flashing Inflation

Like I said the bond market, for one, is catching serious sniffs of price inflation.

If I had to guess why, stimulus, money-printing, near-zero and negative rates, plus massive pent-up post Covid-19 demand would be top of mind.

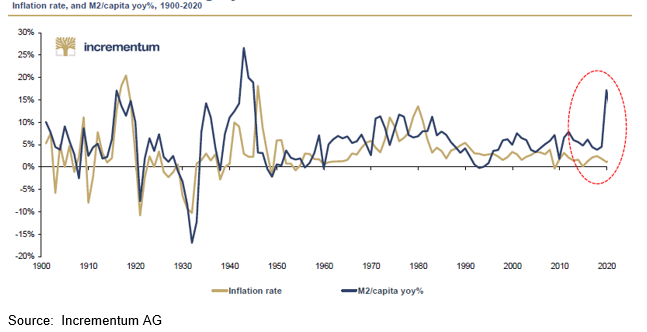

Monetary growth has already far outpaced levels from the 1970s. And we know that inflation follows the money supply, often with a lag.

Money velocity has fallen steadily since the 2008–2009 financial crisis, but it's absolutely plummeted since the start of the pandemic. Is that about to change in a dramatic way? Before you decide, remember recency bias.

Despite low money velocity, a funny thing has happened. Commodities have been soaring along with inflation expectations.

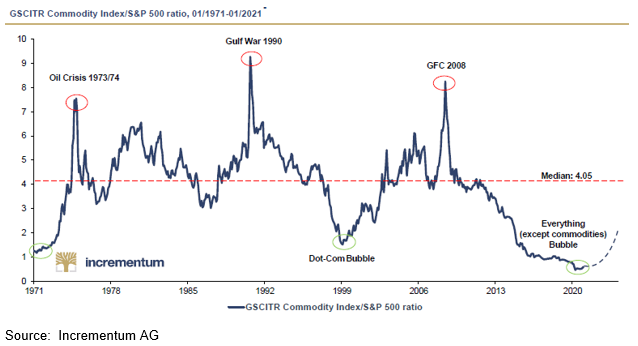

One of the best ways to know where a sector stands in the bigger picture is to compare it to other assets. And looking back over longer periods of time often provides great perspective. That's why I absolutely love this next chart.

Commodities Rising

It's the ratio between the Goldman Sachs Commodity Index and the S&P 500.

Looking back all the way to 1972, commodities have never been cheaper relative to the broad stock market. Never. The average of this ratio is 3.9 over 50 years. Today, it sits near 0.5. But it seems poised to soar.

For commodities just to make it back to their average levels versus stocks, they will need to rise by almost 700%. And remember, that's the overall index, and it's the underlying commodities. Needless to say, some commodities will outperform others. But the companies involved in producing those commodities will do even better as their profits leverage rising revenues.

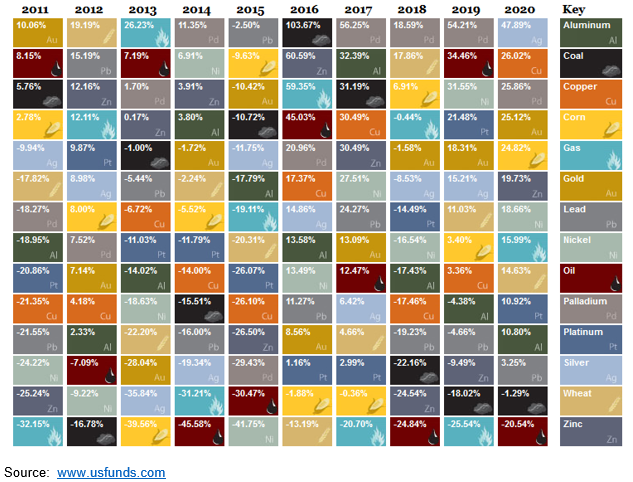

The following table lays out the annual performances of a number of commodities.

As you can see, in 2020 nickel was up 19%, corn gained 25%, while palladium and copper both gained 26%. In a recent 2021 Commodities Outlook: REVing up a structural bull market (Nov. 18, 2020), Goldman Sachs said, "Looking at the 2020s, we believe that similar structural forces to those which drove commodities in the 2000s could be at play."

A commodities supercycle is considered to be a multi-decade trend, where a wide range of basic resources enjoy rising prices thanks to a structural shift in in demand versus supply. Typically, what happens, is that supply stagnates or drops for several years as economic demand is itself weak or constant. However, at one point a new business cycle starts, and demand picks up, while supply is unable to immediately react.

Producing most commodities is a highly capital-intensive endeavor. That means a lot of money to build and ramp up production, not to mention the delays in finding, permitting and building any new projects. Typical delays can be on the order of 10 years or more.

With supply unable to meet growing demand, prices rise. It's Economics 101. So producers of those commodities enjoy higher revenues, and higher profits as their costs remain fixed or rise more slowly than the underlying commodity. And as profits expand, so do their share prices. You have a solid trend for years as supply struggles to catch up to demand. It's a secular bull market.

What's sowing the seeds for a new commodities supercycle? The drivers are numerous, which reinforces the probabilities. First we have a shift. In the above table, 12 of the 14 commodities ranked showed gains last year. In 2019, it was just nine. In 2018, just the top three commodities eked out a gain. Then we have all the usual suspects: near zero interest rates and bond-buying from central banks, massive government spending and deficits, ongoing printing to increase the money supply exponentially, stimulus cheques being given to the majority of the population, huge infrastructure, green energy, and Covid-19 fighting and relief spending. Oh, and possibly a long term bear market in the U.S. dollar, in which commodities are priced. Plus all the pent up demand from people unable to go out and spend due to pandemic restrictions. I believe the large gains in base metals and energy over the past year are the markets sensing that a flood of consumption and inflation are coming our way.

And Goldman Sachs is not alone. Bank of America has also forecast a surge in commodity prices as a result of post-pandemic global economic recovery. JPMorgan said in a recent note that metal, energy and agricultural prices are reaching multi-year highs, signaling a commodity supercycle that may last for several years.

I agree. That's why it's time to position for a new commodities supercyle.

In the Gold Resource Investor newsletter, I provide my outlook on which stocks offer the best prospects as this bull market progresses. I recently added a low-risk commodities royalty company to the portfolio that I believe has exceptional potential to outperform its peers in the next 12 months.

The action in commodities looks and quacks like a duck.

Don't be a victim of recency bias.

--Peter Krauth

Peter Krauth is a former portfolio adviser and a 20-year veteran of the resource market, with special expertise in energy, metals and mining stocks. He has been editor of a widely circulated resource newsletter, and contributed numerous articles to Kitco.com, BNN Bloomberg and the Financial Post. Krauth holds a Master of Business Administration from McGill University and is headquartered in resource-rich Canada.

Disclosure: 1) Peter Krauth: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.