The Great Commodities Con, Dangers of Investing in ETF's, Exchange Traded Funds

Stock-Markets / Exchange Traded Funds May 18, 2010 - 02:48 PM GMTBy: John_Mauldin

A quick introduction for this week's Outside the Box. This is from my London Partner Niels Jensen, talking about the problems with long only commodity funds. This is something I discuss frequently but have not written about in some time. Quite simply, many of the commodity ETFs do not deliver what they promise and in fact many of the inverse funds can lose you money even when you make the right macro call.

A quick introduction for this week's Outside the Box. This is from my London Partner Niels Jensen, talking about the problems with long only commodity funds. This is something I discuss frequently but have not written about in some time. Quite simply, many of the commodity ETFs do not deliver what they promise and in fact many of the inverse funds can lose you money even when you make the right macro call.

Niels gives us a very good explanation of why this is so. So for those of you who have "diversified" into commodity ETFs (not actively managed funds!) or are thinking about it you might really want to read this.

I have worked closely with Niels for years and have found him to be one of the more savvy observers of the markets I know. You can see more of his work at www.arpllp.com and contact them at info@arpllp.com if you want to follow up on their ideas.

Your running our the door for dinner in NYC analyst,

John Mauldin, Editor Outside the Box

The Commodities Con

The Absolute Return Letter - May 2010

"There is a very easy way to return from a casino with a small fortune: go there with a large one." ~ Jack Yelton

I promise you - no mention of Greece in this month's letter. Over the past few months, I have been eating it, drinking it and sleeping it to the point where I need a break.

Instead I will focus on another issue close to my heart - commodities. In last month's Absolute Return Letter I raised a yellow flag concerning the short term outlook for commodities[1]. Quite a few readers asked me to elaborate on that, which is precisely what I am going to do. In the following, my assessment will be based on the following three observations:

- Financial demand is growing much faster than industrial demand;

- The Chinese have aggressively stockpiled over the past 12-15 months;

- Most investors do not understand the complex nature of commodity investments.

Rising demand

Let's begin with the rapidly rising demand for commodities from financial investors. Their allocation to commodities has grown dramatically in recent years - to the point where commodities have become a mainstream asset class. According to Barclays Capital, total commodity linked assets under management grew 36% last year to $257 billion, with ETP[2] programmes growing even faster (+48% to $92 billion).

Chart 1: Worldwide Commodity Assets under Management

| Commodity AuM | 31/12/2009 |

| ETP Programmes | $92bn |

| Index Linked Programmes | $111bn |

| Other Programmes | $54bn |

| Total | $257bn |

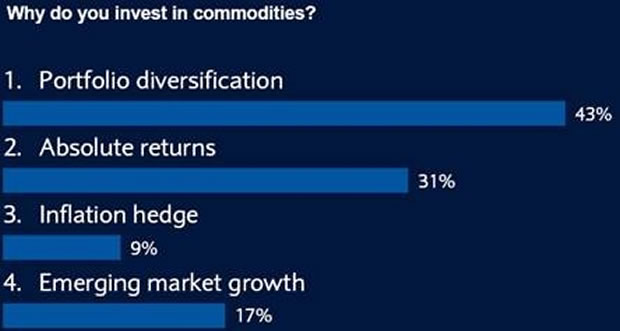

Investors typically allocate to commodities in order to:

- further their portfolio diversification;

- generate absolute (presumably uncorrelated) returns; or

- benefit from the growth of emerging economies - first and foremost China.

Chart 2: Why Invest in Commodities?

Source: Barclays Capital

Again, according to Barclay's research, investors have an affinity for ETPs. Only a few years ago, commodity linked ETPs were a rare phenomenon; however, in recent years it has grown to become the product of choice for many commodity investors (see chart 3). Not a smart choice. Here is why.

Chart 3: The Choice of Product

Source: Barclays Capital

Beware if you are the market

Many commodity markets are surprisingly small and index linked products such as ETPs have become a larger and larger proportion of the market. As a result, commodities have increasingly become financial rather than real assets - a fact which is still lost by many investors (as I learned many moons ago, if you are the market, you are in trouble!). Chart 4 below illustrates the ratio between physical and financial futures contracts in the crude oil markets. Over the past 15 years, financial futures have grown from 2 times the size of physical markets to almost 12 times the size.

