Powell: Inflation Might Not Be Transitory, After All

Economics / Inflation Oct 03, 2021 - 10:03 PM GMTBy: P_Radomski_CFA

At a panel discussion, Fed Chair finally admitted that inflation could be more (!) long-lasting than expected. What does it mean? Hawks. Lots of them.

Capitulation

With Fed Chairman Jerome Powell finally having his ‘come-to-Jesus’ moment on Sep. 29, the central bank chief’s skittish words helped light a fire under the USD Index. For context, I’ve been warning for months that Powell remains materially behind the inflation curve. And with his indecisive speech upending the Fed’s confidence game, the gambit is showing signs of unraveling.

Speaking at an ECB panel discussion on Sep. 29, he said:

“The current inflation spike is really a consequence of supply constraints meeting very strong demand. And that is all associated with the reopening of the economy, which is a process that will have a beginning, middle and an end. It’s very difficult to say how big the effects will be in the meantime or how long they last.”

For context, first it was “base effects,” then it was “transitory” and now “it’s very difficult to say.”

He continued:

“It’s also frustrating to see the bottlenecks and supply chain problems not getting better – in fact, at the margins apparently getting a little bit worse. We see that continuing into next year probably, and holding up inflation longer than we had thought.”

What’s more, Powell actually admitted that the Fed is facing a conundrum that it hasn’t dealt with “for a very long time.”

“Managing through that process over the next couple of years is… going to be very challenging because we have this hypothesis that inflation is going to be transitory. We think that’s right. But we are concerned about underlying inflation expectations remaining stable, as they have so far.”

Wow. If that’s not capitulation, I don’t know what is.

For context, I wrote on Sep. 24:

I’ve warned on several occasions that the only way for the Fed to control inflation is to increase the value of the U.S. dollar and decrease the value of commodities. However, with commodities’ fervor accelerating on Sep. 23 – a day when the USD Index declined – the price action should concern Chairman Jerome Powell. As a result, FOMC participants’ 2022 inflation forecast is likely wishful thinking and they may find that a faster liquidity drain (which is bullish for the U.S. dollar) is their only option to control the pricing pressures.

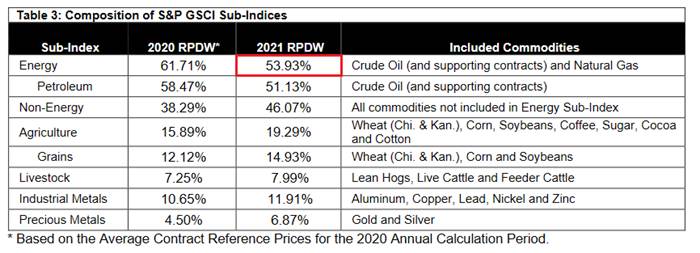

Speaking of which, the S&P Goldman Sachs Commodity Index (S&P GSCI) has rallied by ~5% for the month of September. For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products and two precious metals. However, energy accounts for roughly 54% of the index’s movement.

Please see below:

Source: S&P Global

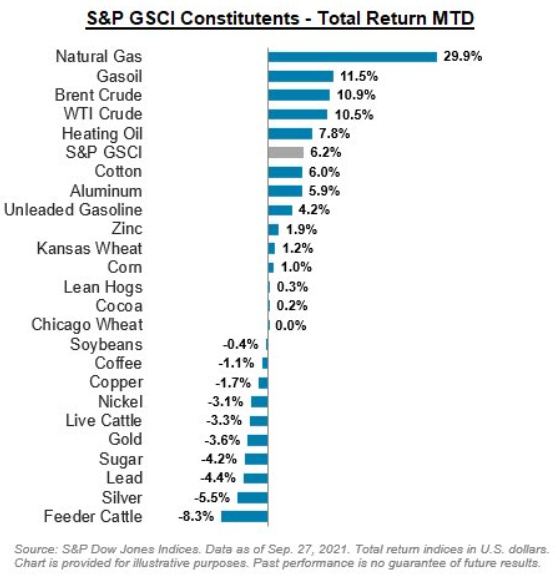

As well, if you analyze the graphic below, you can see the impact that rising energy prices had on the S&P GSCI’s performance in September (MTD returns as of Sep. 27).

To that point, with Brent and WTI surging recently and the latter on track for six straight weeks of weekly gains, Goldman Sachs has upped its year-end Brent target to $90 a barrel. Calling it the “revenge” of the old economy, Jeff Currie, Goldman Sachs global head of commodities research, said that “poor returns saw capital redirected away from the old economy to the new economy. It’s not unique to Europe, it’s not unique to energy, it’s a broad-based old-economy problem.”

