Rebalanced UK Economy and Economic Growth To Fix Britain's Finances

Economics / UK Economy Apr 20, 2010 - 03:30 AM GMTBy: John_Mauldin

Long time readers know that I am a huge fan of Martin Wolf, economist and columnist for the Financial Times. His writing is the reason to get the Pink Lady (as the Financial Times is known) as far as I am concerned.

Long time readers know that I am a huge fan of Martin Wolf, economist and columnist for the Financial Times. His writing is the reason to get the Pink Lady (as the Financial Times is known) as far as I am concerned.

This week's Outside the Box has two columns back to back from last week from Wolf, talking about the problems in Britain which look like the same problem all over the developed world. Wolf argues (rather cogently) that the answer is to increase exports and for a further weakening of the pound. Quoting:

"Weak sterling, far from being the problem, is a big part of the solution. But it will not be enough. Attention must also be paid to nurturing a more dynamic manufacturing sector. With the decline in energy production under way, this is now surely inescapable."

Can I envision the pound at parity with the dollar? Yes, I can. But look at what that implies. It makes it tougher on US exporters just when we need a strong export base. Can every country devalue its currency (or allow it to fall?) as a way to become prosperous? And against whom? Will Europe sit by? What will that do to the US earnings of multi-national corporations? Will Senator Schumer accuse Britain of currency manipulation and want a 25% tariff?

I have made the point many times that not every nation can export their way to prosperity. Someone has to buy! While Wolf has the right prescription for Britain, it is the same prescription that every nation wants to pursue. But we can't all do it at once. Read these columns in that light.

Have a great week.

John Mauldin, Editor

Outside the Box

UK economy must perform a rebalancing act

How ill is the UK economy? What are the challenges for economic policy? These questions seem to me to be far more urgent than before any general election since 1979, when Margaret Thatcher came to power.

The one point on which everybody agrees is over the depth of the fiscal hole: the government is borrowing a pound for every four it spends. But nobody wants to discuss what might need to be done. This is not surprising: today's fiscal deficits exceed those of any previous period in peacetime. Yet even if one accepts that these deficits must be tackled, huge questions remain over the timing and content of such action.

In the UK at least, the fiscal deficits are mirror images of private sector surpluses. Moreover, the direction of causality is from the latter to the former. The necessary conditions for a return to fiscal (and economic) health are a recovery in private spending, a huge increase in net exports or, ideally, both. The big question is whether the essential recovery in private spending and net exports will occur before, or after, it becomes difficult for the government to borrow on reasonable terms. If it comes before, a smooth fiscal exit is feasible. If it comes after, a crisis would intervene. I am optimistic on this, but am not blind to the risks.

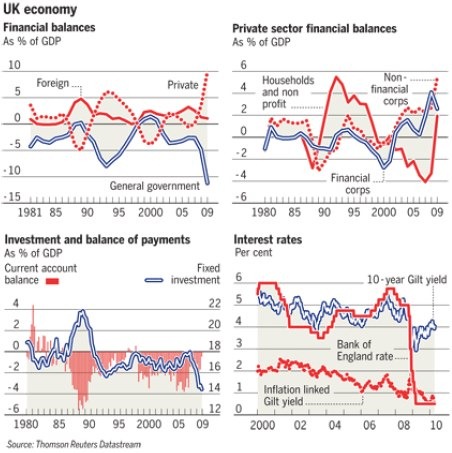

Between 2007 and 2009, net lending - the gap between income and expenditure - of the UK private sector jumped by a massive 9.8 per cent of gross domestic product (see chart). Since the net inflow of capital from abroad fell little, the principal offset to this shift towards frugality was the government's towards profligacy. Net government borrowing jumped by 8.6 per cent of GDP between 2007 and last year.

Now look at the private sector components. Between 2007 and 2009, the shift of households towards surplus was 6 per cent of GDP. The shift of non-financial corporations was 3.2 per cent. The impact of the crisis on private spending has overwhelmed the monetary policy offsets from the Bank of England, at least in the short term.