Chart 4: Financial vs. Physical Oil Markets

Source: Masters Capital Management

If you question the effect financial investors have had on oil prices, I suggest you take a look at chart 5 below which depicts the WTI oil price against total assets under management in passive commodity linked strategies. Although I am very much aware of the dangers of confusing correlation with causation, it is hard not to conclude that financial demand has at least played some role in the run-up of oil prices in recent years.

Chart 5: Passive Commodity Index Investments (USD billion)

Source: Masters Capital Management

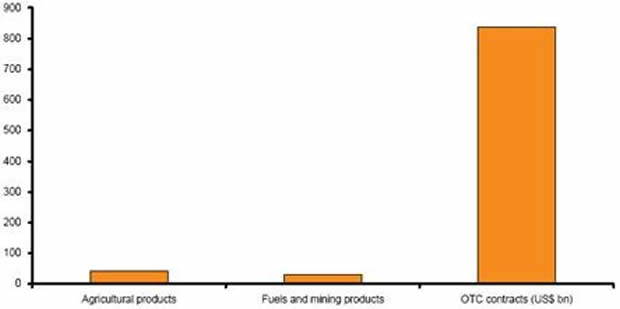

And it is not only energy related products which have been in strong demand from the financial community. The commodities team at Royal Bank of Scotland have found that export driven demand for both agricultural, mining and energy related commodities is dwarfed by the financial demand for those same commodities (see chart 6).

Chart 6: Percentage change of volume of exports vs. notional value of OTC commodity linked derivatives outstanding, 1998-2008

Source: Royal Bank of Scotland

China's master plan

Furthermore, because commodity markets are tiny compared to the size of financial markets, prices are easily distorted. In this respect, it is worth paying particular attention to the behaviour of the largest nation on earth - China. The bull market in commodities is intimately linked to the growth story of China; hence commodity investors are well advised to listen to the signs of policy change emanating from the political leadership in China. And there can be no doubt that there is, at present, a desire to cool down things a notch or two. Only in the last few days, China has (for the third time this year) increased the reserve requirement ratio for Chinese banks. Deutsche Bank now expects growth in Chinese infrastructure spending to be slashed from 120% last year (!) to just 5-10% this year. Industrial metals such as lead, zinc, copper and nickel are particularly sensitive to such investments.

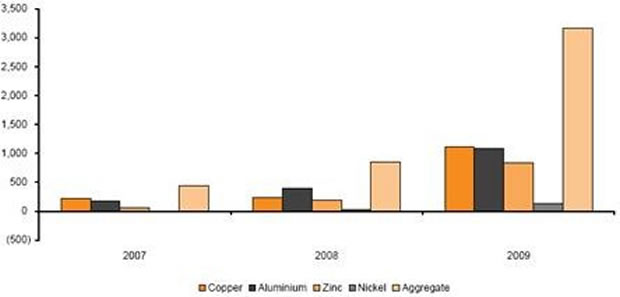

It is broadly accepted that China stockpiled commodities en masse last year, although reliable data is notoriously difficult to get your hands on. One good source is Royal Bank of Scotland who has thoroughly researched the commodities space. They have found a ferocious appetite for industrial metals from Chinese buyers throughout 2009 (see chart 7).

Chart 7: The Chinese stockpiling of industrial metals (thousand tons)

Source: Royal Bank of Scotland

So what is China up to? If spending programmes are to be slashed this year, growing infrastructure spending hardly seems the most likely explanation behind the buying spree. Maybe the Chinese just happen to be bullish on commodities longer term and want to secure supplies. Or perhaps China is driven by the seemingly imprudent behaviour by Washington. After all, China sits on the largest foreign currency reserves in the world - about $2.4 trillion, $878 billion of which are held in US treasuries[3]. Perhaps China suspects that Washington may be only too happy to engineer a covert default on its debt by allowing the continued print of money? Chinese Head of State Wen Jiabao actually alluded to this last spring when he stated:

"We have lent a huge amount of money to the United States, so of course we are concerned about the safety of our assets."[4]

By stock piling commodities on a large scale, Beijing is effectively placing their excess dollars in hard assets rather than buying the more dubious paper assets, also known as US treasuries. And, as China continues to outgrow the rest of the world, they would have had to buy those commodities anyway, so the strategy makes plenty of sense.