Thus, in his view, commodity prices need to be “much higher to get returns sufficient to start attracting capital. People wanted a quick return, and now you’re paying the price for it.”

Please see below:

Supporting the thesis, Bank of America commodities strategist Francisco Blanch told Bloomberg on Sep. 28 that Brent could hit $100 a barrel in 2022 and that a “cold winter” could actually pull forward the forecast.

He said:

“First, there is plenty of pent up mobility demand after an 18 month lockdown. Second, mass transit will lag, boosting private car usage for a prolonged period of time. Third, pre-pandemic studies show more remote work could result in more miles driven, as work-from-home turns into work-from-car. On the supply side, we expect government policy pressure in the U.S. and around the world to curb cap-ex over coming quarters to meet Paris goals. Secondly, investors have become more vocal against energy sector spending for both financial and ESG reasons. Third, judicial pressures are rising to limit carbon dioxide emissions. In short, demand is poised to bounce back and supply may not fully keep up, placing OPEC in control of the oil market in 2022.”

Now, the important point isn’t whether or not Currie and Blanch are correct. The important point is that higher oil prices are mutually exclusive to Powell’s 2% inflation goal. For example, the Commodity Producer Price Index (PPI) – which is a reliable indicator of the next month’s Consumer Price Index (CPI) – recorded its highest monthly year-over-year (YoY) percentage increase in August since 1974. What’s more, the sky-high reading occurred with the S&P GSCI declining by ~2% in August (that’s why monitoring surging container rates is so important). However, as mentioned, the S&P GSCI has already risen by ~5% in September and container rates have also made new highs. As a result, Powell’s hawkish shift isn’t nearly hawkish enough to solve his inflationary dilemma.

Inflation Isn’t Going Anywhere

As further evidence, the Richmond Fed released its Fifth District Survey of Manufacturing Activity on Sep. 28. And while the headline index turned negative as output slumped, pricing pressures remained materially elevated.

Please see below:

Source: Richmond Fed

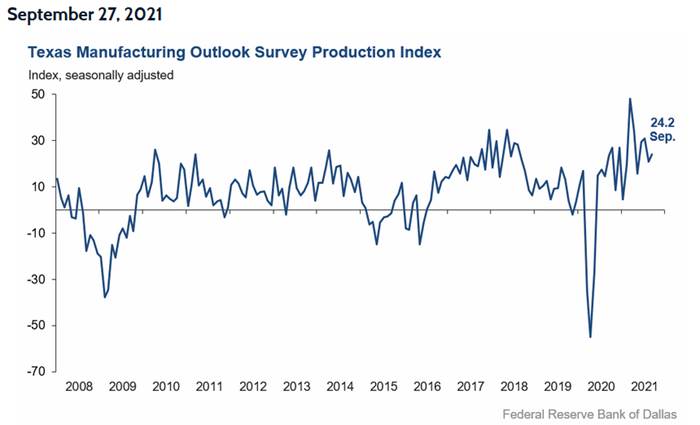

Likewise, the Dallas Fed released its Texas Manufacturing Outlook Survey on Sep. 27. The report revealed:

“Prices and wages continued to increase strongly in September. The price indexes climbed further, with the raw materials prices index at 80.4 and the finished goods prices index at 44.0, an all-time high. The wages and benefits index held steady at a highly elevated reading of 42.7.”

For a visual of the overall index, please see below:

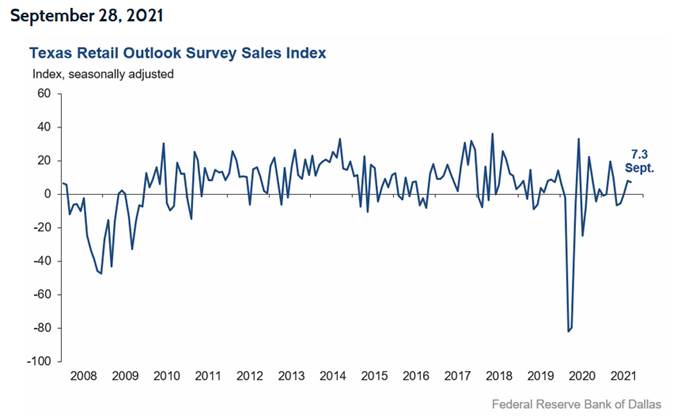

Furthermore, the Dallas Fed also released its Texas Service Sector Outlook Survey and its Texas Retail Outlook Survey on Sep. 28. And though the U.S. service sector has suffered the brunt of the Delta variant’s wrath, pricing pressures remained. The report revealed:

“Wage pressures eased in September, though remained at historically high levels, while price pressures remained highly elevated. The wages and benefits index declined from 32.6 to 26.9. The selling prices index was largely unchanged at 20.2, with nearly a quarter of firms reporting increased prices compared with August, while the input prices index inched up one point to 42.9.”

