U.S. Debt Ceiling Deadlock, Default & the Markets

Stock-Markets / Financial Markets 2011 Jul 24, 2011 - 07:20 PM GMTBy: PhilStockWorld

EU Black Debt Crisis in Remission

EU Black Debt Crisis in Remission

On Thursday, Euro-area leaders stepped up their efforts to resolve the ongoing Greek debt crisis, announcing €159Bn ($229Bn) in new aid for Greece. They arranged for bondholders to foot part of the bill and expanded the power of the €440Bn Euro rescue fund to buy debt across stressed European nations - “after a market rout last week sparked concern the crisis was spreading. The fund can also aid troubled banks and offer credit-lines to repel speculators.” The Euroland leaders hope to construct a financial “firewall” around struggling countries like Spain and Italy, while assuaging fears that the debt crisis is spreading. French President Sarkozy compared the transformation of the bailout fund to the creation of a “European Monetary Fund.” (EU Leaders Offer $229 Billion in New Greek Aid)

Hopes for saving the Eurozone from multiple defaults by weaker EU members strengthened the Euro against the Dollar. We view the solution as another attempt to kick the can down the road. It was, however, a substantial kick and probably good for at least a few months. It whacked the Dollar, and conversely rallied the equity market. As Bruce Krasting wrote, “The Council of the European Union statement makes it pretty clear that the Euro folks are going to do everything they can (including direct intervention in the bond market) to stop the spread of contagion. I think they will succeed in maintaining market peace for a few months. But sometime this fall the issue of default by some Euro members will rise up again. It has to. I think the leaders in Europe are dreaming.” (Whoopie! We got a Greek Deal!)

U.S. Debt Ceiling Deadlock

In the United States, a fierce battle over raising the debt ceiling raged on, with both sides refusing to negotiate a settlement.

A team of six senators, three Republicans and three Democrats, the “gang of six,” put together a decade-long, $3.7 Tn deficit reduction plan. President Obama remarked to reporters before the Tuesday White House press briefing that the Senate “Gang of six” proposal was a “very significant step” towards resolving the impasse, representing a “potential for bipartisan consensus.” (President Obama praises ‘Gang of Six’ debt ceiling plan)

The proposal, however, drew considerable opposition. House members of both parties feel their side had given away too much. “We don’t have to increase the debt ceiling,” says three-term Rep. Paul Broun (R) of Georgia, who voted against the bill. “There are other ways to raise revenue without going into receivership,” he added, suggesting that the government could increase federal revenues by opening up energy reserves or selling unused federal buildings. (Trillion-dollar question in debt-ceiling talks: What can pass the House?)

Robert Borosage of Politico was also displeased: “[T]his isn’t a New Deal or a Fair Deal. It’s a Raw Deal — one that every citizen concerned about rebuilding the middle class should oppose. It would add to unemployment in the short term, increase Gilded Age inequality, leave seniors more vulnerable and shackle any possibility of rebuilding America. It puts the burden of deficit reduction on the elderly, the poor and the vulnerable; endangers jobs and growth; and lards even more tax breaks on the rich. (Senate Gang offers ‘raw deal’)

One line of reasoning from the “no tax hikes” crowd is the inaccurate premise that the very wealthy, the top 0.1%, are job creators. If they’re the “job creators,” it might be in the public interest to protect them from excessive taxation - thereby allowing these top 0.1% to spend money on creating jobs. This is incorrect. The overwhelming majority of U.S. jobs are ‘created’ by ordinary Americans when they spend their paychecks. Consumer spending drives about 70% of our GDP. When average Americans are struggling with high unemployment, which recently popped back up to 9.2%, they are reluctant to spend money on anything beyond basic necessities. The broader U6 unemployment number - which includes the underemployed and “discouraged workers” - is 16.2%.

Meanwhile, U.S. companies are not stepping up hiring due to weakness in the economy - there is no demand. As Paul Ashworth of Capital Economics wrote, “Businesses aren’t confident enough, and the longer this goes on, the harder it is to convince them that they should be.” (Dearth of Demand Seen Behind Weak Hiring)

The impasse between the President and the Republican leadership reached new lows on Friday when talks broke down and Rep. Boehner walked out of negotiations. “The White House deal for the House would have required that alongside these cuts, tax revenues would go up by $1.2 trillion, largely through a rewrite of the tax code to eliminate many deductions and loopholes. That’s substantially less in revenue than the $2 trillion in the “Gang of Six” plan. The problem is that while much of the cutting would start right away, most of the revenue increases would be put off, in part because a tax-code revision would take months, and in part to allow spineless House Republicans to say they did not agree to any specific tax revenue increases (i.e. they planned on lying to their constituents).

“Democratic lawmakers were rightly furious when they heard about these details, calling the plan wholly unbalanced. But, in the end, it was Mr. Boehner who torpedoed the talks. He said Friday evening that he and the President had come close to agreeing on $800 billion of the revenue increases (the equivalent of letting the upper-income Bush tax cuts expire as scheduled next year — not much of a heavy lift) but could not stomach another $400 billion ($40Bn a year!) which the White House wanted to raise by ending tax loopholes and deductions.