Or could the stockpiling be a reaction to the increasingly hostile American stance on China, as far as the bilateral trade situation is concerned? By stockpiling commodities China has effectively turned its large trade surplus into a deficit, making it much harder for Washington to argue that Beijing should allow its currency to appreciate in value. Whether it is one or the other explanation, it looks like Beijing has very much outsmarted Washington with these manoeuvres.

The obvious challenge facing commodity investors is that with Beijing attempting to engineer a slowdown of the Chinese economy and with much of its commodity buying already behind it, is it really a good idea to pile in at current levels? As already alluded to earlier in this letter, there is no denying that the long term outlook for commodities continues to be bullish; however, things do look a little bit too perky for my taste in the short term.

Ever heard of contango?

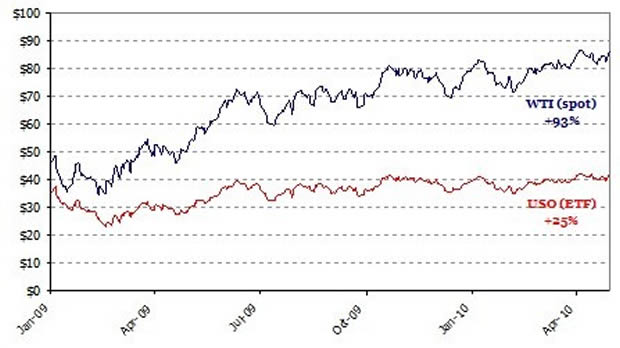

The third and final reason for advocating a more cautious stance on commodities - at least in the near term - has to do with the complexity of commodity linked products, little of which is understood by the majority of investors. Take a look at chart 8 below which illustrates the spot price on oil as measured by West Texas Intermediate (WTI) against one of the largest oil ETFs called United States Oil Fund (ticker symbol: USO).

The ETF has underperformed the benchmark WTI spot price - against which it is pegged - by a whopping 68% since January 2009! Investors have been conned into believing that if they invest in USO, they effectively buy the WTI oil price. In reality they buy an ETF which is so far off the mark that it is almost criminal. And USO is by no means the only ETF which has consistently underperformed, although it is probably one of the worst of its kind. Nobody cared to explain to hopeful investors about a subtlety called contango. Here is what you need to know in order not to fall into the trap:

Investing in the spot market is not a viable solution for most commodity investors; hence most of us invest in commodities through futures. The market can either be in backwardation or in contango. When a market is in backwardation, the future is priced lower than the spot price. When you roll your futures position you will benefit from what is called a positive roll yield. Backwardation is often (but not always) linked to low inventories when immediate delivery comes at a premium.

Chart 8: WTI Oil Price versus United States Oil Fund (Jan 09 - Apr 10)

Source: Bloomberg

On the other hand, when the future is priced higher than the spot price, the market is said to be in contango and the roll yield is negative. Herein lies the problem[5]. Most commodities are in contango more often than not, effectively costing investors the spread between the nearby future and the more distant future every time the position is rolled. Oil has been in contango pretty much constantly since 2005 (with a brief interruption in late 2007 - early 2008) with the contango being exceptionally steep in 2009, most likely a function of the global recession where oil was not in short supply.

Not only do you suffer from a negative roll yield every time the market is in contango but, as a passive investor, you are a sitting duck for more active investors keen to take you out. It is simply too easy for professional traders to jump in front of these large passively managed funds every time they need to roll their positions. Many ETPs have clearly defined - and publicly stated - trading patterns which are only too easy to take advantage of.

Obviously, the theoretical solution to the problem is to invest in the spot market rather than the futures market; however, this is not easily accomplished in most commodity markets. If you buy spot, you need to be prepared to store the physical commodity. This is relatively easy when it comes to non-perishable commodities such as metals but industrial metals would require storage space beyond what most investors have access to. Therefore, typically, only precious metals are traded spot, whereas most other commodities are bought in the futures markets.

Many ETF sponsors are aware of the problem and have taken various initiatives to address it, for example by making trading patterns more opaque by spreading out the rollover trades. However, based on the performance of many commodity ETFs, such initiatives have only been partly successful (please note: this is not a problem for ETFs operating in spot markets such as stock index linked ETFs).

Gold is not without problems

I have not yet mentioned gold. Most gold ETFs have performed pretty much in line with the underlying price of gold, probably because gold ETF sponsors use the spot market rather than the futures market; hence they are not subject to the negative roll yield. However, this raises another set of questions the most important of which is: How certain can you be that your money has actually been placed in physical gold and that this gold is stored in a vault somewhere to support your investment at all times?

