Why TALF is Bad for America

Politics / Credit Crisis Bailouts Mar 05, 2009 - 01:18 PM GMTBy: Chris_Ciovacco

The recent Term Asset-Backed Securities Loan Facility (TALF) announcements bring to mind Einstein's definition of insanity – “doing the same things over and over again and expecting different results”. It is well documented that securitization of loans, use of leverage, and government intervention in the free markets helped inflate assets bubbles, fostered a culture of debt, and distorted the efficient allocation of limited resources in our economy. If you want a good real world example, Fannie Mae bonds guaranteed by the government, backed by a pool of subprime mortgages, and bought using borrowed money (leverage) touches most of the bases.

The recent Term Asset-Backed Securities Loan Facility (TALF) announcements bring to mind Einstein's definition of insanity – “doing the same things over and over again and expecting different results”. It is well documented that securitization of loans, use of leverage, and government intervention in the free markets helped inflate assets bubbles, fostered a culture of debt, and distorted the efficient allocation of limited resources in our economy. If you want a good real world example, Fannie Mae bonds guaranteed by the government, backed by a pool of subprime mortgages, and bought using borrowed money (leverage) touches most of the bases.

In the past, we have outlined the problems associated with the government guarantees and distortions of the free market. Our government created Fannie and Freddie with the noble goal of helping more people become homeowners. The following is a summary of a September 8, 2008 CCM article Welcome to the Mortgage Business , which highlights the law of unintended consequences:

Mortgages carry risk. If you place a guarantee behind a mortgage-backed security, like Fannie and Freddie bonds, there really is no risk to the investors who keep supplying capital to the mortgage market. As investors supply more capital to the system, more questionable mortgages can be written and builders can keep building more houses. Why is anyone guaranteeing mortgages? Placing a guarantee behind a risk asset creates moral hazards. Why? Because the loan originators do not care if the mortgage holder keeps making their payments since they can sell the mortgage to Fannie and Freddie, who in turn will place a guarantee behind the mortgage.

The guarantee behind Freddie and Fannie bonds were and will continue to be a source of moral hazard. If you remove the guarantee and Fannie and Freddie from the entire system, banks and investors would treat mortgages as risk assets, which is what they are. Instead of propping up Fannie and Freddie with taxpayer funds and guarantees, both firms should be gradually removed from the system. The free market can supply mortgage capital to people who have the necessary debt-to-income ratios and credit history. Loans should be made to people who can pay them back. The current state of the mortgage and housing markets clearly illustrates the results of placing guarantees behind risk assets, which is what Fannie and Freddie do. Fannie and Freddie are part of the problem, not part of a solution. Selling a house to someone who is unable to make the payments is not helping anyone and is not part of the American Dream.

In March of 2009, the Federal Reserve's TALF attempts to correct the problems of the day by encouraging more of the same. The highlights of the plan to “return the credit markets back to normal” include:

- The Fed offering cheap credit to large players in the private sector including hedge funds and private equity firms.

- Businesses are encouraged to loan money to small businesses and consumers to purchase more cars, trucks, heavy equipment, houses, commercial real estate, or anything using a credit card.

- Businesses that make loans can securitize them (sound familiar?) and sell them to the hedge funds and private equity firms who buy them using leverage as high as 12-to-1 (sound familiar?). The capital to leverage is provided by our government.

- Hedge funds and private equity firms will not have to post any collateral for their Fed loans, making it even easier to overextend themselves with credit.

- With the government providing a backstop, investors can, according to the Wall Street Journal (03/04/09), "walk away from a deal if they are unable to repay the Fed loan, losing only their initial investment." TARP (a.k.a. the taxpayers) will absorb the initial losses.

The Fed is no longer the lender of last resort, but has become the only lender. For those not keeping tabs at home, the Fed has doubled its balance sheet assets to an eye-popping $1.92 trillion in the past year via the creation of numerous emergency and “temporary” credit programs. Under TALF, the Fed is becoming a giant prime broker for hedge funds and private equity firms. Many of the real world prime brokers effectively ran themselves out of business with securitized loans and use of high leverage (e.g. Bear Stearns and Merrill Lynch). The Fed hopes hedge funds and private equity firms can be enticed to buy more asset-backed securities with favorable loan and repayment terms.

Just as a government backing of mortgages distorted the housing markets, resulting in overbuilding and "homeowners" who should have been renters, the TALF program will distort the free market by effectively subsidizing specific types of loans related to a limited number of industries. There is a reason the "shadow banking system" has dried up – supply and demand. Given the state of the economy and consumers' impaired balance sheets, demand for loans has naturally decreased while the risk of making the loans has increased. Rather than accept the natural consequences of poor decisions, the government is hoping to get the whole cycle started again with TALF as a primary driver.