Now consider the policy challenge: it is not to cut the fiscal deficit, regardless; it is to cut the fiscal deficit, while sustaining recovery and growth. It is stabilisation with growth, not stabilisation at the expense of growth. Economic misery is not desirable but detestable.

If the actual fiscal deficit is to be cut by, let us say, 10 per cent of GDP, then the sum of the financial surpluses of the domestic private and foreign sectors must fall by the same amount. If this is to occur with growth, there needs to be a strong surge in spending in these sectors. Andrew Smithers of London-based Smithers & Co offers a compelling analysis of what this might mean.* In particular, he points out that this is impossible without a massive improvement in the external balance.

Alas, the UK's net household savings are exceptionally low. This is consistent with the sector's huge shift into deficit between 1992 and 2007. Household savings need to rise, not fall. While an offsetting jump in residential investment would be most desirable, it is unlikely to occur.

As Mr Smithers notes, UK fixed investment has been extremely low for years. It has, most recently, been running at a mere 14 per cent of GDP (see chart). A big rise would be desirable, to generate current demand and future growth. It would be optimistic, however, to expect its share of GDP to rise even by as much as 5 percentage points. Moreover, it is unclear that this would drive the non-financial corporate sector all the way to balance, because higher profits (and so retained earnings) would probably be a condition for the higher investment. The overall balance, then, could remain positive.

The conclusion is that the foreign balance - and so net exports - need to shift by at least 5 per cent of GDP. Unfortunately, a disturbing new paper by Ken Coutts and Robert Rowthorn, for the think-tank, Civitas, argues that trends in the UK's external position are in the opposite direction. Weak sterling, far from being the problem, is a big part of the solution. But it will not be enough. Attention must also be paid to nurturing a more dynamic manufacturing sector. With the decline in energy production under way, this is now surely inescapable.

The Panglossian view is that if the fiscal deficit were reduced, domestic private spending and the external balance would adjust automatically. But, with real interest rates on index-linked gilts at just 0.6 per cent, short-term interest rates at 0.5 per cent, yields on conventional 10-year gilts at about 4 per cent and weak growth of credit and broad money, this is a fairy story. The situation is entirely different from that in 1981, when the Tories tightened fiscal policy successfully in a recession.

Yet even if fiscal tightening is far more likely to follow recovery than cause it, it does not follow that current fiscal deficits will be easy to finance for long enough to permit the needed economic adjustments to occur. While the UK's private sector surpluses are nearly big enough to finance the fiscal deficit, this may well not be how it decides to invest its money, at least at present prices. It might buy foreign assets instead.

The question is whether, or when, a further fall in sterling could turn into a rout. Such a loss of confidence might then undermine inflationary expectations and raise long-term interest rates. The result could be both a renewed recession and an explosive path for public debt. At the same time, a further fall in sterling seems desirable, if not inevitable, not least given the poor recent performance of productivity (the flip side of the welcome employment performance). Weak demand in the eurozone, the UK's biggest trading partner, only makes such a fall even more necessary.

The decisive fact about the UK economy, then, is that it has to manage a huge, multi-year economic rebalancing. Policymakers must bear four points in mind: first, they must promote the essential strengthening of investment and net exports; second, they must realise that this big economic adjustment is a necessary condition for a durable fiscal improvement; third, they must also prevent the fiscal deficit from crowding out the needed rebalancing; and, finally, they cannot assume that today's huge fiscal deficits can be comfortably financed indefinitely, should the rebalancing of the economy itself fail to occur.

This is going to be a very tricky policy performance. How to carry it off will be my subject this Friday.

* UK: Either a Large Trade Surplus or Grim Prospects for Profits and the Fiscal Deficit, March 2010, restricted

Growth is the fix for British finances

What is the right economic medicine for the UK? In my column on Wednesday, I argued that rebalancing the economy towards higher investment and higher net exports is a big part of the answer.