Most financial investors buy gold either as an inflation hedge or a disaster hedge. Over time, gold has not been the stellar inflation hedge that most investors seem to think it is, but it has worked quite well as a disaster hedge. In Q4 of 2008, it was one of very few asset classes posting gains. By no stretch of the imagination am I a gold bug, but I can see the rationale for owning gold given the path we are on at present with Greece (sorry, promised not to mention that word!) potentially being the precursor for what is to come in many other countries. If that were to happen, gold would almost certainly be the best performing asset class which you can buy in size.

I just wish it were that simple because, in a world where we face unprecedented and systemic problems, the risk we face will not only be sovereign risk but counterparty risk at all levels. In that sort of environment there is no guarantee that the ETF sponsor will in fact be around to honour its obligations to you when you most need it. Some gold ETFs are based on synthetic trades (i.e. no physical gold stored); other ETFs do not issue actual guarantees that there is always physical gold to support the ETF exposure one-for-one. Therefore, if you choose to buy gold through ETFs, it is effectively like depositing money in a bank where the rate of interest is equal to the move in the price of gold. It is a financial asset; not a physical asset. If you have bought gold as a disaster hedge, you may want to think twice about getting your gold exposure this way.

Conclusion

So where does that leave us? It is my conviction that commodity prices have at least partly been driven not by fundamental demand but by demand from financial investors eager to diversify their equity risk and attracted to the seemingly high probability of generating uncorrelated returns. Little do these investors seem to understand that because they now are the market, the promised land of uncorrelated returns is little more than wishful thinking.

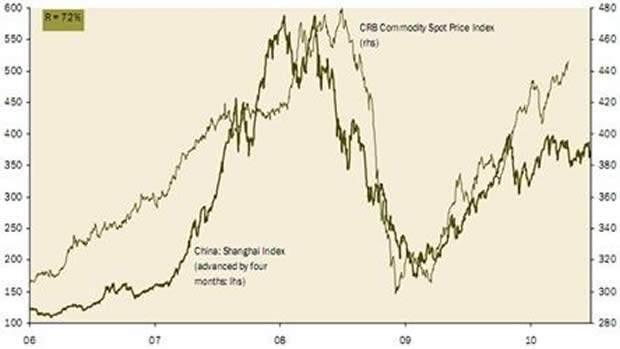

Source: Gluskin Sheff

David Rosenberg at Gluskin Sheff recently produced a fascinating chart (see chart 9), suggesting that there is indeed a strong link between Chinese stock market prices and commodity prices. The Shanghai index leads the CRB commodity index by four months with a 72% correlation (80% with oil prices). Oil, in particular, seems to have become a financial asset and will hence correlate with other financial assets. Supply and demand for oil (the commodity) has become a secondary factor in determining oil prices; supply and demand for the financial asset named oil hold the key to future performance.

Furthermore, as hordes of increasingly disenchanted investors, who thought that ETFs and other index products offered an easy solution to commodity investing, want out of these products, commodity prices could come under substantial pressure, at least temporarily. Again, let me emphasize that this view does not alter my belief that long term, many commodities are likely to do very well as emerging economies require ever rising amounts of oil, copper, nickel, wheat, etc. etc.

So what do you do if you want exposure to commodities? With the exception of precious metals, investing in commodities through the spot market is not a viable option. That leaves you with three options:

- Invest only in commodities when they are in backwardation (not recommended as it may keep you out of the market for long periods of time);

- Treat ETPs as short term trading instruments, not long-term holdings, which will eliminate much of the problem associated with contango (may be an appropriate strategy for some investors although it has its limitations); or

- Invest through active managers who can handle this highly complex problem on your behalf.

Niels C. Jensen

Footnotes:

[1] There is no denying that the long term outlook for commodities continues to be bullish, mainly driven by the strong growth in emerging market economies.

[2] ETPs (exchange traded products), ETFs (exchange traded funds), ETNs (exchange traded notes) and ETCs (exchange traded commodities) are essentially one and the same thing and the terms will be used interchangeably in this letter.

[3] http://www.ustreas.gov/tic/mfh.txt

[4] Wall Street Journal, 13th March 2009

[5] For a more detailed discussion of this problem, I suggest you read this link.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.