“So, on the eve of economic calamity, the Republicans killed an overly generous deal largely over a paltry $40 billion in annual deductions. Mr. Obama was willing to take considerable heat from his liberal critics over the deal, and the Republicans were not willing to do a thing to anger their Tea Party base. As Obama forcefully said, there is no evidence that House Republicans are capable of making those tough decisions. If last-ditch talks beginning Saturday fail, they will have to take responsibility if the unimaginable — a government default — happens in 10 days and the checks stop going out.” (Weekend Reading - Deal or No Deal?)

The Republicans are standing firm against raising taxes, in an era when many American corporations are already paying surprising little in taxes.

Russ Winter of Winter Watch at the Wall Street Examiner discussed the gap between what people think corporations pay in taxes, versus what they really spend. For example, Microsoft “lowers its effective tax rate a full 7% by taking foreign income to $19.2 billion from $15.4 billion, and lowering US income (and expenses) from $9.6 billion to $8.9 billion. Today MSFT is effectively a 68% foreign operation. In return it gets all the benefits of stimulus and minimizes the costs of supporting the US system...

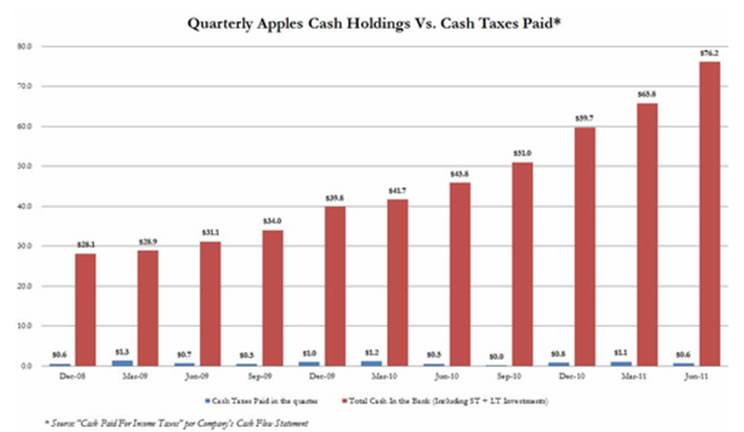

“One of the big economic winners, Apple Computer, is even worse, hardly paying a thin dime to a U.S. Gumnut tottering towards insolvency. Here is the big picture of this foreign company getting U.S. benefits going back a few years [chart by Capital IQ].

Little wonder so much largesse flows into the hands of so few. Matt Taibbi gets into some of the particulars. Bloomberg’s Jesse Drucker estimated that Google all by itself has saved $3.1 billion in taxes in the past three years by shifting its profits overseas. If the U.S. is looking for a source to close its out of control deficits I have some suggestions...

“When one hears talk of tax reform, and closing tax loopholes, prepare to duck and cover if you are an ordinary American. Taxes collected for CY 2011 for the corporation year to date were $131.5 billion, versus $167.2 billion for the same period in CY 2010, down nearly 17% YoY. Little wonder there are so many earnings beats from the corporate sector...

“Mark Kreiger writes a spot on piece regarding the high end luxury bubble that includes this gem - ‘The social crisis facing the country as a result of the most egregious plundering in modern American history will spell the end of the ‘high end’ theme. Buying into this trend now is like getting long Marie Antoinette’s unsevered head in 1792.’”

One fear regarding a U.S. default is that creditors will demand higher interest in return for issuing new debt. Considering how enormous the U.S. debt load currently is (roughly $14.5Tn), higher interest rates would add a crippling burden to an already high burden. This leads to the question of how the markets would react if the U.S. defaults on its debt obligations.

Default & the Markets

Analyzing market action last week and next, Lee Adler of the Wall Street Examiner submits,

“Last week I worried about the possibility of a short squeeze in Treasuries if there’s no deal on the debt ceiling, because of the temporary lack of supply during the period where the Treasury is unable to issue new debt. I dismissed that outcome as unlikely.

Now, having seen the markets rally in the face of all this nonsense, I’ll rate it as a tossup. For sure, the Treasury will make the interest payments and will redeem maturing bonds, and that will reassure investors, regardless of any action by the hated ratings agencies. I would not want to be short the Treasury market until it becomes a little clearer how this drama will unfold. It just doesn’t look like a good bet to me right now. In fact, in spite of the consensus bearishness on Treasuries, the charts suggest that my concern of a continuation of the rally may not be crazy at all. Sorry, Russ [Winter].

“Going into the end of next week, bears will face a huge test. The Treasury has a lot of paper to sell. Most of the new paper will settle on Monday,

August 1. On Thursday, July 28, a sizable paydown will put cash back in investors’ pockets. Continuing fears over the European situation may drive ongoing capital flight out of European paper and European banks into shark infested U.S. pool. So what will happen to all that cash?