More importantly, though, the Texas Retail Outlook Survey revealed:

“Retail price pressures surged once again in September after some signs of moderation in August, while wage pressures held steady. The selling prices index surged nearly 11 points to 50.4 – with 58 percent of retailers increasing prices compared with August – while the input prices index increased from 41.3 to 50.1. The wages and benefits index was flat at 24.6.”

For a visual of the overall index, please see below:

And as the drama unfolds and Powell’s inflationary conundrum intensifies, his hawkish rhetoric on Sep. 29 helped sink the EUR/USD. For context, the EUR/USD accounts for nearly 58% of the movement of the USD Index. And with the currency pair collapsing below 1.1600 on Sep. 29 and closing below key 2020 support, the European dam could be about to break.

Please see below:

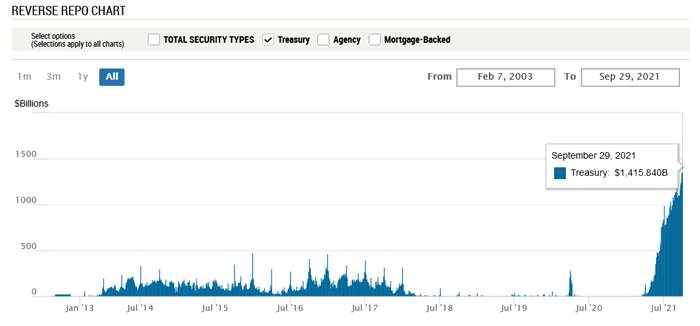

Reverse Repos Hit Another All-Time High!

Also bullish for the U.S. dollar, with Powell’s liquidity circus still on full display, there is too much money floating around with too little use. And upping the ante on what I’ve been highlighting for months, after 80 counterparties drained nearly $1.416 trillion out of the U.S. financial system on Sep. 29, the Fed’s daily reverse repurchase agreements hit another all-time high.

Please see below:

Source: New York Fed

To explain, a reverse repurchase agreement (repo) occurs when an institution offloads cash to the Fed in exchange for a Treasury security (on an overnight or short-term basis). And with U.S. financial institutions currently flooded with excess liquidity, they’re shipping cash to the Fed at an alarming rate. I’ve been warning for months that the activity is the fundamental equivalent of a taper due to the lower supply of U.S. dollars (which is bullish for the USD Index). Thus, while we await a formal announcement from the Fed, the U.S. dollar’s fundamental foundation remains robust.

The bottom line? Powell’s only hope to curb inflation is to strengthen the U.S. dollar and weaken commodity (including gold and silver) prices. For context, major futures contracts are priced in U.S. dollars. And when the dollar rallies, it’s more expensive for foreign buyers (in their currency) to purchase the underlying commodities. As a result, a stronger U.S. dollar often stifles demand. And with the current supply/demand dynamics favoring higher commodity prices, Powell will have to work his magic — strengthen the dollar and reduce demand — if he wants his inflation problem to subside.

In conclusion, gold, silver (ouch) and mining stocks sunk like stones on Sep. 29. And with the USD Index cutting through 94 like a knife through butter, new 2021 lows in the EUR/USD were accompanied by new 2021 highs in the USD Index. Moreover, with the momentum poised to continue, the PMs’ medium-term outlooks remain quite somber. As a result, further weakness will likely materialize before brighter days emerge (probably) near the end of the year.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of today’s all-encompassing Gold & Silver Trading Alert. The latter includes multiple premium details such as the targets for gold and mining stocks that could be reached in the next few weeks. If you’d like to read those premium details, we have good news for you. As soon as you sign up for our free gold newsletter, you’ll get a free 7-day no-obligation trial access to our premium Gold & Silver Trading Alerts. It’s really free – sign up today.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Tools for Effective Gold & Silver Investments - SunshineProfits.com

Tools für Effektives Gold- und Silber-Investment - SunshineProfits.DE

* * * * *

About Sunshine Profits

Sunshine Profits enables anyone to forecast market changes with a level of accuracy that was once only available to closed-door institutions. It provides free trial access to its best investment tools (including lists of best gold stocks and best silver stocks), proprietary gold & silver indicators, buy & sell signals, weekly newsletter, and more. Seeing is believing.

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Przemyslaw Radomski Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.