The supply of asset-backed securities (ABS) is already overwhelming a market with few interested buyers. Increasing the supply of securitized loans, which is what TALF will do, is not going to help stabilize prices in a market that is having trouble finding a bid. The use of leverage basically creates additional buying power and helps distort asset prices. Leveraged buying power has contributed to distorted prices in many markets including housing, stocks, commodities, and the ABS market. The recent crash in asset prices shows us what happens when the artificial demand of excessive leverage is removed from the system. TALF hopes to create more artificial demand via leverage in the ABS market.

The Wall Street Journal (03/04/09) confirms Einstein's definition of insanity:

"The government, in essence, is trying to save the economy by turning to the very financial engineering that spun out of control during the credit boom.”

Government backing of programs, subsidies, and guarantees to limit losses, lead to distortions in the way capital is allocated in our economy. Evidence of this is already surfacing. In a Washington Post article, Stephen Schwartzman, head of the Blackstone Group, said his firm has decided to look into buying up the assets offered in TALF, though the firm has never bought the securities before. The government's program will pull capital away from more productive free market projects as favorable terms change the behavior of market participants. Look no further than the glut of unsold homes to see the effects of inefficient allocation of capital due to government "incentives".

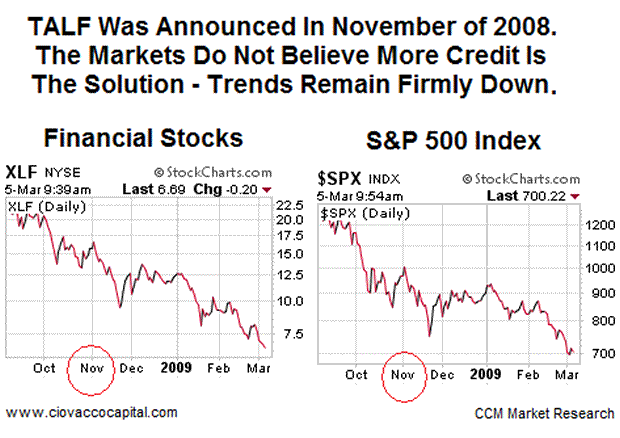

The TALF program and basic concepts were originally announced in November of 2008. Due to the complexities of the program, the first TALF loans to hedge funds and private equity firms will be made available on March 17, 2009. The stock market has not been encouraged by the basic concept of TALF. We will have to see how assets prices react once the program is up and running. The early returns reinforce the need for a disciplined risk management and stop loss discipline. The S&P 500 recently broke through long–term support , an event that should not be taken lightly by investors. The longer the S&P 500 stays below 741, the less likely it will be TALF is the rabbit the markets are hoping policymakers can pull out of their bailout hat.

Rather than letting nature take its course and see consumers begin to pay down excessive levels of debt, the TALF program encourages the accumulation of more debt. Recessions purge bad debt from the system and punish poor decision makers and managers. The United States needs to check itself into credit rehab rather than go on another credit bender that will only create more bubbles.

By Chris Ciovacco

Ciovacco Capital Management

Copyright (C) 2009 Ciovacco Capital Management, LLC All Rights Reserved.

Chris Ciovacco is the Chief Investment Officer for Ciovacco Capital Management, LLC. More on the web at www.ciovaccocapital.com

Ciovacco Capital Management, LLC is an independent money management firm based in Atlanta, Georgia. As a registered investment advisor, CCM helps individual investors, large & small; achieve improved investment results via independent research and globally diversified investment portfolios. Since we are a fee-based firm, our only objective is to help you protect and grow your assets. Our long-term, theme-oriented, buy-and-hold approach allows for portfolio rebalancing from time to time to adjust to new opportunities or changing market conditions. When looking at money managers in Atlanta, take a hard look at CCM.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors and tax advisors before making any investment decisions. Opinions expressed in these reports may change without prior notice. This memorandum is based on information available to the public. No representation is made that it is accurate or complete. This memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned. The investments discussed or recommended in this report may be unsuitable for investors depending on their specific investment objectives and financial position. Past performance is not necessarily a guide to future performance. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors. All prices and yields contained in this report are subject to change without notice. This information is based on hypothetical assumptions and is intended for illustrative purposes only. THERE ARE NO WARRANTIES, EXPRESSED OR IMPLIED, AS TO ACCURACY, COMPLETENESS, OR RESULTS OBTAINED FROM ANY INFORMATION CONTAINED IN THIS ARTICLE. PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

Chris Ciovacco Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.