“If Monday’s settlement is accompanied by no noticeable disruption to stocks or bonds, then that could be a sign that a perversely bullish scenario could be playing out. If bonds crack but stocks hold up, then the “stocks as safe haven” thesis would be gaining currency. That could be grounds for an upside breakout and an extended run in U.S. equities. If both stocks and bonds sell off, that could be great news for precious metals.

“Again, I don’t want to give the impression that I know what might happen... I’ve given you my contrarian concern on what might happen if there is no deal. It goes against the grain of the universal consensus that a failure to increase the debt ceiling would lead to catastrophe. It may, but I’ve put an opposing view out there for you to consider. It could be bullish because of the lack of new supply.

“What if there is a deal? There could be a deal to increase the debt ceiling with the issue of the debt being deferred. I’m pretty sure that would be bearish because supply would increase, and the ratings agencies almost certainly would downgrade. A grand bargain deal which raised the debt ceiling and set draconian targets for cutting the deficit should be bearish because the economy would slow so fast that revenues might shrink faster than outlays, thereby increasing supply, and worsening the nation’s credit outlook.

“For now, the tax data suggests that the economy has stabilized in recent weeks after a June swoon. I do believe that without POMO, the economy should weaken further, but that irrational capital inflows into the US are skewing the picture. Until that stabilizes, the US Treasury and stock markets will apparently get the benefit. I’ll just have to let the data and the markets’ behavior say when those trends might be ending... (Why Not Having Debt Ceiling Deal May Be Bullish - Are Stocks The New Safe Haven?)

Discussing the market on Friday, Russ Winter observed,

“Friday looked like one of the strangest market days yet. Going into the weekend and hours before the wheels fell off the fiscal negotiations, the markets just drifted cluelessly higher on extremely low volume and volatility. The intermediate-term volatility, the VXZ, is now within earshot of breaking to lowest number witnessed back in 2007. The same is true of the 2-year T-Note yield. This goes beyond cognitive dissonance. There is no fear, no worry in this market. It’s completely brain dead and comatose. It’s ironic given the end-of-the-line ungovernable situation we are witnessing. I have compared it to the last days of the Soviet Union - if that system had financial trading markets. The best comment I’ve spotted on the causa proxima of all this was made in the public feedback section of another site. Someone who goes by the name ‘sbernard’ used the term ‘hubris obliviana.’ It’s such an apt descriptor that I’m going to adopt it as a Winterism.

“Wrote sbernard: ‘The truth is that Wall St suffers from a serious disease called hubris obliviana, fueled by endless government interventions, bailouts, stimulus, and Fed money expansion. One of the ‘unexpected’ consequences of this monetary heroin in that Wall St has lost all perception of risk. They reflexively have too much unending faith in the power of government to fix all their troubles. Thus, they are setting us all up for even more risk — risk the government cannot avert because it is the (weak link)!’” (Unbrindled Faith in Hubris Obliviana)

For the latest update on the debt negotiations before this newsletter concludes, Zero Hedge predicts: “With 23 hours left until the Asian open (or, more importantly, 19 hours until FX trading resumes) and with today's round of talks now officially over after a one hour meeting in Boehner's office with congressional leaders achieving nothing, it is becoming clear that the final debt ceiling outcome will be "no change" in spending or taxing habits and a temporary hike in the debt ceiling, so that the soap opera can be repeated again every three months...and again...and again...and so forth for an ‘extended period of time’ as ‘transitory solutions' become the new grand consensus. At least we now know the phrase for complete, impotent incompetence on the Hill is: ‘Two tiered approach’ which is how Nancy Pelosi called the last minute attempt at compromise." (Good News: It's Almost Over After Pelosi Says Congress Looking At "Two-Tiered" Deal)

We have several option trade ideas for the coming week, two shorts (GMCR and oil) and two longs (PLX and SONC). These plays can be revised using stock strategies rather than option strategies, for those so inclined. See the inset boxes on this page (for the full newsletter, sign up for a free trial here). Have a great week!

Phil

Philip R. Davis is a founder of Phil's Stock World (www.philstockworld.com), a stock and options trading site that teaches the art of options trading to newcomers and devises advanced strategies for expert traders. Mr. Davis is a serial entrepreneur, having founded software company Accu-Title, a real estate title insurance software solution, and is also the President of the Delphi Consulting Corp., an M&A consulting firm that helps large and small companies obtain funding and close deals. He was also the founder of Accu-Search, a property data corporation that was sold to DataTrace in 2004 and Personality Plus, a precursor to eHarmony.com. Phil was a former editor of a UMass/Amherst humor magazine and it shows in his writing -- which is filled with colorful commentary along with very specific ideas on stock option purchases (Phil rarely holds actual stocks). Visit: Phil's Stock World (www.philstockworld.com)

© 2011 Copyright PhilStockWorld - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.