Mine is a somewhat different perspective from that offered by Luke Johnson in the Financial Times this week. Labour, he argues, is "an entirely fraudulent organisation that pretends to believe in business, then buries it in bureaucracy and tax. Five more years of Gordon Brown would leave Britain an economic wasteland." I do understand his objection to the overregulation and the over-complication of the tax system. A great deal has been lost since Nigel Lawson simplified taxation in the 1980s.

Mr Johnson makes two further assertions. He argues that "the state's percentage of gross domestic product in Britain has risen from about 38 per cent in 1997 to perhaps 52 per cent today. Funding this vast amount of public largesse means the UK borrows 25 per cent of all its state spending. Clearly the country is living beyond its means." These points need to be put into context.

First, the explanation for the sudden explosions in the share of public spending in GDP and the fiscal deficit is not that spending is out of control. It is, instead, that nominal GDP and tax revenue have fallen far below what was expected just two years ago. According to the 2010 Budget, public spending will be just 2.2 per cent higher this financial year than was expected two years earlier, despite the recession. But nominal GDP will be 9.3 per cent lower and tax revenues 18.1 per cent lower.

The second qualification is that the country is not living beyond its means, to any significant degree; the government is. Not only is the current account deficit modest, but the UK's net liabilities were only 13 per cent of GDP at the end of 2009. On a consolidated basis, the chief creditor of the UK public sector is the UK private sector, not foreigners. Similarly, on a flow of funds basis, the dominant offset to the fiscal deficit is the UK's private surplus.

The implication is that the single most effective way to bring the public finances back under control is greater demand and higher GDP. This needs higher investment and net exports and more dynamic supply. Measures that seek to close the fiscal deficit, but destroy demand in doing so, will not help: fiscal austerity is just not enough.

So what might be done?

First, it would be extremely helpful to reform the taxation of companies, to promote investment. In an interesting discussion of this issue, Andrew Smithers of Smithers & Co argues that a radical reform of corporation tax, to end interest deductibility, offset by a lower rate of tax, would reduce indebtedness and lower the pre-tax return needed to achieve a given post-tax return on equity. The result should be a bigger capital stock. Such a measure could be combined with higher deductibility of investment, which would be helpful to manufacturing.

A second issue is the promotion of net exports. The biggest part of the necessary change in incentives has come from the sharp decline in sterling. The trade-weighted real exchange rate, on the JPMorgan measure, is 10 per cent below the average of the "oil years" between 1980 and 2007. Given the weakness in the production of tradeable goods and the damage to financial services, it may have to fall still further.

Third, more attention needs to be paid to the long-term health of manufacturing, which still generates half of all export earnings. A recent report from Policy Exchange, by my former colleague, John Willman, notes that the UK is still the world's sixth-largest manufacturer, with output similar in size to that of Italy and a little bigger than France. It argues, persuasively, that attempts to recreate a national manufacturing sector are senseless. Similarly, policies aimed at picking winners will surely fail. But some action is possible. Particularly important will be stronger links between industry and universities.

Finally, we have the question of how to tighten the fiscal position. I would have no problem with Conservative opposition to higher employers' national insurance contributions, if they had not suggested that greater efficiency alone might replace it. With a need to tighten fiscal policy by at least £100bn (7 per cent of GDP), the UK must implement all the efficiency savings it can imagine, plus real-terms cuts to public sector pay bills and services, plus tax increases. The parties are determined not to discuss these realities. If politicians treat voters like children, the voters will throw tantrums when cuts come.

The Tories are saying some of the right things, notably over the need for a new economic model, based on higher investment and savings. But none of this is fleshed out in detail. Voters should evaluate the economic programmes of the parties against the following criteria: do they promise a credible fiscal tightening, while supporting rebalancing of the economy and higher longer-term growth of supply? That is the huge challenge ahead. None of the parties has a convincing plan.

John Mauldin

Editor, Outside the Box

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.